Some investment opportunities generate significant upside for investors in a short window of time. Others, however, require patience. One company that I think fits in the latter category is a firm called Herc Holdings (NYSE:HRI). Operationally speaking, the company services customers by renting out equipment such as earth moving devices, material handling equipment, aerial equipment, and even trucks and trailers. The last article that I published about the firm came out in September of 2023. In that article, I reiterated my ‘buy’ rating for the stock. This was based not only on continued revenue and cash flow growth, but also based on how shares were priced. At the time, the firm was trading at price to cash flow multiples well below 5.

With figures like that, you might expect a quick upside. But that has not come to pass. While shares are up 7.2% since then, that is only a small move higher compared to the 18.1% increase seen by the S&P 500 over the same window of time. To be clear, not everything involving the company is going great. But enough is that I think investors would be wise to be bullish. Because of this and in spite of the market’s insistence that shares don’t deserve to be materially higher than where they have been, I’ve decided to keep the company rated a ‘buy’ for now.

Shares look dirt cheap

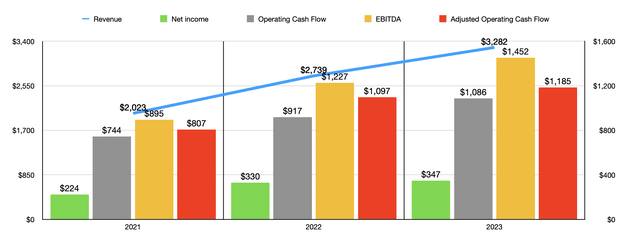

Since I last wrote about Herc Holdings in early September of last year, there have been two additional quarters worth of data that management has provided investors with. This would be the final quarter of 2023 and the first quarter of 2024. It might be best, then, to begin with how the company ended the 2023 fiscal year. During that time, revenue for the enterprise came in at $3.28 billion. That represents an increase of 19.8% over the $2.74 billion generated in 2022. Some of this move higher is most certainly deceptive. I don’t mean that in the legal sense, but rather in the sense it is not recurring.

Author – SEC EDGAR Data

You see, during 2023, equipment rental revenue accounted for $2.87 billion of the company’s overall sales. That’s an impressive 12.5% higher than the 2.55 billion dollars reported for 2022. Management attributed this to price and growth of 6.9% and to higher volume of equipment on rent in the amount of 14.8%. There were other areas in which the company saw expansion as well. Service and other revenue, for instance, inched up from $27 million to $28 million. In addition to this, the sale of new equipment, parts, and supplies grew from $36 million to $38 million. However, the company benefited tremendously from a surge in the sale of rental equipment. This figure skyrocketed from $125 million to $346 million. This was done as supply chain disruptions eased, with such easing making it easier for firms that would like to acquire equipment to do so. This, in turn, would make renting equipment less desirable. And in an effort to right size its operations, management decided that 2023 was the moment to make such a move.

On the bottom line, things were quite positive. Net income went from $330 million to $347 million. Other profitability metrics improved as well. Operating cash flow jumped from $916.7 million to $1.09 billion. If we adjust for changes in working capital, we get an increase from just under $1.10 billion to $1.19 billion. And lastly, EBITDA for the company expanded from $1.23 billion to $1.45 billion.

Author – SEC EDGAR Data

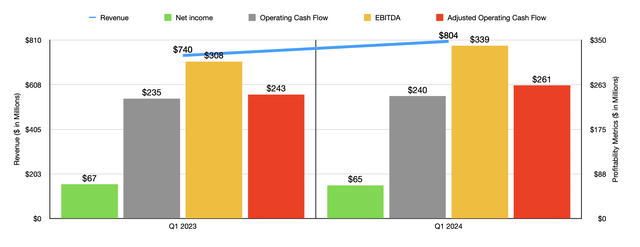

Despite concerns about the economy more broadly, Herc Holdings has continued its growth this year. In the first quarter of 2024, revenue came in at $804 million. That happens to be 8.6% greater than the $740 million reported for the first quarter of 2023. This was actually in spite of run to equipment sales dipping from $71 million to $69 million. The big driver here was actually a 9.9% jump in equipment rental revenue from $654 million to $719 million. Management attributed this largely to an 8% increase in volume for the equipment that was being rented. Having said that, pricing growth of 5.1% also helped tremendously.

There was some weakness on the bottom line. Net income of $65 million fell short of the $67 million reported one year earlier. Higher costs across the board contributed to this. In particular, interest expense rose from $48 million to $61 million. However, the company also suffered from a doubling of its income tax from $8 million to $16 million. Other profitability metrics moved higher without exception. Operating cash flow increased from $235 million to $240 million. On an adjusted basis, the rise was from $243 million to $261 million. And lastly, EBITDA for the business grew from $308 million to $339 million.

For the current fiscal year, management expects growth to continue. The expectation is that equipment rental revenue will rise by between 7% and 10%. This should bring EBITDA up to between $1.55 billion and $1.60 billion. No estimates were provided for other profitability metrics. But if we assume that they will increase at the same rate that EBITDA is expected to, then net income should come in at about $376 million, while adjusted operating cash flow should be just shy of $1.29 billion.

Author – SEC EDGAR Data

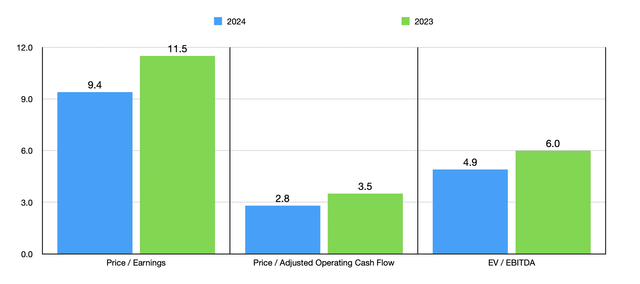

Taking this data, I then valued the company as shown in the chart above. Relative to earnings, shares looked pretty good. But it’s actually the cash flow multiples that impressed me the most. It’s rare to see a company trade in the low- to mid-single digit range. This is especially true of a firm that is growing at a nice rate. Those who disagree with my assessment of the business will argue, rightfully so, that cash flow multiples are low because of the high amounts of spending required, not only for growth, but also for repairs and because of the high rate at which this kind of equipment depreciates. But even factoring that into the equation, it’s difficult to imagine a company this cheap. As part of my analysis, I then compared the firm to three similar enterprises as shown in the table below. On both a price to earnings basis and on an EV to EBITDA basis, two of the three ended up being cheaper than Herc Holdings. This number drops to one of the three when using the price to operating cash flow approach.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Herc Holdings | 9.4 | 2.8 | 4.9 |

| Hertz Global Holdings (HTZ) | 7.2 | 2.6 | 6.6 |

| United Rentals (URI) | 14.3 | 7.1 | 7.4 |

| H&E Equipment Services (HEES) | 10.3 | 4.7 | 4.9 |

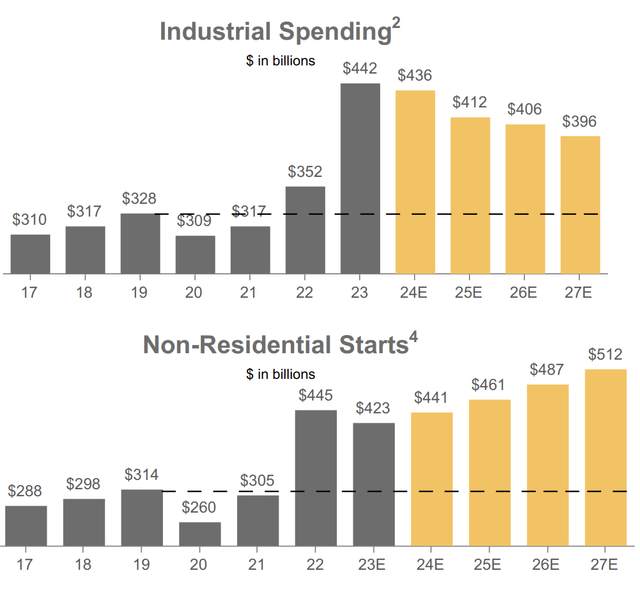

Some investors or prospective investors might be concerned about the future of industrial and other types of spending that could impact Herc Holdings moving forward. As the image below illustrates, there was a spike in industrial spending in 2023 thanks to government investments. That amounted to $442 billion. That was up from $352 billion in 2022. Current government investments are expected to last for multiple years. But as each year goes by, the amount that is expected to be spent is slated to fall. By 2027, we should see a decline to $396 billion. However, the company also has some things working in its favor. As the aforementioned image shows, non-residential property starts are expected to grow over the next several years. This year, spending on these types of properties is expected to be $441 billion. By 2027, we should see growth to $512 billion annually.

Herc Holdings

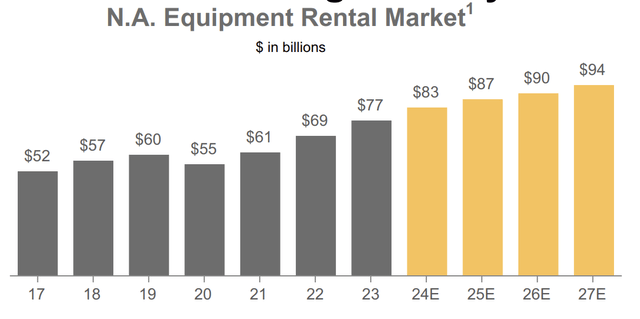

Despite these mixed expectations between industrial spending and non-residential starts, the North American equipment rental market is expected to continue expanding. This year, management expects industry expenditures to be about $83 billion. If this comes to fruition, this should translate to a 7.8% increase over the $77 billion spent last year. And by 2027, we should see spending grow to $94 billion. That represents an annualized increase of 5.1% if we use the baseline year of 2023.

Herc Holdings

Takeaway

The way I see things, the good significantly outweighs the bad for Herc Holdings and its investors. The company is a high-quality firm that has a solid track record for growth. That growth is almost certain to continue for the foreseeable future. When you combine that growth with just how cheap shares are relative to cash flows, it’s difficult to be anything other than bullish. Because of this, I have decided to keep the company rated a ‘buy’ for now.

Read the full article here