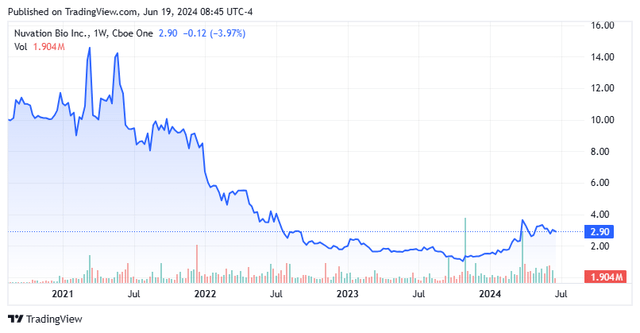

Today, we put Nuvation Bio (NYSE:NUVB) in the spotlight for the first time. The stock price of this oncology focused clinical stage biotech concern has tripled since the market’s recent lows of late October. The shares have weakened a bit recently. What’s ahead for Nuvation Bio and its shareholders for the rest of 2024? An analysis follows below.

Seeking Alpha

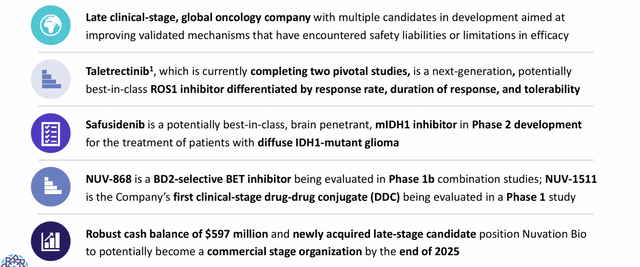

Nuvation Bio is headquartered in New York City. This company is focused on developing differentiated and novel therapeutic candidates in the oncology space. The company is now developing taletrectinib, a compound it acquired earlier this year via the all-stock purchase of AnHeart Therapeutics. This acquisition has been a primary driver of the stock’s surge in 2024.

June 2024 Company Presentation

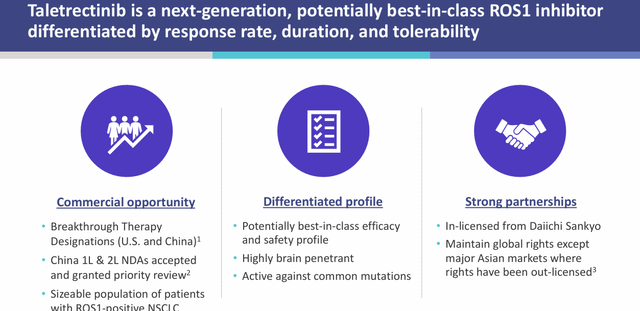

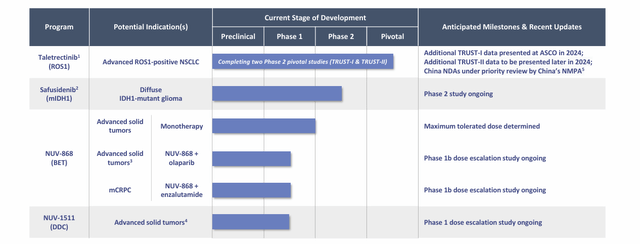

Taletrectinib is a next-generation, potentially best-in-class ROS1 inhibitor. With the buyout of AnHeart, Nuvation also picked up a pipeline asset called safusidenib, a potentially best-in-class mutant IDH1 inhibitor. This compound has shown high blood-brain barrier penetration in early studies, but still is in Phase 1 development.

Of note, development and commercial rights to taletrectinib and safusidenib had been in-licensed from Daiichi Sankyo. Some of these rights (China, Japan and Korea) have been out-licensed.

June 2024 Company Presentation

Developed in house, Nuvation also has a BD2 selective oral small molecule BET inhibitor that epigenetically regulates proteins that control tumor growth and differentiation, dubbed NUV-868. Nuvation also recently got an IND approved for NUV-1511, a drug-drug conjugate (DDC) which is a derivative of a widely used chemotherapy agent. Nuvation is targeting solid tumors with this asset that obviously is very early-stage at this point. The stock currently trades just below three bucks a share and sports an approximate market capitalization of just north of $700 million.

June 2024 Company Presentation

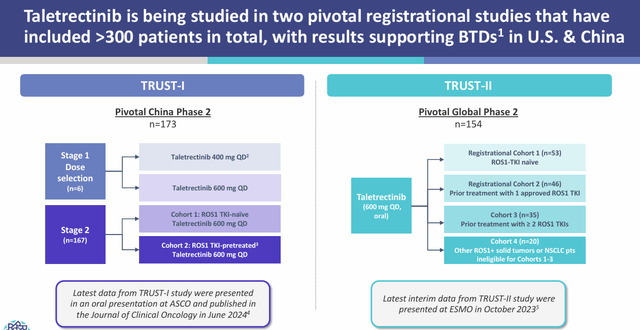

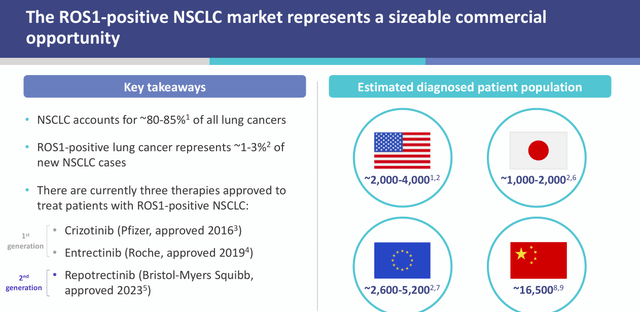

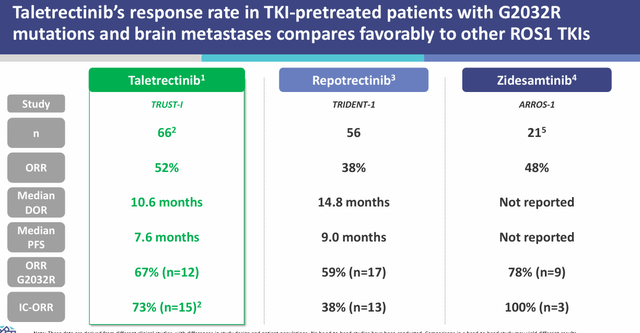

Taletrectinib is currently being evaluated for the treatment of patients with advanced ROS1-positive NSCLC in two Phase 2 single-arm pivotal studies. One of these studies, ‘TRUST-1’, is being conducted in China and the other, ‘TRUST-2’, is a global study. Taletrectinib has garnered Breakthrough Therapy status both in the U.S. and China. In the latter, Nuvation has an NDA for taletrectinib to treat locally advanced or metastatic ROS1-positive NSCLC who either have or have not previously been treated with ROS1 tyrosine kinase inhibitors (TKIs) currently under priority review.

June 2024 Company Presentation June 2024 Company Presentation

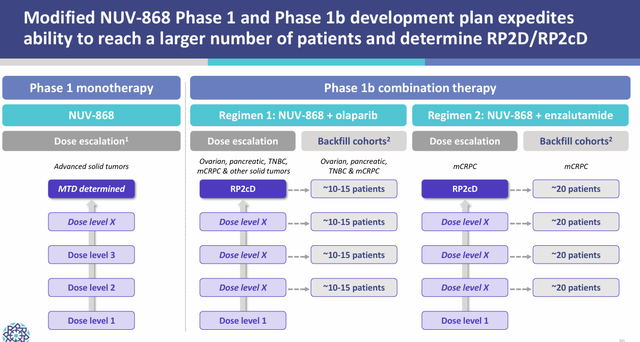

NUV-868 is in earlier stage development. It is currently being evaluated via a Phase 1b dose escalation study in combination with olaparib. This combination is targeting many forms of cancer. These include ovarian pancreatic, mCRPC, triple negative breast cancer, and other solid tumors. Olaparib is a PARP inhibitor and is marketed under the brand name LYNPARZA and is approved as a maintenance treatment of BRCA-mutated advanced ovarian cancer in adults.

June 2024 Company Presentation

Analyst Firm Commentary & Balance Sheet

The analyst community is unanimous right now in its positive view on the company. Since Nuvation Bio posted its Q1 numbers on May 13th, a half dozen analyst firms, including Jefferies, Wedbush and RBC Capital have reissued Buy/Outperform ratings on the stock. Price targets proffered range from $5 to $10 a share.

One of the best parts of Nuvation’s story is its balance sheet. It ended the first quarter with just under $600 million in cash and marketable securities on hand. This represents the majority of the stock’s current market capitalization and comes after the company posted a net loss of $14.8 million for the quarter. Nuvation is blessed with a long ‘cash runway’ to develop its candidate, meaning little chance of shareholder dilution via a capital raise on the horizon. There has been no insider activity in the stock so far in 2024. However, a beneficial owner did add more than $9.5 million of stock to their stake last September when the shares traded below $1.40 a share.

Conclusion

Seeking Alpha

Nuvation is well funded, has several ‘shots on goal‘, potential upcoming catalysts and enjoys universal support of the analyst firm community. The recent acquisition of AnHeart appears to have changed the narrative around Nuvation, a company that has destroyed substantial shareholder value since coming public in the summer of 2020.

June 2024 Company Presentation

That said, even with the recent rally, the market is valuing all the assets of Nuvation at around $120 million after adjusting for the net cash on the company’s balance sheet. Therefore, the shares seem to merit a small ‘watch item‘ holding for risk-tolerant investors.

Read the full article here