The iShares Robotics and Artificial Intelligence Multisector ETF (NYSEARCA:IRBO), as compared to the last time we covered it in 2022, is now much more skewed to the large cap issues that dominate the US market. So while there is still miscellaneous exposure, much more of it is now to stocks that have some sort of connection to the AI boom we’ve witnessed since the debut to the broader public of ChatGPT, which started it all. Valuations are naturally quite high on these AI stocks, although they have the growth in financials to back that up to a good extent. However, we have major concerns in that the valuations are extrapolating the massive current sales at high growth rates in the medium to long term. We think that there are dynamics that justify the environment as being bubbly.

Disillusionment

There is the famous Gartner (IT) hype cycle methodology that often gets referenced whenever anything apparently innovative comes to market. The idea is that after some initial hype, expectations get ahead of reality and the difficulties in moving technology forward result in disillusionment. Later, the technology may actually deliver, and then a more justified appraisal of the situation takes hold.

It’s a nice heuristic, but we think that there is an analogue in finance that helps root it further in hard logic. The idea is that whenever an innovation comes to market, it generates a lot of real uncertainty as to where things might go. A lot of this uncertainty is of course positive, where people start seeing pies in the sky, but it is uncertainty, nonetheless. In options valuation frameworks, option value is driven by uncertainty among a couple of other factors. By paying a premium for an uncertain option, there is a higher likelihood that you can exercise that option to achieve a valuable project. Meanwhile, you are also protected from failure in the technology.

When looking at the performance of stocks like Nvidia (NVDA), there is no question that the cash flows and demand are real right now for chips to power the training of AI. Growth is off the charts. But we think that it’s a major assumption to extrapolate that growth. The NVDA PE is already at 80x, and that is with current incomes already bloated by the achieved growth. We think the perceived momentousness of the AI revolution is reflecting in NVDA results in that the option premium to get into AI is worth a lot, which NVDA is benefiting from, since it could dramatically change respective businesses. It also means that if the options aren’t exercised, the demand is simply a front-loaded component that is non-recurring. We think this is possible and affects many of the other stocks in IRBO as well.

With LLMs in particular, there is so much activity in trying to fine tune the LLMs for specific use cases, for example on industrial manuals and other aspects of industrial technology. Virtually every industry needs to be on top of the matter of AI, in case it becomes a major factor going forward. Service industries, marketing and sales functions in general, entertainment and art.

Disillusionment would mean that a host of industries realise that AI isn’t that useful. There are many ways this could happen, but mainly ChatGPT is trained such that, yes, it can write or speak grammatically well, but the incremental innovation from previous architectures is that major manpower has been involved in labeling and training its responses to prompts on believability. In other words, it’s trained to be convincing, not correct. Being correct is often of vital importance, and hallucinations are not acceptable in many industries.

In the end, AI, or more correctly machine learning is fundamentally regurgitative, or at best combinative – it clearly does a great job at reproducing voices, deepfakes, stylistic writing and producing a new, but relatively same-y genre of art. But currently without the capacity to actually reason, this regurgitation risks being inaccurate, or misrepresentative. Things like reverse causality and other fallacies are a constant occurrence with the current models and architectures. Then there’s also issues like de-biasing, which seeks to reverse vectors that are causing outputs from models that are unpalatable to Western-centric sensibilities. This is time consuming, but apparently necessary to make a model marketable. In general, training involves so much labeling and computing power that is very costly in terms of time, money and energy. One must wonder what those billions of dollars could do for these tech companies in other applications. Even being cynical and purely profit oriented, perhaps a better use of funds would be to finance mass education in computer science in undeveloped markets to create new and cheaper development talent pools.

IRBO Breakdown

Getting into more concrete stuff, IRBO looks like this in terms of major exposures.

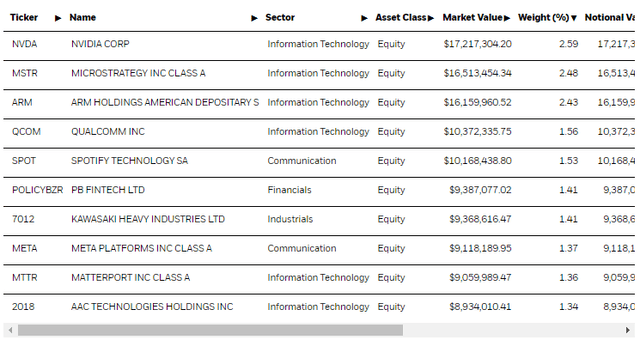

IRBO Top Holdings (iShares.com)

It is quite diversified, with 109 holdings.

In terms of direct upside exposure to AI, 57% of the allocations are in IT, but of those only around 15% have direct links to AI, including datacenters, relevant chipmakers, and various big tech companies involved in designing the architectures themselves.

As we discussed in our two-year-old article on IRBO, a lot of the exposures here aren’t really related to AI. A lot of them are just industrial stocks that have some robotics angle, where robotics isn’t necessarily considered leading edge tech anymore, and can involve all kinds of automation. For example, Kawasaki Heavy Industries (OTCPK:KWHIY) features on the first page with a 1.41% allocation. Much of the Japanese exposures at 10% overall capture these sorts of stocks. Almost 20% of the ETF is in communications and telcos.

Bottom Line

There’s also the matter of fees. At 0.47%, it is pretty expensive. It’s not a very complex global equities ETF, with mostly exposures to highly liquid and accessible markets. There’s nothing really exotic here. If ETF investors actually want to be exposed to AI, one could buy the SPY or the NASDAQ indices, which have the cheapest management fees of all. Since we are not sure and want to see whether or not the AI demand is sustainable, as sustainable growth is already priced in the market, we’d probably not get involved in IRBO or tech-weighted indices at this point. IRBO has a 30x PE, which may seem low, but only because all of the non-AI related exposures feature low PEs, with the AI exposures easily averaging the ETF’s PE ratio up.

Read the full article here