Genco (NYSE:GNK) is a shipper of drybulk cargo, which I covered in detail back in December. I was primarily looking at the stock for its dividend and rated the shares a Hold. In my conclusion, however, I noted:

Genco successfully turned itself around, became profitable, and eliminated debt to the point that I think it’s unlikely to go zero. There’s more to say about this company from a longer-term outlook, and perhaps that’s worth doing once we get farther into 2024

Now that some time has passed, I reassessed a bit, and I am more convinced the shares make for a good Buy to long-term investors.

Business Summary

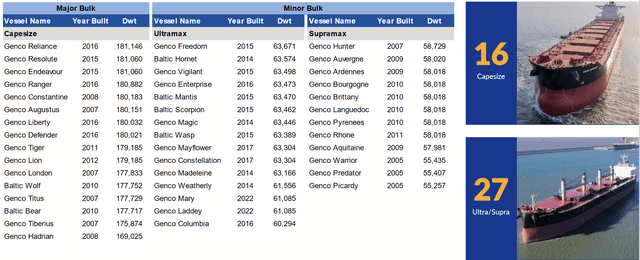

First, I’ll recap what Genco does. They own fleet a of 43 vessels used for international drybulk shipping.

Q1 2024 Company Presentation

Drybulk refers to various forms of cargo, which are broken into two classes: Major Bulk and Minor Bulk. Major largely refers to goods such as iron ore and coal, and some of their vessels are better-suited for those. Meanwhile, Minor refers to a wider variety of things like grain, cement, fertilizer and various metals.

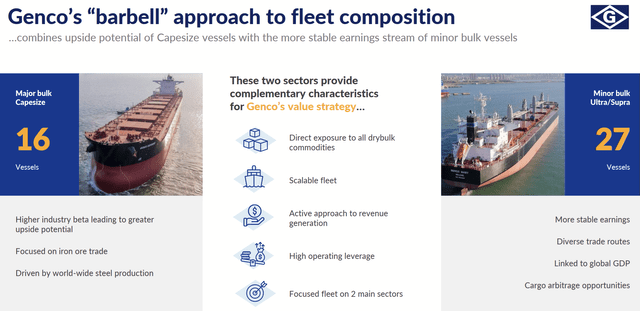

Q1 2024 Company Presentation

With the company employs what is calls a “barbell” strategy, enjoying the benefits of both, with Major being more volatile and possessing potentially strong upside, while Minor is more flexible and ensures a stabler baseline of cash flow.

Their vessels are chartered for use based on the short-term spot market. As such, the company’s financial results are heavily influenced by the Drybulk Index (BDIY:IND), which maps the trend of drybulk shipping rates.

FY 2023 and Q1 2024 Updates

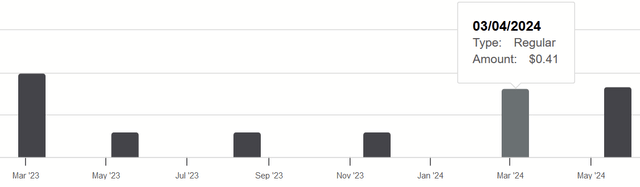

So let’s catch up on what’s happened for the last two quarters. First, the company increased its quarterly dividend substantially.

1Y Dividend History (Seeking Alpha)

It’s up from $0.15 to $0.41 in Q1 and $0.42 in Q2, a significant increase.

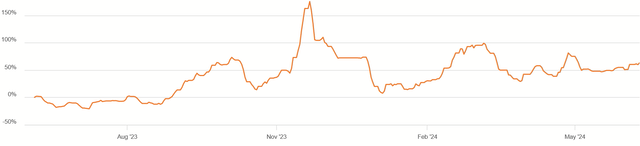

BDIY 1Y History (Seeking Alpha)

This owes to the fact that, while there have been some swings, BDIY is up 63% from a year ago and has generally remained above those levels. These partially owe to complications arising on the Panama and Suez Canals. In Q1 earnings, Michael Orr (Genco’s drybulk market analyst) observed:

As highlighted on Slides 20 and 21, low water levels in the Panama Canal impacted the number of ships that could transit, resulting in heavy delays in rerouting of vessels. Initially, vessels were diverted through the Suez Canal. However, attacks on commercial vessels in the region led many shipping companies to no longer transit the Southern Red Sea and Gulf of Aden area, further disrupting the efficiency of the global drybulk fleet.

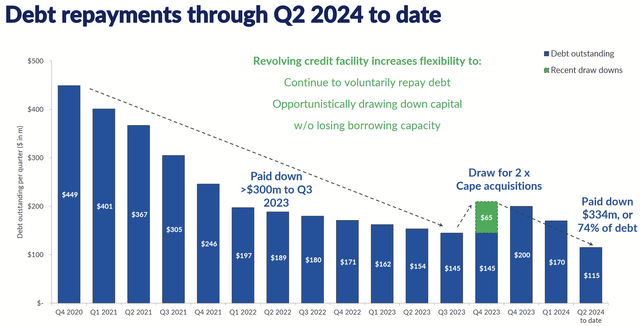

In addition to raising their dividend, they have also paid down more debt.

June 2024 Company Presentation

While they briefly increased it in Q4 2023 to buy some new vessels, that was quickly paid down. While Q2 results are not out yet, the company has reported debt is down to $115M currently.

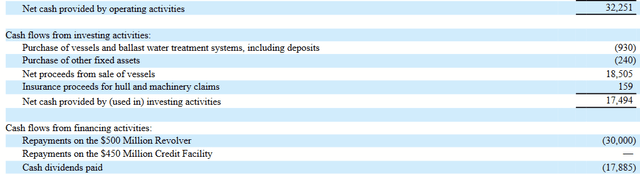

Cash Flow Statement (Q1 2024 Form 10Q)

Operating cash flows are positive, with dividends accounting for just over half of this amount. Remaining cash flow and the proceeds from scrapping the ships they replaced were used to pay down the revolver, showing good flexibility in their capital allocation while still distributing dividends to shareholders.

In summary, more good things happened in the last six months after my first article. It was a demonstration of what the company has become after its previous work to reform itself.

Future Outlook

Now that we can see how Genco cruises post-reformation, we can make some reasonable assumptions about its dividend going forward (as the dividend is the key draw of a shipper like this).

Dividend Policy

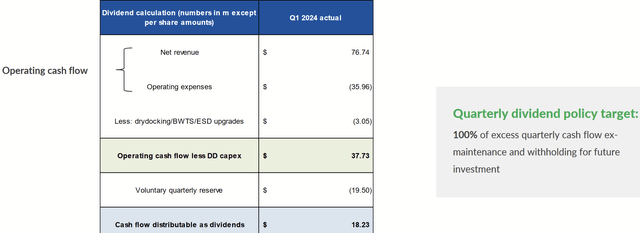

First thing that can inform this is their stated dividend policy. This slide from a recent presentation visualizes it well.

June 2024 Company Presentation

The dividend payout relative to OCF I mentioned earlier is not an accident. The company intends to distribute all excess cash flow after capex for drydocking and the voluntary quarterly reserve.

In their 2023 Form 10K (pg. F-14), they explain how drydocking affects their bottom line:

The Company’s vessels are required to be drydocked approximately every 30 to 60 months for major repairs and maintenance that cannot be performed while the vessels are operating…Costs deferred as part of a vessel’s drydocking include actual costs incurred at the drydocking yard; cost of travel, lodging and subsistence of personnel sent to the drydocking site to supervise; and the cost of hiring a third party to oversee the drydocking

In their Q1 2024 Form 10Q (pg. 41), they also give an estimate for such costs going forward:

Q1 2024 Form 10Q

If we compare that to the $3M spent on drydocking for Q1, we can see that it can vary quite a bit from quarter to quarter, depending on which vessels are due and what is entailed in their capex.

The latest 10Q also explains the voluntary reserve policy (pg. 36):

Anticipated uses for the voluntary quarterly reserve include, but are not limited to, vessel acquisitions, debt prepayments and repayments, and general corporate purposes. In order to set aside funds for these purposes, the voluntary reserve will be set on a quarterly basis in the discretion of our Board and is anticipated to be based on future quarterly debt repayments and interest expense.

In essence, most of this is being used to pay down their debt early. While drydocking capex doesn’t go away, debt can eventually be paid off. This means the baseline of their dividend while likely increase as voluntary reserves cease and as lack of interest expense increases OCF.

2023 Form 10K

Already, we can see that 2023’s interest expense was almost half that of 2021’s, due to the de-leveraging. With the current number of shares outstanding, paying off that debt that would increase dividends per share about $0.20 per year. That would raise the current baseline of about $0.60 (based on recent lows of $0.15 per quarter) to about $0.80. At the current share price, GNK’s financials suggest a minimum yield on cost of 3.8% going forward.

Growth

Growth of the dividend beyond those amounts will depend on other factors. As alluded before, revenues increase if spot prices for freight rates increase, demanding on how much demand for shipping exceeds supply. This is what causes BDIY to move like I said it did.

We can’t predict news events that might shift things in the short-term, but we can look at the key sources of revenue, but we can consider some long-term things.

Q1 2024 Company Presentation

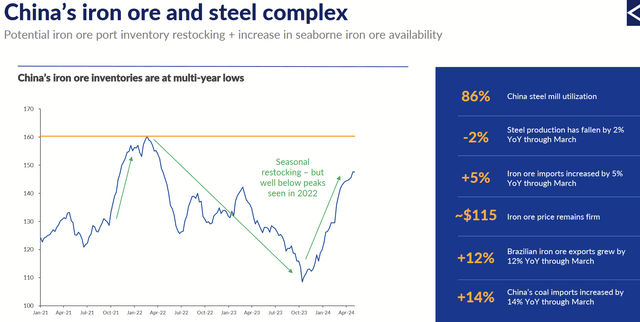

For example, last I mentioned how China is the nation’s leading importer of iron ore. As such, they drive demand for Genco’s ships. As iron ore inventories in China decrease, this results in more imports and follows seasonal trends. In Q1 earnings, management expected China’s 2024 steel production to be similar to 2023 levels. Similar sentiment on flat imports was expressed at the Iron Ore Forum in Singapore. As such, I don’t anticipate any major movements there. This suggests the current dividend, after the hike, can be held stable.

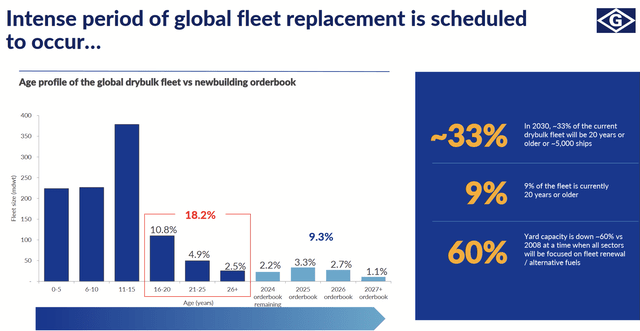

Q1 2024 Company Presentation

On the supply side, management is guiding for a bottleneck in the global drybulk fleet, as 18% of vessels in use are 16-years-old or older. A shortage in ships as they are replaced means that Genco can enjoy higher rates across is Major and Minor cargo.

Capital Allocation

Whatever happens on the supply-demand situation, I think the important takeaway for long-term investors is the adaptive posture Genco has taken with it capital allocation.

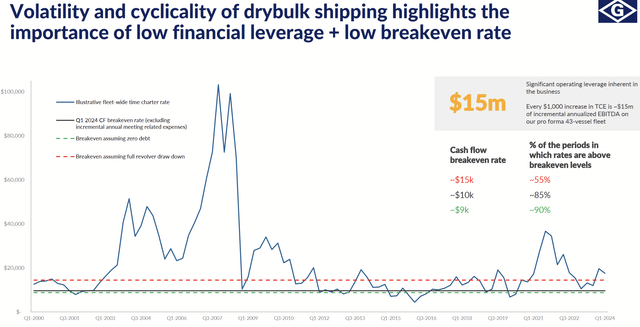

June 2024 Company Presentation

In the slide above, we see that shipping rates have been much higher, even compared to the spike in 2021 – 2022. What’s important, though, is how they operate such that the business is healthy and can survive when rates are lower. Their current breakeven rate, thanks to the cost reduction of years past, makes it more likely that they will stay in the game.

June 2024 Company Presentation

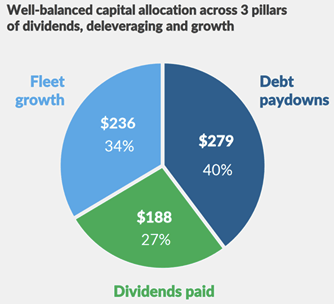

This allows Genco to be opportunistic in their allocation of capital: namely among growth of the fleet, debt reduction, and dividend payments. One might surmise that reducing debt to zero avoids bankruptcy, but such a commitment means capital could be trickier to raise. CEO John Wobensmith indicated that, for the right share price, they would be willing to sell equity for new ships, under the right conditions:

It’s probably more of, we’ve opted not to do things with equity. Clearly, issuing equity below NAV is dilutive and that’s not something we’re looking to do. But yes, as I said before, we’re getting very close to NAV and I’m cautiously optimistic that we’ll get there and hopefully above that as the value strategy continues. And, then you have that as you said, you have that arrow in your quiver in terms of an option to use it as hopefully a large piece of the purchase price.

So I am glad to see that they are not only committed to a strong balance sheet but that share sales will be done with mind to their intrinsic value and not be needlessly dilutive. We can surmise then too that management may also use ATM offerings of shares if they feel the same favorable mismatch between proceeds and the value of the investment exists.

And again, they can move on opportunities that they want, structured like this. It’s not a matter of tough decisions they will have to make like the distant past.

Conclusion

Since I first followed it, the company has executed well and given me a better feeling about its future. With a dividend yield around 5.5% right now, the low-end yield on cost looks to be 2.8% and 3.8% if interest expense is finally eliminated. Based on 2022’s results, it could even be as high a 10%. Growth from there will depend on continued cost reduction and benefiting from the upside of BDIY.

Because of management’s disciplined approach and the ability this gives them to move on opportunities, I think Genco makes for an attractive dividend investment over time, its cyclical ups and downs notwithstanding, and that’s why I’ve upgraded it to a Buy.

Read the full article here