ClearPoint Neuro’s (NASDAQ:CLPT) business continues to perform well, despite the stock languishing, with ClearPoint’s low market capitalization and ongoing losses likely keeping many investors away. This isn’t particularly important for the company’s long-term prospects though. After raising capital in March, ClearPoint appears to have a clear path to breakeven. The drug discovery business continues to perform well, and the broader release of its operating room and laser solutions should boost the rest of the business.

The last time I wrote about ClearPoint I suggested that it was a buy, despite the macro environment weighing on the stock, due to the company’s expanding product portfolio. This continues to be the case, with ClearPoint’s fundamentals strengthening while its valuation has become more attractive.

Biologics and Drug Delivery

ClearPoint’s biologics and drug delivery business delivered 61% YoY revenue growth in Q1. An expanding product portfolio and the progression of drug candidates into and through clinical trials should support growth in coming years. Within this business, ClearPoint offers a navigation system, software and SmartFlow cannulas, which support the delivery of cell and gene therapies directly into the brain. ClearPoint also wants to offer more comprehensive pre-clinical and clinical trial services to support its drug delivery partners through the regulatory process. This includes prototyping of additional routes of administration, as well as new AI enabled predictive and monitoring software.

ClearPoint has over 50 partners and is currently involved in discovery programs targeting 35 different disease states, providing meaningful diversification. Based on its current portfolio, ClearPoint believes that a partner could generate up to 10 million USD revenue before a drug is commercialized. ClearPoint also wants to increase participation in downstream value creation, although this could be a tough ask unless ClearPoint is willing to take on some share of the risk. The company believes that this is supported by value-add services like modelling though. If even just a few treatments are successful, ClearPoint’s revenue will grow significantly due to the volumes involved. In the event of commercialization, revenue is also likely to be extremely sticky due to co-labeling. The deployment of systems and growing practitioner familiarity could also help ClearPoint to build a barrier to entry in clinical trials.

While it is still early days for most of ClearPoint’s partners, data generally looks promising. ClearPoint’s partners are also making large investments, indicating commitment to cell and gene therapies for neurological disorders. This is perhaps best demonstrated by BlueRock Therapeutics, a clinical stage cell therapy company owned by Bayer. BlueRock Therapeutics’ Phase I clinical trial for Parkinson’s disease continues to show positive trends at 18 months. Bemdaneprocel is an investigational cell therapy designed to replace dopamine producing neurons that are lost in Parkinson’s disease. The treatment has the potential to reform neural networks and restore motor and non-motor function to patients. Planning is underway for a Phase II study which is expected to begin enrolling patients later in the year. Bayer has invested 250 million USD in a cell therapy manufacturing facility in the US. The plant will supply cell therapy products for clinical trials and future product launches.

The first quarter also saw the BLA submission of PTC Therapeutics’ AADC deficiency drug Upstaza. This could lead to a commercial gene therapy product in the US sometime in 2025. The therapy is directly injected into the brain, with ClearPoint’s SmartFlow Cannula classified as a co-labeled device.

AviadoBio is developing gene therapies for neurodegenerative diseases like frontotemporal dementia and amyotrophic lateral sclerosis. The company is working with ClearPoint to enable targeted delivery and maximal biodistribution with a favorable safety profile. AviadoBio recently dosed the first human patient with its frontotemporal lobe dementia treatment in a Phase I/II study. AVB-101 is an adeno-associated virus gene therapy which has been designed as a one-time therapy that could halt disease progression by restoring progranulin levels in the brain.

uniQure recently initiated a clinical trial for its gene therapy targeting Huntington’s disease. AMT-130 has been granted RMAT, orphan drug and fast track designations. It consists of an AAV vector, and a gene encoding a microRNA, and is administered once by neurosurgical procedure. UniQure is also developing treatments for Temporal Lobe Epilepsy and ALS.

Neurona is developing cell therapies for single-dose targeted repair of the nervous system. The company is conducting an open-label trial of NRTX-1001 for drug-resistant mesial temporal lobe epilepsy. The company is also developing treatments for neocortical focal epilepsy and Alzheimer’s disease.

ClearPoint doesn’t have a monopoly in this area though. For example, Spark Therapeutics and Neurochase are collaborating on delivery technology for CNS rare disease gene therapies. Neurochase offers technology for delivering therapeutics directly to the central nervous system using convection enhanced delivery. Spark Therapeutics is a gene therapy company acquired by Roche for 4.3 billion USD in 2019. Roche and Spark Therapeutics are committed to gene therapies, having invested 575 million USD in a 500,000 square foot Gene Therapy Innovation Center. This facility will serve as Roche’s center of excellence for gene therapy manufacturing globally.

Navigation for DBS

Deep brain stimulation could be considered the least attractive part of the business, but it often drives initial adoption. ClearPoint’s DBS business continue to grow, and this is being supported by product innovation.

ClearPoint recently released version 2.2 of its software, which included Maestro Brain Model capabilities, a feature that is useful across drug delivery, DBS navigation and laser ablation planning and prediction. Maestro helps users to identify both targets and safety zones in the brain, leading to superior performance versus manual expert segmentation and FreeSurfer, an open-source segmentation solution.

ClearPoint has also received FDA clearance for its SmartFrame OR, which is designed to help drive adoption of ClearPoint’s solutions in the operating room, where over 95% of all stereotactic procedures currently occur. There have already been clinical cases and early feedback appears positive. SmartFrame OR generally fits into existing workflows, which should enable rapid adoption. Full market release occurred at the start of June, with meaningful revenue contribution beginning in the second half of the year.

Laser Therapy

PRISM Laser Therapy is now in full market release and has already led to multiple new users and installations, including ClearPoint’s first laser capital sale. While navigation and laser disposables revenue was down approximately 18% YoY in the first quarter, much of this was due to the loss of brain computer interface revenue. Excluding this, revenue was fairly flat. ClearPoint expects to return positive double-digit revenue growth, starting in the second quarter.

The vast majority of laser ablation procedures are performed with navigation systems other than ClearPoint. As a result, SmartFrame OR could help to drive adoption using commonly available navigation and robotic systems.

ClearPoint expects submission of data for its 1.5-tesla clearance later this year. The study for this is currently being scheduled and planned. ClearPoint has also received FDA clearance for its Array version 1.2 software, which enables surgeons to perform a biopsy down one channel and a laser ablation down a different channel. This software has successfully been used at multiple centers.

Financial Analysis

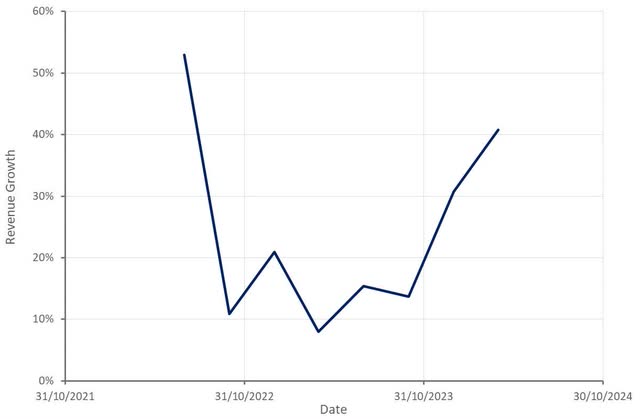

ClearPoint generated 7.6 million USD in the first quarter, an increase of 41% YoY. Biologics and drug delivery revenue totaled 4.3 million USD, up 61% YoY. Functional neurosurgery navigation therapy revenue declined 18% YoY to 1.9 million USD. The drop was attributed to a 0.5 million USD decline in service revenue. Capital equipment and software revenue amounted to 1.4 million USD, driven by multiple placements and ClearPoint’s PRISM laser system. Some hospitals have been opting for lease or rental programs, which has weighed on capital equipment and software revenue.

ClearPoint expects 28-32 million USD revenue in 2024, which would represent approximately 25% YoY growth. The fact that ClearPoint didn’t raise full year guidance, despite extremely strong results in the first quarter, has probably contributed to recent weakness. ClearPoint has suggested that Q1 results were supported by strong capital sales, which isn’t expected to be repeated through the year. Prism Laser and SmartFrame OR should begin to drive growth in coming quarters though.

Figure 1: ClearPoint Revenue Growth (source: Created by author using data from ClearPoint)

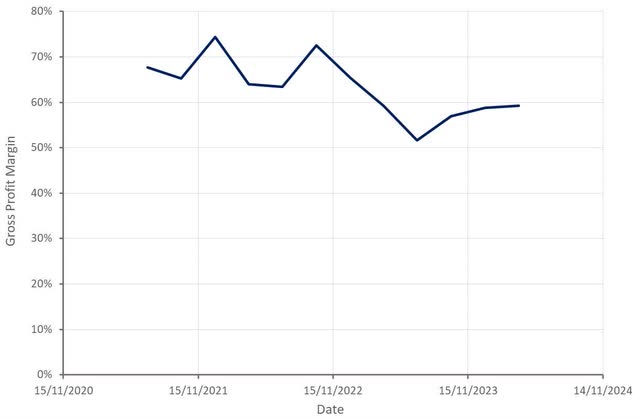

ClearPoint’s gross profit margin has stabilized in recent quarters, which is a positive given the rapid growth of the biologics and drug delivery business. This part of the business is likely to have relatively low gross margins until it begins to mature. ClearPoint has suggested that its margin on capital sales is 35-40% and most biologic deals have gross margins in excess of 50%. The scale up of ClearPoint’s OR and Laser products in coming quarters should also be supportive of margins.

Figure 2: ClearPoint Gross Profit Margin (source: Created by author using data from ClearPoint)

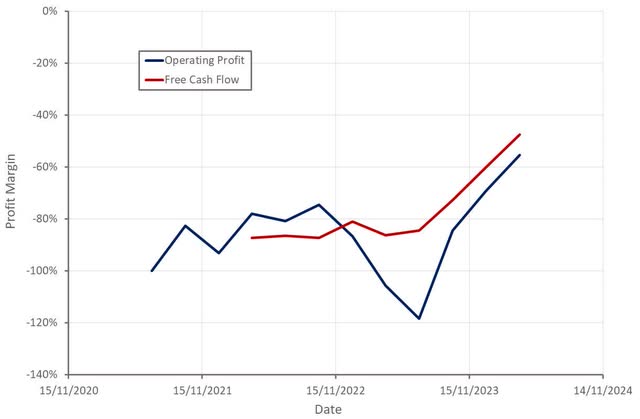

ClearPoint’s R&D expenses have been steady in recent quarters, as a result of the reprioritization of some R&D initiatives. Sales and marketing expenses continue to ramp as ClearPoint adds headcount to support the expansion of its business. Overall, operating expenses were fairly flat YoY, resulting in significant operating leverage.

At the end of Q1, ClearPoint had 35.4 million USD of cash and cash equivalents. The company’s cash burn in the first quarter was only 3.8 million USD. Based on this, ClearPoint appears to be on a clear path to breakeven with a sufficient cash balance to get there.

Figure 3: ClearPoint Operating Profit Margin (source: Created by author using data from ClearPoint)

Conclusion

ClearPoint’s business continues to expand rapidly, and this will be supported by new products throughout the remainder of 2024. The company’s margins are also steadily improving, reducing the risk of further dilution.

A capital raise in March contributed around 16 million USD. As a result, ClearPoint had approximately 35 million USD in cash and equivalents at the end of the first quarter. While there is convertible debt due in January 2025, this isn’t a large concern given the current strength of ClearPoint’s business.

Fundamentals do not seem to matter at the moment, though. Investors have little interest in small cap stocks or companies that are currently unprofitable. I tend to think that this will continue to be the case in the near-term. ClearPoint’s stock isn’t objectively cheap, and hence could still have further to fall. Looking at where the company appears to be heading over the next 5-10 years, ClearPoint looks compelling though.

Figure 4: ClearPoint EV/S Multiple (source: Seeking Alpha)

Read the full article here