Introduction

A few years ago, when I was researching Lithium and EV markets I read accounts that electricity demand from EV penetration could be akin to what was seen in the 1960s & 1970s with the penetration of microwaves, hairdryers, and air-conditioning, etc. that drove demand 30%, or about an additional 2% per year, which is considerable and would require electric utilities to invest in capacity and grid resiliency. Then the summer heat waves began, and another layer of demand was added as it’s unlikely the earth’s climate will become cooler in the next 50 years. More recently yet another layer of demand was added with the rapid development of generative AI that requires more processing power and cooling as well as the rapid build-out of data centers. All combine for an estimated doubling of electricity demand in 10 to 20 years which is a 3% to 7% annual increase, further complicated by the transition to clean energy i.e. eliminating coal and perhaps at some point natural gas-fired power plants. This is where GE Vernova Inc. (NYSE:GEV) comes in as one of the few companies that build and services gas, wind, nuclear, and hydro power plants, and electrical grids.

GEV

What is GE Vernova

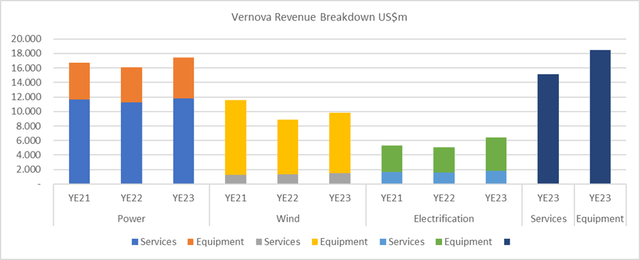

The 100-year-old company, post-split from General Electric Company (GE) is one of a few on the plant that manufactures & services turbines and generators that convert wind, nuclear, natural gas, or coal into electric energy. GEV has three business units, Power, Wind, and Electrification, and further splits each business by Equipment and Services. The chart below illustrates the relative importance of each, Power is the largest with 52% of revenue, followed by Wind with 29%. However, the Equipment side of the business is 55% of revenue with the largest in Wind at 25% followed by Power at 17%. This is relevant as it indicates that revenue growth may be limited given the Services segment is contract-based and applies to the current equipment fleet.

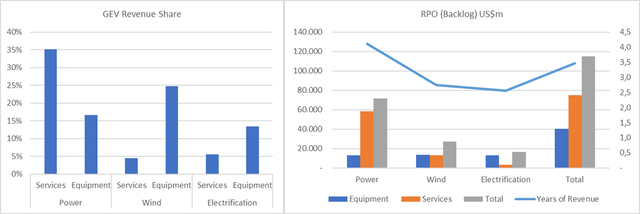

The GEV business was a razor/razor blade model where it broke even on equipment manufacturing and earned a margin on long-term service contracts. The current RPO (Remaining Performance Obligation) or backlog supports over 3 years of future revenue and 65% from services, which does not have high growth and is based on established contracts. The key focus for GEV to attain earnings and cash flow growth is executing cost-cutting and pricing to drive margin expansion from 2% to 10% by 2026.

GEV Revenue Mix (Created by the author with data from GEV) Created by the author with data from GEV

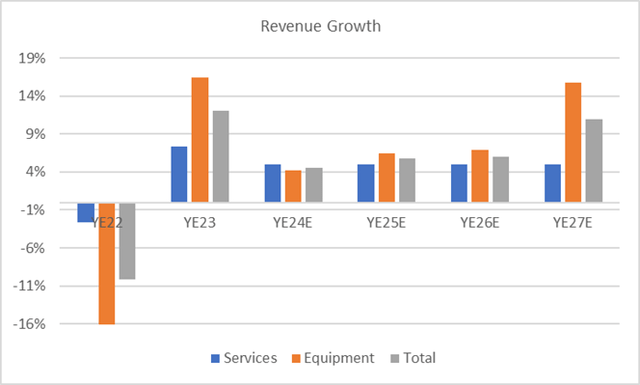

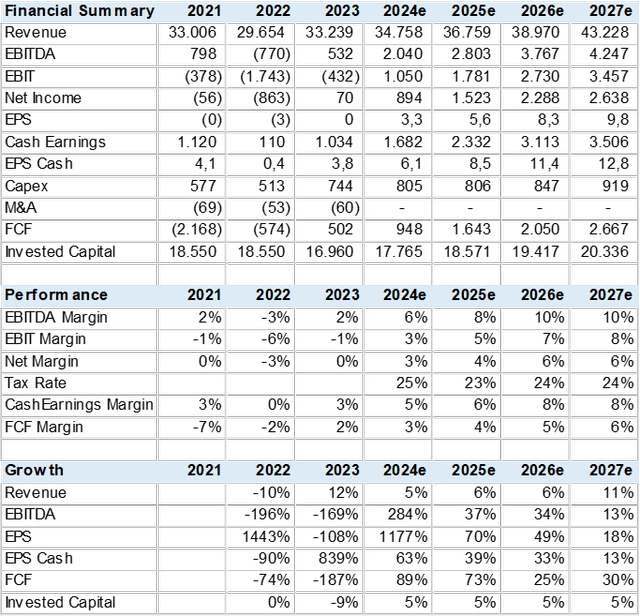

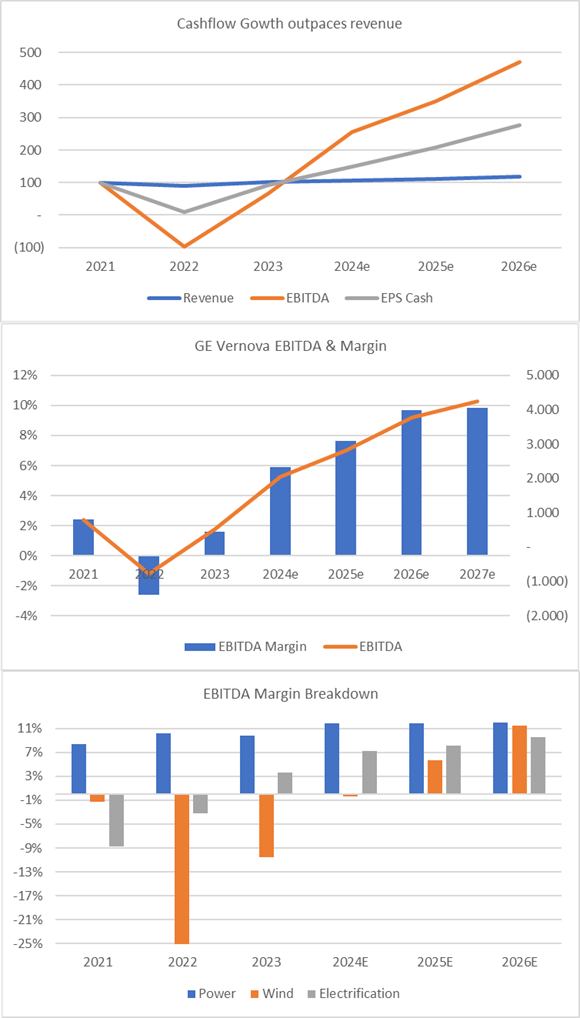

Modest Revenue Growth

GEV is not a high-growth company due to its size, manufacturing limitations, and more importantly because 45% of revenue is derived from long-term service contracts of the existing equipment base. This means the demand for turbines and generators may increase but may not translate into sales for a few years and is added to RPO, which does provide for improved execution, manufacturing planning, capex, and margins. This is illustrated in the chart below, drawn from consensus estimates where revenue growth is estimated at 6% until 2027 when it jumps to 11% on higher equipment sales.

Created by the author with data from GEV & Capital IQ

EPS Driven by Margin Gains

I used consensus estimates from 12 analysts to gauge GEV’s growth and profitability metrics. It seems the consensus is somewhat ahead of guidance on margin expansion. GEV’s goal is to reach a 10% EBITDA margin by 2028 while the market assumes this will occur in 2026. These margin gains seem attainable for several reasons, the first is GEV’s commercial strategy to end the razor/razor blade strategy and seek positive margins for equipment sales. Then there is an internal focus on cutting costs and becoming more efficient across all segments. Finally, and most importantly, is the top-down environment of high electricity demand that shifts pricing power to GEV vs the customer. The scramble for utilities and IPPs to add capacity makes GEV’s task substantially easier than in a flat or down market. The great news is that this high demand scenario is likely to be with us for 10 or more years.

Against this backdrop, consensus estimates EBITDA growth may jump to over 30% and drive EPS growth of 70% in 2025 and 49% in 2026. GEV may be able to post positive FCF that eventually can be used in dividends or share buy-backs, that are not currently forecast.

Consensus Forecast (Created by the author with data from GEV & Capital IQ) Margin Expansion Estimates (Created by the author with data from GEV & Capital IQ)

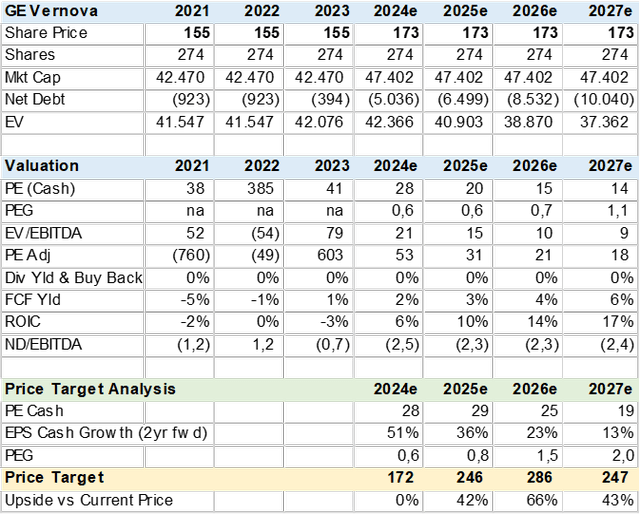

Valuation

The consensus has a 2024 price target of US$172 which is an implied PE (cash) target multiple of 28x or a PEG of 0.6x, which seems reasonable until GEV can deliver on EBITDA margin gains. Using consensus estimates I calculated the EPS (cash) growth rate and assumed a fair PEG should increase to 0.8x for 2025 that provides for a price target of US$246 or 42% upside potential. Note that I utilize EPS cash as a primary growth and valuation metric that is calculated using normalized net income plus depreciation plus share-based compensation.

GEV is a new stock without a trading and valuation history, so I compared its consensus valuation with peers and found that on PEG bases it trades in line and that many have similar high growth forecasts, especially in the wind segment.

Consensus Valuation (Created by the author with data from GEV & Capital IQ) Peer Valuation (Created by the author with data from GEV & Capital IQ)

Risk

The primary risk to the GEV equity investment case is the failure to increase EBITDA margin guidance to 10%. This turnaround could be derailed by several factors such as poor cost control and productivity, manufacturing cost overruns, and or inability to pass on inflation in service contracts. This lack of cash flow would in turn negatively impact earnings and valuation. Revenue is not a particular risk given the 3.5 years of backlog, while the company is net cash and can survive many years with negative margins.

Conclusion

I rate GEV a BUY. While the stock has reached consensus fair value rapidly in only a few months post-spinoff, I find that its turnaround story can have multi-year 20% plus cash flow growth driven by internal productivity execution and, more importantly, the highest demand environment for electricity generation equipment in the last 50 years. This combination should lead to increased valuation and eventually dividends and share buybacks.

Read the full article here