Introduction

Carlyle Secured Lending (NASDAQ:CGBD) is a BDC that I’ve haven’t written on but have kept close tabs on in the sector. Although I don’t currently own them, I’ve been quite impressed with their performance during the high interest rate environment. The company’s fundamentals remain strong showing solid growth year-over-year. Moreover, with interest rates likely to decline in the short to medium-term, I think Carlyle Secured Lending is the perfect BDC to add to your income portfolio on a pullback.

Brief Overview

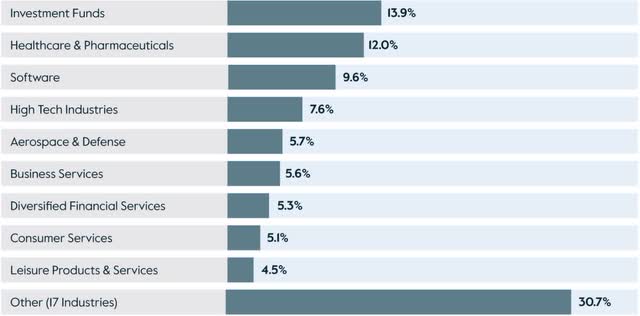

Carlyle Secured Lending is a fairly new BDC having IPO’d just 7 short years ago. They are an externally-managed BDC that lends to U.S middle-market companies with EBITDAs in a range of $25 – $50 million. Most of their loans are highly-diversified in Investment Funds, Healthcare & Pharmaceuticals, and Software.

Carlylesecuredlending

Latest Earnings

CGBD reported their Q1 earnings in early May with a beat on their bottom line. Net investment income came in $0.02 above analysts’ estimates at $0.54. Although this declined $0.02 from the prior quarter, it grew 8% year-over-year.

Total investment income also declined slightly from the prior quarter’s $62.6 million to roughly $62 million. This can be attributed to a decline in their portfolio’s overall value. The BDC exited investments during the quarter as their portfolio value decreased slightly from $1.84 billion to nearly $1.8 billion.

The drop can also be attributed to a decrease in amendment fees and OID acceleration. Despite this, their total company count grew to 131, up from 128 in the quarter prior. Originations were also up double-digits on an annualized basis with the mean EBITDA also increasing double-digits from $73 million in Q1’23 to $81 million during the recent quarter.

So, as the macro environment has presented challenges, specifically for BDCs, CGBD continued to strengthen their portfolio with larger companies. Additionally, non-accruals improved during the quarter as well.

These now account for less than 1% at both cost & fair value. At just 0.2% at cost & fair value, the growth in median EBITDA seems apparent as non-accruals also declined year-over-year. These stood at 3.5% on a fair value basis, a significant decline as management worked tirelessly to positively position their portfolio.

Furthermore, this is a testament to their management team as rising non-accruals have plagued many BDCs during the high interest rate environment. Peer PennantPark Investment (PNNT), who added two new companies to their non-accruals list stood at 3.7% at cost and 3% at fair value.

Monroe Capital (MRCC), a smaller peer in terms of market cap also saw a slight increase of 1.1% in their non-accruals quarter-over-quarter. These represent 2.7% of their portfolio at fair market value. So, in comparison, Carlyle’s borrowers seem to be performing much better.

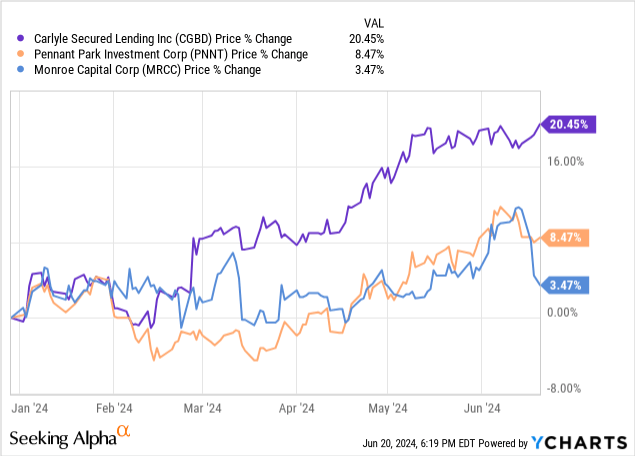

And this is apparent in terms of share price. In the chart you can see CGBD has significantly outperformed both peers, up double-digits more than 20% in comparison to 8.5% for PNNT and 3.5% for MRCC.

Solid NAV Growth

The BDC also showed decent growth in their NAV with this increasing modestly to $17.07, up from $16.99 in Q4. On an annualized basis NAV declined slightly from $17.09. BDCs typically grow their NAV by continuing to grow their portfolio and out-earning their dividends.

But this can see volatility over time as a result of loan repayments and dividend payments. However, this is something investors shouldn’t worry about in the shorter-term. NAV growth over a longer period of time shows the health of the company’s portfolio and should be considered when looking to invest into any BDC.

Consistent NAV erosion is something investors should be concerned with as this typically leads to underperformance in share price and total returns. Since the start of rate hikes in 2022 CGBD has been able to steadily grow its NAV from $16.91 in early 2022. And with them being a fairly new BDC, public less than a decade, I expect their NAV to show solid growth for the foreseeable future.

Strong Dividend Coverage

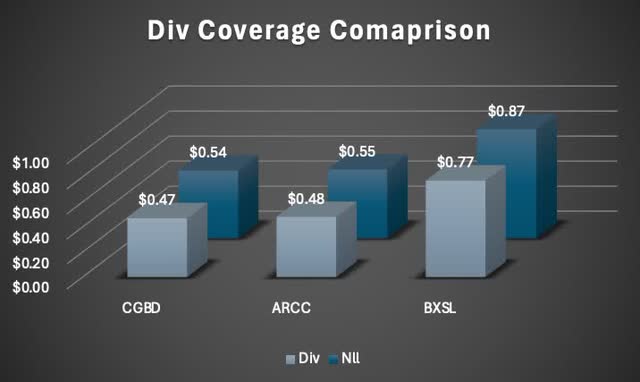

Their alignment with shareholders is another reason I think CGBD is the perfect addition to an income-focused portfolio as externally-managed BDCs are usually more fiscally conservative. And despite the decline in net investment income quarter-over-quarter, Carlyle Secured Lending continued to show strong dividend coverage. Even paying a supplemental of $0.07, Nll of $0.54 still comfortably covered total dividend payout, giving them coverage of 115%.

This was higher than both the aforementioned peers as their net investment income matched their quarterly run rate. For context, this is higher than two favorites within the sector, Blackstone Secured Lending (BXSL) & Ares capital (ARCC) during their latest quarters. Both had dividend coverages of 113% and 114% respectively.

Author creation

Strong Balance Sheet

Carlyle Secured Lending is also in a strong position financially as a result of their balance sheet. Their well-laddered debt gives them capital flexibility. Over the past year the BDC has been increasing their liquidity, which puts them in a strong position to make investments when activity picks up, likely in the back half of the year. CGBD increased their cash & cash equivalents from $42.8 million to nearly $70 million.

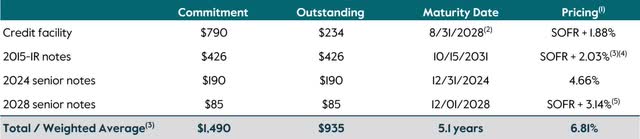

Their debt-to-equity level was also healthy and below the sector mean 116% at 113%. Their debt maturities are also well-laddered with total debt of $1.5 billion with $190 million due in December of this year. This had a weighted-average interest rate of 4.66%. Moreover, their next debt maturity isn’t until four years later in 2028 with $85 million maturing, putting them in a comfortable position to capitalize on future growth opportunities.

CGBD investor presentation

Risks

With interest rates expected to decline this September, Carlyle Secured Lending faces downside risks as lower interest rates are likely to impact their net investment income as 100% of their debt is floating rate. I expect this to be a gradual decline but their financials will be impacted by declining interest rates, placing pressure on their dividend coverage.

CGBD investor presentation

Valuation

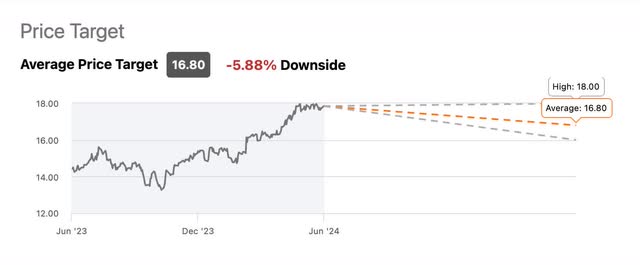

As a result of their strong performance, CGBD now trades at roughly a 5.5% premium above its NAV. This is higher than the 3-year average discount of roughly 14% and slightly above the high premium of 5.39% So in terms of valuation, CGBD appears to be overvalued at the moment.

Moreover, with rates expected to decline, I do anticipate a pullback within the sector. And think CGBD will also see a drop in share price as those investors seeking higher-yields will likely rotate out the sector with BDCs eliminating the specials and/or supplementals for the most part.

Additionally, they are expected to see some downside from Wall Street, likely as a result of lower interest rates. And if so, I think investors looking for income should consider buying CGBD near the $16 level and below for a margin of safety.

Seeking Alpha

Conclusion

Carlyle Secured Lending has all the makings of a great BDC as a result of their overall portfolio quality. Additionally, they have performed exceptionally in an environment where some peers’ portfolios have started to show signs of weakness. Their fundamentals are also strong with well-laddered debt maturities, which gives them capital flexibility to continue growing organically. This is also a testament to their management team and in my opinion, CGBD is the perfect BDC for income-focused investors to buy on a pullback.

Read the full article here