A window has opened between now and the end of June that could see the equity market start a sizeable pullback. The passing of the June options expiration means that hedging flows will no longer support the market as liquidity levels drop heading into quarter-end.

The passing of options expiration on Friday means that the S&P 500 and the equity market will significantly reduce gamma levels. This reduction means that the pinning effects that created the tight trading ranges over the past week will be removed from the market.

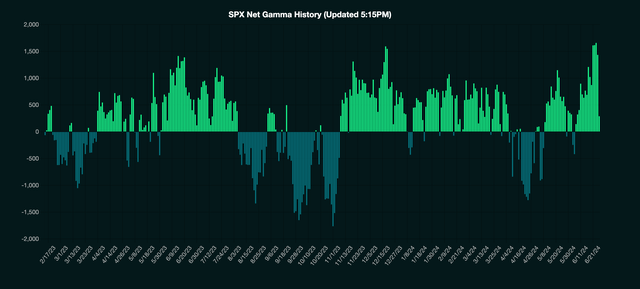

Gamma Level Will Be Reduced

Gamma levels in the S&P 500 had risen sharply in the days leading up to June OPEX, reaching nearly $1.7 trillion. Now that opex has passed, the gamma level dropped to around $260 billion as of Friday’s close. That is a massive reduction in gamma and, with it, a big reduction in market stability.

Large amounts of gamma can help buffer the equity market from pullbacks because, typically, market makers can be buyers of pullbacks. The higher gamma amounts also create tighter trading ranges because market makers become sellers of rallies.

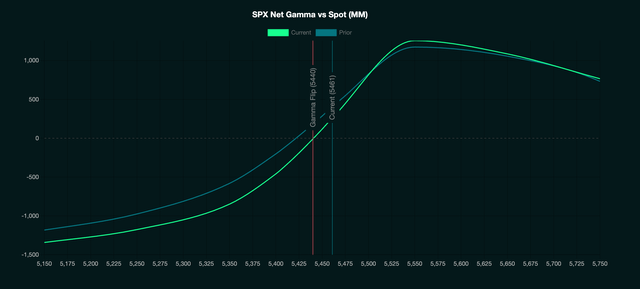

GammaLab

It is also important to note that the zero gamma level, when gamma can flip from positive to negative, is 5,440. That means that below 5,440, supportive flows will vanish, and selling will beget more selling as the market enters a negative gamma regime.

GammaLab

Potential Liquidity Drain

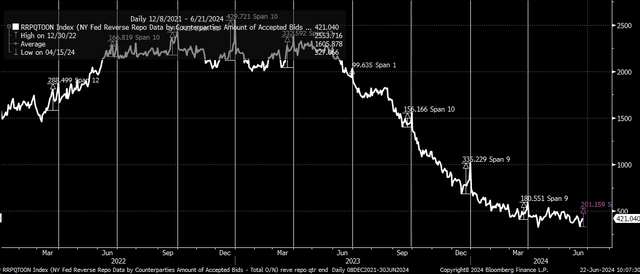

Additionally, the last week of June should see a sizeable increase in the Fed’s reverse repo facility usage. We typically see an increase in reverse repo usage as we head into the quarter-end as banks look to pull cash from the overnight funding market and park it at the safer Fed repo facility to shore up their balance sheets.

Typically, the repo facility rises about 7 to 10 days before quarter-end and tends to increase by around $150 to $300 billion. June of 2023 did not see that increase, rising to only $99 billion. But last year, the repo facility was in the process of draining as Treasury bill issuance surged. This year, the repo facility has been more stable, and net issuance amounts have been lower in most cases or even negative in recent weeks. So, it is possible to see the typical $150 to $300 billion increase in usage heading into the last day of the month.

Bloomberg

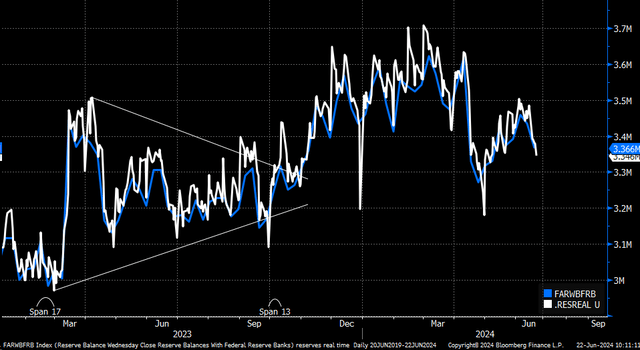

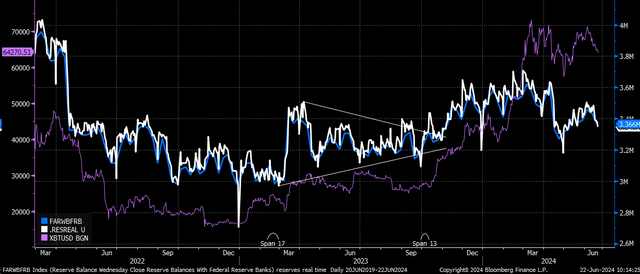

Liquidity at the Fed fell last week as the Treasury General Account increased due to quarterly tax receipts, pushing reserves balances held at the Fed down to $3.35 trillion. When the TGA rises and the reverse repo facility rises, reserve balances held at the Fed are reduced, which can act to drain liquidity from across risk assets.

Bloomberg

Risk Assets Feeling The Effect

This has been the case when evaluating changes in Bitcoin’s (BTC-USD) price versus changes in reserve balances. Bitcoin’s recent weakness seems to correspond to the decline in reserve balances since the beginning of 2024.

Bloomberg

This has also mostly been the case with the S&P 500, with the last couple of weeks being the expectation. It is possible that flows witnessed from this week’s options expiration distorted some of those potential impacts that were witnessed in Bitcoin. Or, it could be that NVIDIA’s (NVDA) stock overrunning the equity market has overcome even the effect of declining liquidity in the market.

Bloomberg

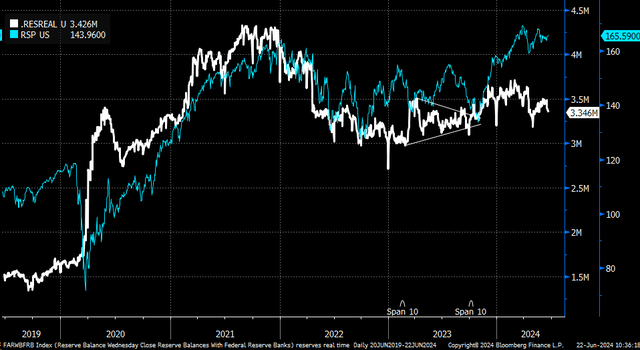

The equally weighted S&P 500 ETF (RSP) has mostly remained unchanged from the changes in reserve balances, which is likely because Nvidia is neutralized in this equal-weighted version.

Bloomberg

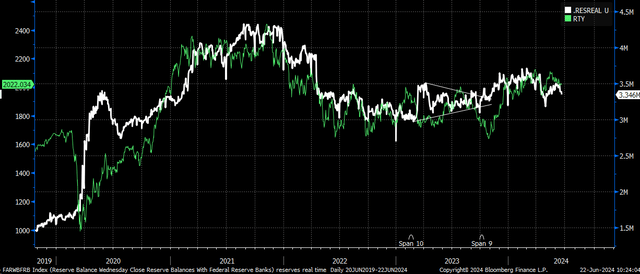

However, Russell 2000 (RTY) followed the changes in reserve balances fairly closely and stuck with the script, as noted by changes in liquidity flows in reserve balances.

Bloomberg

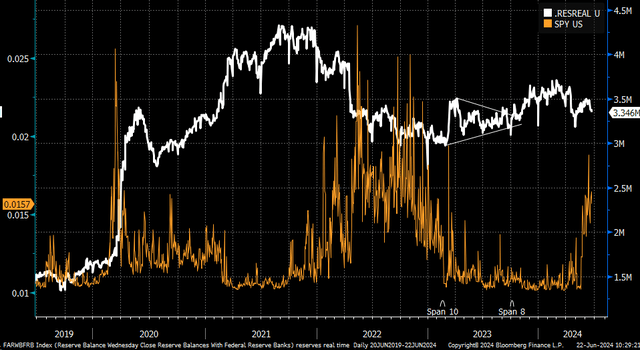

Additionally, the declines in liquidity in reserve balances could even help explain why the spread between the bid and ask in the SPY ETF (SPY) has widened in recent weeks. As liquidity falls, the spreads widen, and the spreads narrow as liquidity stabilizes or rises. The recent widening of the spread between the bid and the ask could be directly tied to liquidity and changes in reserve balances.

Bloomberg

Overall, a combination of events taking place in the equity market over the course of this week could result in volatility rising and equity pricing pulling back as it loses some of those supportive flows and liquidity that have been so critical in boosting stocks and helping them rally.

Read the full article here