iShares National Muni Bond ETF (NYSEARCA:MUB) is a popular way to add (tax-free) municipal bond exposure to a portfolio. This ETF has about $37.6 billion in assets under management and offers an extremely low expense ratio of 0.05%. The 30-day SEC yield is 3.49%, and that puts the tax-equivalent yield at nearly 6%. Since its inception in September 2007, this fund has returned just over 3.19% annually. The one-year and five-year performance numbers are not as good with one-year total returns of just about 2.77% and five-year returns averaging nearly 1.57% annually. However, the one and five year performance numbers were heavily impacted by one of the worst bear markets in history for the bond market. With the Federal Reserve appearing to lay the groundwork for a new rate cutting cycle, this ETF could offer a solid yield, along with the potential for capital gains.

The Chart

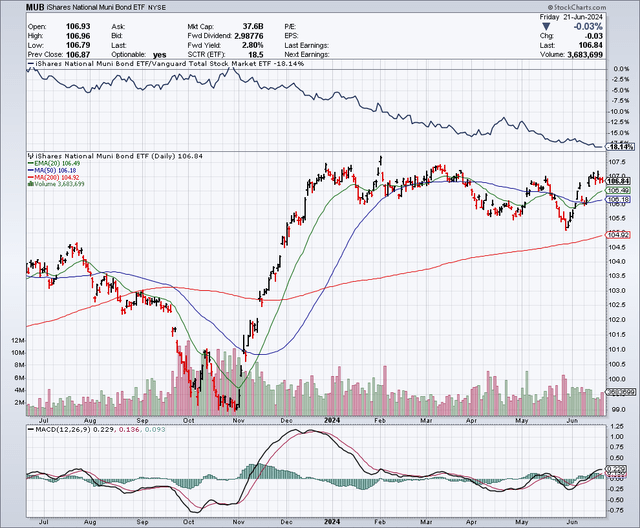

As the chart below shows, this ETF bottomed out in late October 2023, and it has since been moving higher. It has paid off to buy the dips, and I believe that trend will continue. The 50-day moving average is $106.18 and the 200-day moving average is $104.92. The current share price is just slightly above the 50-day and 200-day moving average. Therefore, I would view pullbacks close to these moving averages as buying opportunities.

StockCharts.com

Top Ten Holdings

Source: Seeking Alpha

This ETF has around 5,697 holdings which means it is extremely well diversified. As shown above, none of the top ten holdings even come close to representing half of 1% of the portfolio. This means the default risk or credit rating downgrade of a single position would not have a material impact on this fund. This provides a lot of peace of mind for shareholders. The effective duration of this fund is just over 6 years, which is ideal for many investors since it is not too short term in nature, but also not too long term either.

The Dividend

This ETF pays a dividend that varies somewhat as to the timing and amount. As noted above, the current 30-day SEC yield is about 3.49% and puts the tax-equivalent yield at nearly 6%. With money market yields currently at just around 5%, this is an attractive yield for many investors, especially those that are in higher tax brackets.

The most recent dividend was paid on June 7, and it was for $0.2781 per share.

Why MUB Could Offer Strong Total Returns

I see a number of reasons why buying MUB could make a lot of sense right now. Here are some of the biggest reasons I see this ETF as a strong buy:

1.) The U.S. National debt is exploding, and it is approaching the $35 trillion level. This is equivalent to a debt of roughly $266,952 for every taxpayer in this country. That is possibly not sustainable in the long run and especially so with interest rates much higher than they were a couple of years ago. At some point, the U.S. Government will probably need to reduce spending after years of Covid stimulus, cancelling student loan debt and giving aid to foreign countries, and most likely taxes will have to be increased to pay for this massive existing debt and all the interest that is accruing. If tax rates go up, it will make tax-free investments like MUB even more attractive and valuable to investors, and this could lead to capital gains for those who lock in the current price and yield today.

2.) Unless Congress acts relatively soon, Trump tax cuts are set to expire in 2025, and the expiration of these tax cuts would essentially act as an automatic tax increase for many U.S. taxpayers. The Trump tax cuts have lowered federal income tax brackets and have given bigger standard deductions as well as other benefits to taxpayers. The potential expiration of these Trump tax cuts are estimated to impact about 60% of U.S. taxpayers, and it is being considered as a potential looming tax cliff. Because of this, many tax advisors are suggesting a number of strategies that their clients should consider doing now in order to minimize the impact. I believe locking in tax-free yields could be part of the solution.

3.) We could be late in the economic cycle and investors might start thinking more about return of capital rather than return on capital. There are many “FOMO” (fear of missing out) opportunities in the market today, and that can fuel excessive speculation that eventually leads to losses for many investors in a potential market correction. When there are significant market corrections, many investors look for safe places to hide and investments that let them sleep well at night. MUB won’t make anyone rich, but it can definitely keep you rich and even if you’re not rich, it can be a place to preserve your capital without adding to your tax obligations.

4.) The Federal Reserve recently updated its economic projections, and it continues to forecast a big drop in interest rates between now and 2026. According to the Federal Reserve, the Fed Funds rate could drop from about 5% currently, to just around 3% in 2026. Under this scenario, money market yields are likely to plunge to around 3% in the next couple of years. If this happens, it would make sense for the share price of MUB to rise significantly, since it would become far more attractive to investors in a world where money market yields are much lower.

What I Like About MUB

This ETF offers a solid yield of 3.49% which is even more attractive when you factor in the tax advantages. It is one of the most popular ways to add municipal bond exposure to a portfolio and because of this, it has very high trading volumes which provide liquidity. In addition to liquidity, this fund offers extremely strong diversification since it holds around 5,697 positions and none of them are even close to being even one half of 1% of the portfolio. I believe that in addition to the solid yield, this fund could provide even bigger total returns through the capital appreciation potential it has when interest rates decline and taxes potentially rise in the coming years.

Potential Downside Risks

The Federal Reserve could be wrong about interest rates declining in the next couple of years. If the Fed continues with a higher for longer interest rate policy because inflation reignites, my investment thesis won’t play out as expected. Even worse, if the Fed is forced to raise rates due to inflation, the value of bonds could drop significantly and create a downside risk for investors.

There is also another major potential downside risk to consider and that is if the exploding levels of government debt causes the bond market to demand higher rates with the view that default risks are rising and therefore this warrants a higher yield. Also, if there is an economic slowdown, the U.S. Government and municipalities could see lower levels of tax collection and that could result in a shortfall in their budgets. That could result in credit downgrades and lower bond prices.

In Summary

I think this fund is a strong buy right now, especially on pullbacks. It offers significant diversification and liquidity, plus a yield that is attractive now and will likely be even more attractive if interest rates decline and if tax rates go up. Overall, I see this fund as an ideal core holding to hedge against stock market corrections and as a way to potentially reap the capital gains that could come in the future, driven by the likelihood of higher taxes and lower interest rates.

No guarantees or representations are made. Hawkinvest is not a registered investment advisor and does not provide specific investment advice. The information is for informational purposes only. You should always consult a financial advisor.

Read the full article here