Symbotic’s (NASDAQ:SYM) second quarter results were reasonably strong, with robust growth somewhat undermined by a deterioration in margins. GreenBox appears set to begin contributing though and Symbotic continues to expand its product portfolio. While the narrative hasn’t really changed in recent quarters, Symbotic’s stock has been under pressure, which could be due to moderating growth and poor margins.

I previously suggested that elevated supply chain investments and demand for automation would support Symbotic’s business in the near-term. Even though the company’s growth is declining, I continue to think Symbotic’s business will perform well in coming quarters, but the company’s valuation is not justified by fundamentals.

Market Conditions

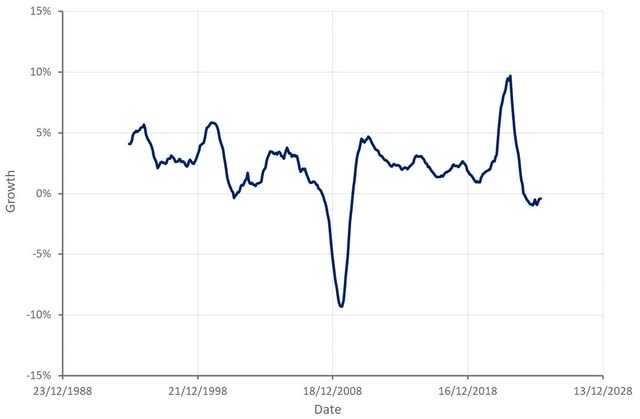

At a macro level, demand for Symbotic’s products is likely heavily dependent on the cost of capital and retail sales. While demand is still currently extremely robust, this could be due to the large backlog created during the pandemic. The longer that current conditions persist (weak retail sales growth and high interest rates), the higher the probability that demand for Symbotic’s products will falter. Symbotic has also possibly been aided by its exposure to larger organizations who have the financial strength to invest through temporary weakness.

Figure 1: Real Retail Sales Growth (source: Created by author using data from The Federal Reserve)

Symbotic Business Updates

Symbotic continues to upgrade its bots, recently improving its time space routing algorithms, allowing it to increase transfer capacity and bot density. The introduction of GPUs has also increased computational power, enabling bots to recognize deformed boxes using vision systems and AI. Around 40% of Symbotic’s bots are vision-enabled. This type of capability is also likely an important force multiplier for Symbotic, helping the company to address the long tail of demand that exists outside of larger customers.

Perishables will likely be one of the next expansion areas for Symbotic. The company has started testing and doesn’t believe that perishables require significantly changed capabilities. Symbotic believes that it will have a compelling solution, if for no other reason than perishable warehouse capacity is expensive (2-3x ambient) and Symbotic’s systems can help customers to more effectively utilize space. Perishable warehouses were not included in Symbotic’s TAM estimate. While the perishable TAM is likely less than the ambient TAM, it is still expected to be large.

Symbotic was planning on beginning its second breakpack installation this summer. Symbotic hasn’t stated who this is for, but the customer could be Walmart, as breakpack is considered part of the Walmart backlog. Walmart uses Breakpack for anything that goes into the store that isn’t full cases. Symbotic believes that this solution could become an important part of omnichannel warehouses, providing both case and each handling capacity. Dollar stores are another potential source of demand that Symbotic will be targeting.

Symbotic recently finished the restructuring and outsourcing of its manufacturing operations, which could help to support the company’s expansion going forward. Symbotic has been supply constrained in the past as it has tried to scale its supply chain and manufacturing operations. As a result, deployments could now reasonably be expected to begin increasing in coming quarters. Whether this just results in a temporary surge as Symbotic works through its existing backlog is less clear, though.

While GreenBox is still being established, the JV recently signed its first logistics-as-a-service customer. Symbotic will begin recognizing GreenBox revenue in Q3. GreenBox will automate and operate a brownfield warehouse for C&S Wholesale Grocers. Partnering with GreenBox allows C&S to accelerate its transition to an autonomous supply chain in a capital efficient way. While this will primarily be a C&S site, there will be extra capacity that could be used for other customers.

Financial Analysis

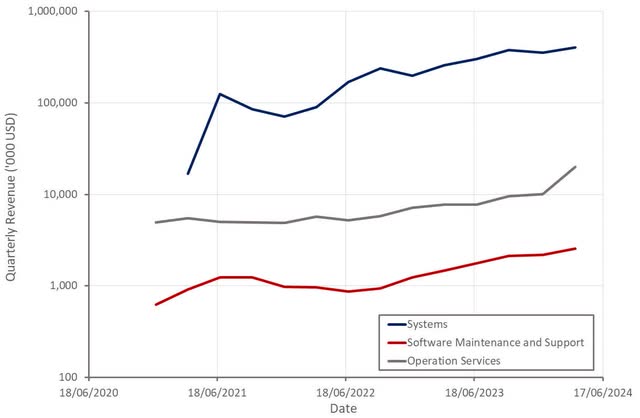

Symbotic generated 424 million USD revenue in the second quarter, an increase of 59% YoY. Three new system deployments were initiated during the quarter and three were completed. While this is somewhat soft, Symbotic expects system starts to accelerate during the rest of the year. Symbotic now has 18 fully operational systems, which is supporting recurring revenue growth. Recurring revenue was up 145% YoY, although this was driven by several one-time events that won’t be repeated going forward.

Symbotic’s backlog declined slightly to 22.8 billion USD at the end of the second quarter. This is worth monitoring as excluding GreenBox, Symbotic’s backlog has been fairly flat for several years.

Symbotic expects 450-470 million USD revenue in the third quarter, which would represent 47% YoY revenue growth at the midpoint. GreenBox and greater supply capacity could drive upside, but Symbotic has struggled to beat guidance in recent quarters.

Figure 2: Symbotic Revenue (source: Created by author using data from Symbotic)

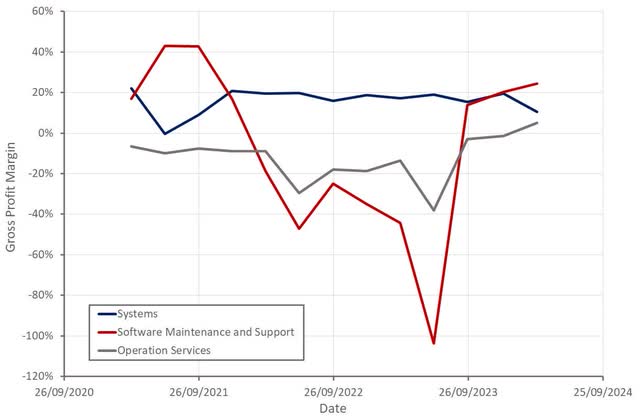

Systems gross margin was down in the second quarter, with innovation projects weighing on margins. Symbotic has stated that some of these lower margin projects will reach completion in the second half of the year. Symbotic also recognized a 34 million USD charge in the quarter related to the outsourcing of bot assembly and component inventory management. Part of the restructuring charge was also related to updating older systems so that everything is standardized going forward.

Recurring revenue gross margins are now progressing towards Symbotic’s 60% target. The benefit of this will be fairly limited in the short-term though, as systems deployment dominate revenue. Gross profit margins could move into the low to mid 20% range over the next 2-3 years, driven by revenue mix and improving recurring revenue margins.

Figure 3: Symbotic Gross Profit Margins (source: Created by author using data from Symbotic)

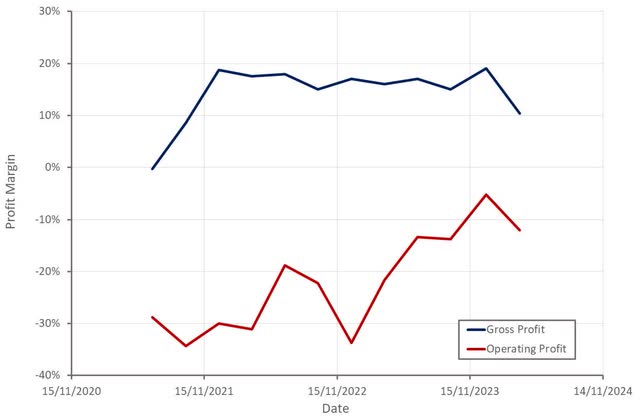

Symbotic’s operating margin declined in the first quarter, driven largely by the drop in gross margin. Stock-based compensation was elevated though due to January vesting. Margins should bounce back in the third quarter, with the absence of restructuring charges and normalized SBC costs, bringing Symbotic close to breakeven. Losses aren’t particularly at this point in time though, due to Symbotic’s generally positive cash flows from operating activities and 951 million USD of cash, cash equivalents and marketable securities.

Figure 4: Symbotic Profit Margins (source: Created by author using data from Symbotic)

Conclusion

Symbotic’s business continues to perform well, with growth remaining robust and margins and cash flows generally improving. The introduction of breakpack and perishable solutions, along with the scale up of GreenBox, should also ensure fundamentals remain strong in the near-term.

There is cause for concern, though. Outside of GreenBox, Symbotic’s backlog has been stagnant for several years and the company’s revenue growth is moderating. A softening macro environment also creates the risk of customers pulling back on warehouse investments.

Independent of this, Symbotic’s valuation remains difficult to understand. Symbotic’s EV/S ratio is still close to 10, which is extremely high given the company’s relatively low gross margins and the non-recurring nature of most of its revenue. From a technical perspective, if Symbotic’s share price doesn’t hold near current levels, there may be little support until the low 20s or even high teens.

Read the full article here