I believe it is one of my most important articles, as we could be on the verge of a major shift that could potentially have a major impact on future returns.

The S&P 500’s recent gains have been heavily concentrated in a few stocks, raising diversification concerns.

There is valid skepticism about the sustainability of these developments.

Future earnings growth is expected to shift towards sectors like health care, materials, consumer discretionaries, and industrials.

Going forward, stock picking could become more attractive, potentially with elevated chances of outperforming the market.

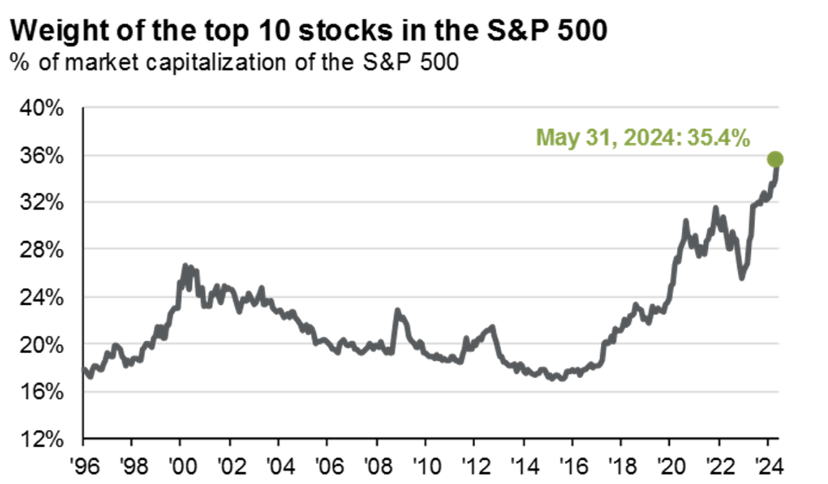

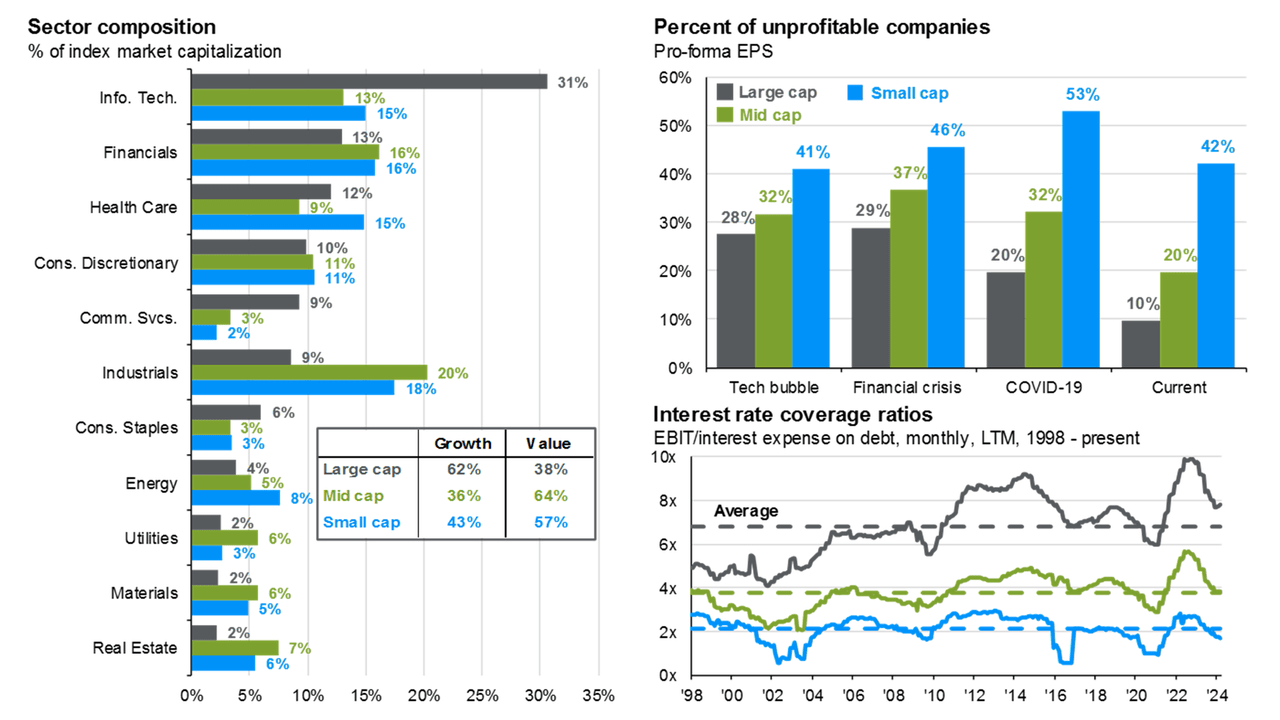

As we can see below, the biggest ten S&P 500 stocks accounted for 35.4% of its weighting going into this month. That number didn’t even make it above 28% during the Dot-com bubble.

JPMorgan

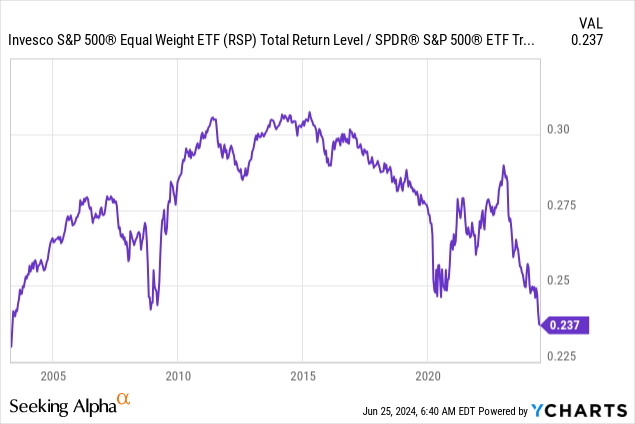

Moreover, I wrote that I expected a bottom in the ratio between the equal-weight S&P 500 (RSP) and the market-weighted S&P 500, which would unlock a lot of potential for stock-picking.

Data by YCharts

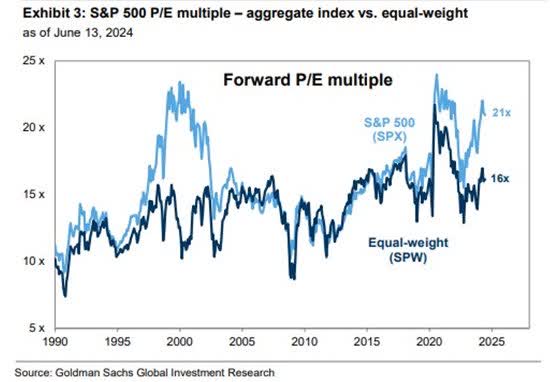

A broadening in market strength could be supported by the fact that the S&P 500 has a forward P/E of 21x, similar to what we saw during the Dot-com bubble and the QE-fueled pandemic rally.

Goldman Sachs

The equal-weighted S&P 500, however, has a 16x multiple, which is close to its long-term median.

With that said, stock picking is not easy. There is a good reason why a lot of money has found its way into “growth” stocks.

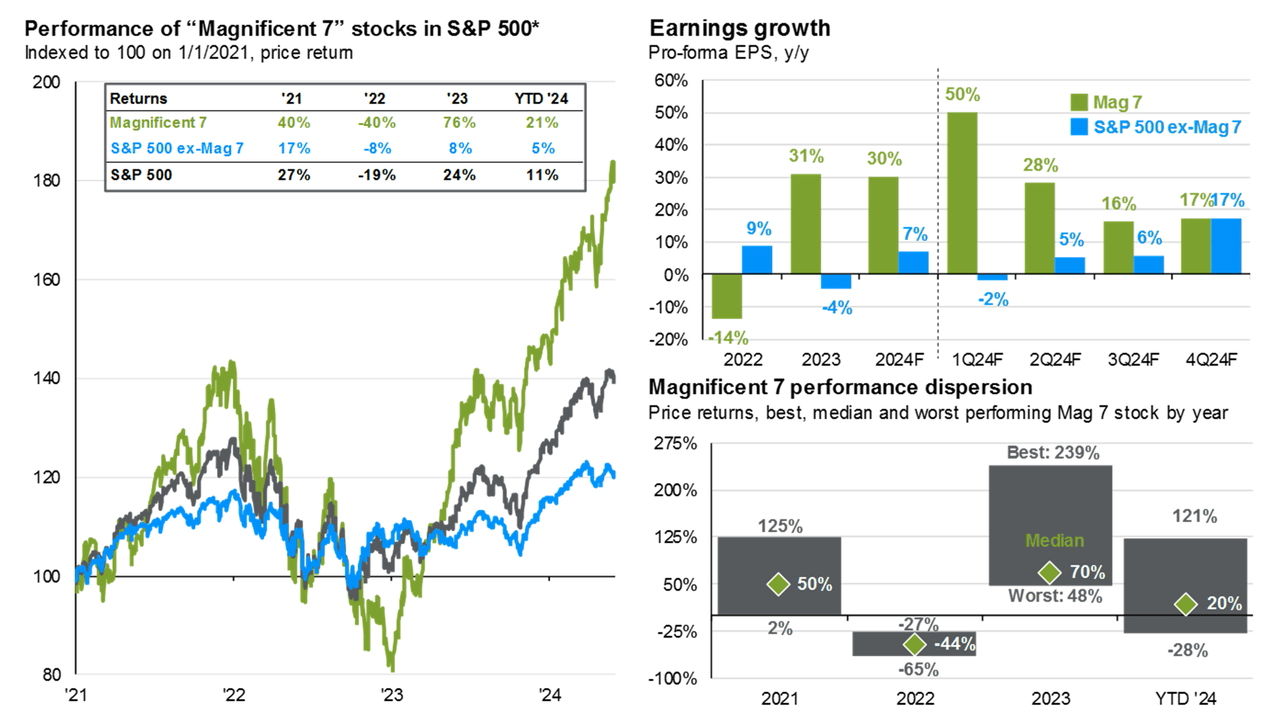

For starters, growth expectations were simply higher. In both 2023 and 2024, the Magnificent-7 stocks are expected to grow EPS by 31% and 30%, respectively.

JPMorgan

To put it bluntly, since mid-2023, artificial intelligence has, more or less, become the only game in town.

It also needs to be said that in light of elevated inflation and interest rates, investors found safety in the attractive balance sheets of large companies.

As we can see below:

Just 10% of large-cap companies are unprofitable. That number was 20% during the pandemic and almost 30% during the Great Financial Crisis.

Among small-cap companies, more than 40% of companies are unprofitable. This is similar to prior recessions. The difference is that, right now, we are not in a recession. How many will be unprofitable once a recession hits?

Small-cap companies have an EBIT/interest expenses ratio of less than 2x, which could mean financial trouble for some if rates remain elevated and growth comes down.

Large-cap companies have elevated interest coverage ratios.

JPMorgan

Hence, I generally make the case for most conservative investors to stay away from small caps that appear cheap. Some stocks are cheap for the same reason certain consumer goods are cheap: the quality is poor.

So, although I’m making the case that a potential broadening in market strength benefits stock picking, by no means am I suggesting investors jump into low-quality small caps or anything that has been beaten down.

With all of this in mind, in this article, I present three stocks that I believe are highly attractive. They all come with consistent dividend growth, they are all at least 40% undervalued (that’s what my title is based on), and all have impressive business models.

Now, let’s dive in!

Canadian Natural Resources (CNQ) – The Special-Dividends Oil Giant

Initially, I wanted to go with Nutrien (NTR), which is one of the world’s biggest fertilizer producers. However, I decided to go with energy instead of agriculture, as I’m a bit more bullish on energy than agriculture.

I also wanted to avoid going with two Canadian stocks in this article.

Canadian Natural Resources has been a recurring star in my articles since I bought it a while ago, as I believe it is hard to beat the value Canada’s largest oil and gas producer brings to the table.

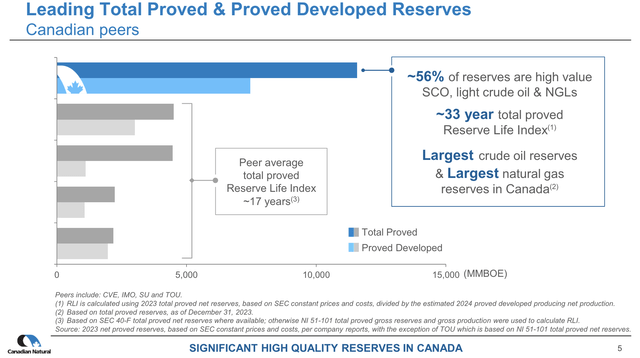

Not only does CNQ come with the largest oil and gas reserves in Canada, but it also benefits from the fact that more than half of these reserves are high-margin oil and natural gas liquids.

Canadian Natural Resources

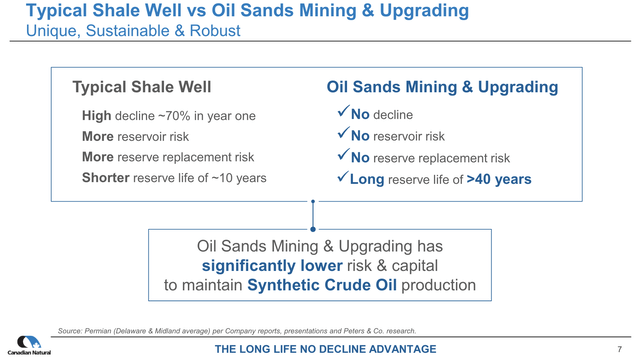

Even better, most of these operations are in Canada’s oil sands, which have no decline, reservoir, or replacement risks. While they are much more polluting than U.S. shale, they also have longer reserve lives, allowing the company to boost output at a time when U.S. shale producers are slowly running out of Tier 1 drilling locations.

Canadian Natural Resources

These oil sand operations account for roughly a third of its total production. Conventional production accounts for 42% of its output, with the remaining productions coming from Pelican & thermal assets with a subdued decline rate of 13%.

As a result, the company’s total decline rate is just 11%, which bodes well for its operating costs, as its oil sand operations are breakeven in the $20-$35 per barrel range.

Of its production, 73% consists of high-margin oil and natural gas liquids, which sets it apart from producers with a gas-focused profile.

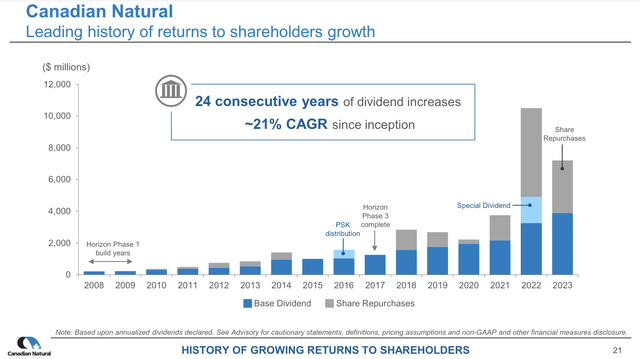

Another thing that sets it apart is the fact that after hitting its net debt target of C$9.9 billion at the end of 2023, it now distributes 100% of its free cash flow to shareholders.

Even before the company made this pledge, it was a reliable source of income. In fact, it has hiked its dividend for 24 consecutive years with a CAGR of 21%.

Canadian Natural Resources

Moreover, once the oil bull case got stronger, the company boosted returns, using special dividends and buybacks.

Currently trading at C$48.30 in Toronto (it is also listed in New York), CNQ shares have a base yield of 4.1%.

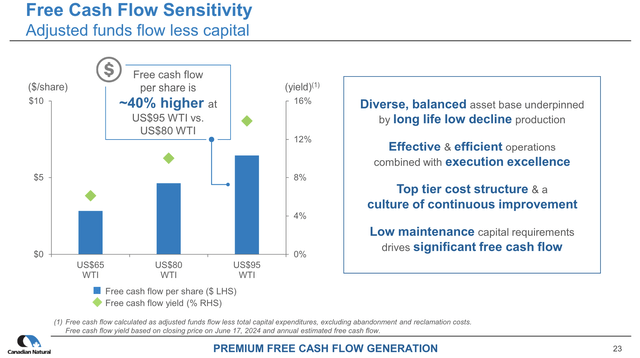

To show you how much potential the company has, we can use the overview below.

At $80 WTI, where oil is currently trading, the company has the potential to generate close to $5 in per-share cash flow. This implies a 10% free cash flow yield! In other words, if oil stays at $80, the company can distribute 10% of its market cap to shareholders.

At $95 WTI, that number rises to roughly $7 – more than 14% of its market cap.

Canadian Natural Resources

As I’m very bullish on both oil and gas, I expect CNQ to be one of the best stocks for the years ahead, making it one of my ultra-high-conviction plays.

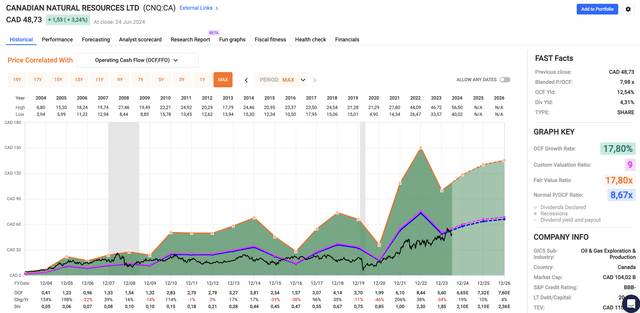

Even excluding my bullish view on oil, the company is attractively valued, as it trades at less than 8x operating cash flow.

Based on FactSet data in the chart below, analysts see a path to C$7.60 in per-share operating cash flow by 2026. When applying a 9x multiple, we are dealing with a fair stock price of C$68 in Toronto. That’s roughly 40% above the current price.

FAST Graphs

The same also applies to New York-listed shares.

It’s also why I keep buying CNQ stock on any correction.

Lamb Weston Holdings (LW) – Because Everyone Loves French Fries

If you have ever ordered french fries at McDonald’s (MCD), you probably had Lamb Weston fries, as it’s the main supplier of its fries.

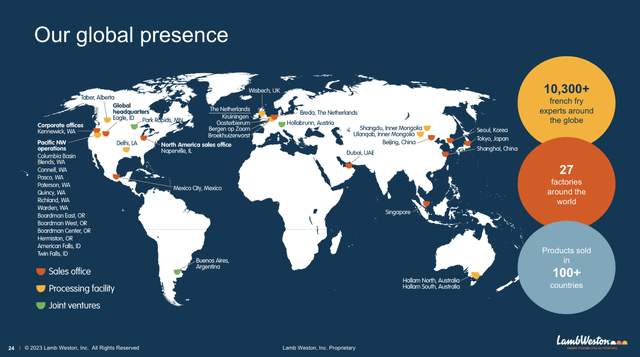

Serving more than 100 nations around the globe, the company generated 13% of its sales from McDonald’s last year.

Lamb Weston Holdings

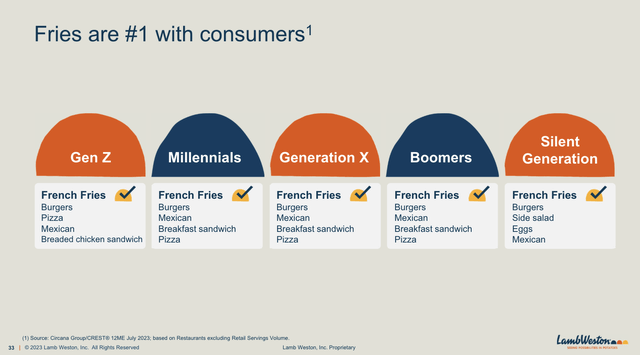

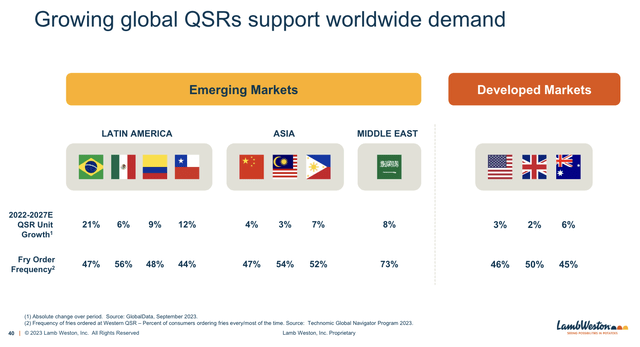

It also benefits from the fact that every generation prefers french fries. As we can see below, french fries are the number one food of Gen Z, the Silent Generation, and everyone in between.

Lamb Weston Holdings

Even highly saturated (pun intended) markets like the United States, the United Kingdom, and Australia are expected to maintain 2-6% annual volume growth, with additional tailwinds from outperforming growth in LATAM and Asian markets.

Lamb Weston Holdings

It also has a keen focus on innovation, with multiple places around the world where it develops new potato-based products for its customers. This includes extra crunchy fries, new tots, and whatnot.

While this may sound like something minor, I got my inbox flooded with comments from restaurant owners and other customers, who all told me how satisfied they were with LW products when I wrote my first in-depth article on the company.

It also has a focus on shareholders.

This is what I wrote in my April article:

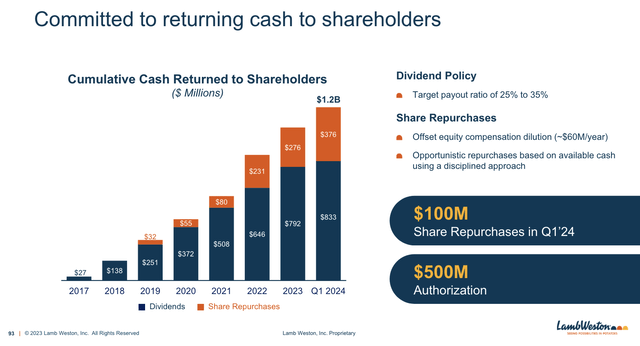

Shortly after becoming independent in 2017, the company spent $27 million on dividends. Since then, and as of 1Q24, that number has grown to a cumulative $833 million. On top of that, the company has spent close to $380 million on buybacks.

Lamb Weston Holdings

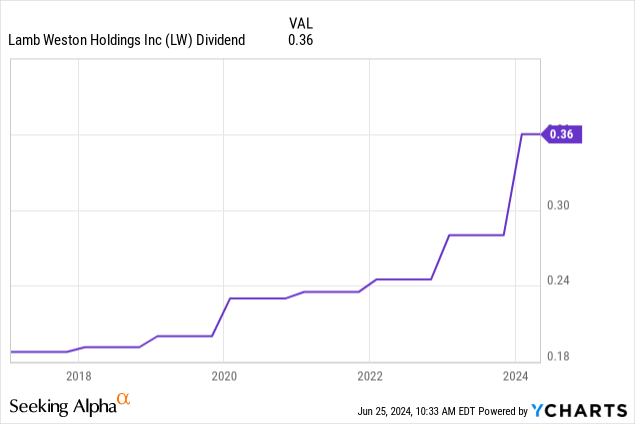

After hiking its dividend by almost 29% on December 4, the company pays $0.36 per share in quarterly dividends. This translates to a yield of 1.7%.

This dividend comes with a 26% payout ratio, which is close to the lower bound of its 25% to 35% payout ratio.

Data by YCharts

This means that future growth is more than likely indicating elevated dividend growth – and a favorable valuation.

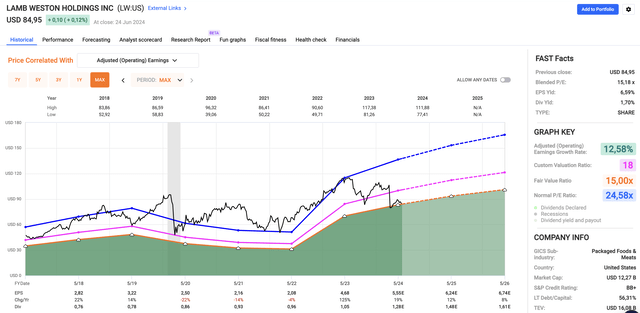

Currently, LW trades at a blended P/E ratio of just 15.2x. This is the result of a 25% share price decline, fueled by poor 1Q24 results.

In the first quarter, the company struggled with the implementation of a new enterprise resource planning system that massively disrupted operations. It also saw some demand weakness, as inflation is putting pressure on the consumer.

However, analysts expect a steep recovery, with 19% EPS growth in 2024, potentially followed by 12% and 8% growth in 2025 and 2026, respectively.

As such, even an 18x EPS multiple would imply a fair stock price of $121, 42% above the current price.

FAST Graphs

Although I do not currently own it, LW is part of multiple family accounts.

Cheniere Energy (LNG) – A Special Energy Company

Just like the first pick, the third pick of this article is also a member of the energy sector. However, it’s a special energy stock, as it does not produce oil or gas. Cheniere Energy turns natural gas into liquified natural gas, which allows foreign nations to buy American natural gas.

On My 8, I wrote an in-depth article on the company titled “Cheniere Energy Is About To Become A Wide-Moat Dividend Growth Powerhouse.”

Since then, shares have risen by 7%, beating the 5% return of the S&P 500 by a small margin.

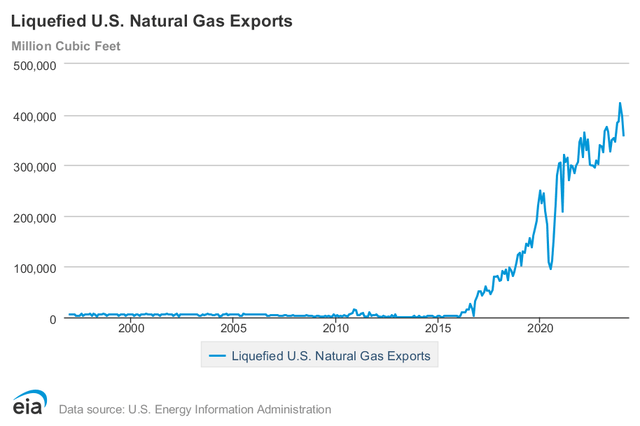

Unlike smaller startups, Cheniere was the first company in the United States with meaningful LNG production capacity, turning the United States into the largest exporter of LNG.

Energy Information Administration

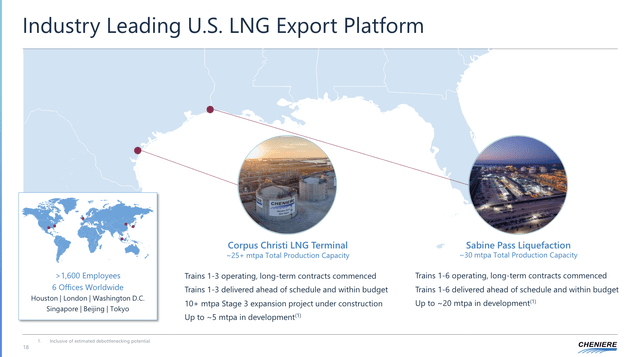

Going into this year, the company was the second-largest LNG producer, with a capacity of 45 million metric tons per year from the Sabine Pass and Corpus Christi terminals on the Gulf Coast.

Cheniere Energy

These facilities sell to a wide range of nations with highly favorable contracts, protecting the company against rising input costs while allowing it to capture potentially higher LNG prices.

We have contracted substantially all of our anticipated production capacity under SPAs, in which our customers are generally required to pay a fixed fee with respect to the contracted volumes irrespective of their election to cancel or suspend deliveries of LNG cargoes, and under IPM agreements, in which the gas producer sells natural gas to us on a global LNG or natural gas index price, less a fixed liquefaction fee, shipping and other costs. The SPAs also have a variable fee component, which is generally structured to cover the cost of natural gas purchases, transportation and liquefaction fuel consumed to produce LNG. – Cheniere 2023 10-K

Thanks to these operations, the company is able to invest in growth, reduce debt, grow its dividend, and buy back stock.

Currently yielding 1.1%, the company is hiking its dividend by 10% per year until it finishes its Corpus Christi Stage 3 expansion in the mid-2020s. After that, dividend growth will accelerate, supported by aggressive buybacks.

Over the past three years, Cheniere has bought back 10% of its shares.

Even better, by 2026, the company is expected to generate roughly $3.4 billion in free cash flow, more than 9% of its market cap.

Again, this makes Cheniere a highly unique company capable of rapid infrastructure growth supported by internal funding that comes with the ability to handsomely reward its investors through buybacks and consistent dividend growth.

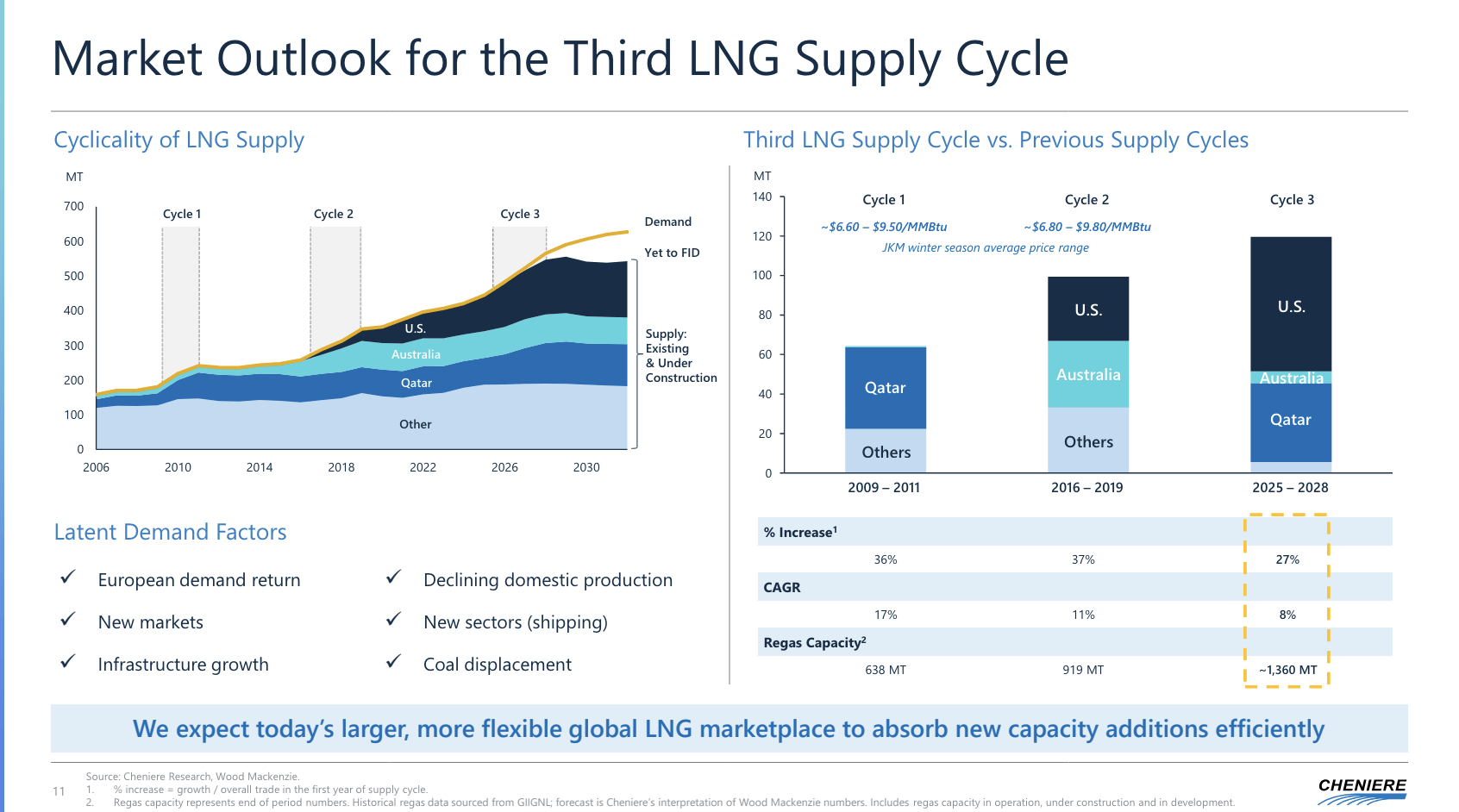

It also benefits from a highly favorable outlook, as it expects the third LNG cycle to be the biggest ever, with enough demand to absorb all new capacity.

In fact, it expects demand to increasingly outpace supply in the 2030s.

Cheniere Energy

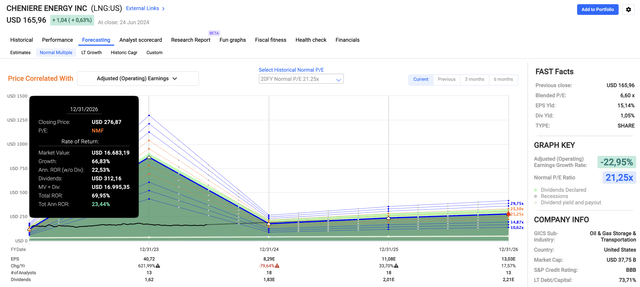

Valuation-wise, I may be one of the biggest bulls, as I give the stock a fair price target of $277, which is almost 70% above the current price.

Using the data below, this wide-moat company is expected to grow its EPS by 34% next year, potentially followed by 18% growth in 2026. After that, I expect consistent double-digit EPS growth, especially once it is able to accelerate buybacks in the mid-2020s.

When adding a 21.3x multiple to these numbers, we arrive at the $277 stock price target.

FAST Graphs

As such, Cheniere absolutely deserves a spot in this article, as I think investors are massively underpaying for what this company could be worth a few years from now.

Takeaway

With the S&P 500’s gains clustered in a few big names, the potential for diversification through selective investments is significant.

I’m particularly optimistic about sectors poised for future growth, like healthcare, energy, materials, and industrials.

My top three picks – Canadian Natural Resources, Lamb Weston, and Cheniere Energy – are all undervalued with strong dividends and fantastic business models.

They offer a unique mix of stability and growth potential, making them standout choices in a market that demands careful, strategic stock selection.