As any gardener can attest, plants need three basic nutrients to flourish: Nitrogen, phosphate, and potassium (potash). Illinois-based CF Industries Holdings, Inc. (NYSE:CF) is the largest producer of nitrogen fertilizer in North America.

Nitrogen fertilizers are produced by mixing nitrogen present in the air – the atmosphere is about 78% nitrogen – with hydrogen present in methane (also known as natural gas with the chemical symbol CH4) under pressure and in the presence of a catalyst.

The basic building block of most nitrogen fertilizers is ammonia, which consists of a nitrogen atom bonded to three hydrogen atoms. Ammonia can also be processed further to produce common nitrogen fertilizer products such as granular urea and urea ammonium nitrate (UAN).

In 2023, CF produced a total of 19.13 million tons of total nitrogen products including about 3.55 million short tons of ammonia, 4.57 million tons of granular urea, and 7.24 million tons of UAN. The company has six nitrogen production facilities in the US, including its largest complex located in Louisiana (near the Mississippi River and New Orleans).

CF also has two facilities in Canada and one smaller plant in the UK.

As I’ll explain in this article, CF enjoys a durable cost advantage over most of its global peers, because of low US natural gas prices relative to other regions of the world, including Europe and Asia. Since gas is the key input cost to produce nitrogen fertilizer products, CF can generate profits and free cash flow at much lower fertilizer prices than most of its global peers.

CF also benefits due to its location – fertilizers are bulky products that can be expensive to transport. However, CF’s operations are located close to the US Midwest, one of the world’s most important agricultural production regions for key crops like corn, soybeans, and wheat.

CF has also taken steps to reduce net debt in recent years and to return capital to shareholders via dividends and share buybacks.

However, while CF is a high-quality, well-managed company, I see limited upside for the stock this year. That’s because there are two key catalysts that have historically been able to generate significant upside for CF shares over the intermediate term.

Neither currently represents a tailwind for the stock.

Let’s start with this:

Catalyst #1: It’s all about the Corn

The three most important field crops in the US are corn, soybeans, and wheat:

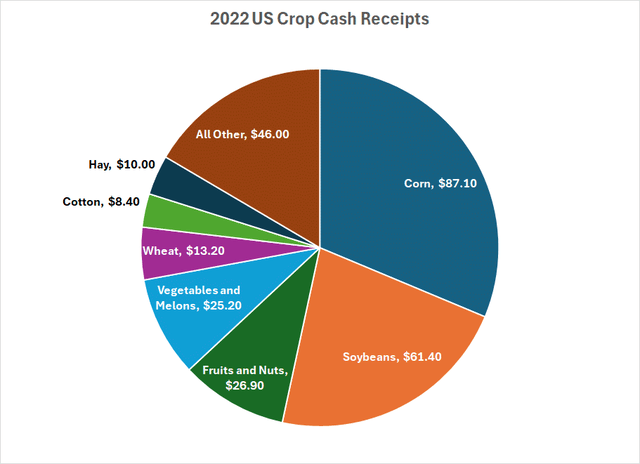

2022 US Crop Cash Receipts (US Department of Agriculture (USDA))

The US Department of Agriculture (USDA) Economic Research Service provides statistics on total farm incomes attributed to individual crops. The figures in my pie chart above are in billions of dollars for 2022, the last full year for which we have data.

Of the $278.2 billion in total US farm cash receipts in 2022, corn accounted for $87.1 billion (31.3%) and soybeans $61.4 billion (22.1%) with wheat a distant third at $13.2 billion (4.8%).

Corn is the most nitrogen-intensive major crop in the US.

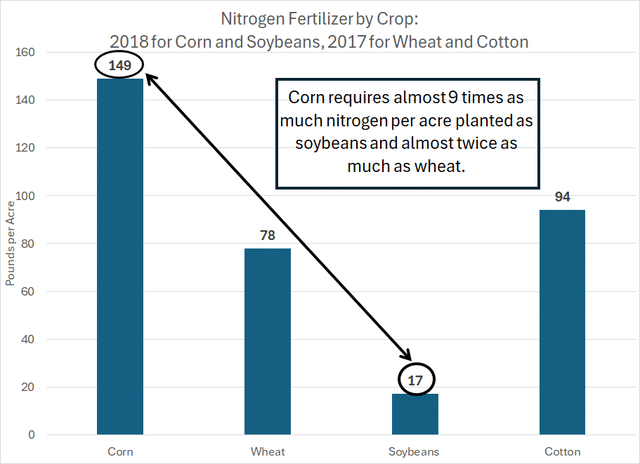

Here’s a look at USDA estimates for nitrogen consumption per acre broken down by crop:

Nitrogen Requirements by Crop (USDA)

As you can see, in 2018 corn required almost nine times as much nitrogen fertilizer per planted acre compared to soybeans and almost twice as much as wheat.

In short, if you’re trying to determine the likely trend of nitrogen fertilizer demand, it’s important to monitor the trend in soybean and corn acres planted each year. If farmers choose to plant more corn acres that will have a positive impact on nitrogen demand.

Unfortunately for CF, that’s just not the case in 2024:

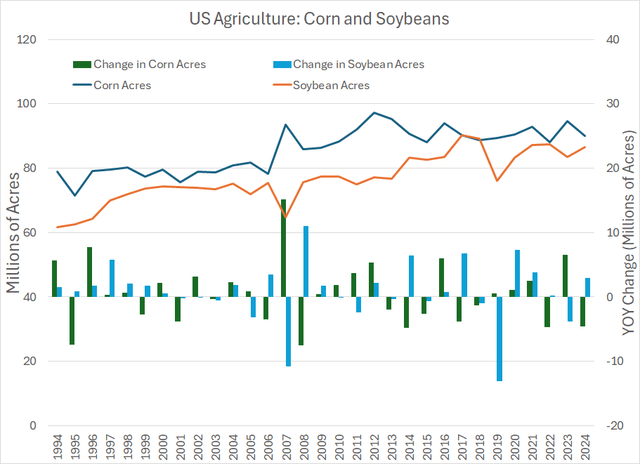

US Corn and Soybean Acres by Year (USDA)

This chart shows data on total planted acres for corn (blue line) and soybeans (orange line) since 1994 from the USDA Natural Agricultural Statistics Service (NASS). The blue bars at the bottom of the chart show the year-over-year change in acres planted for both commodities.

Simply put, when farmers decide to plant more corn acres, that’s bullish for nitrogen demand and, therefore, for CF:

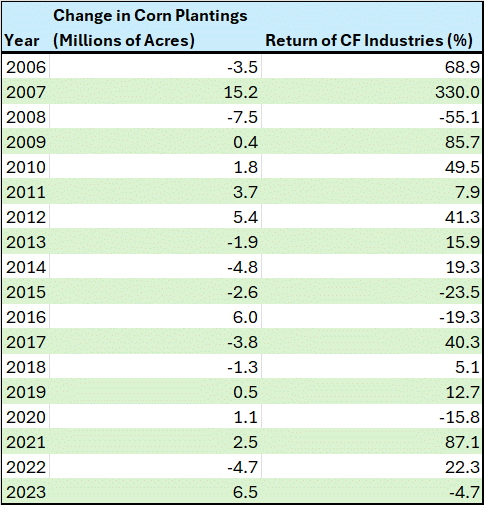

A table showing the US change in corn plantings and returns in CF stock. (USDA, Bloomberg)

This simple table shows the year-over-year change in corn acres planted, the same data from USDA I presented earlier, and the annual total return from CF in the corresponding year.

A quick glance here shows that when corn acres planted see a significant rise, CF shares tend to perform well. For example, in 2007 US corn acres planted surged by more than 15 million and CF shares jumped more than 330% (capital gains and dividends) according to Bloomberg.

In the years 2010-2012, total corn acres saw significant gains each year and CF stock also performed well, gaining 49.5% in 2010, 7.9% in 2011, and 41.3% in 2012.

There are exceptions.

In financial markets, correlations are never perfect, and it’s tough to assess a company’s prospects based solely on a single fundamental trend. In 2016, for example, US corn acres planted rebounded significantly after three straight years of declines; yet, CF shares fell almost 20%. And in 2022, US corn acres fell by 4.7 million and CF still managed a solid 22.3% return.

However, a simple mathematical calculation of the correlation between the annual change in corn acres planted and CF stock over the 18 years covered by my chart shows a positive correlation of 63.9%.

And that’s bad news for CF this year.

According to the USDA’s Prospective Plantings Survey released at the end of March, US farmers intend to plant just over 90 million acres of corn in 2024, about 5% lower than in 2023. Meanwhile, farmers intended to increase soybean acres planted by almost 3 million acres to 86.51 million. That’s a headwind for nitrogen demand and CF stock this year.

It’s not hard to see what’s driving this shift in planted acres favoring soybeans over corn:

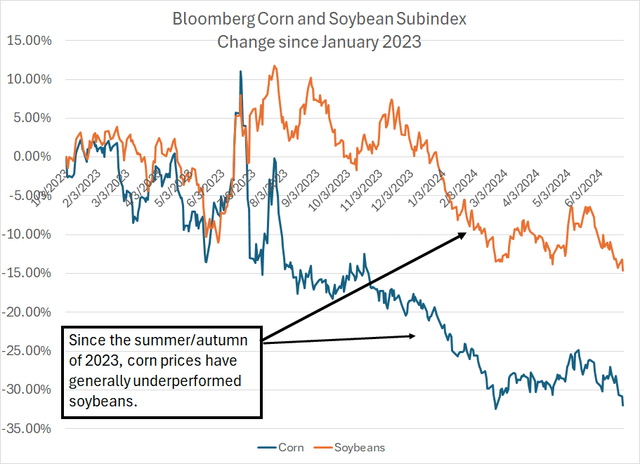

Corn and Soybean Prices (Bloomberg)

Bloomberg publishes corn and soybean subindexes that track commodity futures prices for these two key agricultural commodities over time. This chart shows the total change in the subindex for corn as a blue line and for soybeans as an orange line since January 3, 2023.

And, as you can see, while prices for both commodities have been weak, corn has meaningfully underperformed soybeans, particularly since the late summer and early autumn months last year.

Simply put, strength in soybean prices relative to corn will tend to incentivize farmers to maximize their production of the former relative to the latter this year. That’s a headwind for nitrogen fertilizer demand and CF.

A second key catalyst to watch is on the cost side.

Catalyst #2: US Vs. Global Natural Gas Prices

As I’ve explained, CF owns six nitrogen manufacturing facilities in the US and two in Canada which primarily use natural gas sourced from North America as feedstock. According to CF’s latest 10-K annual report natural gas accounted for 40% of the company’s total production costs last year, its single most important cost center.

This is a major, durable competitive advantage for CF relative to its peers in other regions of the world like Asia and Europe because thanks to soaring production from North American shale fields, US and Canadian gas prices have consistently been low relative to overseas benchmarks:

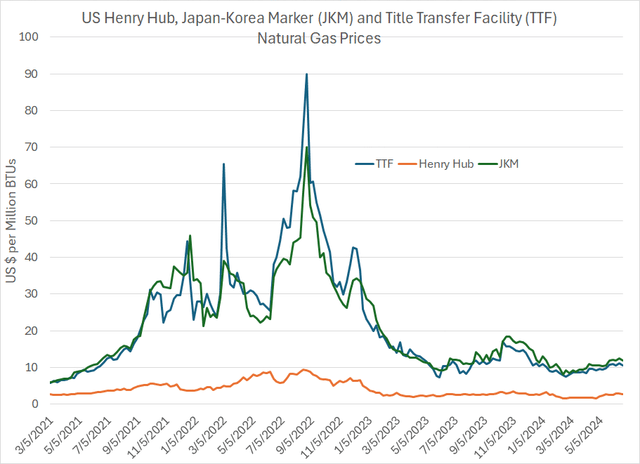

US, European and Asian Natural Gas Prices (Bloomberg)

This chart shows three key global benchmarks for natural gas prices since March 2021, all rebased in terms of US dollars per million British Thermal Units (BTUs), the US pricing standard.

The orange line is the US front-month natural gas futures prices for delivery to Henry Hub on the Louisiana Gulf Coast. The blue line represents the price of natural gas for delivery to the Title Transfer Facility (TTF) in the Netherlands (Europe). Finally, the green line is the Japan-Korea Marker (JKM), an Asian benchmark for natural gas prices.

As you can see, the two non-US benchmarks – TTF and JKM – follow similar trends over time. That’s because, the marginal or “swing” source of natural gas in both markets is liquefied natural gas (LNG), which represents supercooled natural gas loaded onto a specialized tanker ship for transport globally.

So, if prices are significantly higher in Europe (TTF) than in Asia (JKM), incremental LNG cargoes are likely to favor Europe to take advantage of higher prices. Thus, price trends in JKM and TTF are correlated, because both Asia and Europe need to attract LNG cargoes over time to meet demand.

If TTF were to exceed JKM by a large margin, or for a prolonged period of time, it would tend to result in an unsustainable drop in the Asian supply of gas.

In contrast, according to the Energy Information Administration (EIA), the US produced some 37.9 trillion cubic feet of dry natural gas in 2023 and consumed just over 32.5 tcf. In other words, the US is a net exporter of gas in the form of both pipeline exports to regional markets like Mexico and to Europe and Asia in the form of LNG. Thus, the US doesn’t need to compete for LNG cargoes and US natural gas prices are generally lower than most global markets and have less correlation to global benchmarks like TTF and JKM.

This is a major advantage for CF as it’s able to source cheaper US natural gas feedstock as a raw material for its nitrogen production plants.

Take a look:

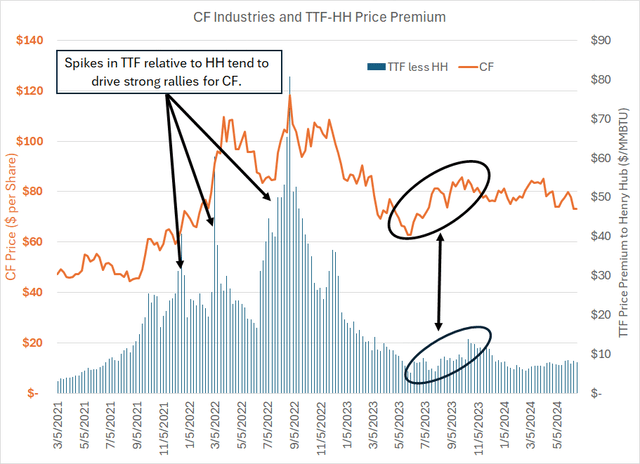

CF and US vs. Europe Gas Prices (Bloomberg)

This chart shows the Price of TTF (European) gas less the price of Henry Hub (US) natural gas on a weekly basis since March 2021 as bars along the bottom of this chart. The orange line represents the weekly closing price of CF stock over the same period.

As you can see, spikes in EU gas prices relative to the US back in 2021-22 tended to lead to commensurate spikes in the price of CF. That makes fundamental sense since high European natural gas feedstock prices rendered CF’s low-cost US nitrogen production facilities more valuable and profitable.

However, even shorter-term and more placid trends in relative US-EU gas prices can lead to periods of strong CF returns. An example, circled in my chart above, is the rally in TTF relative to Henry Hub between late July and mid-October 2023. Over a similar time frame – from the July lows to the October 2023 highs – CF shares rallied from under $70 to over $85 per share.

Over the long haul, plentiful supply and the lower cost of natural gas feedstock in the US represents a powerful tailwind for CF. US natural gas production is already the highest in the world and is growing at an impressive clip:

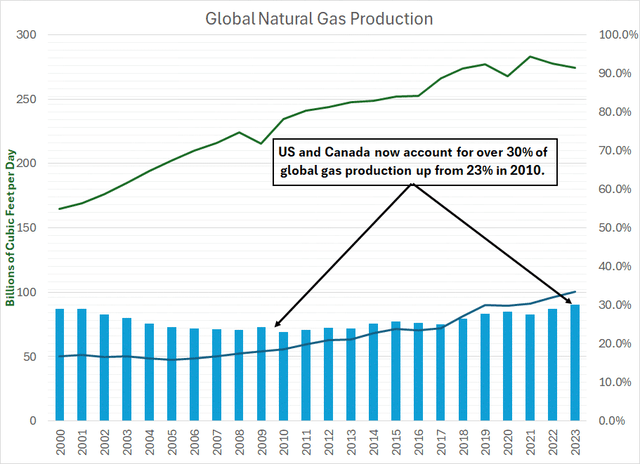

Global and US Gas Production (Energy Institute Statistical Review of World Energy 2024)

This chart shows total world gas production excluding the US and Canada as a green line and total US production as a blue line. The blue bars show US and Canadian combined production as a percentage of the global total. The data is from the Energy Institute’s latest Statistical Review of World Energy covering data through 2023.

As you can see, outside the US and Canada, global gas production has roughly flatlined since 2017. And, between 2010 and 2023, the US and Canadian combined share of global gas production jumped from 23% to over 30% of the global total.

I’ve written about US natural gas production trends and prices extensively here on Seeking Alpha, including in my May 8, 2024 piece covering the largest independent US gas producer, EQT Corporation (EQT), “EQT: Cementing Position as Low-Cost Gas Producer.”

EQT produces natural gas from the Marcellus Shale field in Appalachia, the largest gas shale field in the US. EQT’s all-in cash production costs including capital expenditures (CAPEX) are around $2.30/MMBtu right now and management is targeting a sub-$2/MMBtu gas cost breakeven over the next few years.

The proximity of low-cost domestic supply is a durable competitive advantage for CF and means the company can generate positive free cash flow even at relatively low prices for key nitrogen fertilizer products like Urea.

However, the scale of this advantage changes over time and these shorter-term shifts in relative natural gas prices between the US, Europe, and Asia are what tend to drive price trends in CF.

Simply put, as you can see in my chart above, US gas prices are still much lower than in Europe or Asia however Henry Hub is currently priced at a roughly $8/MMBtu discount to TTF right now compared to nearly $14/MMBtu in mid-October of last year and over $80/MMBtu back in the summer of 2022.

And right now, the European gas market looks well-supplied:

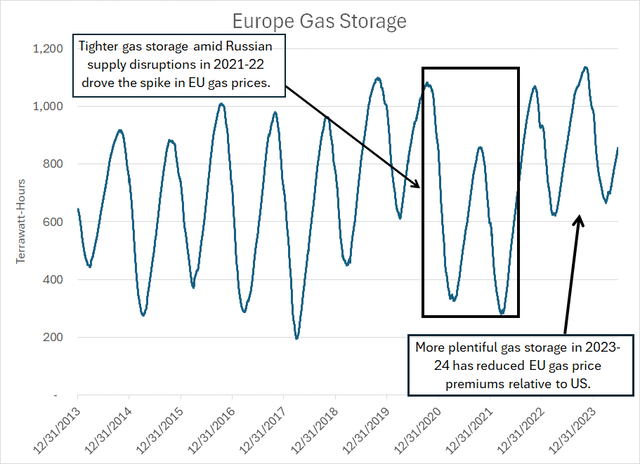

European Gas Storage (Bloomberg, GIE)

This chart, sourced from Bloomberg and Gas Infrastructure Europe (GIE), shows total European gas storage since the end of 2013.

As you can see, there’s a seasonal trend over time. Gas storage across Europe tends to bottom out seasonally in March or April as the winter heating season comes to an end and peaks in October-November just ahead of the heating season.

However, in 2021-22 disruptions to the Russian gas supply helped tighten the EU gas market. This resulted in lower seasonal highs and lower seasonal lows in storage, which helped to drive the surge in EU gas prices relative to the US that I outlined earlier.

Since the end of 2022, however, Europe’s storage outlook has improved significantly. Indeed, by mid-November 2023, just ahead of the start of winter heating demand, European gas storage reached its highest seasonal peak in at least a decade. Thanks to a relatively benign winter in 2023-24, the seasonal low for gas storage this year was also higher than any year covered in my chart.

Longer-term, there’s a significant risk of further price spikes in European gas prices.

Europe’s gas market benefited from a warmer-than-average winter in 2023-24 as well as higher-than-average wind velocities, which boosted output from wind turbines and helped reduce gas demand. However, a colder winter and/or poorer wind generation trends could quickly tighten Europe’s gas market and send prices higher.

In addition, European heavy industry and manufacturing facilities are a major driver of regional gas demand. For example, according to preliminary data from the German government, household users accounted for only 41% of German consumption last year compared to 59% for industrial users.

Growth in European manufacturing industries has been sluggish over the past two years:

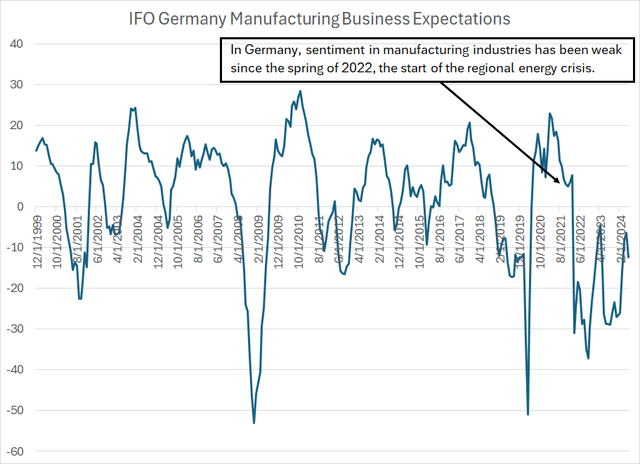

German Manufacturing Business Expectations (Bloomberg)

The IFO Institute conducts a monthly survey of approximately 9,000 German manufacturing businesses around the middle of each month, producing the diffusion index I’ve plotted on this chart. Readings above 0 suggest improving business expectations for manufacturing industries and negative readings are the opposite.

As you can see, German manufacturing business expectations took a dive starting in the spring of 2022 following the disruption to Russian gas supplies and the spike in regional energy prices I outlined earlier. Manufacturing activity has been weak since that time, with this index never climbing back over the zero line that divides expansion from contraction.

So, weakness in German – and EU-wide — gas demand is partly a consequence of weakness in industrial production and economic activity. That’s helped Europe build gas in storage.

Longer-term, Germany is the largest economy in the EU and manufacturing industries are key to the nation’s economic growth, labor market and consumer confidence. An improvement in the EU economy or manufacturing output would drive higher gas demand and tighten the supply-demand balance for this crucial commodity.

However, with natural gas storage ample, and European economic growth and manufacturing activity still weak, I don’t see much scope for a significant spike in TTF gas prices relative to Henry Hub until the start of European gas storage withdrawal season in November.

So, a spike in EU gas prices looks unlikely to power a rally in CF until late this year at the earliest.

Summary and Conclusion

CF nitrogen fertilizer production facilities sit at the low end of the global cost curve thanks to the company’s advantaged access to low-cost US natural gas.

That means CF is able to generate significant free cash flow even in periods like 2018-19 when nitrogen fertilizer prices are relatively low:

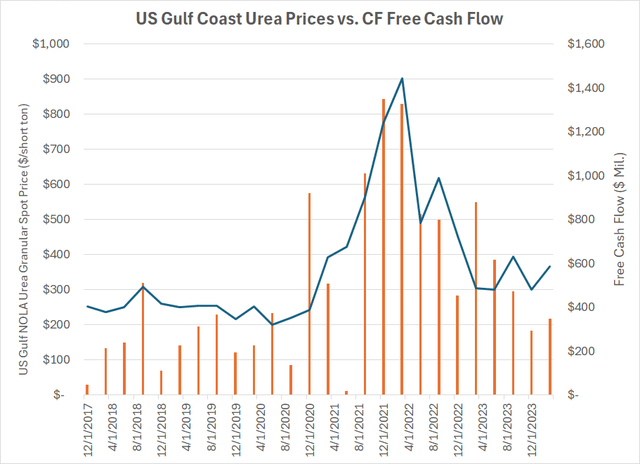

Urea Prices and Free Cash Flow (Bloomberg)

The blue line on my chart shows the cost of granular urea – a key nitrogen fertilizer – delivered to New Orleans, Louisiana from Q4 2017 through Q1 2024. The orange bars represent the quarterly free cash flow for CF in each quarter.

As you can see, CF has generated positive free cash flow in every quarter covered by my chart, even when urea prices were low such as in 2018-19.

When urea prices surged in 2021-2022, so did CF’s free cash flow. Meanwhile, many of its European and Asian competitors struggled with profitability as natural gas prices spiked in that era, and some were forced to suspend or close manufacturing capacity due to elevated gas prices.

Indeed, in CF’s Q1 2024 conference call back in March, management noted that it expects European and Asian utilization rates to remain below average going forward – European and Asian producers will produce at less than full capacity – because of unfavorable economics.

CF has also been a solid steward of capital, using its free cash flow to reduce its net debt from close to $4 billion at the end of 2019 to $1.2 billion as of yearend 2023 per Bloomberg. The company also returns capital to shareholders via a $0.50 quarterly dividend (about 2.7% annualized) and share buybacks; CF’s share count is down about 15.4% since the end of 2019.

However, CF looks fairly valued at the current price:

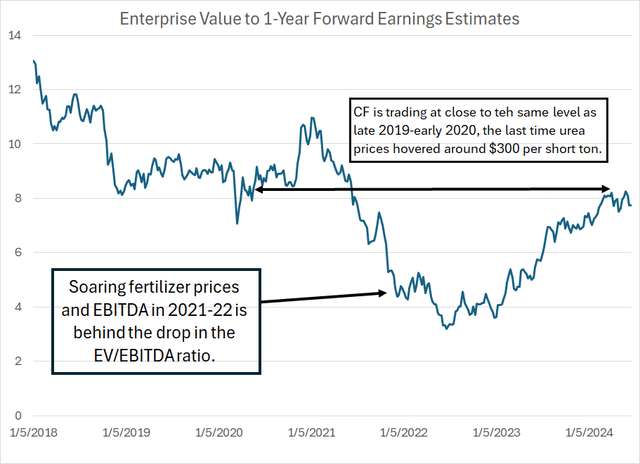

CF EV/EBITDA Valuations (Bloomberg)

This chart shows CF’s enterprise value to forward EBITDA multiple since early 2018.

Enterprise value represents the company’s market capitalization and net debt while EBITDA refers to earnings before interest, taxation, depreciation and amortization.

Today, CF trades at around 9x expected EBITDA over the next 12 months. That’s in line with the company’s valuation in late 2019 and early 2020 when nitrogen fertilizer prices were close to the current level. For example, as you can see in my chart above, urea fertilizer traded at just under $300 per short ton in late 2019 compared to the latest quote from Bloomberg at $299.50/ton.

In 2021-22 CF’s multiples fell, but for a good reason – earnings jumped in the strong fertilizer market at a pace that exceeded the gains in the stock price.

In my view, CF’s favorable cost structure, strong free cash flow generation ability and reasonable valuation limit the downside risk in the stock. However, without a push from either higher corn prices and accelerating nitrogen demand or a major jump in EU gas prices, the upside is limited.

Unfortunately, I don’t see either of those catalysts emerging until late this year at the earliest. CF rates a hold.

Read the full article here