Investment overview

I give a buy rating for Smith Douglas Homes Corp. (NYSE:SDHC) as the business benefits greatly from the current macro situation—high interest rates and home undersupply—in the US. As a home builder, SDHC has a clear demand tailwind for the foreseeable future, and given its differentiated operating model, I believe it will be able to continue capturing demand.

Business description

SDHC operates in the homebuilding industry, with a focus on the construction and sale of single-family detached and attached homes. SDHC currently operates in eight key states: Atlanta, Birmingham, Charlotte, Chattanooga, Huntsville, Nashville, Raleigh, and lastly, Houston (entered via the acquisition of Devon Street Homes). The company went public earlier this year, in January.

Current macro environment is the perfect storm for SDHC

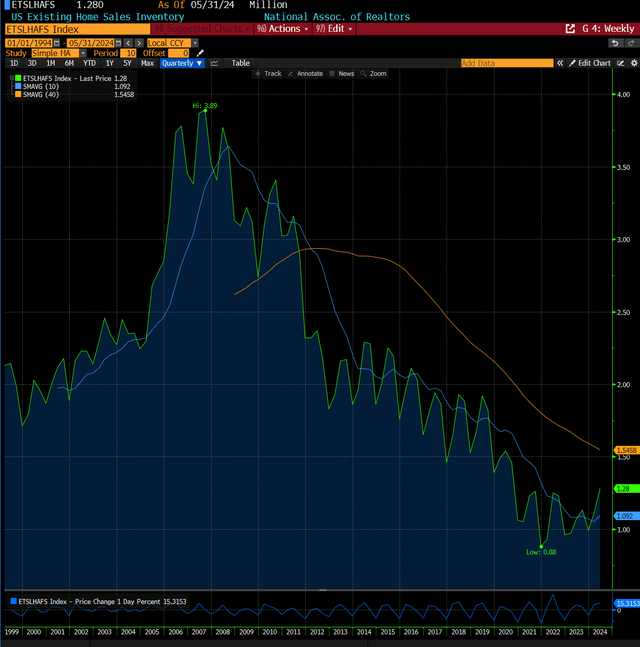

Bloomberg

The current high interest rate environment is a positive thing for SDHC. The surge in mortgage rates has caused many existing home owners to delay selling their homes as they do not want to refinance their mortgages at a much higher rate. According to a study report, nearly 60% of home owners have interest rates below 4%, which is a big difference from the current rate of >7%. This impact can be seen very apparently from the significant drop in existing home sales inventory, now at a near-all-time low. Unfortunately, I do think that rates are going to stay higher for longer, with potential further hikes as inflation has proven to be a lot stickier than expected. Just yesterday, a top Federal Reserve official mentioned that she would support more rate hikes if inflation stayed at the current level. As such, I see very little possibility of the mortgage rate falling in the near term. Even if it does, it is going to be at a slow pace, which means it is going to take some time before the mortgage rate goes below 4% (justifiable for the majority of existing homeowners to be willing to refinance their mortgage). Therefore, a large part of home supply is going to remain out of stock.

Michelle Bowman, one of the Fed’s governors and a voter on its rate-setting Federal Open Market Committee, said she remained “willing to raise” borrowing costs again “should progress on inflation stall or even reverse. FT

FRED

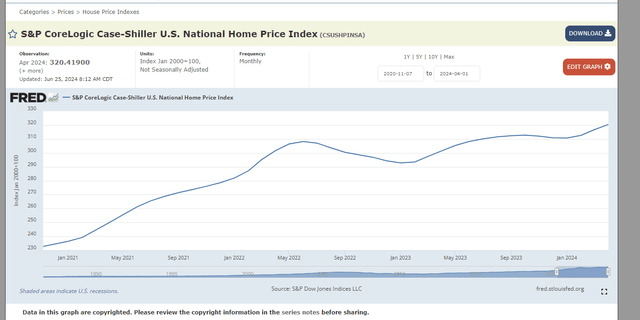

This is a massive tailwind for SDHC, as home buyers are only left with the choice to buy new homes. There are two layers of positive impact here. The first is that SDHC will see more demand. The second is that because demand for single homes outpaces the supply of homes, this has driven home prices up, which is positive for both revenue and earnings growth.

Differentiated business operating model

While this macro tailwind is positive for other home builders, I am more positive on SDHC because its differentiated operating model better positions itself to capture demand from consumers. SDHC offers the unique combination of a customized build- to-order [BTO] approach to the first-time home buyers with short build cycle times. There are a lot of reasons why homebuyers should choose SDHC over other builders. For one, the build time is much shorter (about 60 days according to 1Q24 earnings), which is much better than the industry standard of over 200 days. Secondly, most first-time builders only offer pre-built homes with limited customization options.

Bloomberg

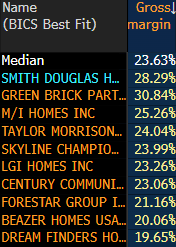

For SDHC, this enables them to achieve minimal cancellation rates (~10) and above-average gross margins, as customization enables SDHC to charge higher.

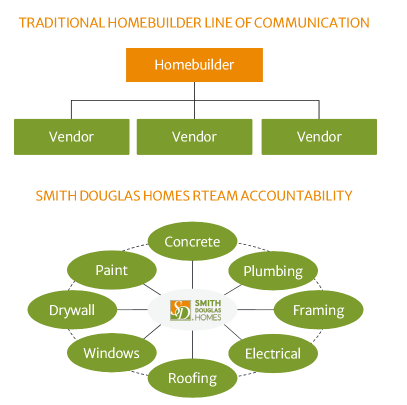

The key underlying cause that enables SDHC to achieve such feats is its two proprietary systems: (1) Rteam, a production process that allows for collaboration and coordination between and across the company and its trade partners; and (2) SMART Builder, a proprietary single database ERP system that is construction management-focused and manages SDHC’s entire homebuilding ecosystem. With less than 30 floor plans accounting for more than 90% of the company’s closings (as per S-1), the company has simplified its floor plan options, which helps manage the complexity of a customized BTO process.

SDHC

One of the biggest hurdles in construction is lack of communication, and this applies to the home building industry as well given there are multiple players in the ecosystem (different partners build different parts of the home). This is an issue that Rteam fixes because it improves production efficiency by streamlining communication among SDHC partners. Essentially, there is real-time communication between all parties involved, with an emphasis on optimizing productivity and the use of standardized processes to improve efficiency. Every trade partner is accountable for seeing a job through to completion before passing it on to the next trade partner, and no party may begin work on a project unless the team has verified that the specifications are accurate (this basically means more checkpoints, and this reduces the occurrence of major “mistakes” at the later part of the project which will be hard to amend).

The SMART Builder system is an ERP database that gives users access to data like project starts and closings, trade scheduling, job site prices, and lot-by-lot workstream status. This allows SDHC to schedule workflow efficiently, which improves utilization, and this translates to higher margins given the fixed cost nature of the labors involved.

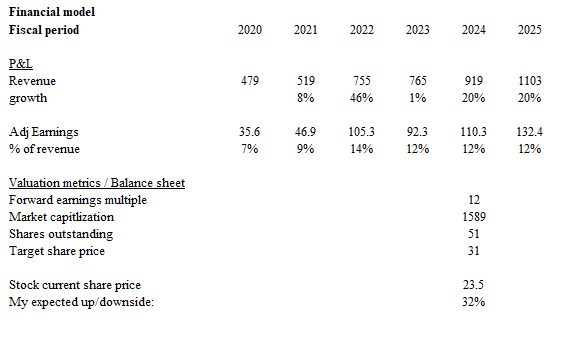

Valuation

May Investing Ideas

Based on my research and analysis, my expected target price for SDHC is $31.

- Revenue growth should continue to benefit from the current macro tailwinds, supported by SDHC’s differentiated business model. My growth target for FY24 is based on management FY24 guidance (units sold and pricing), and for FY25, I have extrapolated the same growth strength as I don’t see the macro situation resolving anytime soon.

- I kept the earnings margin flat for the next two years. I acknowledge that pre-covid SDHC margins are at high single-digits, but because of the current macro situation where demand outpaces supply, I believe SDHC can sustain these elevated margins for the next two years.

- SDHC is currently trading at 12x forward PE, which is near its all-time low. While I don’t think this makes sense given the growth outlook, I believe the upside is attractive enough even without multiples going up.

For the full-year 2024, we reiterate our prior guidance of projected total home closings between 2,600 and 2,800 homes, and now expect our average selling price to range between $338,000 and $343,000. Company 1Q24 earnings

Risk

If the economy continues to remain strong and inflation stays sticky, it may trigger wages to grow much faster than SDHC can raise its prices. This will hurt margins, thereby dampening earnings margins. Management plans to expand into adjacent markets, and while this may drive growth, a lack of local knowledge (expertise) may cause SDHC to see slower consolidated growth as these new markets grow slower than expected.

Conclusion

I give a buy rating for SDHC. SDHC should see strong demand due to limited existing home inventory, as a result of the high rates and lower homes supply situation. SDHC differentiated business model that enables it to achieve short build times and high customization should also allow them to capture this demand effectively. Lastly, SDHC valuation is also attractive as it is trading near all-time-low.

Read the full article here