AppLovin Corporation’s (NASDAQ:APP) stock has massively outperformed over the last year and a half, and that has likely left its holders wanting more. With a 1Y total return of more than 230%, APP has easily outperformed its software peers and the S&P 500 (SP500). Notwithstanding the surge, APP is still valued at a discount relative to its tech sector peers when considering APP’s growth prospects. However, it’s also justified for investors to question whether AppLovin’s incredible growth could slow down as it laps its Axon 2.0 introduction over the past year.

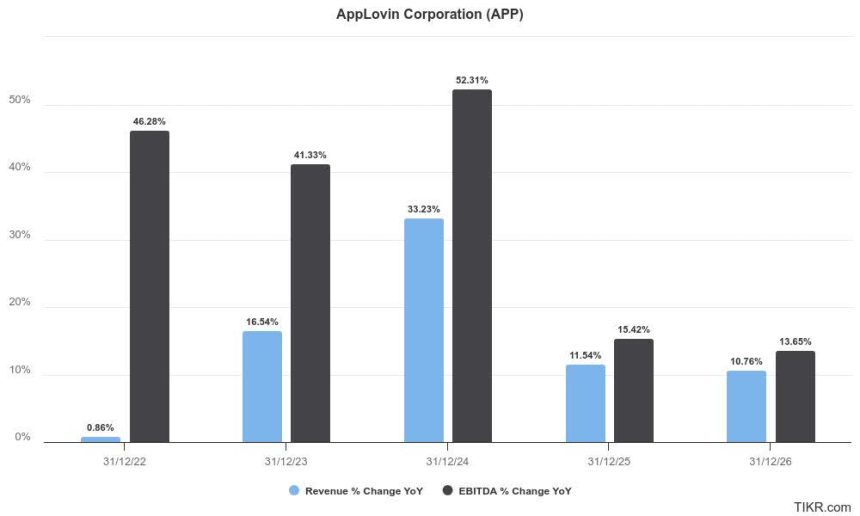

AppLovin forward estimates % (TIKR)

Ad tech investors should be familiar with AppLovin. Given its incredible performance, AppLovin has demonstrated Axon 2.0’s stellar performance while maintaining high operating leverage.

As seen above, Wall Street expects AppLovin to deliver more than 50% growth in adjusted EBITDA in 2024, markedly above its estimated 33% revenue upside. Management also emphasized the self-learning capabilities and ongoing deliberate improvements in Axon’s AI-driven Axon 2.0 model. Therefore, the company is confident that Axon will remain “a key driver for future growth.”

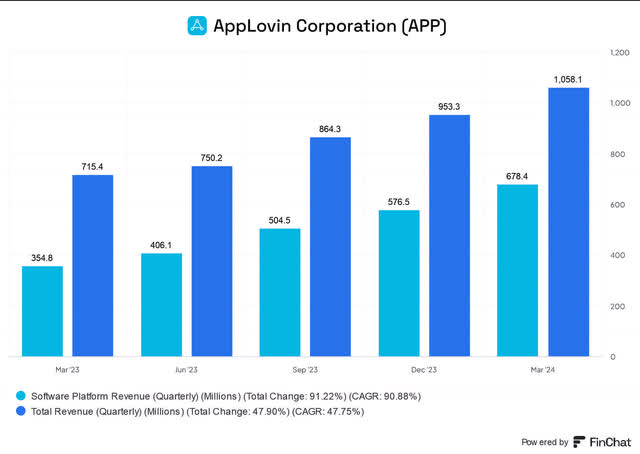

AppLovin software platform revenue (FinChat)

There’s little doubt that AppLovin’s “Black Box” model has helped generate a significant growth inflection over the past year. Software platform revenue surged to almost $680M, up over 90% YoY. It accounted for nearly 64% of AppLovin’s Q1 revenue base, underscoring its increasing importance in AppLovin’s growth opportunities.

In addition, AppLovin’s software-adjusted EBITDA surged by almost 125%, highlighting the inherent margin accretion gains to the company’s overall profitability. The critical question is whether such gains are sustainable over the next few years as it laps these incredible growth metrics.

AppLovin management anticipates broadening its advantages beyond mobile gaming to other growth verticals. Notably, they see increased opportunities in the web e-commerce vertical. Therefore, I assess investors will likely take note of AppLovin’s capabilities to broaden its market share beyond its core growth segment.

Undoubtedly, there are execution risks, given the more specialized mobile gaming vertical to which AppLovin has been exposed. Despite that, the high profitability business model is predicated on the success of its highly-performant ad-tech model. In addition, AppLovin’s ability to scale with higher-quality data being ingested by its model shouldn’t be understated. Management articulated its data advantages, potentially helping to maintain its leadership. The company believes that the “sheer volume of data processed by AppLovin enhances the effectiveness of their models over time.”

AppLovin plays a crucial role in performance advertising for its customers. Therefore, I assess that it helps its customers determine the effectiveness of their spending. Customers aren’t perturbed by the “Black Box” nature of Axon 2.0, as advertisers are ultimately looking for enhanced ROAS. Therefore, investors are encouraged to continue monitoring the increase in installation volume as one of the critical metrics for success. Accordingly, management highlighted that “the significant increase in installation volume indicates a corresponding rise in advertiser spend.”

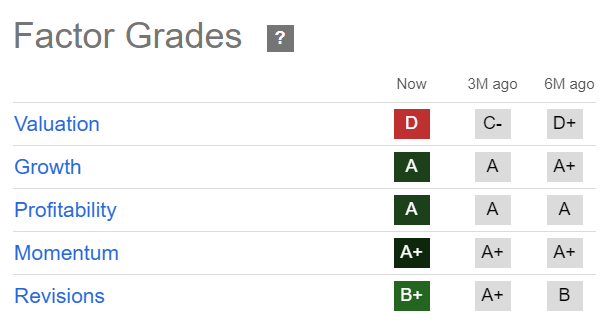

APP Quant Grades (Seeking Alpha)

Seeking Alpha Quant assigns APP three “A” range grades, highlighting the robustness of AppLovin’s bullish thesis. However, APP’s valuation is no longer assessed as cheap, as seen with its “D” valuation grade.

APP’s forward adjusted PEG ratio of 0.72 is more than 60% below its tech sector median. However, it’s also possible that AppLovin’s massive growth spurt could slow, even as it aims to expand beyond its core mobile gaming vertical.

Higher execution risks must be assessed, suggesting Wall Street may bake in a growth normalization phase from 2025. In addition, a broader macroeconomic slowdown could hurt APP more than its enterprise software peers, who are less dependent on the advertising vertical. Advertising budgets are assessed to be more cyclical than core IT spending budgets. Therefore, it’s necessary to reflect higher execution risks on APP’s growth potential.

Is APP Stock A Buy, Sell, Or Hold?

AppLovin has demonstrated its prowess as a key ad tech player in the mobile gaming space. Moving forward, the company needs to convince the market that it can seamlessly expand to other potential growth verticals, such as web e-commerce.

APP’s relatively attractive PEG ratio suggests the market has likely baked in higher execution risks. AppLovin’s solid execution (“B+” earnings revisions grade) has also helped underpin robust buying sentiment (“A+” momentum grade). Therefore, I assess that the risk/reward is still skewed favorably toward the upside, supported by AppLovin’s fundamentally strong business model (“A” profitability grade).

Rating: Initiate Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here