In our previous analysis, we assessed Teradyne, Inc.’s (NASDAQ:TER) position in the semiconductor ATE market where Teradyne and Advantest (OTCPK:ATEYY) are dominant players, holding over 60% of the market share. We believe Teradyne’s extensive equipment portfolio targets various semiconductor product categories and expected Teradyne’s leading position to be maintained due to high entry barriers in the concentrated market.

In this analysis, we covered the company again as we noticed its revenues have been declining in the past 2 years, thus we examined whether it could recover going forward. Firstly, we examined its segment breakdown as seen in the table below. The company’s revenues are broken down into its Semiconductor Test, Systems Test, Wireless Test and Industrial Automation segments. We analyzed the performance of each segment and determined the company’s competitiveness in each. We also analyzed the market growth outlook of its segments and determined if its growth could recover.

|

Teradyne Revenue by Segments ($ mln) |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

10Y Avr. |

|

Semiconductor Test |

1,301 |

1,202 |

1,368 |

1,663 |

1,492 |

1,553 |

2,260 |

2,642 |

2,081 |

1,819 |

|

|

Growth % |

27.2% |

-7.6% |

13.9% |

21.5% |

-10.2% |

4.0% |

45.5% |

16.9% |

-21.3% |

-12.6% |

7.7% |

|

System Test |

162.5 |

211.6 |

189.8 |

170.1 |

261.5 |

287.5 |

409.7 |

467.7 |

469.3 |

338.2 |

|

|

Growth % |

-35.5% |

30.2% |

-10.3% |

-10.4% |

53.7% |

9.9% |

42.5% |

14.2% |

0.3% |

-27.9% |

6.7% |

|

Wireless Test |

184.5 |

184.6 |

96.2 |

192.1 |

216.1 |

157.3 |

173.0 |

375.9 |

201.7 |

144.3 |

|

|

Growth % |

20.6% |

0.1% |

-47.9% |

99.7% |

12.5% |

-27.2% |

10.0% |

117.3% |

-46.3% |

-28.5% |

11.0% |

|

Industrial Automation |

41.9 |

99.0 |

111.9 |

132.0 |

298.1 |

279.7 |

216.9 |

403.1 |

375.2 |

||

|

Growth % |

136.3% |

13.0% |

18.0% |

125.8% |

-6.2% |

-22.5% |

85.8% |

-6.9% |

42.9% |

||

|

Total |

1,648 |

1,640 |

1,753 |

2,137 |

2,102 |

2,296 |

3,122 |

3,703 |

3,155 |

2,676 |

|

|

Total Growth % |

15.4% |

-0.5% |

6.9% |

21.9% |

-1.6% |

9.2% |

36.0% |

18.6% |

-14.8% |

-15.2% |

7.6% |

Source: Company Data, Khaveen Investments

Semiconductor Test Segment

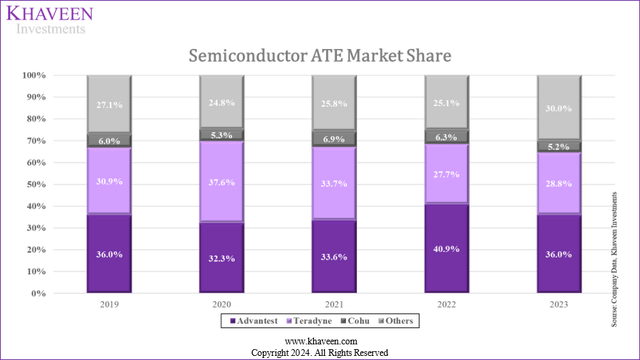

Firstly, we examined its semiconductor test segment, which accounts for the majority of its revenues (68%) and is the largest segment. Notably, while the segment has a 10-year average growth of 7.7%, its performance in the past 2 years has been negative, the worst in its past 10 years. We updated our market share from our previous analysis.

Company Data, Khaveen Investments

|

Semicon ATE Market Revenue ($ mln) |

2019 |

2020 |

2021 |

2022 |

2023 |

Average |

|

Advantest (ATEYY) |

1,809 |

1,941 |

2,630 |

3,075 |

2,277 |

|

|

Growth % |

7.3% |

35.5% |

16.9% |

-26.0% |

8.4% |

|

|

Teradyne |

1,553 |

2,260 |

2,642 |

2,081 |

1,819 |

|

|

Growth % |

45.5% |

16.9% |

-21.3% |

-12.6% |

7.2% |

|

|

Cohu (COHU) |

299 |

318 |

542 |

475 |

326 |

|

|

Growth % |

6.2% |

70.3% |

-12.4% |

-31.2% |

8.2% |

|

|

Others |

1,359 |

1,492 |

2,016 |

1,890 |

1,898 |

|

|

Growth % |

9.8% |

35.2% |

-6.3% |

0.4% |

9.8% |

|

|

Semiconductor ATE Market Size |

5,020 |

6,010 |

7,830 |

7,520 |

6,320 |

|

|

Growth % |

19.7% |

30.3% |

-4.0% |

-16.0% |

7.5% |

Source: SEMI, Company Data, Khaveen Investments

Based on the market share, the overall semicon ATE market appears stable with 3 companies representing the majority of the market which are Advantest, Teradyne and Cohu. All 3 top companies’ market share has been similar over the period except for certain outlier periods which are in 2020 for Teradyne and 2022 for Advantest as they experienced significant growth compared to the market. The Semiconductor Test Equipment has declined in the past 2 years as Teradyne’s management had previously highlighted that “the Semi Test equipment market was entering a downturn, with demand declining in end markets such as smartphones”.

Furthermore, in terms of market share, Teradyne’s market share surged in 2020 and overtook Advantest, outperforming the overall market growth. According to management, the surge in growth is attributable to strong growth in mobility test and the launch of the new UltraFLEXplus product. Management highlighted that 2020 “saw the beginning of meaningful 5G silicon content, which necessitated a build-out of new tester capacity”. In 2020, 5G smartphone adoption which was still nascent saw explosive growth with shipments rising by 1,176%. The company also highlighted Qualcomm, a key company in smartphone AP and RF, as one of its top customers, accounting for 11% of revenues.

However, in the following years, Teradyne’s growth moderated and its market share eroded, being overtaken by Advantest in 2021 as the market leader through 2023. In 2022 and 2023, its growth was negative. This corresponds with the weakness in the smartphone market, in which shipments declined by 11.1% and 3.3% in 2022 and 2023 respectively. Furthermore, 5G adoption has slowed as the market grows towards maturity with shipment growth slowing to 11% in 2023 with an adoption rate of 61%.

Furthermore, Advantest experienced robust growth in 2022. This is as management highlighted its growth in data center as it was “ capturing the growing test demand for high-performance semiconductors such as HPC and Al devices, and gained market share”. Overall, the semicon test equipment’s top 3 companies’ average growth is close to the market average, indicating stagnant competition between the 3 companies. In our previous analysis, we determined that Teradyne had a slightly wider product breadth compared to Advantest which has a similar breadth of semiconductor test solutions across “categories including memory, logic, discrete, analog and optical semiconductors” except for FPGA.

Teradyne

However, the market is also becoming more competitive as the share of the non-top 3 companies has risen, outpacing the market growth. According to DigiTimes, China’s semiconductor equipment companies continued to experience strong double-digit growth. This is despite the slowdown in the global semicon equipment market. China is the largest OSAT market in the world. Teradyne derived 70% of revenues from Asia Pacific, including China.

Market Research Reports, Khaveen Investments

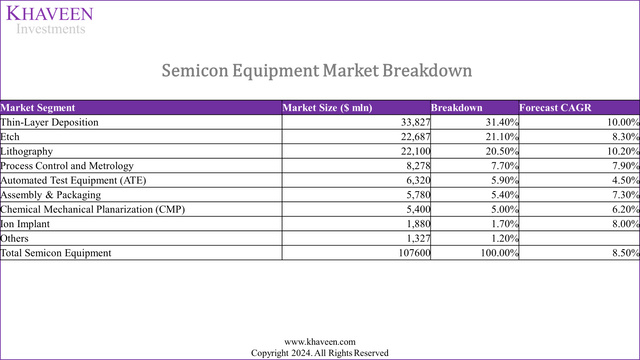

We updated the semicon equipment market breakdown from our previous analysis. The ATE segment represents 5.9% of the total semicon equipment market and has a forecast CAGR of 4.5% according to Precedence Research, lower than the overall semicon equipment growth forecasts. Market leader Advantest expects a 5% growth in 2024, which is in line with the market CAGR. The market growth is expected to be driven by increasing demand for semiconductors due to the rise of technologies such as AI, Cloud, IoT, 5G, ADAS and EV. However, we believe the lower growth in comparison with the semicon equipment market is due to the ATE segment catering to the OSAT market, which has a lower CAGR of 6.6% compared to the overall semicon industry CAGR of 8.8%. Nonetheless, we expect Teradyne to capitalize on the market growth as one of the leading companies.

Systems and Wireless Test Segment

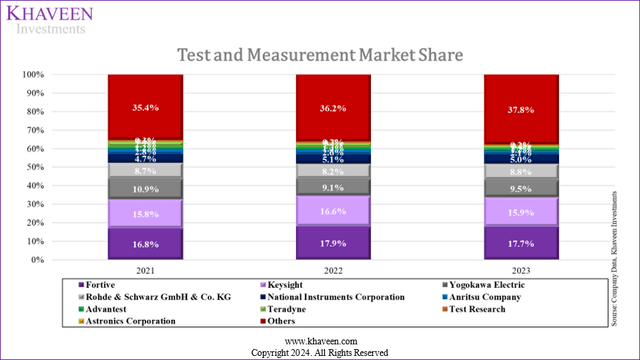

In the second point, we examined its System Test and Wireless Test segments. Based on its annual report, its Systems Test segments consist of 3 business units which include its Storage Test, Defense/Aerospace, Production Board Test units which all commonly provide test systems. Furthermore, the Wireless Test segment provides test systems for devices such as smartphones and PCs. Both systems tests and wireless tests fall under the test and measurement market. We compiled the market share of the company based on revenues of publicly traded competitors below.

Company Data, Khaveen Investments

|

Test and Measurement Equipment Market |

2021 |

2022 |

2023 |

Average |

|

Teradyne Revenue |

844 |

671 |

483 |

|

|

Growth % |

-20.5% |

-28.1% |

-24.3% |

|

|

Teradyne Market Share |

2.7% |

2.1% |

1.4% |

Source: Company Data, Khaveen Investments

Based on the chart above, Teradyne is a relatively small player with a market share of only 1.4% of the $34.3 bln Test and Measurement market, which is 10% of the Electronic Equipment & Instruments subindustry ($345 bln). The market appears fragmented except for 4 notably large companies such as Fortive (FTV), Keysight (KEYS), Yokogawa Electric and Rohde & Schwarz Global accounting for 51% of the market share combined. Furthermore, Teradyne’s market share eroded over the period as its revenue declined by over 20% each year. The share of Others increased slightly in the past 2 years, indicating increasing competition.

In 2023, Teradyne’s performance was impacted by poor performance in both System Test and Wireless Test. In System Test, the primary factor attributed by management is due to weakness in the Storage Test business unit, which represented 46% of the segment revenue. Management highlighted that “HDD and system-level test in our storage business was down in total nearly 50% from 2022” as there is “excess test capacity in the HDD and SLT test markets”. The HDD market declined by 35% in 2023.

Furthermore, in Wireless Test, the company attributed the decline to “weakness in PC and mobile markets”. Its growth was the lowest in 2022 as both the PC and smartphone markets saw sharp declines of 11.1% and 16.1%. However, its performance improved slightly in 2023 as the PC and smartphone market started recovering in H2 2023 as we previously highlighted.

The Test and Measurement market has a forecast CAGR of 4.6% according to MarketsandMarkets, which is similar to the semicon test equipment market growth forecast as mentioned above. The market growth drivers are the increasing need for interoperability testing and increased demand for electronic devices and IoT devices. In the near term, we expect the company’s System Test segment to recover in 2024 amid the ongoing memory market recovery, which the company also guided for “ as HDD end markets begin to recover” but also cautioned of headwinds as “tester capacity utilization rates remain low”. Furthermore, in the Wireless Test, we expect the company to benefit from the ongoing recovery in the PC and smartphone markets.

Robotics

Finally, the company’s Industrial Automation segment is the smallest segment of the company (14%) but also has the fastest average growth of 42.9%. However, in 2023, its revenue performance declined despite the company highlighting robust demand and orders as the company also highlighted in its 2023 annual report that “the impact of our channel transformation resulted in a weaker than forecasted first half of 2023”.

Teradyne

The segment includes collaborative robots (cobots) and industrial automation robots. The company highlighted its competitors in the segment has a diverse range of large established industrial companies expanding into the market such as Fanuc (OTCPK:FANUY), OMRON (OTCPK:OMRNY) and ABB (OTCPK:ABBNY) to smaller emerging companies that are more specialized in the market such as AUBO Robotics, Jaka, Agilox. We compiled the market sizes of the collaborative robots and autonomous mobile robots in the table below.

Source: Company Data, Khaveen Investments

Based on the table above, we derived the total market size of its Industrial Automation segment is $6.52 bln, which is small compared to the $321 bln Industrial Machinery & Supplies & Components subindustry. Teradyne revenue from collaborative robots is higher compared to autonomous mobile robots, and its market share in collaborative robots is higher at 9.6% compared to 2.1%. We believe this could favor the company as the collaborative robots market has a higher forecast CAGR of 32.4% compared to the autonomous mobile robot market. One of the drivers of the cobots market is the advantages over traditional industrial robots, including reduced initial expenses, simpler integration processes, and quicker deployment times. Furthermore, the autonomous robot market growth is expected to be driven by “increasing demand for automation”. Furthermore, the company announced a partnership with Nvidia for AI-powered solutions for automation.

Last month we announced a collaboration with NVIDIA to utilize their robotic stack on UR hardware and demonstrated the power of that collaboration at GTC with a visual inspection application. Also in the first quarter, we announced the MiR1200 Pallet Jack, a new AI-powered solution that uses 3D Vision to identify, pick up and deliver pallets even in dynamic and complex environments, making it a valuable resource for autonomous material handling in factories and warehouses. – Greg Smith – Chief Executive Officer

Overall, we believe Teradyne’s Industrial Automation segment, though the smallest at 14% of the company, has the strongest growth outlook, supported by the high market growth in cobots and autonomous mobile robots as well as its partnership with Nvidia to integrate its AI software in Teradyne’s products, which we believe is positive as we previously highlighted that we view Nvidia as a leader in AI. Furthermore, we believe Teradyne’s greater focus on cobots and having a higher market share bodes well, as it has a higher CAGR compared to the autonomous mobile robot market. All in all, we derived a weighted average forecast CAGR of 29.2% for the company’s Industrial Automation segment based on a weighted average of the company’s segment revenue breakdown and the Collaborative Robot and Autonomous Mobile Robot market forecast CAGR.

Risk: Weak Market Conditions

According to management in its recent earnings briefing, the company highlighted that the company continues to face weak market conditions and that they “don’t see a significant improvement right now in terms of end market conditions”. However, we expect a recovery in the semiconductor equipment market overall in 2024 which could bode well for its recovery this year. Additionally, the company highlighted its orders for the industrial automation segment remain strong, boding well for its growth outlook.

Verdict

|

Revenue Breakdown by Segments ($ mln) |

2021 |

2022 |

2023 |

2024F |

2025F |

2026F |

|

Semiconductor test |

2642 |

2081 |

1819 |

1,900 |

1,986 |

2,075 |

|

Growth % |

16.9% |

-21.3% |

-12.6% |

4.5% |

4.5% |

4.5% |

|

System Test |

468 |

469 |

338 |

354 |

370 |

387 |

|

Growth % |

14.2% |

0.3% |

-27.9% |

4.6% |

4.6% |

4.6% |

|

Wireless Test |

376 |

202 |

144 |

151 |

158 |

165 |

|

Growth % |

117.3% |

-46.3% |

-28.5% |

4.6% |

4.6% |

4.6% |

|

Industrial Automation |

217 |

403 |

375 |

485 |

626 |

809 |

|

Growth % |

-22.5% |

85.8% |

-6.9% |

29.2% |

29.2% |

29.2% |

|

Total |

3,704 |

3,155 |

2,676 |

2,890 |

3,140 |

3,437 |

|

Growth % |

18.6% |

-14.8% |

-15.2% |

8.0% |

8.7% |

9.4% |

Source: Company Data, Khaveen Investments

In conclusion, we believe Teradyne stands to benefit from the growth opportunities within its various segments. While the semiconductor equipment market is forecasted to grow at a moderate pace, we anticipate Teradyne’s ATE segment to leverage the market’s expansion, despite catering to the slightly slower-growing OSAT market. Additionally, with the Test and Measurement market aligning closely with the semiconductor test equipment market growth forecasts, we foresee a recovery in Teradyne’s System Test segment, particularly amidst the ongoing memory market rebound and the resurgence in demand for electronic and IoT devices.

Moreover, we expect Teradyne’s Industrial Automation segment to emerge as a key driver of growth, fuelled by the robust market expansion in cobots and autonomous mobile robots. Given Teradyne’s emphasis on cobots and its higher market share in this segment, we believe the company is well-positioned to capitalize on the opportunities presented by the accelerating adoption of automation technologies across various industries.

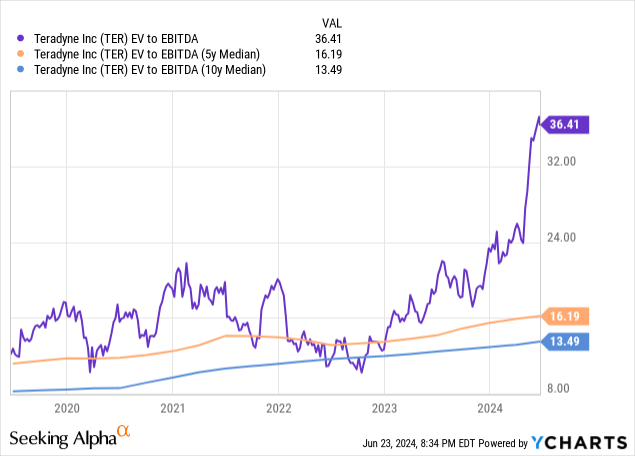

YCharts

However, the company’s EV/EBITDA valuation ratio appears to be significantly higher than its historical average, which is currently 2.2x higher than its 5-year median and 2.7x than its 10-year median ratio, indicating it may be overvalued.

Seeking Alpha

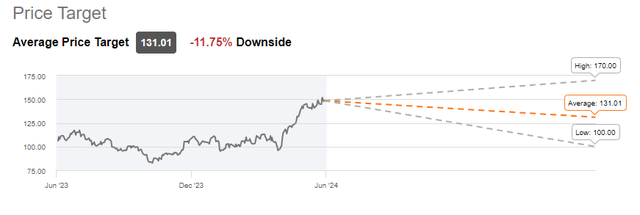

Furthermore, based on analysts’ consensus, the company has an average price target of $131.01, a downside of -11.75%, thus we rate it as a Sell.

Read the full article here