We last covered DoubleLine Income Solutions Fund (NYSE:DSL) earlier in 2024, at a time when more interest rate cuts looked likely than they do now. The fund has seen its discount little changed since our prior update, trading at a slight premium. The closed-end fund has moved mostly sideways since that update as well, in terms of its share price, but on a total return basis, we saw some gains.

DSL Performance Since Prior Update (Seeking Alpha)

Today, DSL still doesn’t look like a bargain due to its valuation. However, we do have a new semi-annual report that they have posted for the six months ended March 31, 2024.

DSL Basics

1-Year Z-score: 0.73

Premium: 1.70%

Distribution Yield: 10.50%

Expense Ratio: 1.44%

Leverage: 23.22%

Managed Assets: $1.661 billion

Structure: Perpetual

DSL has an investment objective to “provide a high level of current income, and its secondary objective is to seek capital appreciation.” The fund is invested “in a portfolio of investments selected for their potential to provide high current income, growth of capital, or both. The fund may invest in debt securities and other income-producing investments anywhere in the world, including in emerging markets.”

The fund’s leverage remains rather moderate, as we’ve seen the leverage ratio barely move since our prior update. Total leverage came in at around $367 million; that amount is actually a touch lower than what we saw at the end of the fiscal year 2023 when it came in at nearly $372 million but up slightly from the last semi-annual report, where borrowings stood at $365 million.

With that said, any leverage is going to negatively impact the fund in a down market and positively impact it in a rising market. This increases the volatility of the fund, bringing higher risks, but also potentially greater rewards.

Like most CEFs, the fund has seen its borrowing rates rise as the Fed lifted its target rate. DSL pays a rate of Overnight Bank Financing Rate (“OBFR”) plus 1%. That has seen the fund’s total expense ratio climb to 3.24% in the latest report, stable from the last annual report but up from 2.17% in fiscal 2022.

This fund carries a meaningful sleeve of floating rate exposure to a degree where the higher borrowing costs were significantly offset. Interestingly, though, the fund has taken a hit in the last semi-annual report in terms of net investment income. This could be due to the timing of interest payments the fund itself receives, defaults in the portfolio or just portfolio holding shifts due to being actively managed. In all likelihood, it is probably a combination of all three of these factors contributing to the decline.

Performance – Slight Premium Means No Bargain

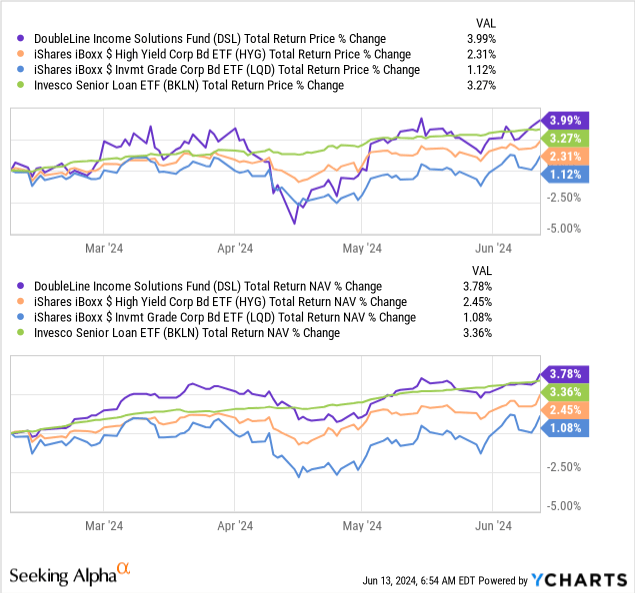

Shallow total returns are certainly not what investors are looking for, as has been the case with DSL’s results since our prior update. However, on a relative basis, against several other fixed income-focused ETFs, the fund’s performance came out on top. The fund delivered slightly better than the Invesco Senior Loan ETF (BKLN) during this time.

Ycharts

BKLN is a fund focused on senior loans, which leads the fund to be invested heavily in floating-rate securities. DSL, on the other hand, is a multi-sector bond fund with far greater flexibility on when, where and how it invests. In our last update, the fund was favoring emerging markets, and that remains the case with the latest data we have available for the fund at this time as well.

DSL is also leveraged, whereas these other barometer ETFs that we are using are not. So, on that front, one might be disappointed with only marginally beating out these fixed-income peers.

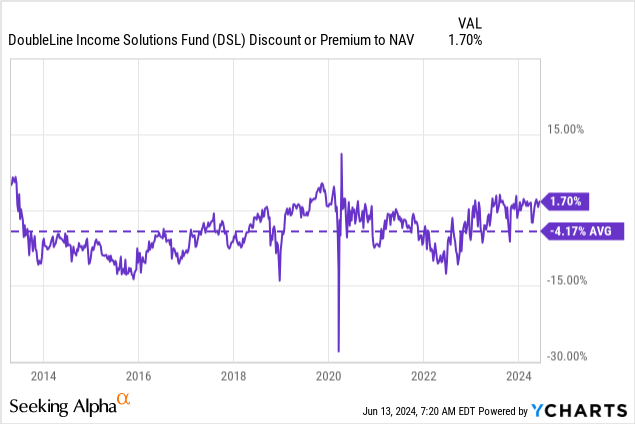

Where DSL could have an edge against those baskets of ETFs would be if the fund carried an unusually large discount. At this time, that isn’t the case. It continues to trade at a slight premium — and while premiums aren’t unheard of for this fund, it continues to make it only worth a ‘Hold’ at this time, in my opinion. Further, the fund is trading above its longer-term average as well.

Ycharts

Distribution Coverage Sinks

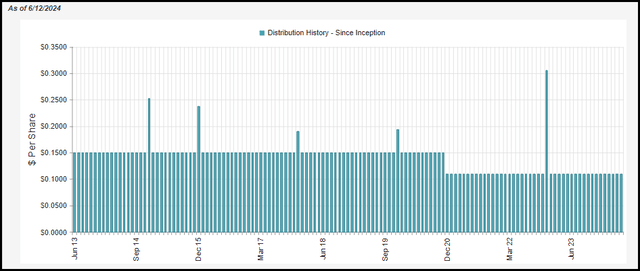

Despite the higher borrowing costs and seeing net investment income decline in the latest fiscal year, the fund has continued to maintain its same distribution rate. Currently, that works out to a distribution rate of 10.50% and a NAV rate of 10.68%.

DSL Distribution History (CEFConnect)

In the prior coverage, I noted that NII could possibly increase going forward based on seeing some rate cuts. However, that simply hasn’t been the case yet, and with the latest Fed projections just recently announced, that wait is likely to be even longer.

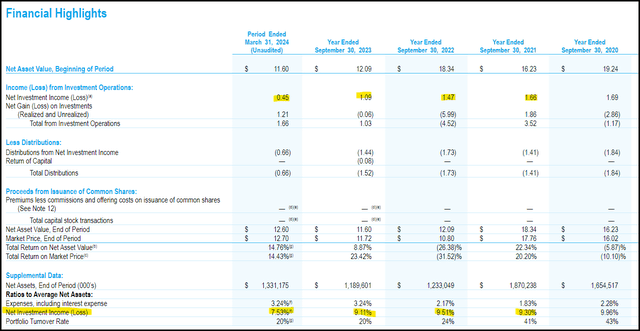

Even worse, coverage with this latest report has sunk even lower if the second six months of this fiscal year mirrors the first. The annotation (f) here is simply stating that it is an annualized figure. Based on this first six-month figure, we’d see NII for the year come in at $0.90, which would mark another ~17.5% decline from the prior year. The floating rate exposure this fund carried seemed to be helping the fund maintain a relatively limited impact of the higher borrowing rate environment, as the NII ratio didn’t decline materially.

DSL Financial Highlights (DoubleLine (highlights from author))

Of course, these latest figures aren’t encouraging, as it translates into meaning that the fund’s NII distribution coverage hit a lower level of around 68.2%; that would be down from the 83% coverage level prior. That’s certainly not a great trend for this fund, and it could indicate that the fund needs rate cuts sooner rather than later or potentially could face another distribution cut.

At the same time, CEFs can pay out what they’d like for as long as they’d like, so long as NAV doesn’t go to $0. If the manager expects the environment to change going forward to be more conducive to operating a leveraged high-yield fund, that’s likely a factor for choosing to maintain the current rate as well.

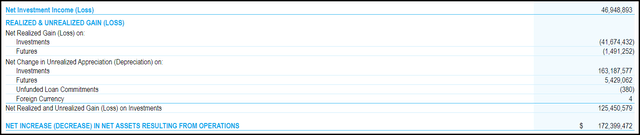

With lower rates, the fund could see its NII tick up a bit and reverse some of the declines we’ve seen. The underlying portfolio could also see some appreciation, which helped the fund see a meaningful climb in unrealized appreciation in the latest report. That unrealized appreciation more than offset the realized losses the fund took during this time. Despite the lack of NII distribution coverage, it is the unrealized appreciation being so strong that saw the fund’s NAV rise anyway.

DSL Realized/Unrealized Gains/Losses (DoubleLine (highlights from author))

Additionally, thanks to the slight premium for the fund, they can issue new shares through an at-the-market offering. The premium has been rather shallow, and that has meant that it hasn’t seen a measurable per-share accretion level for investors. Overall, it is neutral for investors at this time, not damaging but not producing an actual measurable benefit.

However, consider that by being able to raise capital through this ATM, they can continue to pay out a higher distribution while they don’t experience a significant hit to the overall pool of assets they are managing. That means their fees continue to trickle in, and that gives them an incentive to maintain the current distribution rate despite a lack of coverage.

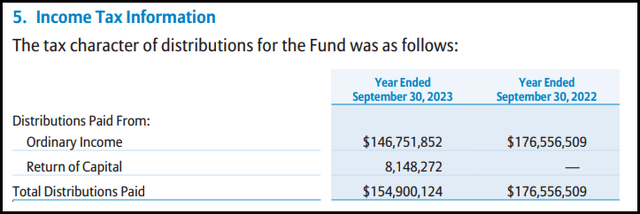

Given the lack of distribution coverage, we could continue to expect to see some return of capital in the fund’s distribution as we saw last year. Otherwise, the fund’s distribution is primarily classified as ordinary income.

For tax purposes, the fund has listed primarily ordinary income in each of the last two years. This is something that we would expect to be the case going forward as a fixed-income-focused fund.

DSL Distribution Tax Classification (DoubleLine)

DSL’s Portfolio

In looking at the fund’s portfolio, we have some names in default, and it highlights a good example of why higher rates also come with a downside. For example, BYJU’s Alpha Inc. pays at a prime rate plus 7%. As rates shot higher, their rate has now shifted up to 15.50%. With a climb in rates so rapidly, it contributes to more defaults by seeing significantly higher borrowing costs — which is exactly how the Fed’s tool works to slow down the economy. In the case of this company, another contributing factor is that it was an online learning platform that “fizzled out” after the Covid boom.

DSL Holding (DoubleLine)

One of the ways that the fund can manage its duration risk is through futures contracts or various other derivatives.

For the fund’s latest report, they were long futures contracts, and as we saw above, that contributed to some realized losses, but those were offset by unrealized appreciation. Being long means they are betting that risk-free rates will actually rise.

DSL Futures Contracts (DoubleLine)

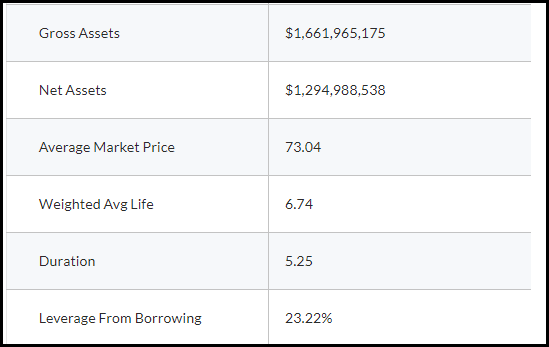

For DSL, the latest duration comes in at 5.25 years. That’s down slightly from the 5.65 years. However, the other material change we saw in the fund’s underlying portfolio was the average market price of the underlying securities. That most recently came in at $73.04, an increase from the $70.95 in our prior update, and that is why we saw net assets and managed assets rise.

DSL Stats (DoubleLine)

This could be a factor in why investors are willing to pay a slight premium for the portfolio when buying DSL because the underlying portfolio is heavily discounted in anticipation of higher default expectations with the higher rate environment.

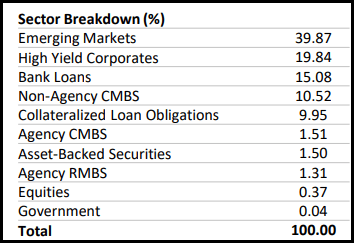

The fund continues to invest heavily in emerging markets, which traditionally do come with more risks and this is why these debt instruments are likely trading at such a substantial discount.

DSL Sector Allocation (DoubleLine)

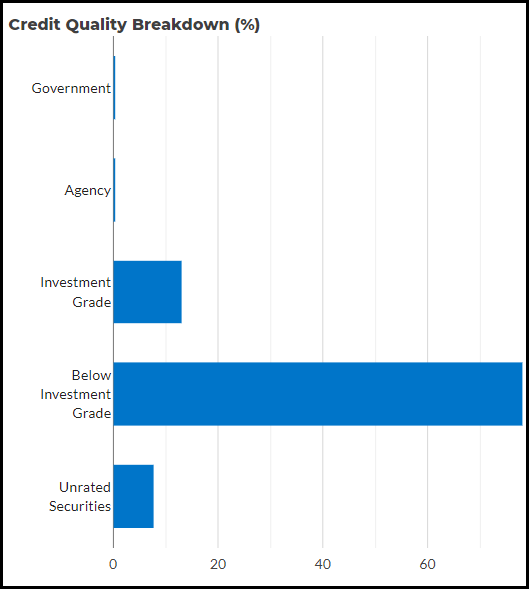

In total, 78.15% of the fund is invested in below-investment-grade securities. There is 7.85% invested in unrated securities and 13.08% classified as investment-grade.

DSL Credit Quality Breakdown (DoubleLine)

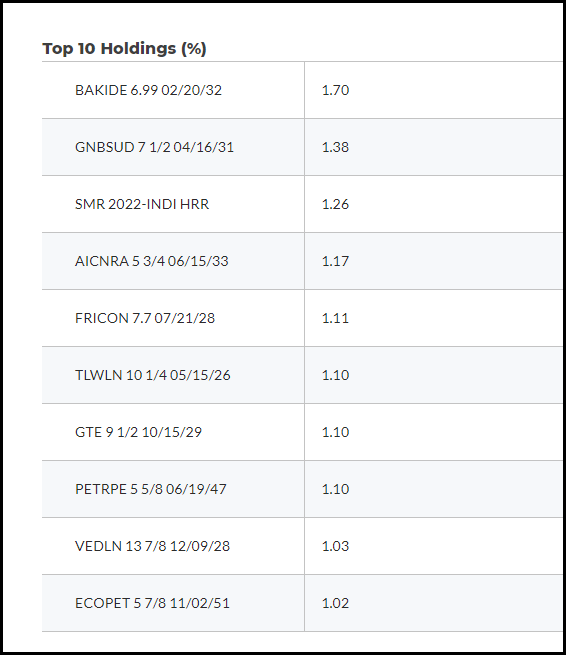

So, there are substantial risks overall in this type of portfolio then adding leverage on top of it. What makes the fund a bit safer is the significant diversification it carries. No security makes up an overly outsized weighting of the fund, and CEFConnect notes there are 482 holdings.

DSL Top Ten Holdings (DoubleLine)

Even further, being that several of these are securitized and pooled investments means there are hundreds or even thousands of underlying loans pooled together. Those would include the funds non-agency CMBS, collateralized loan obligations, agency CMBS, asset-backed securities and agency RMBS allocations. Combined, those made up nearly 25% of the fund’s invested assets.

Conclusion

DSL’s distribution coverage has weakened in its latest report, which isn’t encouraging when considering the stability of its distribution. With rate cuts being pushed out even further, that lack of coverage could become more of a concern.

On the other hand, given that the distribution is likely keeping investors pacified and allowing the fund to trade at a premium, they can issue new shares through their ATM. That cash then can be used to pay investors where the NII coverage is lacking.

If/when rates are cut, that could further improve coverage of the fund’s distribution and could lead to some recovery in the underlying portfolio. That could also play a role in why the fund is choosing to maintain its distribution as well.

The underlying portfolio is trading at a huge discount to par, but that’s simply compensation for the elevated risks of its heavily leaning emerging market portfolio, in my opinion. With a higher rate environment designed to literally drive financially unstable companies to default and bankruptcy, to slow the economy, that also needs to be compensated with a discount to face value. The fund’s own slight premium then takes away some of that appeal.

This all combines for me to continue to not view this fund as overly favorable and would maintain a ‘Hold’ rating. If the fund moved a discount of 5-10%, then my view could possibly be persuaded otherwise.