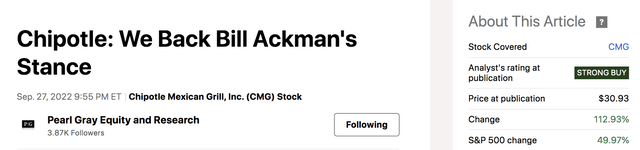

Today’s article circles back to Chipotle Mexican Grill, Inc. (NYSE:NYSE:CMG), a stock we’ve covered several times during our tenure on Seeking Alpha. Our first coverage was in September 2022, when we argued in favor of Bill Ackman’s outlook on Chipotle. Our rating was successful, as the stock has rallied by approximately 1.12x ever since.

Our 1st Chipotle Rating (Seeking Alpha)

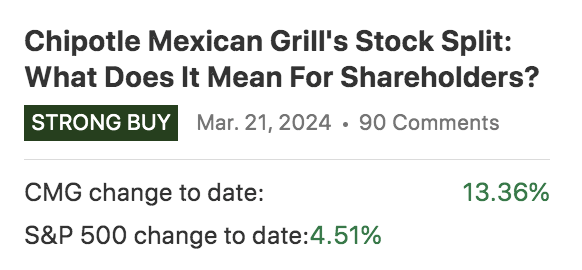

We followed up on our initial analysis by authoring an article in March 2024, stating that Chipotle’s pending stock split would favor its stock price. As shown below, Chipotle’s stock has gained by about 13% since we dispensed our thoughts.

Our Second Chipotle Rating (Seeking Alpha)

Earlier this week, we decided to engage with Chipotle’s stock again and share our updated thoughts in this article. The company’s stock split has been executed. Moreover, Chipotle is set to release its second-quarter earnings report next month, providing us with a stellar opportunity to update our thesis.

Here’s what we think about Chipotle’s stock in today’s climate.

Chipotle’s Stock Split

Chipotle’s 50-1 stock split has been executed, bringing its stock price down to around the $65 handle from previously trading above $3200. Although trading at a lower price, a split provides no unitary adjustment and, therefore, doesn’t directly influence shareholders’ economic value.

Despite not adjusting in economic value, Chipotle’s stock split raises a few market-based inflection points, primarily pertaining to liquidity. Firstly, the stock’s liquidity could improve as its supply is denser. Increased liquidity might reduce indirect costs, such as market impact and opportunity costs.

We think the stock split will enhance market efficiency. The consequent direction of the stock’s price will probably be dictated by other factors like fundamentals, valuation, and market sentiment.

Let’s move ahead

Fundamental Performance

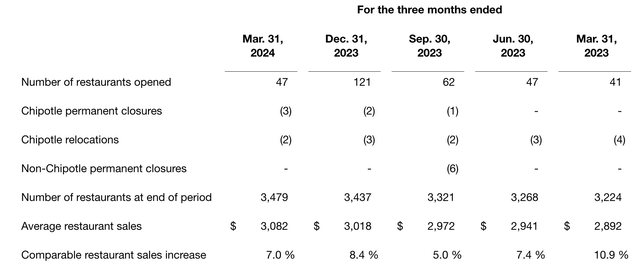

Chipotle has displayed steady growth on an asset level since our latest coverage, adding to its net restaurant count. Moreover, the firm’s comparable store sales have increased steadily in past quarters. Comparable sales increased by 7% in Q1, which is well ahead of the global and U.S. inflation rates. Chipotle’s comparable sales grew slower than in some of its previous quarters. However, keep in mind that stagflation has occurred, suggesting slower comparable sales weren’t due to structural concerns.

Restaurant Data (Chipotle)

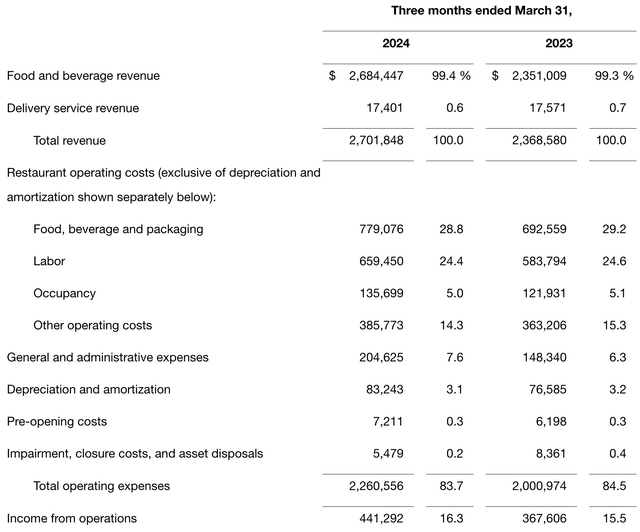

Chipotle’s restaurant-level performance is reflected in its income statement. The company’s revenue increased in Q1. Additionally, Chipotle’s operating profit margin ticked up by 80 basis points.

We think its income statement is encouraging, showing an increase in sales with a contemporaneous decrease in common-size operating expenses. Although debatable, we believe additional margin expansion is possible, as Chipotle’s strong branding and online sales strategy allow robust top-line potential. At the same time, factors such as a softer labor market and growing power over suppliers via economies of scale could drop the firm’s cost base.

Income Statement (Chipotle)

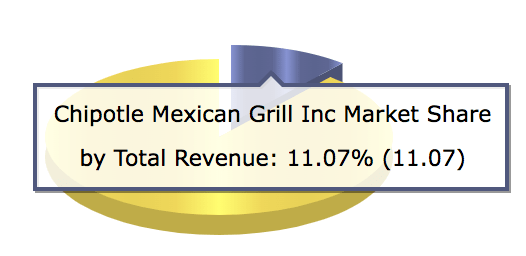

Furthermore, we like the look of Chipotle’s peer-based stance. Its broad-based market share of 11.07% provides it with “throughout-the-cycle” potential that could see it sustain its performance during cyclical environments harming smaller restaurants.

Goldman Sachs’ (GS) Christine Cho recently echoed the abovementioned, stating that consumer tailwinds are fading and that

“traffic and unit growth will become an increasingly important part of the restaurants’ growth equation, driving a bigger divergence across the peer set.”

Cho contemporaneously assigned a bullish rating on Chipotle’s stock based on its potential to diverge from its smaller peers.

Chipotle Market Share (CSI Markets)

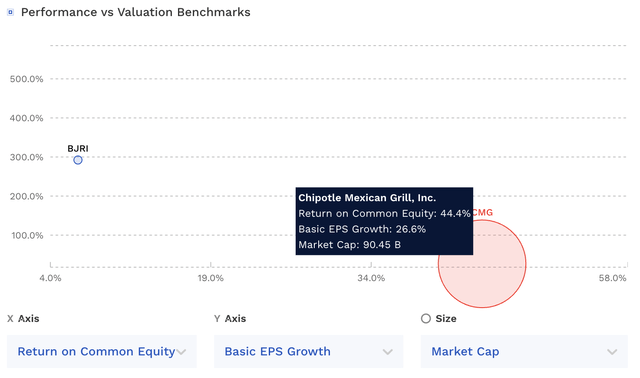

The aforementioned attributes have contributed to impressive growth rates across the board, arguably providing Chipotle with a secular growth tile. Additionally, Chipotle’s Return on Common Equity ratio of 44.37% echoes shareholder value, as it exceeds its sector median by about 2.79x and its own five-year average by 46%.

In essence, we think this is a growth asset with continuous shareholder value creation phased in.

Seeking Alpha

A Few Concerns

Surrendering Product Quality?

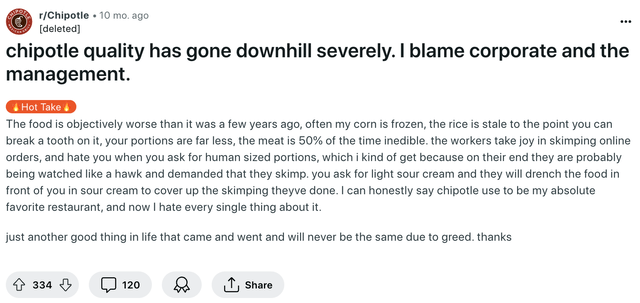

Despite our optimism about the restaurant chain’s fundamentals, we have a few reservations about Chipotle. Firstly, although it is an anecdotal opinion, a product’s quality analysis holds validity.

We believe Chipotle’s product quality has dipped recently. We’ve also taken note of similar opinions. As such, we worry that the firm might be riding on its reputation while aiming to expand its profit margins with lower-quality products.

Again, this is an anecdotal opinion. However, we think it holds weight.

Customer Review With Significant Upvote Support (Reddit)

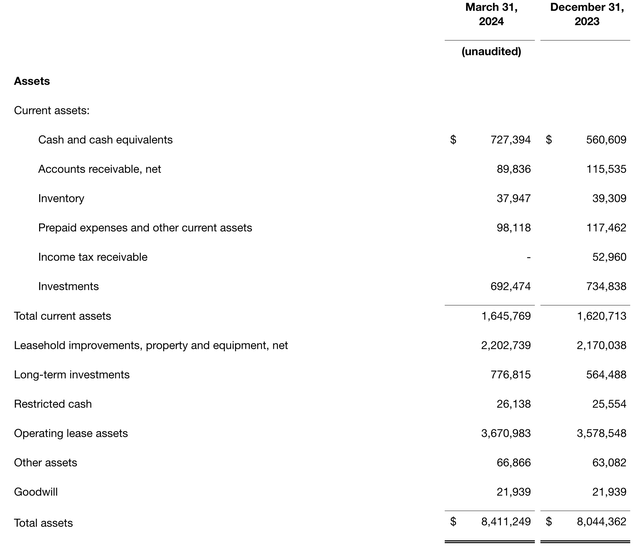

Balance Sheet Interpretation

Another area of concern is the interpretation of Chipotle’s balance sheet.

Some investors might look at the firm’s balance sheet metrics in isolation, deeming it solid. However, a deeper dive shows that a significant portion of Chipotle’s balance sheet comprises operating leases, which it uses to host its restaurants and offices. Although we don’t think this produces a liquidity risk, we urge investors to avoid confusing this line item with organic asset growth.

Balance Sheet (Chipotle)

Aside: Here’s a link to more information on how operating leases are accounted for on the balance sheet – Link Here.

Valuation and Technical Analysis

Multiples

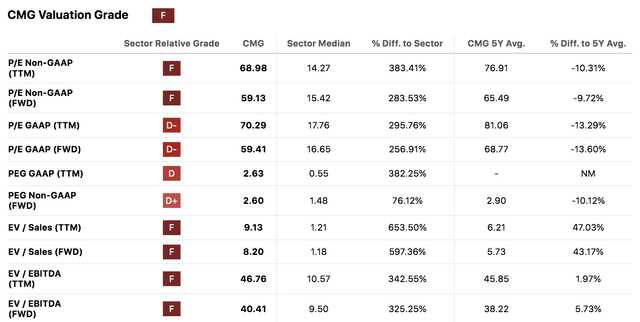

We have noticed that many analysts are worried about Chipotle’s price multiples, and quite rightly so. I mean, we are discussing a stock with a price-to-earnings ratio of 68.98x.

Seeking Alpha

Despite its high multiples, it is necessary to put matters into context. We think Chipotle’s splendid growth justifies most of its high price multiples, meaning investors will likely reinvest in its stock until its growth slows.

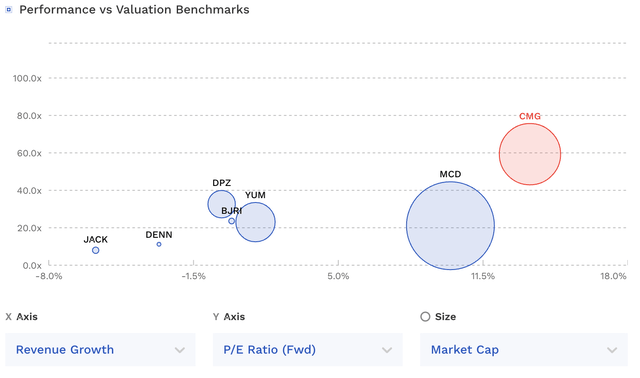

The following diagram displays Chipotle’s peer-based price-to-earnings ratio alongside its growth, illustrating why its multiples might be elevated.

Multiples (FinBox)

The next diagram adds substance to the aforementioned claim, showing that Chipotle has a best-in-class ROE and solid earnings-per-share growth. I pointed this out earlier in the article. However, I reiterated it in this section to emphasize its shareholder value pass-through (shareholder value isn’t just about price multiples).

Value Ratios (FinBox)

Absolute Valuation

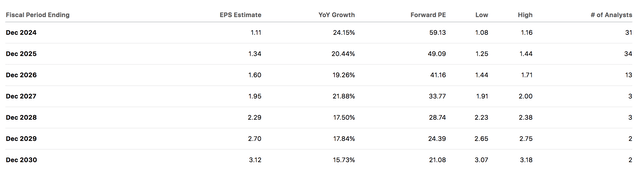

Many analysts use a price-to-earnings expansion formula to determine a stock’s absolute valuation. Although simple and inaccurate at times, this formula holds validity.

We decided to utilize the formula and calculated a fair price target of $87.76 by December 2025, which is significantly higher than Chipotle’s current stock price of $65.86 (closing price on 26/06/2024).

The stock doesn’t pay a dividend. Therefore, we don’t see any need to detract from this price forecast.

CMG Stock EPS Forecast (Seeking Alpha)

Technical Analysis

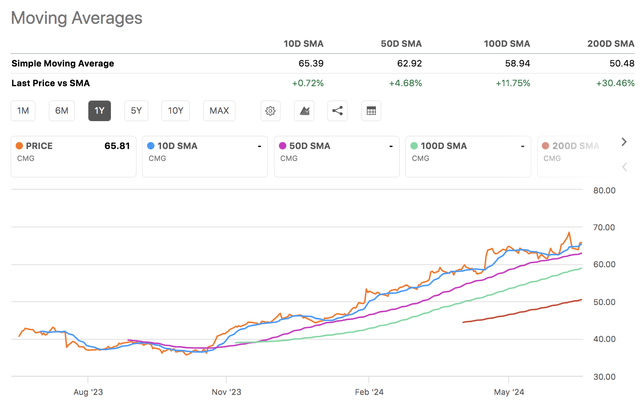

A technical analysis shows that Chipotle’s stock has formed a momentum pattern by exceeding its 10-, 50-, 100-, and 200-day moving averages. Although a pullback isn’t out of the question, Chipotle’s RSI of 57.51 is far from the overbought threshold of 70, suggesting its stock has additional room to roam into.

Unless the firm reports an underwhelming Q2 financial report or systematic risk occurs in the financial markets, we anticipate this trend to resume.

Seeking Alpha

Final Word

We assessed Chipotle Mexican Grill, Inc.’s fundamental aspects and market-based attributes to garner an updated understanding of its stock. Although we recognized a few risks, we remain bullish about the stock’s prospects based on its market expansion story and comprehensive shareholder pass-through attributes. Moreover, we see potential in the stock from a technical vantage point.

After considering various factors, we decided to maintain our Strong Buy rating on Chipotle stock.

Read the full article here