Financial Headwinds Challenge Bluebird Bio’s Breakthrough in Sickle Cell

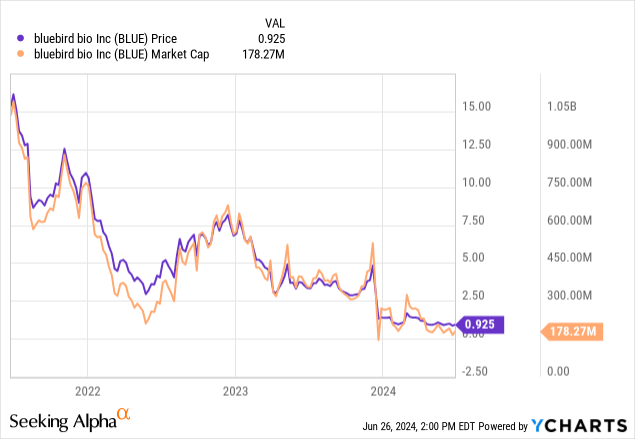

bluebird bio, Inc. (NASDAQ:BLUE) stock has plummeted 73% since my initial look nearly a year ago. Back then, bluebird was awaiting FDA approval for their sickle cell disease gene therapy, lovo-cel. Despite the potential in gene therapy, I recommended a “sell” for bluebird “due to financial risks, the need for long-term efficacy data, and the company’s precarious cash position.”

Its gene therapy, named Lyfgenia, has since been approved, but things are rarely as simple as crossing the regulatory finish line. A lot of logistics (e.g., manufacturing, marketing, etc.) go into launching a revolutionary treatment for a disease like sickle cell. Moreover, bluebird’s spiraling stock price creates a snowball effect of “bad.” It limits their ability to capitalize on stock equity without causing significant dilution for their investors.

The excitement surrounding this new technology has collided with the reality of convincing providers and patients to embrace it while lacking sufficient resources to market it.

Current treatment guidelines favor potentially curative therapies, such as gene therapy and hematopoietic stem cell transplantation, for adult patients with complications that cause severe disability or early death.

Sickle cell disease is a rare disease, as it is, with a U.S. prevalence of ~100,000. It’s likely that ~1/3 of patients have ‘severe disease’ (e.g., frequent pain crises, severe complications). Echoing this, bluebird estimates the market for Lyfgenia to be 20,000 patients. Moreover, CRISPR Therapeutics’ (CRSP) own gene therapy, Casgevy, was approved the same day for sickle cell disease. Given that there is no comparative data between the two, neither Casgevy nor Lyfgenia have an overt efficacy and/or safety advantage, essentially splitting the already small market in two. However, CRISPR does have the support of pharma giant ($122 billion market capitalization) Vertex Pharmacueticals (VRTX). Since the two that are marketing Casgevy have far more resources (e.g., cash, marketing experience in rare diseases) than bluebird, Casgevy is likely to win a lion’s share of the market.

In May, a report came out that CRISPR appears to be having a “faster rollout” than bluebird, which should be of no surprise. In their Q1 report, bluebird management predicted “85 to 105 patient starts” across its portfolio (which includes Zynteglo, Skysona, and Lyfgenia). Lyfgenia had just one patient start in May 2024. Bluebird did not provide specific guidance for Lyfgenia, but did say they expect to start seeing revenue from the product in Q3.

Financial Health

Unfortunately, bluebird has not yet filed a 10-Q for Q1 nor a 10-K for 2023 due to a delay. The company issued a notification in May.

As previously reported, the identified errors in the periods to be restated resulted from the Company’s identification of embedded leases and the application of its accounting policy for the treatment of non-lease components contained in lease agreements. The Company’s accounting policy required that lease and non-lease components in agreements with contract manufacturing organizations that are accounted for as leases be combined. The Company determined that it did not consistently combine such components. The Company does not expect the errors to result in any impact on its cash position or revenue.

So, this somewhat limits my ability to gauge their financial health. We do know, from their Q1 report, that their cash, cash equivalents and restricted cash balance stand at $264 million. Total revenue was $18.6 million in Q1, primarily due to increased Zynteglo product revenue. I cannot find any information on expenses or net loss since its Q3 report (in which, in terms of cash burn, they recorded a $71.7 million net loss). Assuming similar expenses, their cash runway extends into 2H 2025. However, this estimate is based on historical figures and is limited by the scarcity of information.

Management’s forward-looking cash runway estimate is “through Q1 2026,” assuming their “ability to achieve certain commercial revenue targets.”

The company does have an additional $100 million to draw upon the Hercules Capital loan, depending on certain milestones.

Risk/Reward Analysis and Investment Recommendation

In conclusion, bluebird bio has many obstacles to overcome and the most pressing one is their financial situation, especially as a “going concern.” Moreover, operational risks are substantial, as bluebird faces competition from companies with far more resources.

In my most recent article on bluebird, I laid out the steps that could turn things around for the company.

(…) a significant reduction in operating expenses, successful market penetration of Lyfgenia despite its high cost and safety concerns, and evidence of sustainable financial management that extends beyond short-term cash infusions. Additionally, positive long-term clinical data and patient outcomes (over a period of several years) could improve Lyfgenia’s market acceptance, potentially altering its competitive stance.

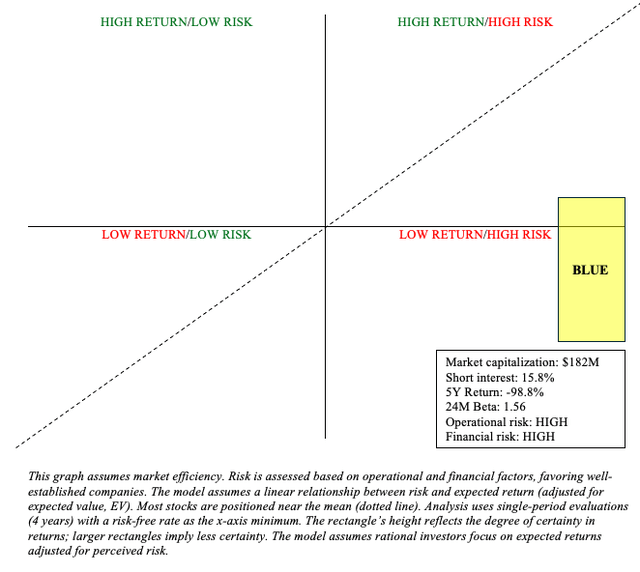

Not much has changed since December (maintain sell), except for the absence of key information ordinarily present within a 10-Q. These documents, required by the SEC, are vital to keeping investors informed. Without them, we are left in the dark regarding the company’s operational and financial standing. Admittedly, BLUE is, after all, largely priced for failure already, but one should never discount the possibility of a biotech stock falling another 98.8%+ in the next five years.

Author

The return (y-axis) above is muted due to the possibility of dilution ahead. For bluebird to raise just $200 million in a stock offering, this would result in dilution exceeding 100%. This is a risk common to microcap stocks such as BLUE. Other microcap risks include information asymmetry, low liquidity, and high volatility. Because of these concerns, I place BLUE primarily in Quadrant 4 (low return/high risk), and I believe the likelihood of long-term success is low.

There are some risks associated with my sell recommendation. Specifically, opportunity costs. BLUE may very well outperform the risk-free rate. They do, after all, have three revolutionary commercial products in areas with high unmet needs, despite current and future competition and patient/provider skepticism. This may attract acquirers or partners. Furthermore, BLUE’s high short interest may result in a short squeeze, causing significant upside in the stock.

bluebird bio, Inc. could serve as a lottery ticket in a barbell portfolio that allocates 90% of funds to lower-risk investments such as Treasuries and broad-market ETFs, with the remaining 10% going to speculative positions like BLUE. However, I’d rather put my cash in a security that doesn’t face imminent existential threats.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here