Investment Overview – Cabaletta’s Miraculous Recovery On Potential Best-In-Class Autoimmune Cell Therapy

I last covered Cabaletta Bio, Inc. (NASDAQ:CABA) in a note for Seeking Alpha in September last year, giving the Philadelphia-based biotech’s stock a “buy” rating. In that note, I provided an overview of the company’s progress since its IPO in 2019, which raised ~$75m at $11 per share.

The (relatively) unique aspect of Cabaletta’s business is that it is a cell therapy company, but rather than focusing its energies on the oncology market – a sector in which multiple cell therapies have been approved, with several generating revenues >$500m per annum, it is instead focused on autoimmune diseases.

While Cabaletta’s initial efforts did not generate much in the way of positive data – its CAART, or Chimeric AutoAntibody Receptor T cell approach led to two candidates entering studies in patients with mucosal pemphigus vulgaris, and myasthenia gravis respectively. Limited efficacy was demonstrated – hopes are higher for Cabaletta’s second approach – known as Chimeric Antigen Receptor T cells for Autoimmunity, or “CARTA.”

Using this approach, Cabaletta has developed a new candidate, CABA-201, which it describes as a “4-1BB co-stimulatory domain-containing fully human CD19-CAR T construct.”

Much of the reason that Wall Street is excited about this candidate stems from the success of a “CD19-CAR T construct employed in academic reports published in journals including Nature Medicine, Lancet Rheumatology, and the Journal of the American Medical Association”, according to Cabaletta’s 2023 annual report / 10K submission. The drug was used to treat patients in Germany by a collection of researchers and academics, with remarkable results – up to 15 patients have been treated successfully to date.

Cabaletta states that:

studies have employed a CD19-CAR T cell therapy incorporating a 4-1BB co-stimulatory domain following standard lymphodepletion with fludarabine and cyclophosphamide. According to reports to date, in patients with systemic lupus erythematosus, anti-synthetase syndrome, and systemic sclerosis, the 4-1BB containing CD19-CAR T cell therapy has led to robust improvement in clinical disease activity within three months of treatment through rapid and deep depletion of CD19-expressing B cells followed by return of healthy B cells within seven months of treatment.

These findings led several Wall Street analysts to issue “buy” ratings on Cabaletta stock, variously setting a price target of $16 per share, suggesting CABA-201 could generate ~$1.9bn, and $1.4bn in peak revenues, in the indications of lupus and myositis respectively, and naming the company as “one of the most compelling small-cap names in biotech.”

Before its development of CABA-201, Cabaletta’s stock looked in danger of being delisted, as it fell <$1 per share towards the end of 2022, but by the end of 2023, shares were trading at >$25 per share.

As such, my “buy” recommendation last September, when stock was priced at $19 per share, initially looked like being a good call, as shares quickly rose in value by >30%, but 2024 to date has been problematic for the company, and today, Cabaletta’s stock price has fallen to $7 per share (at the time of writing).

2024’s Sell-Off Explained – Pace of Progress, Manufacturing & Data Woes

2024 actually began well for Cabaletta, with the company receiving an FDA Fast Track award for CABA-201, and Orphan Drug Status in the treatment of systemic sclerosis (“SSc”).

At the end of February, however, the share price began to slide. By early April, the stock had sunk in value from >$25, to $17, then it fell rapidly again, to $11 per share by late April, and then again in June, to an 18-month low of ~$7 per share.

The reasons for the various drops are not crystal clear, but we can speculate they were caused by a few different issues. For example, Cabaletta has been using a China-based manufacturing partner, Wuxi, to help produce quantities of its drug products, but news surfaced in January this year that the US government was considering introducing a bill known as the “Biosecure Act”, which could prevent Wuxi working with any company that receives federal funding.

Cabaletta has warned that it is not in a position to manufacture all of its own product, and that a disruption to its contract with Wuxi would be detrimental to its business – the cost of manufacturing product in the US or Europe, for example, would be significantly more expensive.

Otherwise, my suspicion would be that, after the initial enthusiasm generated by the successful study discussed above, Cabaletta’s slow progress and lack of regular data updates has softened Wall Street’s stance, and perhaps its faith that Cabaletta has the right structure in place to successfully bring its drug to market.

The reason for the latest selloff in June is more clear. Cabaletta finally reported data from two patients dosed with CABA-201 in its Phase 1/2 RESET-Myositis and RESET-SLE trials. In a press release, Cabaletta’s Chief Medical Officer (“CMO”) David J. Chang commented as follows:

By demonstrating a potentially well-tolerated safety profile along with initial clinical and translational data consistent with the academic experience of a similar 4-1BB CD19-CAR T construct, we believe CABA-201 may be uniquely positioned to fulfill unmet patient needs across a broad range of autoimmune diseases

From a safety perspective, Cabaletta reported that CABA-201 was administered to both patients:

- During a four-day hospital stay, as currently required by the protocol, and was generally well-tolerated with no serious adverse events reported for either patient through the follow-up period.

- No evidence of cytokine release syndrome (“CRS”) or immune effector cell-associated neurotoxicity syndrome (“ICANS”) of any grade was observed for either patient through the follow-up period. Tocilizumab was not administered for either patient.

With an autologous cell therapy like CABA-201, a patient’s own cells are harvested and extracted, taken to a lab, engineered ex-vivo, and then reinfused back into the patient. This process requires a preconditioning regime not unlike chemotherapy, that can be difficult for patients, while there is a risk that reinfused cells can be rejected by the patient’s immune system, causing cytokine release syndrome, a dangerous side effect.

Thankfully, this part of Cabaletta’s study seems to have gone smoothly, although the CMO’s use of the work “potentially” in the above quote may, or may not, suggest Cabaletta itself harbors some concerns around safety.

On the efficacy side, Cabaletta said that:

- Complete B cell depletion was observed within 15 days post-infusion with CABA-201 in both patients. Both patients had early, transient leukopenia, as expected with the preconditioning regimen.

- CAR T cell expansion associated with CABA-201 reached its peak magnitude at day 15 post-infusion in both patients and the magnitude of expansion was consistent with the academic experience with a similar 4-1BB CD19-CAR T construct.

Cabaletta compares the effect of CABA-201 with that experienced by patients treated in the German studies, stating that, at Week 12, the patient with immune-mediated necrotizing myopathy (“IMNM”) experienced “a decline in creatinine kinase from 617 at infusion to 308 and a total improvement score (“TIS”) of 30″, and the patient treated for systemic lupus erythematosus (“SLE”) “demonstrated an improvement in the SLEDAI-2K (systemic lupus erythematosus disease activity index) score from 26 at baseline to 10.”

Whilst there are some encouraging signs in the data, the market may have been hoping for more of a treatment effect and more tangible signs of improvement in their condition, which seemed to happen rapidly with the German studies – this report seems to suggest the first patient treated with that drug showed a greater response than has been achieved to date with CABA-201:

signs of serologic remission were paralleled by clinical remission with proteinuria decreasing from above 2000 mg of protein per gram of creatinine to less than 250 mg of protein per gram of creatinine (Figure 1B), and the Systemic Lupus Erythematosus Disease Activity Index score (with the SELENA [Safety of Estrogens in Lupus National Assessment] modification) decreased from 16 at baseline to 0 at follow-up

When Cabaletta released its data, its shares traded at a value of ~$13, but two weeks later, they had sunk <$7.5.

Looking Ahead – Can Cabaletta Recover Market’s Trust As Competition Mounts?

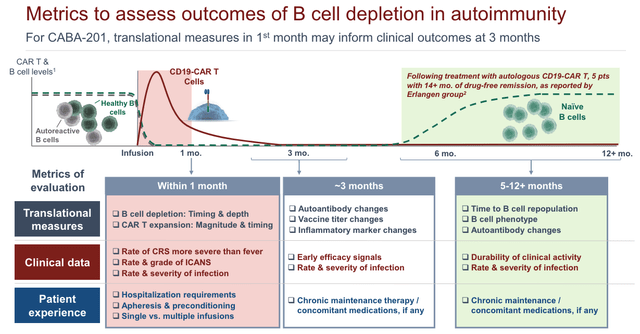

According to a recent corporate presentation, Cabaletta intends to 6 patients in up to nine different cohorts, treating different autoimmune conditions, including SLE, SSc, myasthenia gravis (“MG”), IMNM, and others. The company will also look at treating pemphigus patients without preconditioning.

There will be multiple metrics of evaluation, as shown below:

study evaluation metrics (presentation)

Cabaletts is promising more data from its myositis and SLE study cohorts this year, plus initial data in its SSc and gMG studies, which ought to provide more meaningful data and make it easier to judge whether CABA-201 is having a similar treatment effect as the drug used in Germany.

As such, if data is positive, then Cabaletta’s share price may be on track to recapture highs of >$25 per share because the company will be a front-runner in the race to bring a first autoimmune focused cell therapy to market. Autoimmune markets are vast, worth >$100bn per annum, so it would not be surprising to see Cabaletta’s market cap jump >$1bn on positive news.

In Q1 2024, Cabaletta reported a net loss, or cash burn, of $(25m), spending $22m on R&D, and a cash position of $223m. There is therefore a near 2-year funding cash runway in place, however I’d expect to see management complete a fundraising if its data shared later this year is positive.

Naturally, the risk is that CABA-201 fails to match the effects seen with the drug developed in Germany, and that risk is clearly weighing heavily on Cabaletta’s current share price. Unfortunately, this month’s data release did not provide the comfort the market was seeking, and there are competitors in the autoimmune cell therapy space as well.

For example, Kyverna Therapeutics (KYTX) completed a $319m IPO this February. The company has two CD-19 targeting, autoimmune disease directed CAR-T therapies in clinical studies, one autologous – using patient’s own cells, and one “allogeneic” – using donor cells.

Intriguingly, Georg Schett, M.D., one of the key figures behind the successful studies in Germany, is a member of Kyverna’s Scientific Advisory Board, although Kyverna stock has also been suffering after its latest data for its autologous therapy seemed to indicate a lack of durability of response.

Another Cabaletta rival is Cartesian Therapeutics (RNAC), which is developing a messenger-RNA based cell therapy indicated for autoimmune conditions, which may require a much gentler for of preconditioning, and has shown some promising early data – recently, Cartesian seems to have supplanted Cabaletta and Kyverna in Wall Street’s affections, with several VC’s issuing “buy” recommendations, Oppenheimer being one.

Concluding Thoughts – Am I Maintaining My “Buy” Rating On Cabaletta?

This is a tricky question to answer. Overall, I’d say I am still relatively impressed with Cabaletta’s progress to date, being able to rapidly transition into a new approach after its first approach did not show sufficient signs of success.

The Phase 1/2 studies of CABA-201 seem to be well organized and will surely provide significantly more insight into whether this therapy can be successful, so the optimal strategy, if you are a Cabaletta shareholder, may be to hold on and wait and see what that data looks like.

Of course, there is a risk that the data disappoints, in which case Cabaletta would be left more or less empty-handed, and the prospect of delisting / winding up of the company would presumably come into play at that point.

In terms of buying at today’s prices, the upside opportunity is apparent – any company that can bring an autoimmune-directed cell therapy to market that mimic’s the success of the one produced by researchers at University Hospital Erlangen, will be handsomely rewarded, as will its shareholders.

You can make the case that Cabaletta is keeping its cards close to its chest while carrying out its studies in a disciplined fashion, and not trying to curry favor with the market at this time, or you could make the case that the data already seems to have fallen below the standards of the drug whose MoA it is designed to mimic.

There is a lot of uncertainty in play in this space, as several companies attempt to replicate the success of the German studies, including Pharma giants Novartis (NVS), and Regeneron (REGN) – both could bid for a company like Cabaletta if it can show sufficient signs of progress.

Cabaletta is a risky investment opportunity, but an intriguing one if you are betting money you can afford to lose, with the rewards for success likely to include share price upside of >200%, in my view, which is why I am maintaining a “Buy” rating, but it is important to understand Cabaletta’s next set of data will need to show patients responding well to treatment. If that doesn’t happen, Cabaletta’s chances of success will start to look remote.

Read the full article here