Summary

I am positive about Remitly Global (NASDAQ:RELY) because I believe that RELY should continue to capture share from legacy channels in the remittance industry, given the superior value proposition it offers to customers relative to how things are traditionally done. RELY’s strong track record of capturing demand to drive growth is well seen when compared to peers. Importantly, RELY is at the inflection point where the adj. EBITDA margin should continue to ramp up in the coming quarters, and I expect this to help close the valuation gap between itself and PayPal Holdings.

Company overview

RELY is a mobile native remittances company focused on cross-border money transfers. Its main product is its core remittance platform via its mobile app. So far, the business has been categorized as a fast-growing company, where its revenue grew by almost eight times between FY19 and FY23. To gain a better sense of demand traction, RELY has processed a total send volume of $11.5 billion, up from $7 billion in FY19.

Large addressable market for cross border remittances

RELY

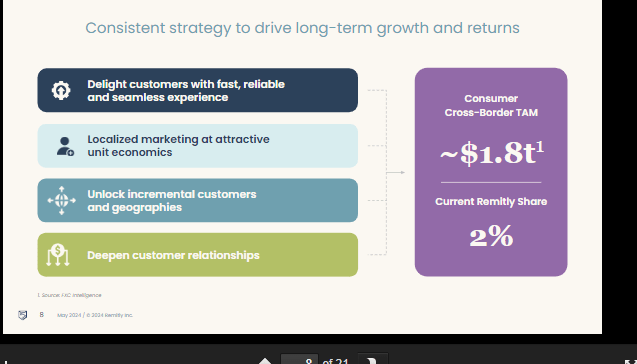

I believe the growth runway for RELY is extremely long given the large addressable market. Based on management estimates, the total consumer-cross-border TAM sits at around $1.8 trillion, and RELY currently only has just 2% market share. The vast majority of remittances are still being processed by legacy methods such as in-person remittances, bank transfers, or cash, and they still exist for good reasons. For one, there is still a relatively large portion of the unbanked population in the world that cannot readily use digital tools. Hence, I think the more realistic address market that RELY can immediately target is much lower (>$600 billion is the number management provided in the 2Q22 call). Even adjusting for that, the growth potential is still huge, as RELY still has <10% market share.

Importantly, the overall remittance TAM is likely to get larger as there will be more immigration moving forward, and more immigrants directly translates to more remittance occasions. This has been a trend since multiple decades ago, and the data shows that more immigrants lead to more remittances. This makes absolute sense because, generally, the remittance market is driven by immigrants sending money to support families in their home countries. This also plays well into the region on which RELY focuses most today: the US (67% of total revenue), which is the most popular remittance corridor in the world.

RELY is a disruptor

RELY

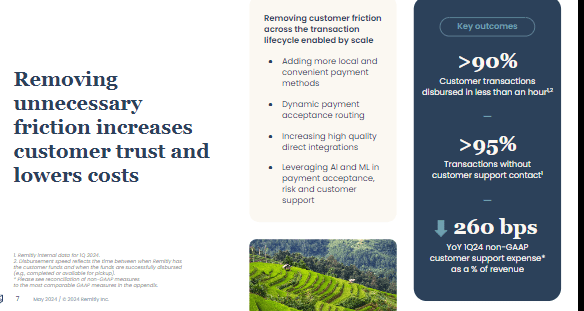

RELY, with its mobile native solution, is a disruptor in this industry that enables it to continue capturing share. My opinion is that RELY provides a strong customer value proposition for digital remittances in terms of convenience and ease of use. For instance, there is little visibility into the timing (when the cash will reach the other party) and procedure for the transfer when using in-person remittance channels. It is also very inconvenient, as customers are required to physically deposit cash at a designated location (high security risk too). This contrasts deeply with digital remittances, which are straightforward; all a consumer needs is a smartphone app, a debit or credit card, or even a bank account to fund a transaction. To put out some numbers, more than 90% of customer transactions are disbursed in less than an hour, and more than 95% of transactions are done without any human interaction.

Looking ahead, I don’t see any structural headwinds to digital adoption in the remittance space (unbanked populations are coming down as well). A report by Visa clearly points to consumers demanding digital solutions. At the industry level (digital remittance), it is expected to reach a size of ~$6.5 trillion worth of transaction value in 2028 (~mid-teens growth CAGR from 2024).

RELY growth outlook

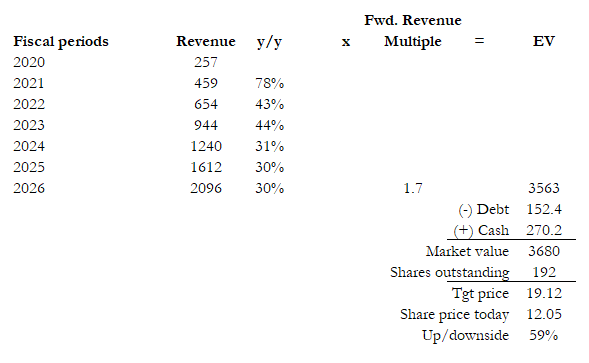

Source: Author’s calculation

I strongly believe that RELY can continue to grow at >30% for the foreseeable future, given the macro tailwinds and its solid track record of capturing growth. Despite that, RELY share price has been punished heavily over the past year, and I think there are a few reasons why:

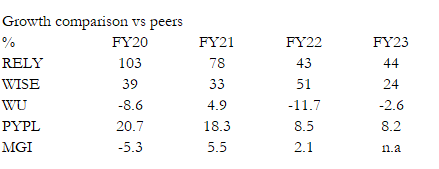

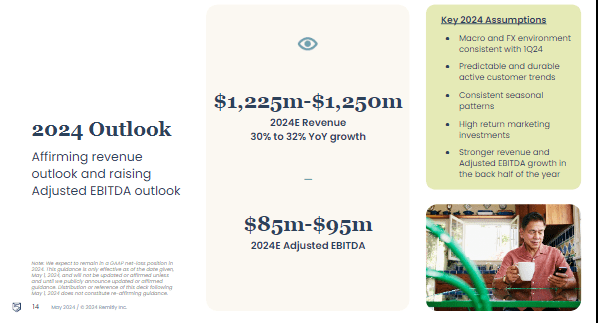

- Revenue growth slowed for 4 consecutive quarters (from ~40% in 1Q23 to 32% in 1Q24). I believe the decline in growth is mostly due to management focusing on profits, as the adj. EBITDA margin has improved significantly from 2.6% in 1Q23 to 7.2% in 1Q24 (apparently not reflected in the share price). The way I see it, the metric to track growth and whether RELY is winning share is overall send volume growth, which continues to grow at >30% (more than 10x faster than the overall remittances market).

- The rate fell for the first time on a y/y basis in 1Q24, and this probably led investors to believe that RELY is facing pricing pressure. I don’t think this is the case. The volatility in take rates is more likely due to the mix shift, which is heavily influenced by transaction size. For instance, US-to-India has an average higher transaction size but a lower take rate. Management literally said this in the latest earnings call: “Will, it’s a great question. I think the punchline answer to the take rate question is mix shift. So that’s within the normal range. There’s nothing that’s happening from a competitive standpoint in Q1 that changed that.” In fact, I see RELY should see strong pricing power ahead, given that digital disbursements are way better than cash pickup, and I expect consumers to be willing to pay for the convenience, security, and speed.

Source: Author’s calculation

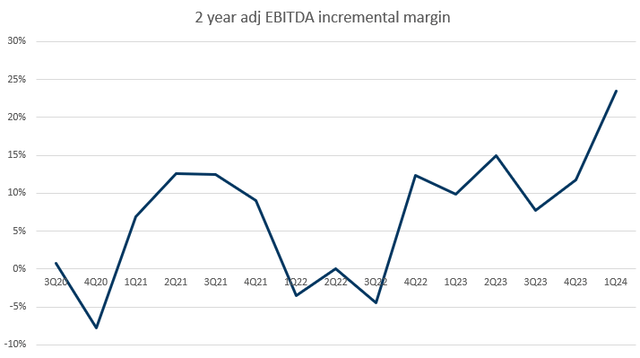

What I think is also not getting the attention it deserves is RELY ability to drive up profitability over the next few quarters. Incremental EBITDA margins have reached new heights, and this is without any one-off events like COVID. This step-up is organic and has translated to an adj. EBITDA margin expansion over the past few quarters. At the current pace, and assuming RELY continues to grow at 30%, margins should continue to expand at a rapid pace.

Valuation

Source: Author’s calculation Source: Author’s calculation

I believe RELY is worth 60% more than the current share price. My target price is based on FY26 revenue of ~$2.1 billion and a forward revenue multiple of 1.7x.

Revenue bridge: Revenue to grow at ~30% ahead using FY24-guided revenue growth as a baseline. Structural macro tailwinds and RELY’s ability to continue capturing share are key factors driving this level of growth.

Valuation justification: Among the peers (listed above), PayPal is the player that trades higher than RELY today on a forward revenue multiple basis, despite lower growth. My belief is that the difference in profitability (adj. EBITDA margin in this case) is the main reason why RELY trades at a discount. Thankfully, RELY has shown its ability to drive up margins, and incremental margin gains point to the potential of reaching similar levels of profitability over the next few years. As such, I am valuing RELY using PayPal’s current multiple of 1.7x.

Investment Risk

RELY operates financial transactions and has bank partnerships in many regulatory regimes that have differing compliance requirements. As these requirements may change, RELY business may be affected. Additionally, there are growing threats of cybercrime. Any form of security incidents would also cause reputational damage to RELY, as much of its consumer base expects reliable and safe service to transfer money.

Conclusion

My positive view on RELY is because of the strong macro tailwinds and RELY solid track record of growth. I believe RELY is well-positioned to capture significant share in the massive remittance market due to its superior customer value proposition. RELY’s ability to expand profitability further should help it to close the valuation gap vs. PayPal. That said, there are inherent risks that RELY has and investors should be aware of.

Read the full article here