XOMA Corporation (NASDAQ:XOMA) operates as a biotechnology royalty aggregator, acquiring economic rights to milestones and royalties from partnered approved or clinical-stage drugs. The company’s diverse IP across various development phases mitigates these risks. Some of the company’s notable IP generates royalties from Roche’s Faricimab for diabetic macular edema and age-related macular degeneration, Dsuvia from AcelRx Pharmaceuticals for acute pain, Ixinity from Medexus for hemophilia B, Xaciato from Organon for bacterial vaginosis, and Ojemda from Day One for pediatric low-grade glioma. Also, its recent acquisition of Kinnate Biopharma (KNTE) extended its IP portfolio into oncology. Nevertheless, while I think XOMA’s business is viable for the foreseeable future, I’m not sure the stock has the same explosive upside potential as other biotechs. Therefore, I deem XOMA a “hold,” but its preferred shares (NASDAQ:XOMAP) could fit well into to a diversified dividend portfolio.

Diversified IP: Business Overview

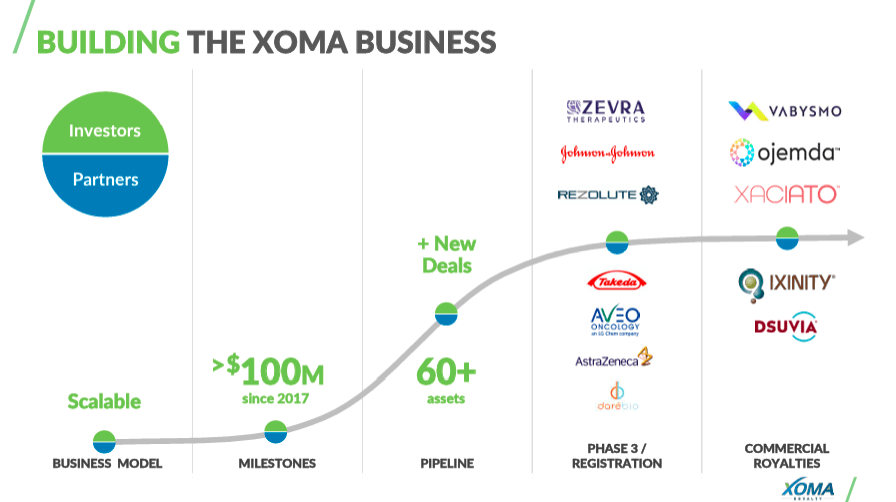

XOMA is a biotechnology royalty aggregator founded in 1981 and based in Emeryville, California. XOMA’s business model involves acquiring the rights of drug candidates to receive future payments after achieving milestones or obtaining royalty rates based on sales if the drugs are approved and launched commercially. You can think of XOMA as an “investment manager” of biotech IP rather than a typical biotech company with in-house R&D. XOMA funds biotech companies to advance their pipelines in a diverse portfolio that spans multiple therapeutic areas such as oncology, immunology, rare diseases, and acute pain. The pharmaceutical industry is inherently risky due to the high level of uncertainty about the success of its drug candidates.

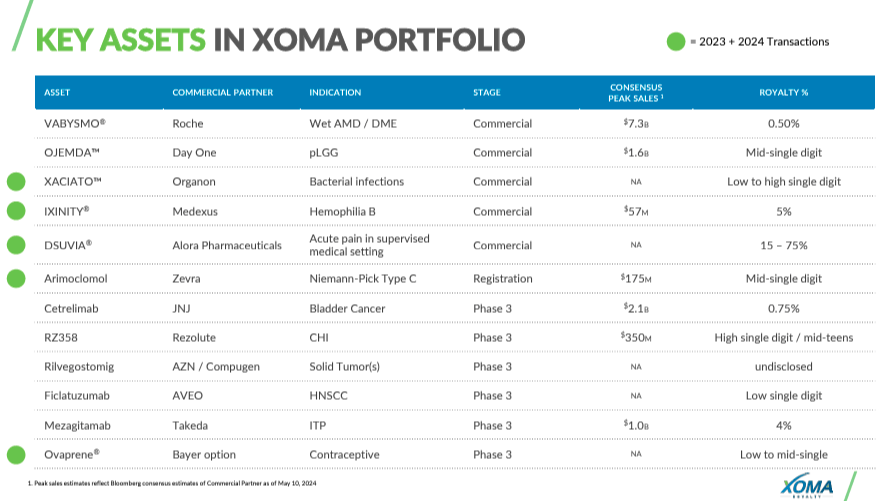

Currently, XOMA’s portfolio has over 70 assets. It includes several commercial and investigational drugs from various biotechnology firms spanning multiple phases of clinical trials. The key partners include large and smaller biotech companies and cover areas such as oncology, immunology, rare diseases, and acute pain.

Source: Corporate Presentation. May 2024.

For instance, XOMA receives royalties from Roche’s Faricimab, a drug indicated for the treatment of diabetic macular edema [DME] and age-related macular degeneration [AMD]. The royalty rate is 0.5% of the sales. In addition, XOMA’s portfolio has several other FDA-approved drugs, such as Alora’s Dsuvia, indicated for acute pain; Medexus’s Ixinity for hemophilia B; Organon’s Xaciato for bacterial vaginosis; and Day One’s Ojemda for relapsed or refractory pediatric low-grade [pLGG].

Also, XOMA has royalty rights to Rezolute’s RZ358 and other late-stage investigational drugs that could reach FDA approvals and generate additional revenues. For instance, RZ358 is a drug candidate indicated for congenital hyperinsulinism [CHI] currently enrolling patients for phase 3 clinical trials. If approved, this drug could provide XOMA with approximately 8% to 15% of net sales.

Akin to a Biotech Investment Manager

As previously noted, pharmaceuticals are inherently risky due to the uncertainty related to investigational drugs. However, XOMA’s diversified approach to IP can theoretically reduce this risk by spreading its exposure across diverse medical fields and development phases. Therefore, the failure of a single investigational drug has a less negative impact, but its upside is also reduced if they’re successful. The underlying benefit is that XOMA’s managers know how to pick winners and losers among biotech IP, focusing on drugs with promising clinical results to reduce the possibility of loss. This is essentially the same as an active investment manager in biotech IP.

Source: Corporate Presentation. May 2024.

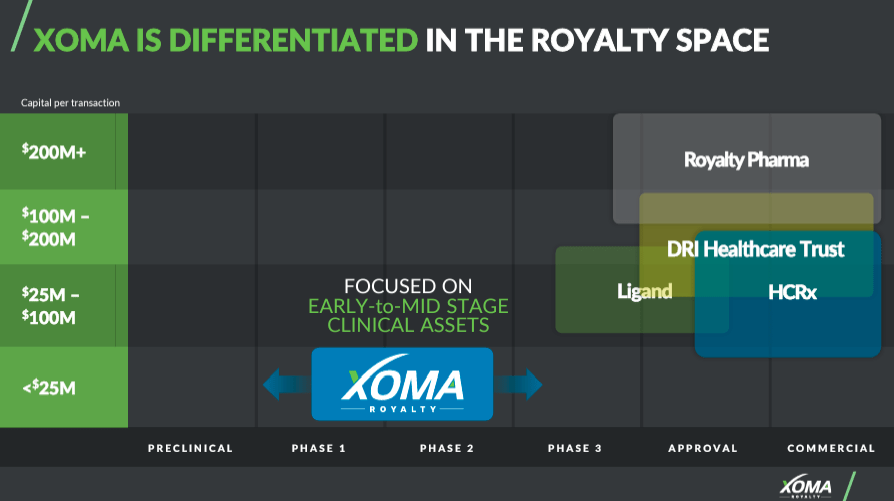

The idea is that XOMA can focus on acquiring rights to early-to-mid-stage clinical drugs, making transactions between $25.0 million and $100.0 million. This segment is different, as big pharma typically focuses on larger M&A transactions and assets in phase 3 or commercial stages. XOMA differentiates by addressing different segments of the market, capitalizing on early development assets that are riskier but also present high-reward prospects.

Latest IP Portfolio Developments

In April 2024, XOMA acquired Kinnate Biopharma Inc (KNTE) for approximately $120.0 million, including cash payment and estimated future payments from the CVR. This acquisition permits XOMA to grow its portfolio with KNTE’s oncology programs and benefits from future royalty and milestone revenues related to these assets. Using the CVR mechanism ensures that KNTE also benefits from the cash payout and future income from its assets. Should XOMA sell any of KNTE’s programs up to a year post-merger, 85% of the net proceeds will be allocated to CVR holders.

Unfortunately, KITE sold exarafenib and other assets to Pierre Fabre Laboratories before the acquisition, executed in March 2024. So, these gains are 100% distributed to the CVR holders. Exarafenib was KITE’s crown jewel IP to maintain a manageable transaction, but I imagine XOMA accepted KNTE selling it before the acquisition. This means that XOMA’s bet on KITE is mostly focused on the rest of KNTE’s IP, potentially promising in oncology but still mostly pre-clinical.

Source: Corporate Presentation. May 2024.

Since the acquisition, KNTE has operated as a wholly-owned subsidiary of XOMA, continuing to advance its pipeline. The investigational programs not sold to Pierre Fabre Laboratories include a c-MET inhibitor implicated in various cancers that have become unsusceptible to other treatments and a brain-penetrant CDK4 Selective Program that stops the overactivation of CDK4, leading to uncontrolled malignant cell proliferation in cancers. This drug crosses the blood-brain barrier [BBB] to overcome resistance in challenging cases. These preclinical drugs offer potential solutions for treating cancer resistance to other medicines. This last acquisition is part of XOMA’s efforts to expand its portfolio and provide a diversified income stream from approved and clinical-stage drugs.

Unattractive Equity: Valuation Analysis

From a valuation perspective, XOMA’s equity trades at a $266.5 million market cap. Its balance sheet holds $136.2 million in cash and equivalents plus $9.8 million in short-term royalty receivables. I think it’s sensible to add these two figures to estimate the company’s available short-term liquidity of $146.0 million. However, XOMA also holds $150.7 million in financial debt and makes roughly $3.5 million in quarterly interest payments.

I estimate XOMA’s latest quarterly cash burn was roughly $13.6 million. I obtained this figure by adding the company’s CFOs, CFIs, and preferred dividends. I think this is the correct cash burn approach because the company’s IP-related transactions are essentially CAPEX, and the payments to the preferred shares also result in cash outflows. This figure implies that XOMA’s cash runway is approximately 10.0 years, which is quite healthy.

Source: Seeking Alpha.

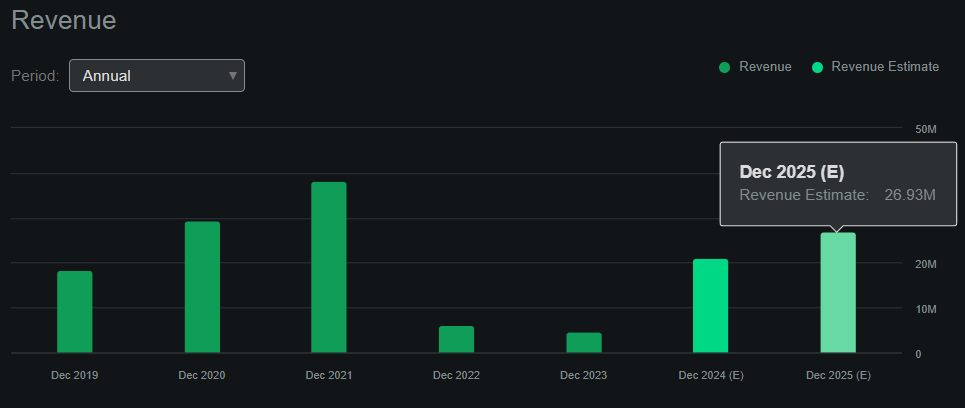

Moreover, according to Seeking Alpha’s dashboard on XOMA, the company’s revenues will probably pick up in the near term. XOMA is forecasted to generate roughly $26.9 million in revenues by 2025, a 28.2% increase compared to 2024. Most of this growth will likely stem from Ojemda’s recent FDA approval in April 2024 and its future commercialization. XOMA received $9.0 from this milestone and owns mid-single digit royalties on its sales, estimated at $500.0 million to $600.0 million in peak sales. Therefore, I think XOMA’s long-term viability seems secure for the foreseeable future based on these future cash flows, the diversity and potential of its IP portfolio, and its long cash runway.

Nevertheless, while I think XOMA’s business is viable for the foreseeable future, I’m not sure the stock has the same explosive upside potential as other biotechs. As you might imagine, diversification mitigates risks and somewhat caps the upside. Since XOMA often doesn’t wholly own the royalty rights to its IP, big wins such as Ojemda don’t translate into huge revenue streams for XOMA.

Moreover, the company doesn’t have direct control over the progress of its IP along FDA regulatory pathways because it’s often licensed to some other entity. Hence, unlike other biotech companies, XOMA isn’t potentially a few trials away from unlocking billions in revenue for shareholders. Instead, the company’s goal seems to remain in business with predictable cashflows to meet its obligations.

Source: TradingView.

Ultimately, the company’s forward P/S multiple is self-evidently high at 9.9. For context, XOMA’s sector’s median forward P/S is 3.5, so the stock equity seems somewhat pricy relative to peers. This is why I lean neutral on its equity. While its diverse portfolio is promising, and its business seems safe, its current valuation and ongoing cash burn don’t leave much room for upside or value accumulation.

Prefer the Preferreds: Risk Analysis

I don’t discount the unlikely possibility of a single IP becoming a homerun for XOMA, but from an investment perspective, we shouldn’t make that our base case. I’m neutral and rate the stock itself a “hold.” However, I believe that XOMA’s business is viable for the consistent payments to its debt and preferred shareholders. In that sense, the preferred shares might be a better alternative for investors, but as previously noted, they’re more of a dividend play than biotech itself. The preferred shares (XOMAP) yield roughly 8.5%, which is attractive for income investors. The company’s financials and future revenues with Ojemda suggest the yield is sustainable for those looking to diversify into biotech.

XOMAP’s dividend yield. Source: Seeking Alpha.

On the downside, it’s important to remember that XOMA’s revenue streams are diversified but could become somewhat concentrated over time. Since regulatory risks are inherent in biotech, a single negative FDA decision regarding an already approved IP could be devastating for income investors. But overall, I don’t think such a scenario is highly likely, making XOMAP a fine addition to a diversified dividend portfolio.

XOMAP over XOMA: Conclusion

On balance, XOMA’s business model is intriguing. On its face, I compare it to an investment manager of biotech patents and IP. This yields a relatively steady diversified set of revenue streams with some speculative potential inherent in biotech. However, while this approach mitigates downside risk, it also caps its upside potential. XOMA’s valuation and ongoing cash burn make it unattractive since it doesn’t hold the same explosive upside potential as regular biotech stocks. However, this business model seems appropriate for investors looking into steady dividend income via the preferred shares (XOMAP). Hence, I rate XOMA a “hold,” but I think XOMAP could be a fine addition to a diversified dividend portfolio at these levels.

Read the full article here