POWL’s Investment Thesis Remains Promising, Assuming Successful Data Center Monetization

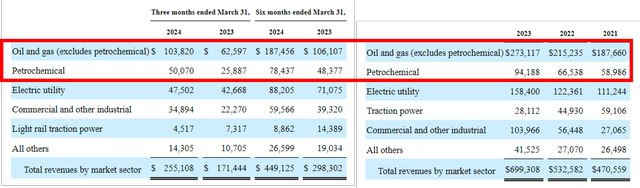

POWL’s Revenue Segments

Seeking Alpha

Powell Industries, Inc. (NASDAQ:NASDAQ:POWL) is a company that develops, manufactures, and sells custom-engineered electronic equipment and systems for multiple end markets, most notably the Oil and Gas and Petrochemical industry, which comprises 52.5% (-0.4 points YoY) of its FY2023 revenues and 60.3% in FQ2’24 (+2.6 points QoQ/ +8.7 YoY).

Given the relatively higher crude oil and LNG spot prices compared to pre-pandemic levels, it is unsurprising that the company has reported drastically higher overall revenues of $699.3M (+31.3% YoY) and EPS of $4.12 (+291.3% YoY) in FY2023.

The same double/ triple digit growths have also reported in FQ2’24 at $255.1M (+31.4% QoQ/ +48.7% YoY) and $2.75 (+38.8% QoQ/ +292.8% YoY), respectively, further underscoring POWL’s robust prospects during the oil/ gas boom.

With the OPEC+ further cutting output through the end of 2025, it is unsurprising that the US EIA has already expected the oil spot prices to remain elevated at $85 per barrel through H2’24 and 2025, with the higher for longer prices continuing to be a boon to the electronic company.

At the same time, the generative AI boom and resultant intensified capex on data centers have also triggered new growth opportunities for POWL, attributed to the increased electrical power demands and expanded utility/ data center projects.

The same has been observed in its financial performance, with commercial and other industrial segment (where data center is embedded) comprising $34.89M (+41.4% QoQ/ +56.6% YoY) or the equivalent 13.6% (+0.9 points QoQ/ +0.7 YoY) of its FQ2’24 revenues.

However, while POWL has highlighted “a foothold now with a lot of these folks (in data center) over the last three years or four years,” we believe that readers must temper their near-term expectations.

The management has highlighted that they “today could compete, but we’re not optimized to compete in that,” with the “space that started pretty strongly by some very large multinational competitors.“

This is because POWL’s products/ services remain at the qualification stage with limited sales contribution, despite the “potential for further penetration within the 4 walls of the data center.“

At the same time, it is undeniable that market competition will remain intense, with two of POWL’s direct competitor, Eaton (ETN) and Schneider Electric SE (OTCPK:SBGSF) (OTCPK:SBGSY), already reporting massive design wins with multiple data center REITs and hyperscalers thus far.

For example, Schneider reported that data center accounts for 21% of its FY2023 sales (at approximately $8.32B, based on author’s calculation), up drastically from the 12% reported for FY2022 (at approximately $4.39B).

The Schneider management also expects 2024 to bring forth “strong demand for System offers notably driven by trends in Data Centers, Grid Infrastructure investment, and increased investments across Process Industries served by both businesses,” with it remaining “the market leader in that space and we’d expect to maintain our strong positioning.“

Even so, POWL continues to boast a relatively promising multi-year backlog of $1.3B (inline QoQ/ +30% YoY), albeit with a relatively lumpy net bookings of $235.4M (+19.1% QoQ/ -53.6% YoY) in FQ2’24.

With a growing backlog, the management continues to report higher capex of $6.6M over the LTM (+40.7% sequentially) to incrementally expand its capacity in Houston by mid FY2025, building upon those recently completed in November 2023.

This is on top of POWL’s intensified R&D efforts of $2.28M (+15.7% QoQ/ +48% YoY), as part of the management’s initiative to release new products and drive future growth opportunities, likely in the data center end markets.

As a result of these efforts, we believe that the company appears to be well positioned to capture incremental data center revenues ahead, for so long that the management is able to push sampling into sales.

This is especially since the market is big enough to accommodate multiple players, with ETN projecting a robust data center market growth at a raised CAGR of +25% through 2025, compared to the original estimates of +16%.

POWL Is Attractively Undervalued Compared To Its Peers

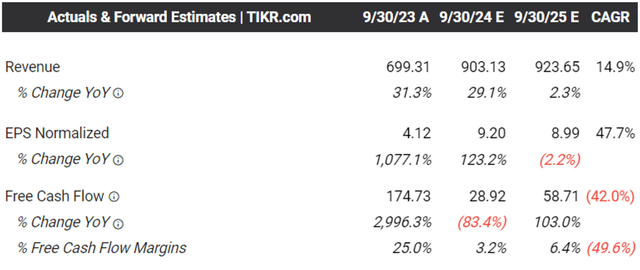

The Consensus Forward Estimates

Tikr Terminal

As a result of the great insights into its near-term performance, thanks to the growing backlog and intensified capex, it is unsurprising that the consensus have raised their forward estimates with POWL expected to generate an accelerated top/ bottom-line growth at a CAGR of +14.9%/ +47.7% through FY2025.

This is compared to the original estimates of +7.7%/ +13.2% and the historical growth of +3.1%/ +11.9% between FY2016 and FY2023, respectively, with the market seemingly convinced about the company’s ability to monetize the data center end market.

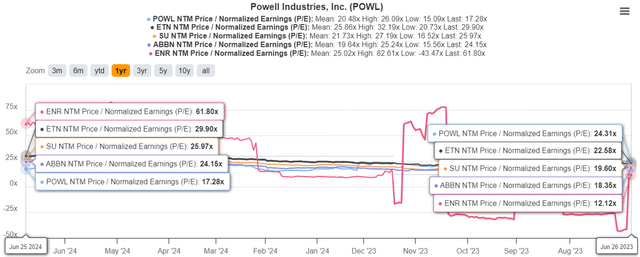

POWL Valuations

Seeking Alpha

Perhaps this is why the market has awarded POWL with the premium FWD P/E valuations of 17.28x, discounted compared to its 1Y mean of 20.48x though inflated compared to its 3Y mean of 10.01x.

However, when compared to its principal competitors, including ABB (OTCPK:ABBNY) at FWD P/E valuations of 24.15x, ETN at 29.90x, Schneider at 25.97x, Siemens (OTCPK:SMNEY) at 61.80x, and the sector median of 18.65x, it appears that POWL remains cheap here.

This is especially when comparing POWL’s top/ bottom-line growth projections through FY2025, to ABBNY at +4.8%/ +4%, ETN at +7.7%/ +13.3%, Schneider at +6.6%/ +14.8%, and Siemens at +7.8%/ +16.9%, respectively, with the former reasonably priced for the accelerated projected growth trend.

So, Is POWL Stock A Buy, Sell, or Hold?

POWL 1Y Stock Price

Trading View

For now, POWL has already charted new heights in May 2024, before returning much of those gains to retest its previous support levels of $151s.

Based on the LTM EPS of $8.20 (+450% sequentially) and the FWD P/E valuations of 17.28x, the stock is trading not too far from our fair value estimates of $141.60.

Unfortunately, based on the consensus FY2025 adj EPS estimates of $8.99, there appears to be a minimal upside potential of +2.2% to our long-term price target of $155.30.

At the same time, POWL’s dividend investment thesis appears to be underwhelming at forward yields of 0.70%, compared to the 4Y average yields of 3.04%, the sector median of 1.47%, and the US Treasury Yields of between 4.26% and 5.36%, mostly attributed to the stock’s +156.4% rally over the past year.

As a result of the unattractive risk/ reward ratio at current levels, we prefer to prudently rate POWL as a Hold (Neutral) here.

At the same time, with the stock already displaying a head and shoulder pattern since April 2024, it appears that there may be more volatility in the near term as the wider market also pulls back and “locked in their profits” during the recent heights.

Anyone looking to add may consider doing so after a deep pullback to its previous support level of $120s for an improved margin of safety, especially given the elevated short interest of 17.1% at the time of writing.

Before that, despite the promising prospects from its cyclical oil/ gas and (prospective) data center opportunities, we do not recommend anyone to chase POWL here.

Read the full article here