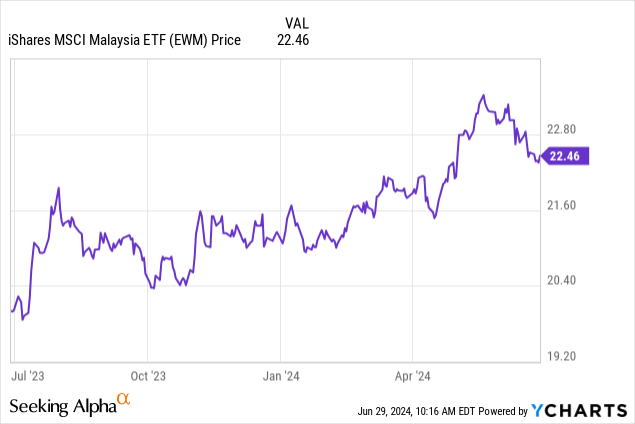

It’s been a torrid decade for investors in Malaysian large-cap equities, but thanks to a confluence of new tailwinds, the country’s fortunes may finally be turning. Since my last piece on iShares’ MSCI Malaysia ETF (NYSEARCA:EWM) (see EWM: Clearer Skies Ahead For Malaysian Stocks), Malaysian large-caps have bottomed out and, over the last year, delivered the best returns in Southeast Asia.

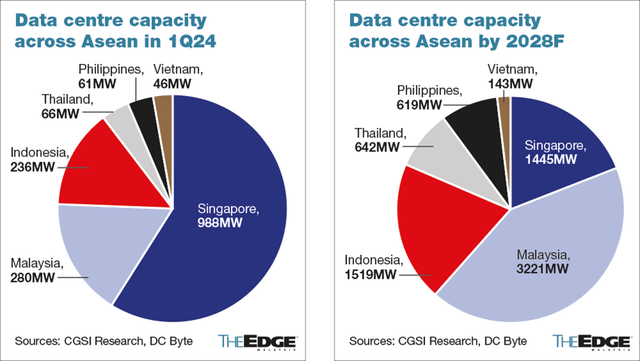

A key reason for this newfound optimism is a wave of new AI and cloud-driven investments in the country, particularly related to data centers. Malaysia has some unique advantages in this regard, most notably its cheap energy, geopolitical neutrality, and foreign-friendly investment policies, all of which have attracted the world’s ‘big tech’ names. Think Microsoft (MSFT) (cloud and AI infrastructure), Amazon (AMZN) (cloud services infrastructure), Nvidia (NVDA) (AI data centers), and Google (GOOG) (data center and cloud hub). Utilities, the second-largest EWM sector exposure, has naturally re-rated on the buildout of new power-hungry data centers, though expect the benefits to broaden out further over time, posing a tailwind to overall long-term earnings growth.

The Edge

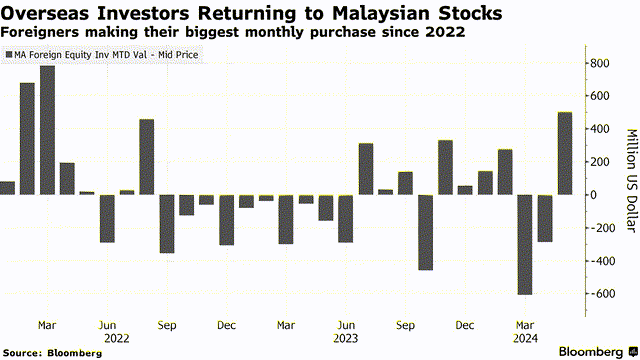

Beyond the fundamentals, Malaysia’s technicals also stand out in the region. Foreign sentiment, as reflected in near all-time participation levels, is still as low as it’s ever been – even after a recent upturn in buying activity for the more obvious data center beneficiaries.

Bloomberg

Complementing the prospect of a foreign bid is buying support from local institutional funds – likely in reaction to the government’s call last year for a larger domestic allocation. In a market tightly held by a handful of institutions and where free float is low, incremental inflows will have an outsized impact on stock prices and should thus, deliver some upside surprises down the line. Valuation-wise, EWM isn’t priced that expensively either relative to forward earnings, so the setup for Malaysian stocks remains compelling.

JPMorgan

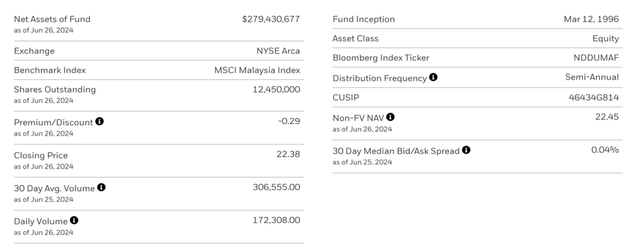

EWM Overview – The Largest and Most Liquid Malaysia Pure Play

The iShares MSCI Malaysia ETF is the only US-listed vehicle for access to Malaysian equities. For context, this is a fund that tracks the MSCI Malaysia Index, a basket of the country’s largest companies. This hasn’t been a particularly exciting geography for investors, as reflected in EWM’s relatively small ~$279m of managed assets. Still, the fund’s expense ratio is competitive at 0.5%, and liquidity is not an issue, with the bid/ask spread at ~4bps. Thus, as a cost-effective option for single-country exposure, EWM is as good as it gets.

iShares

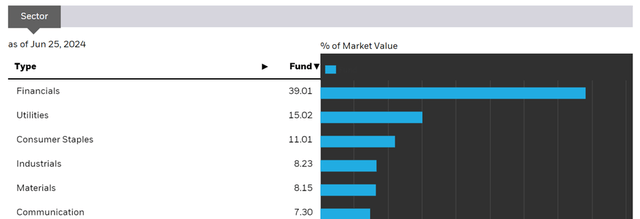

EWM Portfolio – More Top Heavy and Concentrated than Before

In line with last year, Financials remains the top EWM sector allocation at a broadly unchanged ~39%. The big change, though, is the exposure to Utilities, now a 15.0% allocation (vs. high-single-digits % previously) following a big AI/data center-led rally for the sector. Other notable sector exposures include Consumer Staples (down to 11.0%), Industrials (up to 8.2%), and Materials (unchanged at 8.2%). In total, EWM’s concentration has increased for its top two (54.0%) and top five sectors (81.4%), so investors should be mindful of the top-heavy portfolio.

iShares

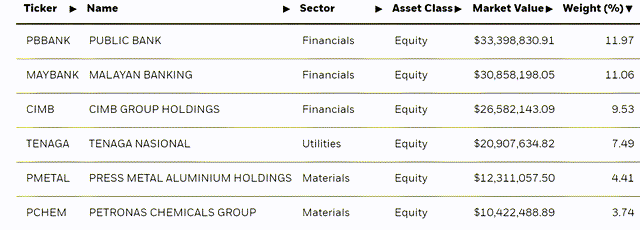

The single-stock composition, in line with the Financials sector concentration, continues to be led by Malaysia’s three big banks – Public Bank (OTCPK:PBLOF) (12.0%), Malayan Banking (OTCPK:MLYBY) (11.1%), and CIMB Group (OTCPK:CIMDF) (9.5%). The key changes, on the other hand, are the significantly increased holding in Malaysia’s grid operator, Tenaga Nasional (OTCPK:TNABY) at 7.5%, as well as other names exposed to the AI/data center theme like construction company Gamuda (2.6%) and YTL Power (2.4%). Also notable is that the portfolio has been narrowed to 32 holdings, with the top five stocks now contributing a larger 44.5% (~33% from the big three banks). Thus, EWM’s single-stock concentration will also be worth keeping an eye on

iShares

EWM Performance – The Pick of Southeast Asia

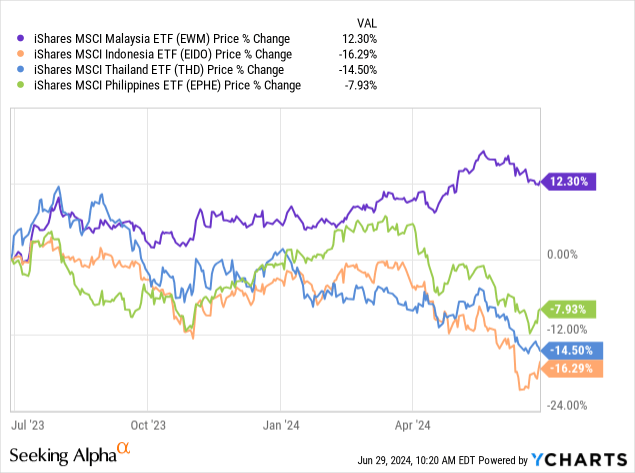

Along with the rest of Southeast Asia, EWM has been on a steady decline over the last decade, with an annualized -3.3% total return. Toward the second half of 2023, on the other hand, Malaysian equities finally caught a bid, as evidenced by the fund’s low-teens % one-year return and +7.2% gain year-to-date. By comparison, iShares’ MSCI Philippines ETF (EPHE), iShares’ MSCI Indonesia ETF (EIDO), and iShares’ MSCI Thailand ETF (THD) are all in the red this year.

While there is a very decent ~3% yield on offer and good defensiveness (0.51 beta vs the S&P 500 (SPY)), Malaysia’s selling point is really its growth potential. The latest new theme is the country’s success in attracting some hefty data center investments (mainly for AI and cloud) from both sides of the US-China divide. Expectations have therefore been rebased higher and the more obvious beneficiaries (e.g., large-cap utility and construction stocks) have re-rated.

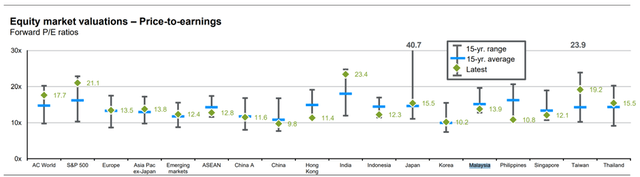

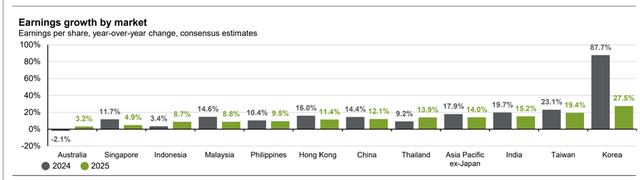

Yet, utility valuations in the low to mid-teens forward earnings indicate sentiment isn’t all that stretched relative to the prospect of a multi-year capex cycle. Similarly, EWM’s benchmark MSCI Malaysia index is currently on offer at ~14x forward P/E – very reasonable relative to consensus estimates for +15%/+9% earnings growth through 2024/2025.

JPMorgan

Final Say

Malaysia has not been a happy hunting ground for investors in the past, but the times may be a-changing, with many large-caps now emerging as ‘picks and shovels’ AI beneficiaries. Balanced with the fact that this is a market 1) still off the foreign investor radar and 2) priced at a very reasonable earnings multiple, and you have a quite favorable risk/reward here, in my view.

Read the full article here