Written by Sam Kovacs

Introduction

In a recent article titled “Sell Alert: 3 Dividend Aristocrats that will kill your passive income snowball” I made the case that for dividend investors that wanted to see their income compound at phenomenal rates, blindly investing in popular Dividend Aristocrats was not the way to go.

You see, our methodology is quite simple: based on how long you’ve got to retire (or if you’re already retired) find the stocks which will give you the most bang for your buck when it comes to dividends.

This can be achieved by balancing out dividend yield and dividend growth in the correct dosage.

Author’s art

If you do this right, then your dividends will snowball. I explained this in detail in an article humbly titled “Sam’s Dividend Income Snowball Retirement Masterclass“:

Imagine you are at the top of a hill, holding a snowball. This snowball represents the dividends you’ll receive in the first year you start investing. Of course, the size of this snowball is determined by two factors: how much cash you can invest into dividend stocks, and the dividend yield of the stocks which you chose to buy.

More cash creates a bigger snowball, as does a higher yield. Now, as you let go, the snowball begins to roll down the hill.

As the snowball rolls down the hill, it starts to gather more snow, becoming larger and larger. This gathering of snow symbolizes the growing dividend checks you receive. When you reinvest dividends, this packs more snow onto the snowball.

If you’re not yet retired, and are making monthly contributions towards your portfolio, this too packs on more snow. This reinvestment increases your principal, which in turn generates more dividends in the next cycle, causing the snowball to grow faster and faster.

Now, consider the slope of the hill. This slope represents the growth rate of your dividends. Stocks with higher dividend growth rates cause the snowball to gain momentum more quickly.

The problem, I argued with many dividend aristocrats is that they have been growing their dividends for so long that they’ve essentially driven themselves out of the dividend competition: Each year you increase makes it harder to increase by the same relative amount the next year.

Increasing by 10% when you pay out $1mn is easy. Increasing by 10% when you pay out $10bn in dividends is another matter.

Some of these companies are viewed as safe, stable, blue chip steady eddy’s and as such have very high valuations relative to their earnings, and to their dividends (that is to say they have a low yield).

(Cough…Ahem…Walmart (WMT)…Cough)

Of course this is the case of some Dividend Aristocrats, not all of them.

So in this article I wanted to highlight that if I was forced to retire on 10 stocks, that they could only be dividend aristocrats, then I could still build a suitable list of stocks.

Now it should be noted that I don’t think a 10 stock portfolio makes sense for anyone, except someone who is starting from scratch and wants to progressively add more stocks over the course of a year or two. In that case, a 10 stock portfolio might make sense. But even then, it would be a transitory phenomenon.

The Current Dividend Aristocrats list

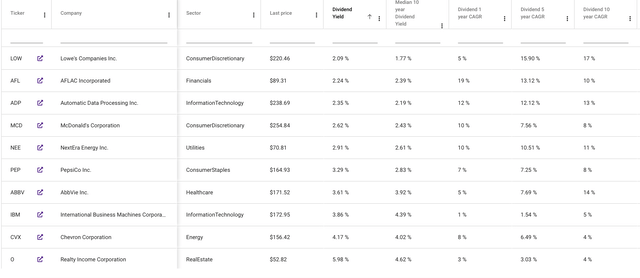

Below I compiled the current list of Dividend Aristocrats and sorted them by dividend yield.

In the second column I included the median 10-year dividend yield, and in the 2 last columns I included the 1 year and 5 year dividend CAGR.

| Company | Last price | Sector | Dividend Yield | Median 10 year Dividend Yield | Dividend 1 year CAGR |

Dividend 5 year CAGR |

| Realty Income (O) | $52.82 | Real Estate | 5.98% | 4.62% | 2.94% | 3.03% |

| Franklin Resources (BEN) | $22.35 | Financials | 5.55% | 3.32% | 3.33% | 3.58% |

| Amcor Plc (AMCR) | $9.78 | Materials | 5.11% | 4.98% | 2.04% | 1.16% |

| Federal Realty Investment Trust (FRT) | $100.97 | Real Estate | 4.32% | 3.28% | 0.93% | 1.34% |

| T. Rowe Price Group (TROW) | $115.31 | Financials | 4.30% | 2.82% | 1.64% | 10.29% |

| Chevron (CVX) | $156.42 | Energy | 4.17% | 4.02% | 7.95% | 6.49% |

| Stanley Black & Decker (SWK) | $79.89 | Industrials | 4.06% | 1.97% | 1.25% | 4.18% |

| J.M. Smucker Company (SJM) | $109.04 | Consumer Staples | 3.89% | 2.80% | 3.92% | 4.51% |

| International Business Machines (IBM) | $172.95 | Information Technology | 3.86% | 4.39% | 0.60% | 1.54% |

| Consolidated Edison (ED) | $89.42 | Utilities | 3.71% | 3.65% | 2.47% | 2.32% |

| Hormel Foods (HRL) | $30.49 | Consumer Staples | 3.71% | 1.99% | 2.73% | 6.11% |

| AbbVie (ABBV) | $171.52 | Healthcare | 3.61% | 3.92% | 4.73% | 7.69% |

| Medtronic plc.(MDT) | $78.71 | Healthcare | 3.56% | 2.15% | 1.45% | 5.33% |

| Kimberly-Clark (KMB) | $138.20 | Consumer Staples | 3.53% | 3.27% | 3.39% | 3.44% |

| Clorox Company (CLX) | $136.47 | Consumer Staples | 3.52% | 2.67% | 1.69% | 4.56% |

| Johnson & Johnson (JNJ) | $146.16 | Healthcare | 3.39% | 2.70% | 4.20% | 5.47% |

| Archer-Daniels-Midland Company (ADM) | $60.45 | Consumer Staples | 3.31% | 2.76% | 11.11% | 7.39% |

| Exxon Mobil (XOM) | $115.12 | Energy | 3.30% | 3.80% | 4.40% | 1.77% |

| PepsiCo (PEP) | $164.93 | Consumer Staples | 3.29% | 2.83% | 7.11% | 7.25% |

| Coca-Cola Company (KO) | $63.65 | Consumer Staples | 3.05% | 3.14% | 5.43% | 3.93% |

| Target (TGT) | $148.04 | Consumer Discretionary | 3.03% | 2.87% | 1.82% | 11.16% |

| NextEra Energy (NEE) | $70.81 | Utilities | 2.91% | 2.61% | 10.16% | 10.51% |

| Genuine Parts Company (GPC) | $138.32 | Consumer Discretionary | 2.89% | 2.75% | 5.26% | 5.57% |

| Sysco (SYY) | $71.39 | Consumer Staples | 2.86% | 2.50% | 2.00% | 5.51% |

| C.H. Robinson Worldwide (CHRW) | $88.12 | Industrials | 2.77% | 2.31% | 0.00% | 4.06% |

| Atmos Energy (ATO) | $116.65 | Utilities | 2.76% | 2.42% | 8.78% | 8.92% |

| Air Products and Chemicals (APD) | $258.05 | Materials | 2.74% | 2.36% | 1.14% | 8.82% |

| Cincinnati Financial (CINF) | $118.10 | Financials | 2.74% | 2.74% | 8.00% | 7.66% |

| McDonald’s (MCD) | $254.84 | Consumer Discretionary | 2.62% | 2.43% | 9.87% | 7.56% |

| Procter & Gamble Company (PG) | $164.92 | Consumer Staples | 2.44% | 2.77% | 6.99% | 6.18% |

| McCormick & Company (MKC) | $70.94 | Consumer Staples | 2.37% | 1.80% | 7.69% | 8.06% |

| Illinois Tool Works (ITW) | $236.96 | Industrials | 2.36% | 2.20% | 6.87% | 6.96% |

| Automatic Data Processing (ADP) | $238.69 | Information Technology | 2.35% | 2.19% | 12.00% | 12.12% |

| Aflac (AFL) | $89.31 | Financials | 2.24% | 2.39% | 19.05% | 13.12% |

| Abbott Laboratories (ABT) | $103.91 | Healthcare | 2.12% | 1.87% | 7.84% | 11.44% |

| Lowe’s Companies (LOW) | $220.46 | Consumer Discretionary | 2.09% | 1.77% | 4.55% | 15.90% |

| PPG Industries (PPG) | $125.89 | Materials | 2.07% | 1.63% | 4.84% | 6.25% |

| Cardinal Health (CAH) | $98.32 | Healthcare | 2.06% | 2.76% | 1.00% | 1.00% |

| Colgate-Palmolive Company (CL) | $97.04 | Consumer Staples | 2.06% | 2.31% | 4.17% | 3.06% |

| General Dynamics (GD) | $290.14 | Industrials | 1.96% | 2.11% | 7.58% | 6.84% |

| Emerson Electric Company (EMR) | $110.16 | Industrials | 1.91% | 2.79% | 0.96% | 1.39% |

| Caterpillar (CAT) | $333.10 | Industrials | 1.69% | 2.59% | 8.46% | 6.48% |

| Albemarle (ALB) | $95.52 | Materials | 1.68% | 1.38% | 0.00% | 1.71% |

| Becton, Dickinson and Company (BDX) | $233.71 | Healthcare | 1.63% | 1.41% | 4.40% | 4.82% |

| A.O. Smith (AOS) | $81.78 | Industrials | 1.57% | 1.50% | 6.67% | 7.78% |

| Chubb Limited (CB) | $255.08 | Financials | 1.43% | 1.98% | 5.81% | 3.94% |

| Nucor (NUE) | $158.08 | Materials | 1.37% | 2.61% | 5.88% | 6.19% |

| Linde Plc (LIN) | $438.81 | Materials | 1.27% | 1.94% | 9.02% | 9.70% |

| Walmart (WMT) | $67.71 | Consumer Staples | 1.23% | 1.93% | 9.21% | 3.27% |

| Pentair plc.(PNR) | $76.67 | Industrials | 1.20% | 1.83% | 4.55% | 5.02% |

| Expeditors International of Washington (EXPD) | $124.79 | Industrials | 1.17% | 1.31% | 5.80% | 7.86% |

| Nordson (NDSN) | $231.94 | Industrials | 1.17% | 1.02% | 4.62% | 14.21% |

| Dover (DOV) | $180.45 | Industrials | 1.13% | 1.95% | 0.99% | 1.22% |

| Church & Dwight Company (CHD) | $103.68 | Consumer Staples | 1.09% | 1.33% | 4.15% | 4.52% |

| Ecolab (ECL) | $238.00 | Materials | 0.96% | 1.13% | 7.55% | 4.38% |

| Sherwin-Williams Company (SHW) | $298.43 | Materials | 0.96% | 0.93% | 18.18% | 13.67% |

| W.W. Grainger (GWW) | $902.24 | Industrials | 0.91% | 1.77% | 10.22% | 7.32% |

| S&P Global (SPGI) | $446.00 | Financials | 0.82% | 1.00% | 1.11% | 9.81% |

| Cintas (CTAS) | $700.26 | Industrials | 0.77% | 1.02% | 17.39% | -11.94% |

| Brown & Brown (BRO) | $89.41 | Financials | 0.58% | 0.97% | 13.04% | 10.20% |

| Roper Technologies (ROP) | $563.66 | Industrials | 0.53% | 0.57% | 9.89% | 10.15% |

| West Pharmaceutical Services (WST) | $329.39 | Healthcare | 0.24% | 0.48% | 5.26% | 5.92% |

Refining the list

The task of cutting from 60+ to 10 is quick and fast to start with then gets slower as we get closer to the final list.

To start with I will cut out all 26 stocks which yield less than Lowe’s (LOW). All of those stocks which yield 2% or less don’t have anywhere near the growth rates to justify these small yields.

What do I mean by that?

Let’s compare two stocks, one that will make the list of 10, and a few from this subset that I just cut.

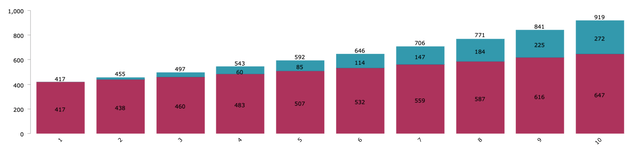

Chevron (CVX) currently yields 4.17%. Last year it increased its dividend by 8%. Over the past 10 years it has averaged 4.3% dividend growth. During the past 5 years it has averaged 6.5%.

By how much do we believe it will grow over the next 10 years? 5% seems like a reasonable benchmark.

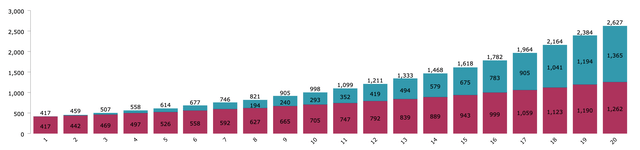

If you invest $10K in CVX at the current price, and reinvest dividends every year at the current yield while the dividend grows at 5% per year, then in 10 years you can expect to receive $919 in annual dividends.

CVX 10 Year Dividend Snowball (Dividend Freedom Tribe)

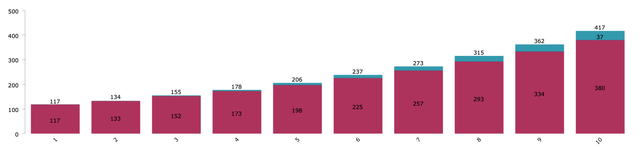

Now let’s compare that to the stock with the highest 5 year growth rate in those 26 that I’m cutting: Nordson (NDSN)

Nordson has been growing its dividend at a 14% CAGR over the past 5 years and over the past decade. Sure in the last year it increased by just 5%, but for the sake of proving a point, let’s assume that the dividend continues to increase at 14% per annum in upcoming year. NDSN currently yields 1.17%.

We’ll simulate how a position in NDSN will snowball over time.

NDSN 10 Year Dividend Snowball (Dividend Freedom Tribe)

You wouldn’t even get half the income 10 years from now.

The more astute of you, however, would realize that the relation of NDSN to CVX dividends went from about 1/4 in year 1 to about 4/9ths in year 10.

Of course a higher growth rate will always eventually catch up with a lower growth rate, it is bound by the laws of compounding.

But in the case of CVX vs NDSN, the NDSN income would finally overtake the CVX income in year 25.

And that assumes that you can actually achieve the 14% dividend growth every year for the next 25 years. Something which is harder to bank on, given it suggests it would need to increase by a factor of 25x.

The message is quite clear: while low yield & high dividend growth eventually beats high-yield & low growth, it really only makes sense for investors who have decades before retirement.

And even then, you’d want to stick to those that are able to grow their dividends at least in the teens, if you’re focusing on stocks with yields less than 2%. Less than 1.5%, and I’d be looking at least for 20% annual dividend growth potential.

Low yield & low growth is a dividend snowball’s death wish.

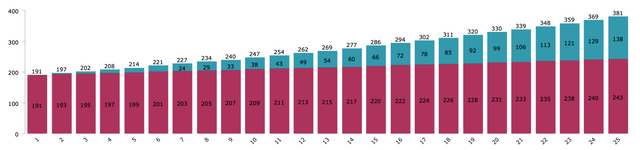

Let’s look at Emerson Electric (EMR) as an example.

The stock currently yields 1.91%. During the last decade, it has grown its dividend at a 2% CAGR. This has slowed down to a 1.4% CAGR over the past 5 years, and to just a 1% increase this last year.

Now let’s say you were going to invest $10K in EMR and reinvest dividends every year, while the dividend continues to grow just at 1% per year. Then in year 10 you’d expect $247 in annual income, and in year 25 you’d expect $381 in annual income.

EMR 25 Year Dividend Snowball (Dividend Freedom Tribe)

If we’re using our snowball metaphor, you’re trying to get a snowball going by dropping a snowflake onto a 0.5 degree slope. It’s not gonna happen.

Cardinal Health (CAH), Colgate (CL), Walmart (WMT), Chubb (CB) are all in that category: dividend snowflakes.

Further refining: favorite business models

At this point, I’m at a crossroads in my selection because there are a lot of these business which I fundamentally like, just not at these prices.

In fact, the following is true of virtually all of the stocks on this list: At the right price, they are a buy. The reason I discarded the 26 above is that they’ve been at high prices and low yields for so long, that the perspective of them trading at an attractive yield in the near future seems quite remote.

So from the lower yielding to higher yielding, these are some of my favorite business models.

- Lowe’s (LOW): The US remains undersupplied in homes, which provides a good tailwind in upcoming years.

-

Aflac (AFL): The rising healthcare costs and aging population ensure steady demand for supplemental insurance.

-

Automatic Data Processing (ADP): Increasing automation and a growing gig economy boost demand for advanced payroll and HR solutions.

-

Procter & Gamble (PG): Strong brand portfolio and global consumer reach ensure consistent revenue growth in essential goods.

-

McDonald’s (MCD): Expanding global presence and innovative delivery services drive long-term growth in fast food.

-

Air Products in Chemicals (APD): Leading position in hydrogen and clean energy technologies supports future industrial demand.

-

NextEra Energy (NEE): A leader in renewable energy, well-positioned to capitalize on the global shift towards green energy solutions.

-

Target (TGT): Strong digital sales growth and effective supply chain management bolster its competitive edge in retail.

-

Coca-Cola (KO): Diversified beverage portfolio and strong global distribution network ensure stable demand.

-

PepsiCo (PEP): Combination of food and beverage segments provides diversified revenue streams and resilience against market shifts.

- Exxon (XOM): Leading oil major. Integrated model, large barriers to entry.

-

Medtronic (MDT): Innovation in medical devices and a focus on chronic disease management support long-term healthcare needs.

-

AbbVie (ABBV): Robust pharmaceutical pipeline and strong performance in immunology and oncology drive sustainable growth.

-

IBM (IBM): Pioneering in AI and cloud computing services positions it well for future technological advancements.

-

Chevron (CVX): Integrated energy operations and low cost per barrel.

-

T. Rowe Price (TROW): Strong asset management performance and moat in retirement accounts.

-

Federal Realty Investment Trust (FRT): High-quality retail properties in prime locations offer stable rental income and capital appreciation.

-

Realty Income (O): Focus on high-quality tenants and long-term leases provides reliable income and financial stability.

Not to say the others don’t have great business models, but these are by far my favorite, and are not tainted by accounting scandals, legal woes, or other pains in the neck.

Now this has helped a lot and reduces our list to just 18 stocks.

If we were going to retire with just 10 stocks, we’d try and strive for as much diversity as possible.

So we wouldn’t want PEP & KO, just one of both. We wouldn’t want O and FRT, just one of both, and so on.

So I’ll remove KO because PEP has proven a track record of growing faster and PEP yields more today. I’ll remove FRT, MDT and XOM for the same reasons.

Down to 14, 4 still need to be axed.

I’ll remove TGT because if we keep just one consumer discretionary stock it should be MCD, I’ll remove APD because growth has slowed in the past couple years, I’ll remove PG because once again PEP is better in the Staples category, and I’ll remove TROW because if we’re going to keep just one financial, AFL has demonstrated better management and doesn’t face the displacement from passive investing that TROW does.

And there you have it, we’re left with our list of 10 aristocrats we’d retire with if we had to.

The list of 10 Dividend Aristocrats

These are sorted from low yield to high yield.

Top 10 Dividend Aristocrats (Dividend Freedom Tribe)

Let’s take a little look at the income profile of each.

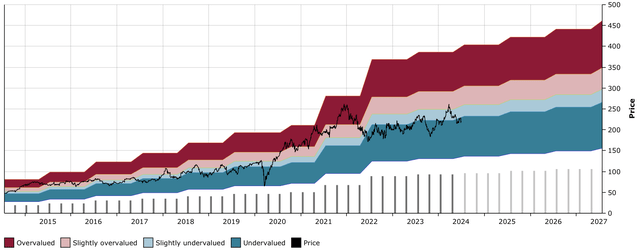

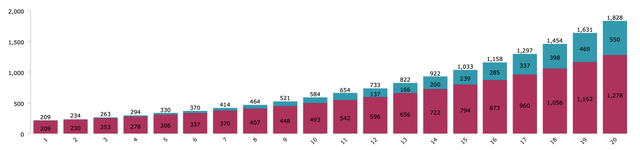

1. Lowes

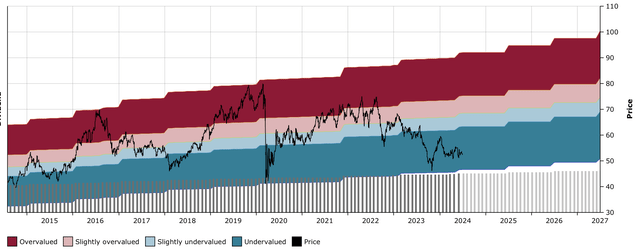

LOW currently trades at $220 and yields 2.09% which is above its 10-year median yield of 1.77%.

LOW DFT Chart (Dividend Freedom Tribe)

During the past 5 years, the dividend has a grown at a 16% CAGR and over the past 10 years, at a 17% CAGR.

I believe that LOW will grow the dividend at 10% going forward, which suggests that if we invest $10K today at the current yield and reinvest dividends, then in 10 years we could expect $584 in yearly income and in 20 years we could expect $1,828 in yearly income.

LOW 20 Year Dividend Snowball (Dividend Freedom Tribe)

While LOW is historically undervalued, these numbers suggest that to be truly happy investing in LOW, I’d need a higher dividend yield or higher dividend growth.

Unsurprisingly, LOW is currently on our watch/hold list.

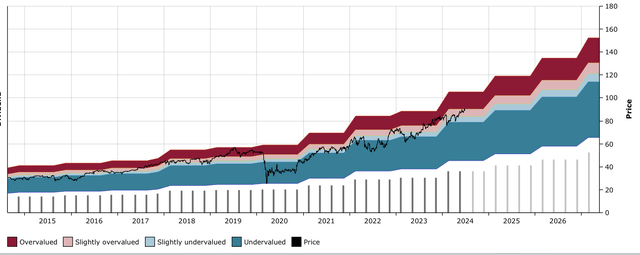

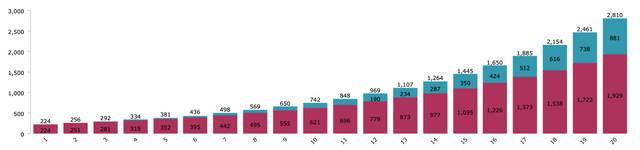

2. Aflac

AFL currently trades at $89 and yields 2.25%, which is below its 10-year median yield of 2.4%.

AFL DFT Chart (Dividend Freedom Tribe)

During the past 5 years, the dividend has a grown at a 13% CAGR and over the past 10 years, at a 10.5% CAGR.

This last year, they increased the dividend by an impressive 19%. I believe another big dividend increase is coming this year.

I believe that will grow at 12% going forward, which suggests that if we invest $10K today at the current yield and reinvest dividends, then in 10 years we could expect $742 in yearly income and in 20 years we could expect $2,810 in yearly income.

AFL 20 Year Dividend Snowball (Dividend Freedom Tribe)

My rule of thumb is $800 on $10K in 10 years. AFL is very close, and for investors with a longer time horizon, it makes a lot of sense at the current prices.

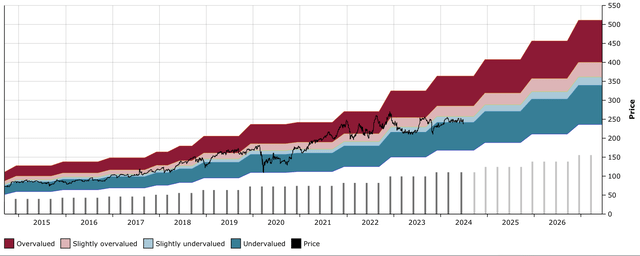

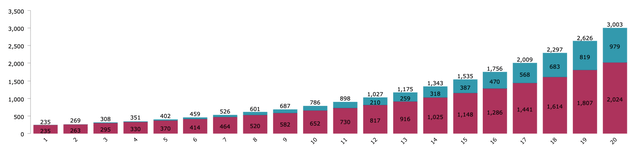

3. Automatic Data Processing

ADP currently trades at $238 and yields 2.35% which is just slightly above its 10-year median yield of 2.2%.

During the past 5 years, the dividend has a grown at a 12% CAGR and over the past 10 years, at a 12% CAGR. Last year, it also grew 12%. ADP has been particularly consistent in increasing its dividend over time.

ADP DFT Chart (Dividend Freedom Tribe)

I believe that will grow at 12% going forward as management has shown its commitment to that level, which suggests that if we invest $10K today at the current yield and reinvest dividends, then in 10 years we could expect $786 in yearly income and in 20 years we could expect $3,003 in yearly income.

AFL 20 Year Dividend Snowball (Dividend Freedom Tribe)

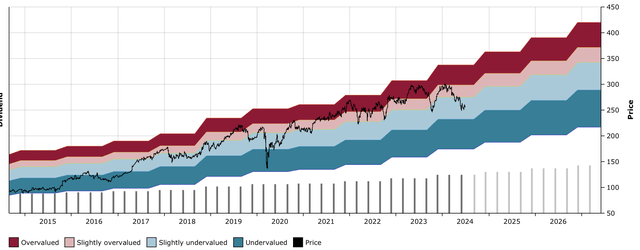

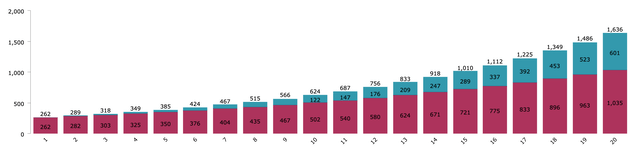

4. McDonald’s

MCD currently trades at $255 and yields 2.61% which is above its 10-year median yield of 2.4%.

MCD DFT Chart (Dividend Freedom Tribe)

During the past 5 years, the dividend has a grown at a 7.6% CAGR and over the past 10 years, at a 7.5% CAGR.

While it increased its dividend by 10% this past year, it is safer to continue forecasting 7.5% dividend growth going forward, which suggests that if we invest $10K today at the current yield and reinvest dividends, then in 10 years we could expect $624 in yearly income and in 20 years we could expect $1,636 in yearly income.

MCD 20 Year Dividend Snowball (Dividend Freedom Tribe)

The correct conclusion with MCD is that even though the price has come down, it hasn’t yet reached a level which I’d be content initiating a position in.

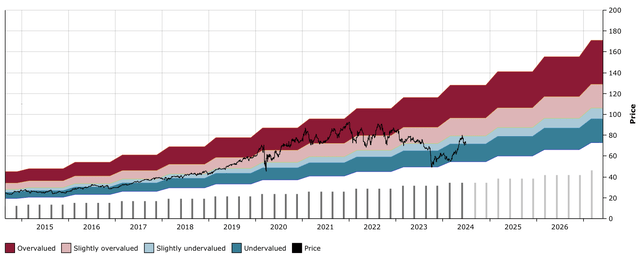

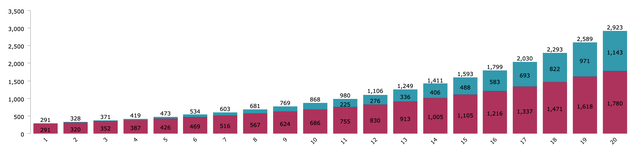

5. NextEra Energy

NEE currently trades at $71 and yields 2.9% which is above its 10-year median yield of 2.61%.

NEE DFT Chart (Dividend Freedom Tribe)

During the past 5 years, the dividend has a grown at a 10.5% CAGR and over the past 10 years, at an 11% CAGR. This year, a 10.2% growth rate.

This slight reduction in growth rates isn’t worrisome, given the opportunity set for NEE, I believe it should comfortably be able to deliver 10% growth going forward.

NEE 20 Year Dividend Snowball (Dividend Freedom Tribe)

This suggests that if we invest $10K today at the current yield and reinvest dividends, then in 10 years we could expect $868 in yearly income and in 20 years we could expect $2,923 in yearly income.

As you can imagine, and as I’ve already written about in past articles, I believe NEE is a buy.

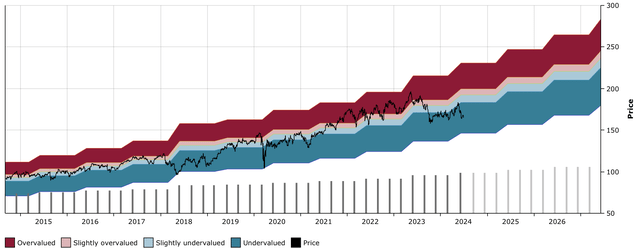

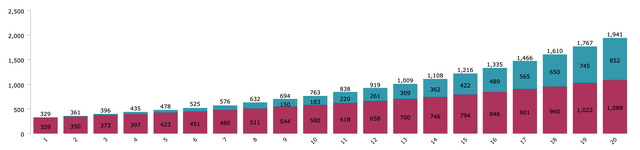

6. PepsiCo

PEP currently trades at $165 and yields 3.3% which is above its 10-year median yield of 2.8%.

PEP DFT Chart (Dividend Freedom Tribe)

During the past 5 years, the dividend has a grown at a 7.3% CAGR and over the past 10 years, at a 7.5% CAGR.

This year, it grew at a 7.1% CAGR. In the name of conservatism, let’s assume this continues to slow to a 6.5% CAGR going forward.

This would suggest that if we invest $10K today at the current yield and reinvest dividends, then in 10 years we could expect $761 in yearly income and in 20 years we could expect $1,941 in yearly income.

PEP 20 Year Dividend Snowball (Dividend Freedom Tribe)

Like AFL, the dividend would be just below our target of $800 in 10 years on $10K, but wouldn’t grow to nearly as much over 20 years. As such we’d refrain from buying PEP until it yields at least 3.5%, which for the record, has happened multiple times in the past. Given the high payout ratios, this seems to be the conservative and appropriate approach.

7. AbbVie

ABBV currently trades at $171 and yields 3.6% which is slightly below its 10-year median yield of 3.9%.

ABBV DFT Chart (Dividend Freedom Tribe)

During the past 5 years, the dividend has a grown at a 7.7% CAGR and over the past 10 years, at a 10% CAGR.

This past year, the dividend grew by 4.7%. ABBV’s dividend has been growing at a slower rate, and a look back at the chart will show that this has been a progressive phenomenon.

I believe that the dividend will grow at most at 4.5% going forward, which suggests that if we invest $10K today at the current yield and reinvest dividends, then in 10 years we could expect $718 in yearly income and in 20 years we could expect $1568 in yearly income.

ABBV 20 Year Dividend Simulation (Dividend Freedom Tribe)

This also suggests that the shares are trading at a higher level than those at which we would purchase. For us, ABBV is a hold/watch.

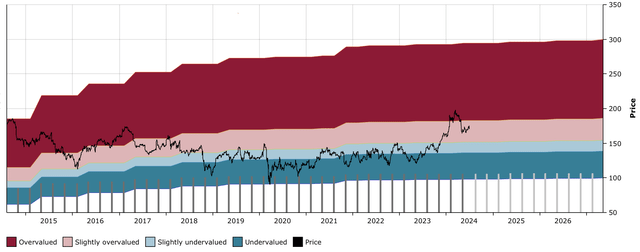

8. IBM

IBM currently trades at $173 and yields 3.86% which is below its 10-year median yield of 4.4%.

IBM DFT Chart (Dividend Freedom Tribe)

During the past 5 years, the dividend has a grown at a 1.6% CAGR and over the past 10 years, at a 4.7% CAGR.

This past year, the increase was just 0.6%.

This one is more difficult to assess future dividend growth. If the AI revenues and profits truly take off, then we could see growth in line with the past decade. But management hasn’t shown willingness to return to higher levels of dividend growth yet, with these small bumbling increases.

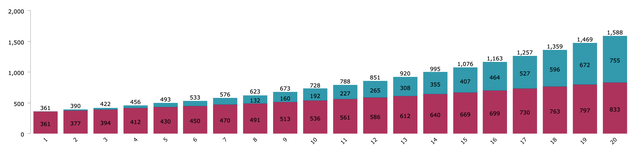

It’s safe to assume 2% growth going forward, and we’ll reassess when the time comes. This suggests that if we invest $10K today at the current yield and reinvest dividends, then in 10 years we could expect $644 in yearly income and in 20 years we could expect $1,139 in yearly income.

IBM 20 Year Dividend Snowball (Dividend Freedom Tribe)

This, of course, would be unsatisfactory, and therefore IBM is on our sell list. We’ve sold shares at $170 and more at $190, and hold on to the remaining position, which we’ll offload if the shares gain traction again this cycle.

9. Chevron

CVX currently trades at $156 and yields 4.18% which is slightly above its 10-year median yield of 4%.

CVX DFT Chart (Dividend Freedom Tribe)

During the past 5 years, the dividend has a grown at a 6.5% CAGR and over the past 10 years, at a 4.3% CAGR.

This year it was increased by 8%.

Given the trajectory, it is likely that CVX continues to grow at 5-8% in upcoming years. Let’s project using 6% growth.

This suggests that if we invest $10K today at the current yield and reinvest dividends, then in 10 years we could expect $998 in yearly income and in 20 years we could expect $2,627 in yearly income.

CVX 20 Year Dividend Snowball (Dividend Freedom Tribe)

This is of course attractive, and makes CVX a buy.

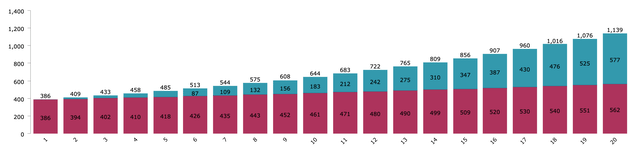

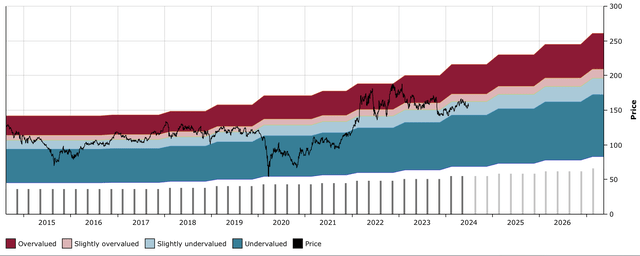

10. Realty Income

O currently trades at $53 and yields 5.98% which is above its 10-year median yield of 4.6%.

O DFT Chart (Dividend Freedom Tribe)

During the past 5 years, the dividend has a grown at a 3% CAGR and over the past 10 years, at a 3.7% CAGR.

This last year it increased by 2.9%, and I believe this is a fair amount to project going forward. O’s size challenges future growth, but the international opportunity enables this modest level of dividend growth.

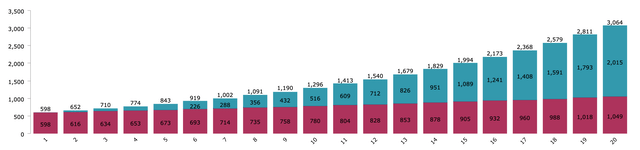

If we invest $10K today at the current yield and reinvest dividends, then in 10 years we could expect $1,296 in yearly income and in 20 years we could expect $3,064 in yearly income.

O 20 year Dividend Snowball (Dividend Freedom Tribe)

It won’t come as a surprise to learn that O is still on our Buy list at these prices.

Conclusion

I wouldn’t want to own just 10 stocks to retire, and particularly, I wouldn’t want to own just Dividend Aristocrats, and even of these 10 I’d be happy to own, it would only make sense at certain prices.

Author’s art

Only a subset of all Dividend Aristocrats make sense for most portfolios, and for investors who are looking for more yield because of a lower time horizon, very few fit the bill.

If you take away anything from this article, I’d like it to be:

- The best combination of dividend yield and growth depends on your time horizon.

- Even the best companies are only buys at the right prices.

I’d like to close this article with a great Warren Buffett quote:

Whether it’s stocks or socks, I like to buy good quality merchandise at a discount.

Read the full article here