Introduction & investment thesis

Chewy, Inc. (NYSE:CHWY) is a pet-ecommerce business that has recently seen tremendous volatility in its stock price after Roaring Kitty posted a picture of a dog on social media site X. I had last written about Chewy on April 26, where I had rated the stock a “hold.” My thesis was predicated on my belief that the stock did not have sufficient upside as the management had warned that the company was going to see a slowdown in its revenue growth in FY24, driven by macroeconomic and pricing pressures. Since then, the stock has climbed 72% outperforming the index, though most of it is driven by meme trade sentiment rather than fundamental factors.

The company reported its Q1 FY24 earnings on May 29, where its revenue and earnings grew 3% and 46.8% YoY, respectively. During the quarter, the company saw its Net Sales per Active Customer (“NSPAC”) grow 9.5% YoY as it was able to acquire net new customers and reactivate old ones, while deepening adoption among its existing customer base with its Autoship subscription program as well as in new categories with Chewy Health. Simultaneously, the company is also expanding on its strategic initiatives, which include testing its Chewy Plus paid membership program in beta, launching new Chewy Vet Care Clinics, and gaining market share in Canada. While the management is optimistic on some of the emerging customer trends, they did not raise their revenue guidance for FY24.

However, given the latest volatility spikes in the stock price from meme trade, there have been growing downside risks with short traders having a 14.8% position in Chewy. Plus, I believe that its valuation is unsupportable. As a result, I will be cautious with the stock at its current levels and wait for the volatility to subside before initiating a position. Meanwhile, I will rate the stock a “sell.”

The good: customers increase wallet share on Autoship & Chewy Health, optimism in Chewy Vet Care clinics, expanding profitability

Chewy reported Q1 FY24 earnings where net sales grew 3% YoY to $2.88B exceeding estimates as demand for consumables and health remained strong, accounting for 85% of total sales, while Autoship customer sales grew 6.4% YoY, representing 77.6% of total sales.

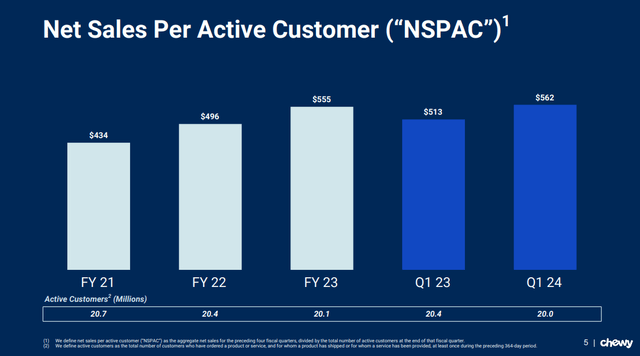

During the quarter, NSPAC grew 9.5% to $562 as the company started to see some encouraging customer trends through their pet type personalization efforts, resulting in acquiring net new customers as well as reactivating existing customers, highlighting their strong value proposition, while existing customers deepened their engagement with Autoship as well as new categories with Chewy Health.

Q1 FY24 Earnings Slides: Growing wallet share among customers

Plus, Chewy has also launched a paid membership program called Chewy Plus, which is still in beta state and will offer its customers a range of benefits such as free shipping, cash rewards, and others. This can play an important role in helping the company expand its NSPAC as it rolls the program out in the coming quarters, along with driving more in-depth customer engagement and unlocking operating leverage.

Simultaneously, the company also launched its first Chewy Vet Care clinic in Florida, along with three additional clinics in Atlanta and Denver, as part of its strategic initiative to expand their total addressable market (“TAM”) by $25B, while simultaneously growing wallet share among customers. During the earnings call, the management outlined that they are optimistic with the initial demand generation as net new customers and appointment utilization are trending higher than internal expectations, and as a result, they are confident that they will be able to reach the high end of their stated range of opening four to eight clinics in 2024.

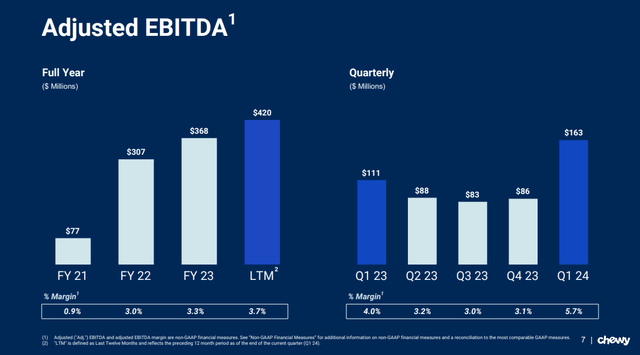

Shifting gears to profitability, the company generated $163M in Adjusted EBITDA, which grew 46.8% YoY, with a margin of 5.7%, an improvement of 170 basis points from the previous year. While the expansion of NSPAC helped Chewy unlock operating leverage, sponsored ads also played an important role in improving margins, along with lower than expected promotions and increased sales penetration into Chewy Health and premium consumables. At the same time, the management also kept their operating expenses relative to net sales anchored at approximately 27.5% on a GAAP basis, as teams executed methodically on the controllable elements of the business in a disciplined manner. This has enabled the company to generate $52.6M in free cash flow in Q1, which consists of $81.9M in operating cash flow and $29.3B in capital expenditures. This is encouraging, especially as the company embarks upon expanding on its strategic priorities in Health and international expansion to fuel the next phase of its growth trajectory, while remaining debt-free at the same time. As part of its growing operating leverage and strong balance sheet, Chewy has authorized the first-ever share repurchase program of $500M to enhance its shareholder returns, while mitigating the diluting impact of share-based compensation.

Q1 FY24 Earnings Slides: Expanding Profitability as the company unlocks operating leverage

The bad: increased volatility from meme trade, no upward revision to revenue guidance despite a strong start to FY24

Recently, Chewy and its competitor Petco (NYSE:WOOF) have been under tremendous volatility after Keith Gill, also known as “Roaring Kitty,” posted an image of a dog on X without any accompanying text, with short traders having a 14.8% position in Chewy and 22.4% in Petco. Keith Gill is largely credited for playing a leading role in the GameStop meme frenzy in 2020 through his popular YouTube account and Reddit persona. Since the spike on Thursday to over $39, the stock has declined 30% in a day to its current price of $27.24. However, given the recent volatility associated with the meme trades, investors should be cautious about trading the stock in this environment, and investment decisions should be made based on its fundamentals.

Speaking of fundamentals, the management maintained its previous revenue guidance of $11.6-$11.8B for FY24, which represents 4-6% growth, while raising its expectations for Adjusted EBITDA margin from 3.8% to 4.2%. Given the fact that it had a stronger than expected start to the year, as it was able to acquire new customers and reactivate old ones faster than expected, while simultaneously expanding NSPAC among its customer base from Autoship and Chewy Health, it would have been more encouraging for investors had the management raised the revenue guidance. However, the management reiterated that it would be “premature” to revise their view on the pet industry’s overall outlook for the remainder of the year as it tries to manage analyst expectations relative to its chances of outperforming its guidance for FY24.

Revisiting my valuation: recent volatility spikes have caused the stock’s valuation to become unsupportable

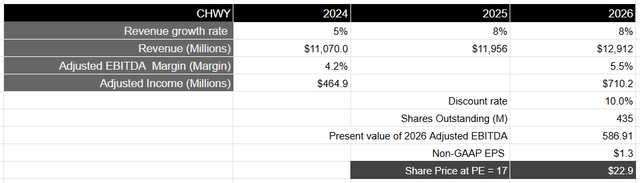

Looking forward, I believe that Chewy should be able to reach its FY24 revenue expectations, especially as it sees success in acquiring new customers and reactivating old ones in its Autoship program, while simultaneously expanding its strategic initiatives to roll out its paid membership program of Chewy Plus throughout the year, ramping up its sponsored ads, launching new Chewy Vet Care clinics, and gaining market share in Canada. Assuming that it can return to growing its revenue in the high single digits, especially as macroeconomic conditions ease along with greater pet household formations in the coming years, it should generate close to $12.9B in FY26.

From a profitability standpoint, I believe that it should be able to unlock operating leverage over the coming years from a projected 4.2% in Adjusted EBITDA margin to at least 5.5% by FY26, as it sees NSPAC expand from growing wallet share among customers along with sponsored ads from its partners. This will enable it to streamline its operating expenses further and drive margin expansion, thus generating Adjusted EBITDA of approximately $710M by FY26, which is equivalent to a present value of $586M when discounted at 10%.

Taking the S&P 500 as a proxy, where its companies grow their earnings on average by 8% over a 10-year period with a price-to-earnings ratio of 15-18, I believe that it should trade at par with the S&P 500 given the growth of its earnings during this period of time. This will translate to a price target of approximately $20-$23, which represents a downside of approximately 20% from its current levels.

Author’s Valuation Model

My final verdict and conclusion

While I am encouraged by the fact that Chewy is growing its NSPAC among its customer base as it deepens its adoption of Autoship while innovating on Chewy Health with its strategic expansion into Chewy Vet Care clinics, I am also concerned about the state of volatility that has been induced by the meme trade.

Although I believe that Chewy should be able to grow in the high single digits over the coming years with expanding profitability, I believe that its current share price has fully priced in the future growth prospects, and its latest stock price spikes are unsupported by fundamentals. As a result, I would be cautious at present levels and wait for the volatility to subside before initiating a long-term position in Chewy, Inc., rating the stock a “sell” at its current levels.

Read the full article here