High Yields, High Premiums, Bargain Prices (For Some)

I’ve struggled for years trying to understand the two Cornerstone funds, Cornerstone Total Return (NYSE:CRF) and Cornerstone Strategic Value (NYSE:CLM). The funds are unusual in that they seem to deliberately pay out much higher distributions than they actually earn, which has resulted in their Net Asset Values depreciating regularly over their long lives, since being founded 37 years ago (CLM in 1987) and 51 years ago (CRF in 1973).

Since then, CRF has seen its NAV drop about 95%, from $140 to about $7, while CLM’s NAV has dropped about 97%, from $200 to $7. Despite this, CLM reports a lifetime average total return on NAV of 8.6% per annum since 1987, while CRF’s lifetime total return on NAV since 1973 is a somewhat more modest 6% per annum. For the past 10 years, both funds have done much better, with average annual total returns on NAV for each of them of 11% or more.

On the one hand, the Cornerstone funds’ experience would tend to confirm the idea that “total return” is indeed the sum of BOTH cash distributions as well as capital gains or losses in the price or NAV of the investment. In other words, it appears that CLM and CRF’s ultra-high distributions have indeed offset the steady depreciation in the funds’ NAVs, resulting in what has been, so far, a satisfactory total return (especially in the past 10 years).

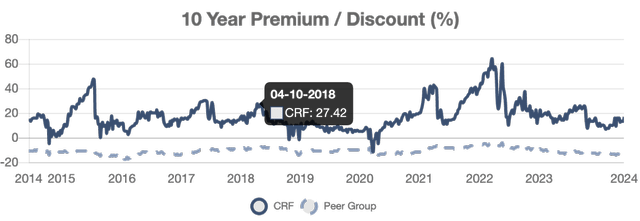

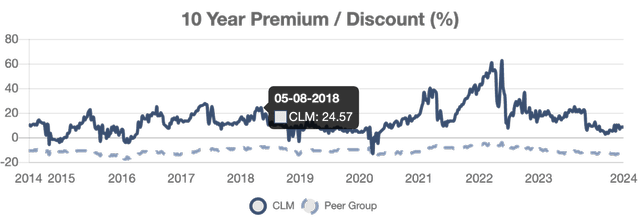

Another unusual feature of both funds is that they’ve both sold at high, even nosebleed level, premiums over the past 10 years – often 20% and as high as 40% and 60% at various times. The premiums have receded recently, and are currently 8.3% for CLM and 15.6% for CRF.

I assume the historically high premiums may have been a result of the funds’ high distribution yields (currently CRF’s 15.8% and CLM’s 16.9%), since we all know high distributions can often induce some investors to ignore basic analytics and just pursue the high cash yields.

Another interesting feature of both funds is that they offer a dividend-reinvestment plan that allows shareholders who “DRIP” their distributions the ability to reinvest those distributions at the net asset value (“NAV”) of the particular fund (i.e. CRF or CLM, as the case may be).

DRIP funds that allow DRIPPERS to reinvest at discounted prices are not unusual among closed-end funds. But what seemed unique about CLM and CRF, and made them attractive to shareholders savvy enough to appreciate the opportunity it presented, was the combination of (1) the ultra-high distribution yields, (2) the ultra-high premium prices, and (3) the discounted DRIP reinvestment policy. This resulted in huge purchase discounts for shareholders who took advantage of the discounted DRIP policy at times in the past when the premiums were at such nosebleed levels.

This benefit has accrued to those fund shareholders who have been savvy and motivated enough to (1) read the fine print of their shareholder materials and learn about the price advantage given to DRIPPERS, and (2) take the steps (which can sometimes be complicated depending on your broker) to organize the DRIP feature on their CLM and/or CRF share holdings.

“Discount DRIPs,” where shareholders get to buy new shares at bargain prices if they automatically reinvest their distributions, are not that unusual in the closed-end fund world. They represent an advantage to the participating DRIP shareholders, who get bargain-priced new shares that they can either (1) keep and enjoy all the benefits of ownership, going forward, knowing they got it at a discounted price, or (2) sell the shares immediately for more than they paid for them, essentially collecting a higher cash dividend than they would have received had they taken cash to begin with and not participated in the bargain DRIP. Other popular closed-end funds offering discounted DRIPs include some we own in our investing group service like Eagle Point Credit (ECC), Oxford Lane Capital (OXLC), Carlyle Credit Income (CCIF), Eagle Point Income (EIC), OFS Credit (OCCI), and XAI Octagon Alternative Income (XFLT).

The cost of the “non-accretive” share issuance to DRIPPERS is borne by the fund as a whole, so the real “net” cost falls on the shareholders who do not participate in the DRIP and therefore fail to get the off-setting benefit of the cheaper, below-market shares. The issuance is “non-accretive” since it is the opposite of when a fund issues new shares at MORE than their current market price, where the additional “profit” on the sale of new shares “accretes” to the benefit of ALL the fund’s shareholders.

Who Benefits, and When?

Once we think about it, it becomes pretty clear that if a small minority of a fund’s shareholders are consistently allowed to buy shares of the fund at a discount, over time they will accumulate more shares and will have bought them at consistently cheaper prices than other shareholders who don’t participate in the bargain program (i.e. who don’t DRIP).

Several aspects of this may not be obvious, so let’s point them out:

- The bigger the share price premium, the bigger the discount that any DRIPPER gets who participates. For example, if the premium were 63%, as it was on CRF shares two years ago, a DRIPPER was paying 100% of NAV for shares that were selling at 163% of NAV. That’s a savings (i.e. discount) of 63/163 = 38.6%.

- As premiums have shrunk recently, the discount on the new shares being DRIPPED becomes less, as we have seen. Currently, CRF’s premium is 15.6%, which means if the distribution reinvestment date were today, investors would be paying 100% of NAV for shares whose market price was 115.6% of NAV, so their savings (discount) would be 15.6% divided by 115.6%, or 13%. That’s still a good deal for those shareholders, but a far cry from the 38.6% savings of two years ago.

- The DRIP discount on CLM’s shares has come down even further. CLM’s premium is currently 8.3%, having peaked at 61% two years ago. At that time, shareholders who DRIPPED as part of the program received savings on their newly issued shares of 61% divided by 161%, or 37.8%. At today’s premium of 8.3%, the savings (i.e. discount) would be 8.3% divided by 108.3%, or only 7.6%. Again, a good deal for shareholders, but nowhere near the bargain it was two years ago, or even just last August when CLM’s premium was still over 25%; which would have given DRIPPERS a discounted price that was 25%/125%, or 20% lower than CLM’s market price back then.

- The exact prices and percentage savings for DRIPPERS may vary slightly from brokerage firm to brokerage firm, depending on their internal administrative procedures. Some firms, like Fidelity in my experience, give the advantages of various closed-end fund discount-DRIP programs to their clients automatically, as long as the client chooses the standard DRIP link on their account. Some other firms, from what I hear from members and readers, may make you jump through additional hoops (calling the firm, providing additional instructions, etc.) to participate in the discounted DRIP programs; while some others may not even let clients participate at all.

Implications for Shareholders

- It should be pretty obvious that the lower the percentage premium the market price of fund shares is to the Net Asset Value (NAV) of those shares, the less value there is to participating in the CLM or CRF DRIP programs.

- Likewise, the higher percentage of CLM and CRF shareholders who get wise to the program, and begin to DRIP at the discounted price (i.e. NAV), the less advantage they receive. That’s because, while they get the advantage of bargain-priced new shares, the more shareholders take advantage of the program, the greater the cost to the fund as a whole and the greater the financial hit (1) to the shares held by the Non-DRIPPING shareholders, and (2) to the other shares the DRIPPING shareholders already own.

- If the last point doesn’t seem immediately obvious, think of it this way. When a fund issues new shares and the purchasers of the new shares pay the fund MORE than the current market price of existing shares, that is said to be “accretive” to the existing shareholders. The “accretion” (i.e. the “profit” to the fund of selling new shares at a higher price than those shares are currently “worth” on the market) is shared proportionally by all the existing shareholders of the fund.

- If a fund does the opposite of that, and issues new shares for less than the same shares would sell on the open market (which is what a fund like CLM or CRF does when it issues new shares to DRIPPERS for less than the shares’ market value) the effect is “negative accretion” in that every existing share of that fund is worth a tiny bit less (or literally, represents a tiny bit smaller proportion of the fund than it did previously, before the new shares were issued at the discounted price).

- To illustrate this, suppose every shareholder – 100% of them – took advantage of CLM and CRF’s subsidized, bargain-priced DRIP programs.

- That means the advantage the DRIPPERS received (i.e. the cost of the “non-accretive” issuance of new shares) would now be evenly spread among all the shareholders, since every shareholder would be a DRIPPER.

- So there would be NO NET ADVANTAGE to one shareholder group over another. No “robbing Peter to pay Paul” since every Peter would also be Paul. The “bargain price” of each new DRIPPED share would come out of the pocket of the other shares each shareholder already owned.

- In other words, discounted DRIPPING policies, of which CLM and CRF had long been a somewhat extreme example (until their premiums dropped over the past year), are a zero sum game in that the profits/discounts given to the participating DRIPPERS come at the expense of the shareholders at large.

I think the more investors realize this, the more the air may continue to go out of this particular balloon. Now that CRF and CLM’s premiums have come down from the stratosphere to about 15% and 8%, respectively, the potential DRIP discount is considerably reduced, although probably still worth our participation).

The other trend worth noting is the percentage participation. The Cornerstone website only has financial information going back a few years. But even so, we can see that participation rates in the DRIP program have increased considerably just recently.

CRF had 17.5% of its distribution in 2021 DRIPPED back into fund shares. By 2023 that had almost doubled, to 32%. That means the “non-accretion” hit to fund shares overall increased; so the net advantage to a DRIPPER is reduced, as their existing (“pre-DRIP”) shares incur a bigger loss the more other shareholders participate and the more non-accretive DRIP shares are created.

Similarly, CLM had only 15.6% participation in its DRIP program back in 2020. That participation rate more than doubled to 35% in 2023. Again, the hit to existing shares would have increased considerably, as the percentage of participating DRIP shares increased.

Bottom line: This means the advantage for being “smarter” than other shareholders, and knowing what a great deal the DRIP program is (or was) surely declines as more investors figure it out and decide to get on board.

If the percentage participation in Cornerstone’s DRIP program continues to climb higher as more shareholders come to understand the program, the advantage of participating will become less and less. If participation reaches 100%, then there would be no advantage at all, since the bargain achieved on the new shares would be exactly canceled out across the board as the non-accretion cost were spread out proportionately.

Conclusion

It is hard not to imagine that these funds may have operated for a long time, with the “smart money” knowing how the game was played and having little incentive to share the secret with the broader ownership. We all know that most investors don’t read the “fine print” in annual reports and fund websites.

So it’s quite possible that many Cornerstone shareholders probably had (and maybe still have) little idea they are subsidizing the rest of us who have figured out that a lot of the value in owning these funds has come from participating in the DRIP. This is similar to “tender offers” (Link here) where the smart money hopes most investors will ignore them, leaving more money on the table for the more “active” and/or knowledgeable investors.

Now that we know, we need to keep an eye on the premium price levels. For example, at a 15% premium, CRF may be a better bargain than CLM at an 8% premium, even though that at first appears counter-intuitive. That’s because, as a DRIPPER, you get a much bigger discount with CRF than when you DRIP CLM with its smaller premium. As the premiums on CLM and CRF have been coming down, investors have to ask ourselves why we are holding these funds. If their performance is such that we’d want to hold them regardless of the discounted DRIP program, and that we regard that as essentially “icing on the cake,” then so be it. All the other funds I own and DRIP that are mentioned above (ECC, OXLC, CCIF, OCCI, EIC, XFLT), are funds I would choose to own even without the additional benefit of their DRIP programs. But I honestly have not yet decided if I want to own CLM and CRF without the inducement of what was, until relatively recently, a much larger-than-normal DRIP discount. That’s a topic for further analysis, and I hope other Seeking Alpha writers will join the discussion.

Besides the premium trend, we also need to monitor the percentage shareholder participation in the DRIP programs of both funds, since the higher it goes, the less advantage the DRIP program’s unique pricing feature provides to individual shareholders.

In general, I like funds that are managed for the benefit of all shareholders, and don’t appear to offer one set of shareholders benefits so obviously at the expense of other shareholders. Having said that, I’m not averse to making some money in the short term, while the rest of the shareholders are figuring things out, as I believe they eventually will.

As always, I appreciate your comments and questions. On this topic in particular (i.e. CLM, CRF and their unusual dividend policies), I may have missed something and look forward to your thoughts and reactions.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here