Introduction

Everyone knows Ferrari (NYSE:RACE) either as a company that makes ultra-luxury cars or as the best team in the history of F1. However, what would you think if I told you that one aspect feeds the other, and vice versa, resulting in one of the best companies in the world?

Since its IPO, Ferrari has delivered a spectacular 31% annual compounded return. Such a performance over so many years cannot be attributed to mere chance. In this article, we will uncover the secrets that make Ferrari an extraordinary company, despite operating in an industry as challenging as the automotive sector when it comes to generating shareholder value.

We will delve deeper into this throughout the article, but the summary of this investment thesis is that, by investing in Ferrari, we are not really investing in automobiles but in luxury. This detail may seem trivial, but from my point of view, it completely changes the approach we should take as investors when considering this company.

The History of Ferrari

I don’t usually spend much time researching the distant past of the companies I analyze, but in this case, I believe it is crucial. So, let’s take a brief look at the history of the ‘prancing horse’.

The history of Ferrari begins with Enzo Ferrari, born in 1898 in Modena, Italy. From a young age, he showed a great interest in motorsports, influenced by his father and older brother, who also shared this passion. In the 1920s, Enzo began his career as a race car driver, competing for the Alfa Romeo team. His passion for racing led him to found Scuderia Ferrari in 1929, initially as a racing team for Alfa Romeo. For more than a decade, Scuderia Ferrari was responsible for managing and preparing race cars for Alfa Romeo. However, Enzo had a more ambitious dream: to build his own cars.

Enzo Ferrari (Ferrari Investor Relations)

In 1939, Enzo Ferrari left Alfa Romeo to establish Auto Avio Costruzioni. Due to a clause in his contract, he could not use the Ferrari name on his cars for the first few years. During World War II, the company focused on producing tools and mechanical equipment. After the war, in 1947, Enzo was finally able to realize his dream and introduced the first car under the Ferrari brand, the 125 S.

The following years witnessed the consolidation of Ferrari in the world of racing and luxury car production. However, it was in Formula 1 where Ferrari would achieve unprecedented success. In 1950, Scuderia Ferrari made its debut in the Formula 1 World Championship, and in 1952, Alberto Ascari won the first drivers’ championship for Ferrari. The 1960s and 1970s brought more championships and glory. Legendary drivers like Juan Manuel Fangio and Niki Lauda contributed to the team’s rich history. In the following years, Ferrari cemented its name as the greatest racing team in history, with drivers like Michael Schumacher, Fernando Alonso, and Sebastian Vettel behind the wheel.

In 1969, facing financial challenges, Enzo Ferrari decided to sell a majority stake in his company to Fiat S.p.A., thus ensuring the stability and future of Ferrari. This alliance allowed Ferrari to benefit from Fiat’s resources and infrastructure while continuing its dominance on the racetracks and its production of luxury cars. However, in 2015, Fiat decided to spin off Ferrari, and it went public as an independent entity.

Today, Ferrari has millions of fans around the world, thanks to its numerous successes in racing. These triumphs in competitions have allowed the brand to launch high-end car models for the general public, becoming the company’s main business.

The relationship between racing and road cars has been crucial for Ferrari, not only for technology and innovation but also because the prestige and mystique of the brand are nourished by its legacy on the tracks. Each victory and championship won reinforces Ferrari’s image as a symbol of luxury, performance, and exclusivity. This combination of racing heritage and engineering excellence has positioned Ferrari as one of the most exclusive and desired car manufacturers in the world. Each model not only represents luxury and prestige, but also the passion and competitive spirit that have characterized the brand since its inception.

Business Model

Luxury cars

The main part of Ferrari’s business and the focus of this analysis is the sale of luxury vehicles, as it constitutes more than 80% of Ferrari’s business. This is where the story we just told about Ferrari comes into play, as the brand has an aura that is practically irreplicable by other luxury car manufacturers, thanks to its history of success in motorsport. There may be other brands that produce exclusive luxury cars that match Ferrari’s performance, but none will be able to replicate the brand’s aura. This is what makes Ferrari truly irreplicable.

In addition to this, the company skillfully plays with the exclusivity of its vehicles to generate scarcity, thereby increasing the desire for the brand. In fact, when the company was once asked how many vehicles it would manufacture, the response was brilliant: “We will always manufacture at least one car fewer than the market demands.”

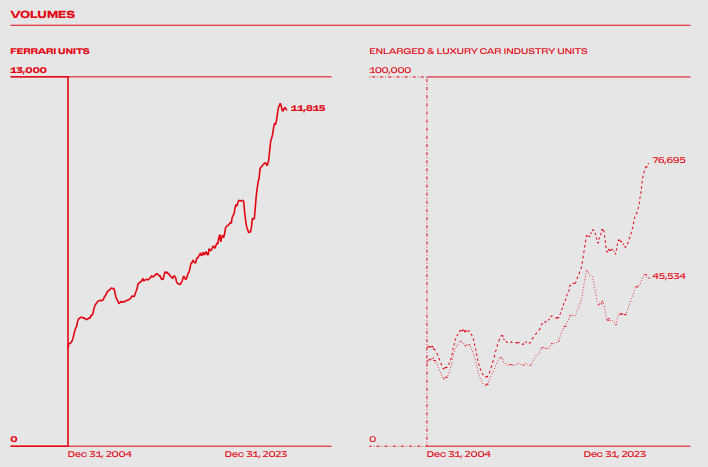

While premium vehicle companies such as BMW or Mercedes-Benz sell more than 2 million cars a year, and even more premium brands sometimes considered luxury like Porsche sell over 300,000 vehicles a year, Ferrari in 2023 sold around 13,000 units. While these three German brands and many others considered premium, sell as many units as they can at the highest price they can, Ferrari sells the number of cars it wants, artificially limiting the supply.

Ferrari 2023 10K

Some might think that it makes no sense for Ferrari to limit the supply when it could sell more cars, as this means the results are not as high as they could be, and you would be absolutely right. However, this strategy significantly increases the terminal value of the company and extends its growth as much as possible over time. Consider that the demand for Ferrari is much higher than its limited supply, making it very easy for them to grow the number of vehicles sold each year or systematically increase prices, which users will accept. As investors, this is fantastic because we have very high visibility of the cash flows the company will generate in the long term and very little uncertainty.

Besides the aura that the Ferrari brand has due to its racing history, the company uses a series of mechanisms to further increase the desire and exclusivity of the brand. For example, they will never sell you a car if you go directly to the Ferrari dealership to buy it; they intentionally make you wait on a waiting list so that you value the product more. Additionally, the brand does not allow modifications to their cars that are not certified by them. If you do so, they remove you from their client list, and you will never be able to buy another car from the brand again. This news about Justin Bieber is a good example of this policy.

They also play a very interesting strategy to keep customers loyal to the brand. When you buy a Ferrari for the first time, they let you access their standard models. However, if you want to access one of the limited editions that they release from time to time, you must have bought a vehicle from the brand before; otherwise, you will not be able to access it. Considering that their target market is multimillionaires with a lot of money, securing them as recurring customers is very valuable for the company in the long run.

Engines

On the other hand, Ferrari sells some of the engines it designs to other manufacturers for both street cars and competition vehicles. For example, Ferrari supplies the engines for the Haas and Alfa Romeo Formula 1 teams and sells street car engines to Maserati and Alfa Romeo, among others. This part represents a very small percentage of their revenue, but I believe it is a good way to leverage the work and resources put into engine manufacturing, generating extra sales.

Sponsors, merchandising and others

Lastly, Ferrari also generates revenue from the sale of merchandise such as caps, sunglasses, and clothing related to F1. They also operate theme parks and engage in other minor activities. Additionally, their strong racing image attracts many advertisers who want to place their logos on Ferrari cars. For instance, Celsius has signed an agreement with them, and HP is set to pay over $70 million annually to be the team’s official sponsor.

Financials

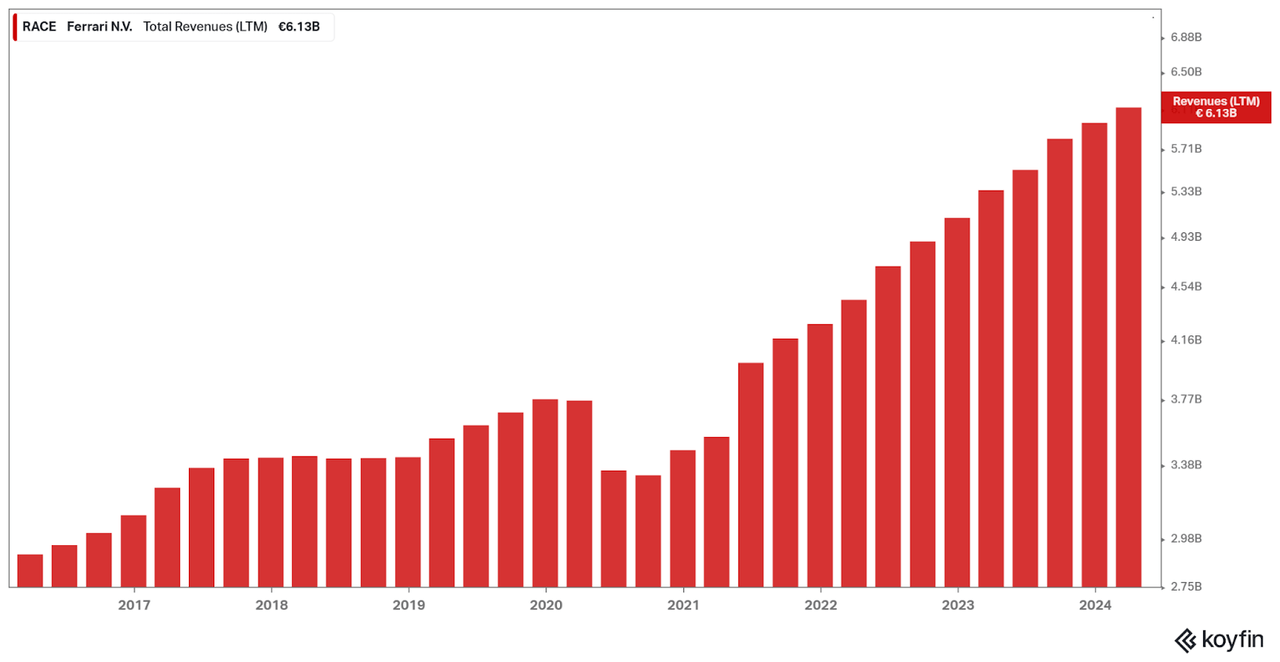

All these fundamentals have translated into extraordinary numbers. Since its IPO in 2016, Ferrari has grown its sales by 11%, with a dip in 2020 for obvious reasons, but with an extraordinary recovery in the following years. This increase, as you can see, has been quite linear, which is remarkably noteworthy in a cyclical market like the automotive industry. This is precisely the investment thesis in Ferrari: they are not a traditional car company; they are a company that sells luxury in the form of cars and is completely unaffected by the typical cycles that impact the industry.

Koyfin

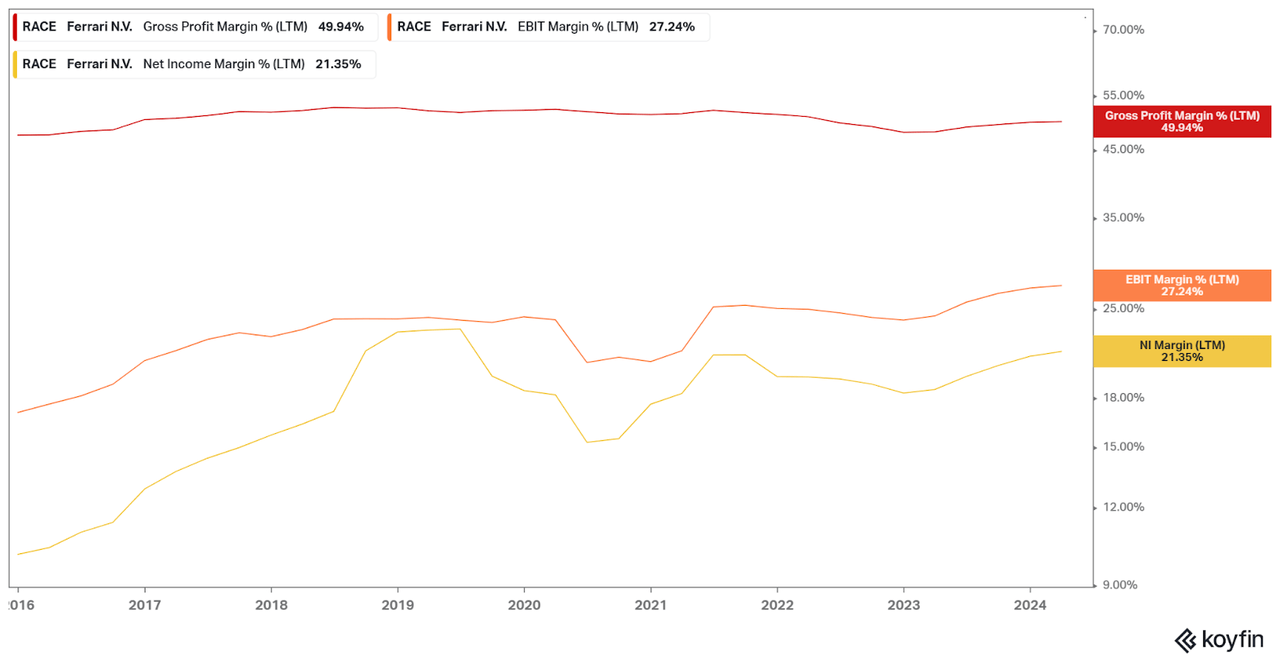

This growth has also translated into spectacular growth in the bottom line. Both the Free Cash Flow (FCF) and net earnings per share have compounded at over 20% annually. This has obviously been due to a significant margin expansion driven by the pricing power we have been discussing and thanks to their vertical integration, which gives them great control over the supply chain. The operational leverage has been more than evident, and although from my point of view, I highly doubt that margins can continue to grow at this pace, I do believe they can keep expanding until they achieve at least a 30% operating margin and a 25% net margin.

Koyfin

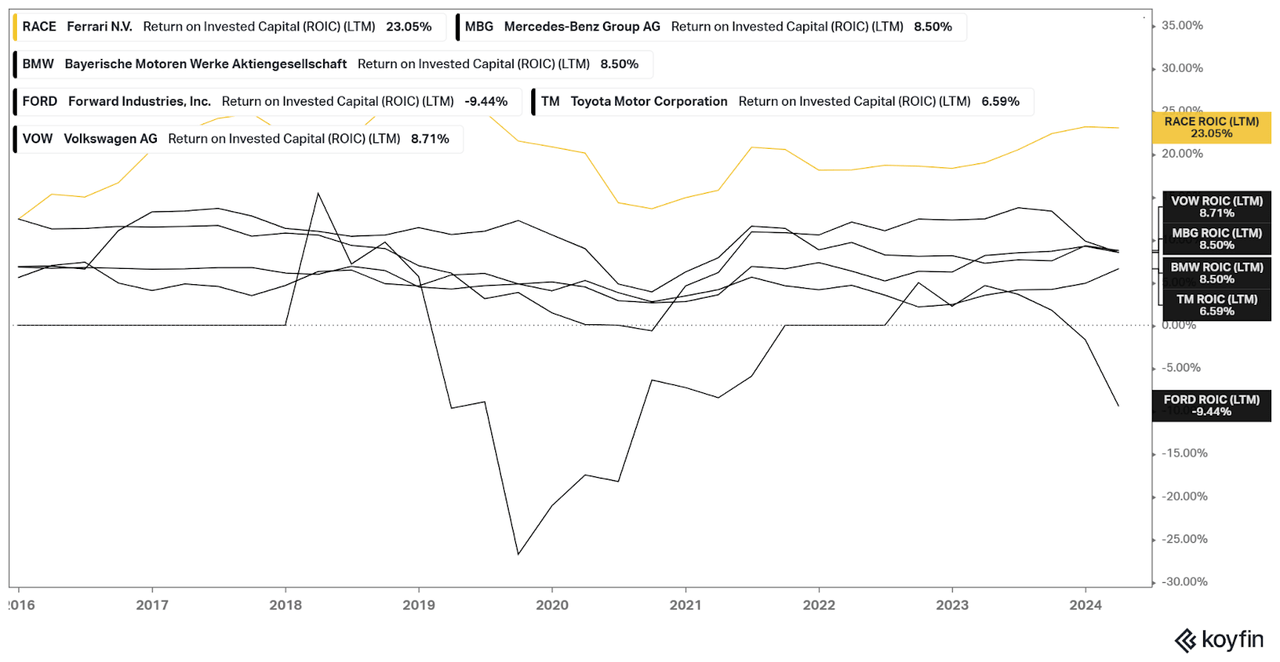

I believe the graph that best represents everything we’ve been discussing is the following. Here we can see the returns on invested capital for different companies in the automotive sector. We see how traditional car companies rarely exceed 10%, while Ferrari comfortably surpasses 20%. Again, this is because Ferrari is more of a luxury company than a car company, with total control over supply, allowing them to generate much more value for their shareholders than the rest of the companies in the automotive sector.

Koyfin

Risks

In my long-term thesis, I see only two real risks that could affect Ferrari’s performance: one internal and the other external.

-

Execution Risk: As I have tried to convey throughout this article, the most important aspect of Ferrari is its brand image. If its image were to deteriorate and Ferrari were no longer considered a luxury company but just another premium car manufacturer, the terminal value would obviously decrease, and the valuation multiples would contract significantly. For example, a very large increase in the number of vehicles sold per year could dilute the brand’s exclusivity. If you see a couple of Ferraris every day on the street, you would obviously lose that sense of exclusivity with the brand. I don’t think this is very likely to happen since the management itself is aware of this and always focuses on preserving the brand’s value, but it is something we, as shareholders, must monitor.

-

Regulatory Risk: On the other hand, regulatory risk could pose a clear threat to Ferrari, especially with electric vehicles. Some governments, such as those in Europe or California, are considering regulations to ban internal combustion vehicles by 2035 or similar dates. Ferrari would have to transition to electric vehicles, which I find challenging because the gasoline engine with its characteristic noise is something that greatly attracts people to the brand, and without it, they might lose the interest of some buyers. While there are reports of possible laws allowing supercars to continue running on gasoline, this is an issue that could affect Ferrari and is currently surrounded by considerable uncertainty for the coming years.

Valuation and conclusions

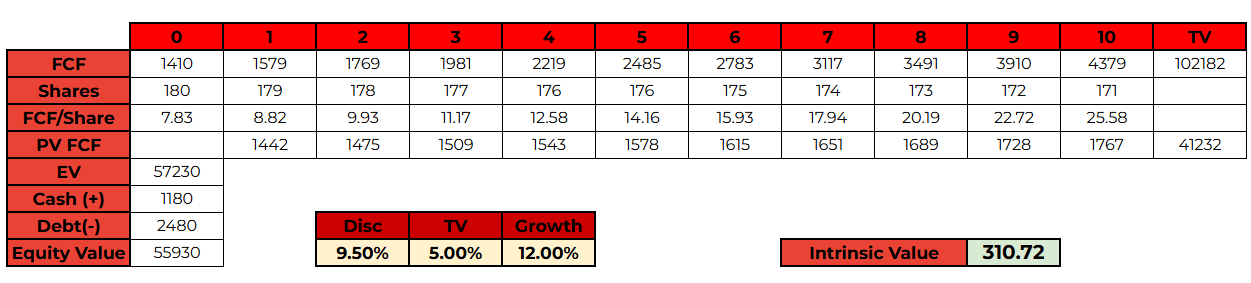

If we want to reach a realistic target value for Ferrari, I think we need to consider its extremely high terminal value, as we have discussed. From my point of view, it wouldn’t make sense to apply a terminal value of 2% in its valuation, given their control over supply and the fact that the demand for their vehicles far exceeds this. Ferrari will be able to continue growing its sales above 5% after year 10 with almost total certainty, so it is very important to reflect this in its valuation.

Even so, being quite optimistic and estimating a 12% growth in FCF until year 10, applying a perpetual growth of 5% and a WACC of 9.5%, the current valuation of €370 does not seem very attractive to me for buying Ferrari. A price around €300 per share would seem like a much better entry if we want to add Ferrari to the portfolio.

Author’s calculations

Anyway, as I often repeat in many of my analyses, I don’t think it’s a good decision to sell this type of high-quality company just because we might be in a temporary overvaluation. These companies have shown that they always tend to beat estimates and grow beyond expectations, so I am going to assign a ‘Hold’ rating to Ferrari shares.

In summary, I believe the key to analyzing Ferrari is to realize that it is not just another car company, and it doesn’t make sense to analyze it with the same metrics and models as other manufacturers. Ferrari is a luxury company with everything that entails. If we take this into account, the multiples at which it trades don’t seem so outrageous, and we can achieve returns above the market average, even buying at valuations that would be unthinkable for other vehicle manufacturers.

Read the full article here