Co-authored with Beyond Saving.

Today, I want to discuss diversification and allocations. Questions about allocations and their management are among the most common inquiries I receive, both within my private Investing Group and in public forums. It is important to be aware of this because diversification is a key component of risk management.

With The Income Method, we have developed a few guidelines to help investors have an idea of what they should aim for. These include the Rule of 42 and the guideline of keeping position sizes at a maximum of 2-3% of your portfolio (up to 4% or 5% for some funds).

How strictly do you need to follow these numbers? That’s complicated. Remember, I am in a position where my ideas are being read by people with widely varying investment experience, financial positions, and needs. I don’t know your specific situation, your specific goals, and your specific needs. If I did, I still wouldn’t offer you specific advice. I write for people who are interested in managing their own portfolios. My goal is not to tell you precisely what to do with your portfolio. Rather, I aim to pass along the lessons I have learned over the years to make your path a little bit easier.

That said, the Income Method is not “one size fits all.” It is an investment strategy that can be adapted to your particular situation and needs. We provide the framework; you fill in the details to customize the approach to you. It can be tailored to perfectly fit your specific needs and goals.

Today, I want to dive into what we are trying to achieve through managing allocation sizes. The goal is to prepare you to consider your individual situation through a lens where you can decide what is an appropriate amount of diversification for you.

The Rule Of 42

Why is it the “Rule of 42” and not the “Rule of 40” or “Rule of 20” or “Rule of 100”? Two reasons:

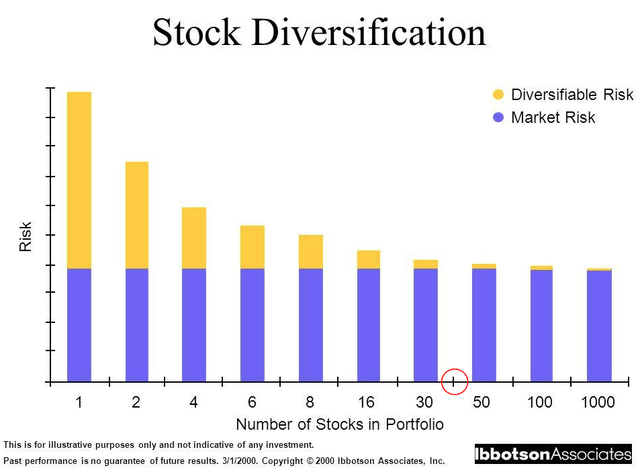

First, around 40 securities are the “sweet spot” for managing what is known as “diversifiable risk.” Diversifiable risk is the risk inherent in a single company. Suppose we have our entire portfolio in one company; then, we carry all the risk if management underperforms. If that one company you decided to invest in was named Enron… You get my point.

Spreading our money to other investments is an easy way to resolve that risk. If you only have 50% of your money in Enron, then your risk is dramatically reduced when the FBI raids their offices; “only” 50% of your portfolio is exposed. While you still lose a lot of money, adding one additional holding “saved” 50% of your money from Enron risk. Instead of losing nearly 100%, you only lose approximately 50%. That’s a big difference.

Say you buy three companies and one is Enron. Now you lose 33%. Note that compared to going from 1 to 2 holdings, the amount of risk reduction is smaller. Investing in one additional company reduced your diversifiable risk by 50%. Adding a third company reduced your risk from 50% – 33% = 17%. Each additional holding you add reduces the amount at risk in a single bad holding, but each addition is less powerful than the addition before it. Eventually, adding another holding or two has a negligible improvement in reducing your risk.

Note that even as you diversify away from company-specific risk, you cannot diversify away from market risk. Diversification does not magically erase all investment risks.

When you get around 40 stocks, you reach a point where adding more doesn’t make what most would consider a significant improvement in risk.

Daviscapitalsite Website

The second reason the Rule of 42 exists is that 42 is the answer to the ultimate question of life, the universe, and everything. It reminds us that we don’t need to get wrapped up in the precision of having exactly 40 holdings. Rather than looking for a specific answer, we need to understand why we want to diversify so that we know whether we are diversified enough.

Also note that 100%/42 = 2.38%. So if you have 42 investments, your individual allocations should be in the 1.5-3% range.

The FBI Gut Check

I am fascinated by the show “American Greed.” For those of you who haven’t seen it, it is a documentary-style show that covers financial crimes, much like Dateline or other real-crime series cover murders.

A recurring theme of the show is that the perpetrator of some fraud is raising money, ostensibly for some kind of super profitable business venture that either isn’t very successful or, in some cases, doesn’t even exist. The victims are often handing over hundreds of thousands of dollars to the fraudster. Often, they are handing over their entire life savings. Then, at some point, law enforcement is raiding the offices and these victims hear the news that everything is gone.

Why do people hand over their entire life savings to a fraudster?

- Their greed – they are convinced that this person has some special way of producing incredible returns. They think they have some special inside track to make more money than everyone else.

- Their fear – many people fear the volatility of the stock market. Fraudsters will often promise that they are taking very little risk with the money. Ironically, out of fear of losing money, they hand money over to a thief for “safekeeping.”

The sad part is, that these fraudsters often take advantage of the people who are closest to them. They are usually stealing from friends, family, and other close associates who have every reason in the world to trust them.

So I propose that with any investment, whether in the stock market, through a friend, family, or wherever, that you do the “FBI Gut Check.” Before you write that check, wire that money, or click that buy button, close your eyes. Imagine you wake up tomorrow, turn on the morning news, and see the offices of the company or person you just invested in being raided by the FBI. How would you rank your feelings?

- Devastated, how will you even make it through the day?

- Panicked about your ability to secure your financial future?

- Do you feel like you need to significantly modify your standard of living?

- Like you were punched in the gut, but you’ll get over it?

- You are upset that you were taken advantage of, but financially, you can shrug it off, take your lumps, and move on.

If your response is 1 through 3 – you are about to make yourself over-allocated. Don’t click that button. A lot of bad news you receive in the market will be nowhere near as bad as the FBI raiding offices, but the point is that you should imagine an extreme scenario. They do happen.

I once invested some money in a “friend’s” business, and after a few checks and after about 6 months, it became apparent to me that this person wasn’t doing what they claimed they would do with the money. Because I did the FBI Gut Check and invested an amount of money that was well into category 5 above, the emotional pain from being taken advantage of by someone who had shared my dinner table was far worse than the financial pain.

For income investors, the most common “bad news” we are going to get is a surprise dividend cut, which often comes with a crashing share price. If you are doing the FBI Gut Check, you will find that when these things happen, it isn’t a big deal. You can shrug it off, and take a look at what happened to decide if there was some red flag you shouldn’t have ignored for your own edification, or if it was just one of those risks you decided to take.

What’s Your Number

I suggest a 2-3% investment in an individual security, which is both consistent with the Rule of 42 and a number that I believe most stock market investors can comfortably shrug off. Is that appropriate for you?

Everyone knows I’m a fan of Warren Buffett. When I mention diversification, many are quick to point out that he has allocations that are much larger than I typically recommend. While he does have 41 holdings in Berkshire’s (BRK.B) equity portfolio, Apple (AAPL) makes up over 40% of it.

Valuesider Website

What gives? Is Buffett taking on crazy risk?

Not really, for two reasons.

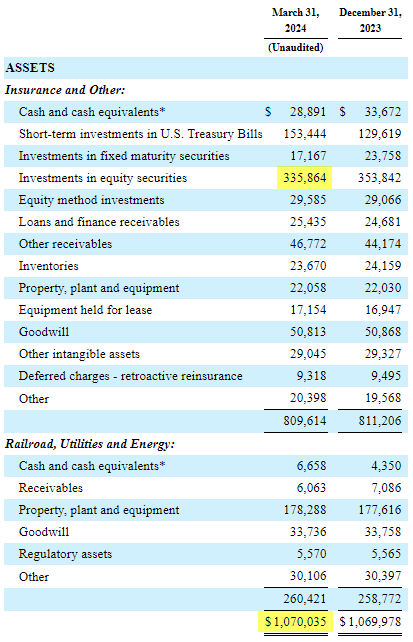

First, BRK’s equity portfolio is not the only source of its wealth. BRK owns several other businesses. Publicly traded equities make up less than $336 billion of its $1.07 trillion in assets (roughly 31.5%).

BRK Q1 2024 10-Q

That is a big chunk of cash, but BRK also has $153 billion in U.S. Treasuries, plus the value of all its businesses which on the balance sheet is very likely an understatement of their value. The assets of these businesses are not marked to market, and there is likely some intangible value. If BRK decided to sell GEICO, it would probably get much more than its book value. Additionally, Buffett owns numerous businesses, real estate, and other investments that are not publicly traded or disclosed.

So when doing the FBI Gut Check, I suspect that Warren Buffett is at a level 5 if AAPL goes belly up. He would most likely be among the least distressed people in the world, and the entire stock market and everyone else in the world would be utterly losing their minds. It would be the collapse of the millennium. If BRK went under, he would probably be at level 4. Even if all of BRK was a big fat $0, does Buffett have to change his daily standard of living? I’d bet not.

Now, if you lost 40% of your investment portfolio, for most of us, that would be a life-altering event – even if you have other types of investments or income outside that portfolio.

Conclusion

We suggest holding at least 42 income-producing investments to ensure that you have a diverse base of income sources in your retirement. Is this a number you must reach immediately? No. Don’t buy stocks just for the sake of diversification. Diversification is one benefit to put on the pro side of the checklist when researching a new investment, but it is not the only concern. You want to make sure you are buying 42 securities that you are confident in. If you are just starting out, that will take time. For our Investing Group veterans, that 42-holding guideline has likely been exceeded. Our “model portfolio” includes well over 45 securities, targeting a +9% overall yield, allowing readers to find the best fit for their income needs. Personally, I would struggle greatly to trim my portfolio down to my top 42. Take your time, do your research, and invest in companies as you find opportunities that suit your goals and risk tolerance.

We recommend 2-3% allocation sizes per holding because that is a range where most are not going to have a hard time if they have a loss. If the number is different for you, that is fine. If you are in a fortunate position where losing 5-10% of your portfolio is negligible to your life, and you have that one position you want to bet big on, that is fine. Just make sure you understand the risks and are willing to accept them if the worst does come to pass.

If you are a hoarder of stocks, and you find that getting a position to 2% is nearly impossible because you have 100+ holdings, that is great too. You aren’t getting much incremental improvement in risk from each holding at that number, but you are likely gaining great sector diversification. Most importantly, you will find it much easier to shrug it off when an individual company turns into a bad investment. The larger your portfolio, the more effort it takes to keep up with what is happening. That’s one of the reasons I’ve surrounded myself with some of the smartest experts I’ve met to help me follow my portfolio.

If you conclude that you are over-allocated to some positions, I would recommend this article:

Managing Risk, How To Rebalance Your Portfolio

This article will help you identify what method of rebalancing works best for you.

When it comes to allocation sizes, it is important to keep in mind why we diversify, and for you to be able to measure your own risk tolerance. This is far more important than the exact numbers. Hopefully, today, we have provided you with some insight to chew over and think about your own portfolio to find the ranges that are best for you.

Read the full article here