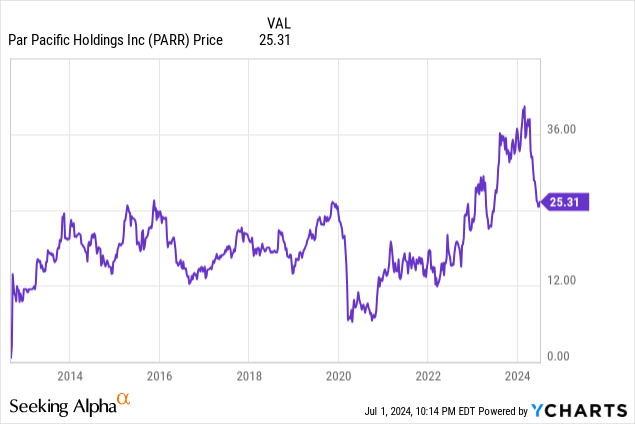

Refiner and gas station operator Par Pacific Holdings (NYSE:PARR) has had a wild run over the last eight years. With the stock price dropping sharply this year because of poor operating results, some consider the stock now to be a buy. I am not so sure because I see too many problems with their operations and management. I rate PARR a hold. This is an update to my prior articles.

Irrational Stock Repurchases

I want to start with a major reason why I will not buy PARR. In the past, I recommended buying PARR in a June 2016 article, and I bought/sold the stock multiple times over the years. Since my last article in February 2023, it seems management has become irrational managing their finances, in my opinion. In 2023, they used $67.821 million to repurchase 1.946 million shares at an average price per share of $34.85 compared to the current PARR price of $25.31. Up to May 6 of this year, they spent $73 million to repurchase stock, and they just authorized a new $250 million stock repurchase program. I am absolutely against this repurchase. Par Pacific has junk debt ratings of Ba3 by Moody’s and $635 million long-term debt. Plus, the company lost $3.7 million in 1Q’24. Instead of stock repurchases they should pay down debt to improve their debt ratings because under the March 2024 amended ABL loan agreement if S&P upgrades their debt the interest rate on the ABL loan would decrease 0.25%.

They are in a very high-risk commodity business where financial leverage can be a friend or your worst enemy. These stock repurchases are very troubling, in my opinion, especially when their CEO was selling PARR stock. William Pate, who was CEO until a few weeks ago when he retired in May, sold 150,000 shares last November at an average price of $34.88.

While I doubt, Par Pacific is headed into serious financial trouble. I too often see large stock repurchases eventually put companies into very serious trouble. Big Lots (BIG) is currently in serious financial trouble after making massive stock repurchases a few years ago, for example. I often cover distressed/bankrupt companies, and I constantly see that prior irrational stock repurchases were a major factor for the company’s demise.

Billings Refinery – Purchased in 2023

My initial reaction to their purchase last year of Exxon’s Billings refinery was positive. Now, however, I have a mixed opinion. The headline purchase price of $310 million is misleading. That price included a 65% interest in Yellowstone Energy Limited Partnership and a 40% interest in Yellowstone Pipeline Company, which collectively were carried on their June 30, 2023, balance sheet after the purchase for about $84 million. This implies that Par Pacific paid about $226 million just for the refinery. This seems very cheap for a 63,000-bpd refinery. There are two problems with this assertion. First, they also had to pay over $299 million for the refinery’s inventory. Second, this is a very old inefficient refinery that had production costs of $12.44 per throughput barrel in 1Q’24 (Compared to $4.89 in Hawaii, $7.86 in Wyoming, and $6.07 in Washington.) The total purchase price was over $638 million – not $310 million. When you analyze the return on their refinery investment, you really need to add $226 million plus the $299 million inventory and use $525 million.

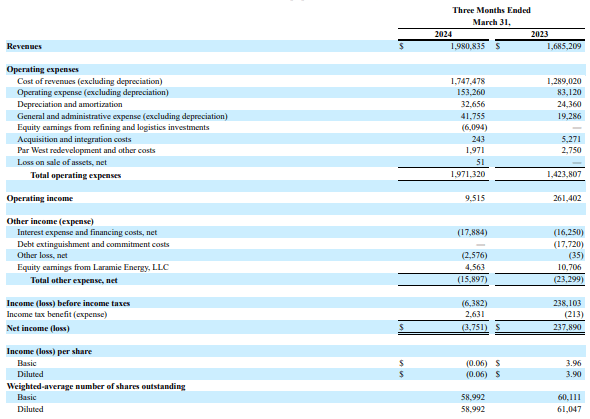

First Quarter 2024 Results Were Disappointing

The current PARR stock price reflects their very disappointing 1Q’24 results. While the winter season usually has a negative impact, the profit margins at all their refineries were weak, especially compared to 1Q’23. Par Pacific reported a GAAP loss of $(0.06) per share, compared to a profit of $3.96 in 1Q’23.

First Quarter Income Statement 2024 and 2023

1Q 10-Q (sec.gov)

Hawaii’s adjusted gross profit margin was $14.00 per barrel compared to $19.11 in 1Q’23; Washington $6.13 compared to $11.07; Wyoming $14.84 compared to $27.54; and Montana was $13.82. (Note: The results for 2Q’24 will be negatively impacted by major maintenance/turnaround at the Billings refinery.) These lower margins were the result of weaker crack spreads in their various markets. The retail segment had an operating income of $11 million in 1Q’24 compared to $13.5 million in 1Q’23. The only bright spot was logistics’ operating income increased in 1Q’24 to $20.4 million from $12.6 million.

Par Pacific Is Also in the Tourism Industry

Many investors just consider PARR to be an energy trade, but you really need to look at it from other angles. For example, it is also effectively in the tourism industry. Much of the Hawaiian economy is based on tourism, plus many tourists rent cars that use gas from their Hele gas stations. Tourist travel to Hawaii is down 4.1% so far this year compared to last year. Seasonal tourists traveling to national parks in Wyoming, Montana, and South Dakota use a lot of gas from their Billings and Newcastle refineries. So far, this year, tourist travel in this area has improved over last year. Yellowstone visitor numbers are up 11%, for example.

EV Sales Impacting PARR

Within the energy industry, EV usage has a significant long-term impact on Par Pacific. Their refineries in Montana and Wyoming are expected to be impacted much less than their Hawaii and Washington refineries/gas stations because it is often not practical to drive an EV in rural areas. This is reflected in 2023 EV sales. In Montana, 3.40% of vehicle sales were EVs last year, 2.11% in Wyoming, and 2.12% in South Dakota. Hawaii and some of their Washington markets are urban, so EVs are more practical. EV sales in Washington were 18.79% of vehicle sales in 2023 and 11.01% in Hawaii. If these percentages increase, it would have a very negative long-term impact on the company’s operations.

Laramie Energy – Natural Gas Exposure

Their 46% ownership of Laramie Energy, which has natural gas production in the Piceance Basin in Colorado, had some developments since my February 2023 article. As I mentioned in that article, it was carried on Par Pacific’s balance sheet at zero, but it is now carried at $18.8 million and actually had a one-time $10.7 million distribution in March 2023. While the $18.8 million is only about $0.32 per PARR share, it is a nice improvement.

May Conference Call

There were some interesting discussions during the May conference call. Matthew Blair from Tudor, Pickering, Holt asked as part of a question: “…is Par open to being acquired?” CEO Will Monteleone answered:

And ultimately, I think any future M&A activity, whether we’re acquiring or we’re the target, I think we’re ultimately focused on maximizing shareholder value….it wouldn’t be appropriate to specifically comment on whether we would be a target, but I think at the end of the day, we’re focused on shareholder value.

Interesting. Often, management strongly assert that they want to remain independent and have no interest in being acquired.

A different part of that same line of questions was regarding NOLs. According to management, the company has about $900 million NOLs. Using the 21% current corporate tax rate, that implies a value of about $189 million without factoring the present value of the income tax savings, or about $3.25 per share.

Renewable Fuel Project in Hawaii

I am taking a wait and see approach regarding their new $90 million liquid renewable fuels manufacturing facility under construction in Hawaii. According to management it is “expected to produce approximately 61 million gallons per year of renewable diesel, sustainable aviation fuel, renewable naphtha and liquified petroleum gases”. In theory, this could be very profitable and also help reduce greenhouse gas emissions. I worry, however, it could also reduce Par Pacific’s profits if there are operating issues, but we will have to wait until 2025 or 2026 to see actual production/profit results.

PARR Stock Valuation

Some may assert that PARR stock is cheap because of their low P/E. I am not so sure. The 2024 EPS consensus estimate is $2.84 with a high of $3.52 and a low of $2.50. Using $2.84 and the latest PARR price of $25.31, their P/E based on estimated EPS is 8.9x. That is not cheap, in my opinion, because they don’t pay a dividend, their debt has a junk rating, they are in a risky commodity business, and their long-term outlook is questionable because much of the world wants to end the use of fossil fuels. The only positive “kicker” might be the potential for some future buyout.

Conclusion

I bought/sold PARR stock a number of times over the last 8 years. One of the reasons I originally became interested in the company in 2016 was because Sam Zell was a major holder, but he died in 2023. I will not consider buying the stock now because of the irrational financial approach that the current management is taking by making large stock repurchases instead of paying down debt.

Because I don’t see refinery margins improving significantly and because I worry about EV sales in Hawaii/Washington on a long-term basis, their 8.9x P/E is no bargain. I continue to rate PARR a hold.

Read the full article here