I reviewed Zoetis (NYSE:ZTS) nearly a year ago and gave the company a “Buy” rating. I liked that the company was focused on continued innovation and is a global leader in a niche market.

Since that article, the stock is nearly flat, certainly underachieving compared to the S&P 500. Despite these lackluster results, I’m still a believer in Zoetis and remain bullish on the business.

Let’s dig into current events and the company’s recent financial performance.

Safety Concerns?

I believe Zoetis’s lackluster performance in the first half of 2024 is in some part due to the Wall Street Journal article published last April, which accused Zoetis’s arthritis drugs (Librela and Solensia) of having harmful effects to owners’ pets.

On the company’s Q1 2024 conference call, CEO Kristin Peck adamantly defeated the company’s arthritis treatment drugs, saying this about Librela, “…I really want to underscore that we have the utmost confidence in the safety and efficacy of Librela. It has been used for over three years across the globe and over 14 million dogs, and it’s approved in over 50 countries. And if you overall look at the rate of reported adverse events, it’s about 18% per 10,000 or 0.18% globally.”

Regarding both drugs and Zoetis’s safety standards, Peck went on to state, “We are unwavering in our commitment to rigorous safety and quality standards, which has earned us the trust and confidence of veterinarians worldwide. Backed by that commitment, Librela and Solensia are safe and effective. They are anchored in 10 years of science and have been used in Europe for more than three years. In the U.S., 78% of veterinarians who are at the center of care are very satisfied with Librela. This is driven by real world experience and consistent with the feedback we hear in other markets. And our research indicates that 46% of vets globally will treat OA earlier and 65% will treat more dogs now that Librela is available.”

Safety concerns are always a risk with a healthcare company, but it seems to me these accusations might have overstated. The company’s management still believes osteoarthritis pain (OA) will be the next billion-dollar opportunity for Zoetis.

In the first quarter, Librela sales grew 189% percentage globally, with $40 million in U.S. sales. Despite, the negative media attention, management didn’t alter revenue guidance for Librela. Until guidance is changed, or the adverse side effects become more of a pronounced issue, I’m inclined to believe the investment thesis for Zoetis is firmly on track.

People Love Their Pets

A bet on Zoetis is a bet on individuals continuing to care about their pets. The data certainly supports the human-animal bond is strong, as 86% of pet owners stated they would pay “whatever it takes” if their pet needed extensive veterinary care. Furthermore, a study found even with a 20% decrease in a family’s budget, pet owners would not spend less on their pets.

Moreover, the “loneliness epidemic” has been gaining attention after the COVID-19 pandemic. In a past survey conducted by the U.S. Health Resources and Services Administration, “Two in five Americans report that they sometimes or always feel their social relationships are not meaningful, and one in five say they feel lonely or socially isolated.”

Many studies have been conducted which show that pet ownership can help alleviate loneliness. One particular study conducted by BMC Geriatrics found that in an analysis of roughly 5,000 older adults, those who owned pets were less likely to report being lonely.

As I don’t see the human-pet connection fading, nor do I foresee the “loneliness epidemic” going away (although I understand it’s a more complex issue than simply getting a pet). Humans will continue to have pets, and that’s why Zoetis’s focus on companion animals will pay dividends in the future.

Financials

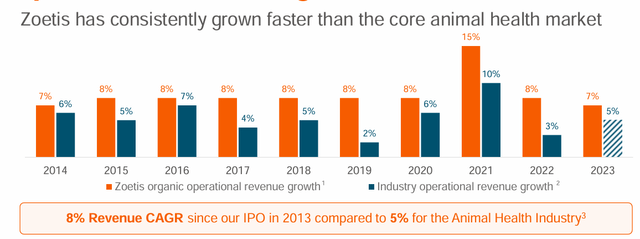

Since Zoetis went public back in 2013, the company has outpaced the S&P 500 despite the company’s subpar performance this year.

As you can see below, Zoetis has an 8% revenue CAGR since that time:

Investor Presentation

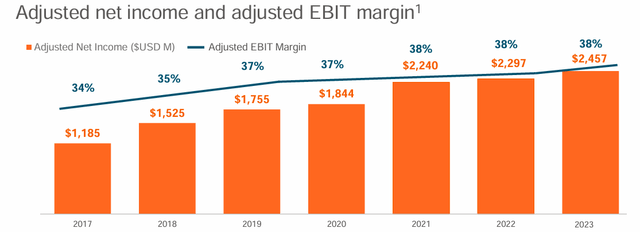

The company’s adjusted net income and adjusted EBIT margin have continued to climb as well:

Investor Presentation

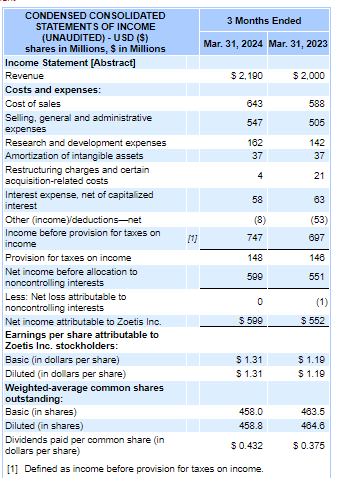

In the latest quarter Zoetis delivered sales of roughly $2.2 billion, which is an increase of 10% compared to the prior year quarter. U.S. sales for the quarter were $1.2 billion, an increase of 16% compared to Q1 2023. International sales were $1 billion for the quarter, which is an increase of 3% compared to Q1, 2023.

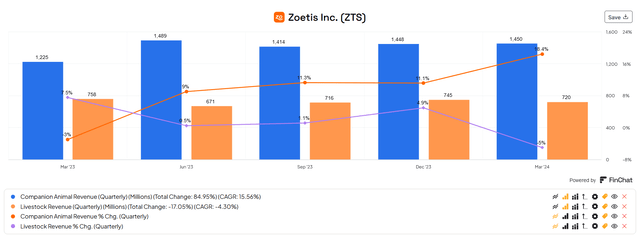

Zoetis’s companion animal portfolio was the main driver of revenue growth for the quarter, as sales of companion animal products grew 25% in the United States and 10% internationally.

As you can see from this graphic, companion animal revenue has continued to lead livestock revenue over the last few quarters and revenue growth is significantly higher for companion animal compared to livestock:

Finchat.io

This revenue growth led to Zoetis reporting higher net income and higher earnings per share, as you can see below:

SEC.gov

Given the strength of the company’s companion animals products, Zoetis increased their full year 2024 guidance as they now expect revenue between $9.05 billion to $9.2 billion and net income between $2.45 billion and $2.495 billion.

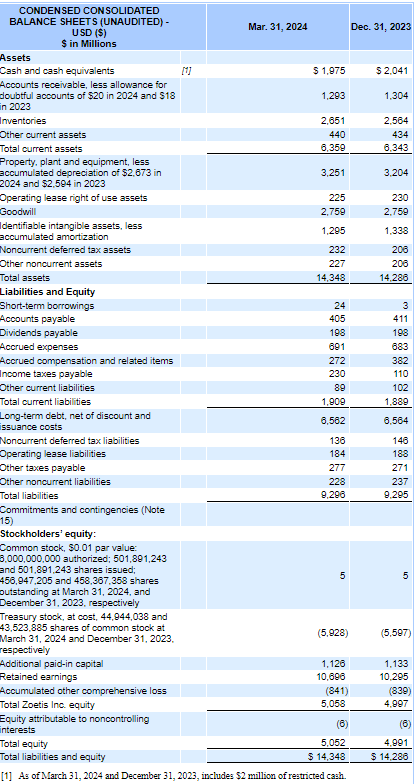

From a balance sheet perspective, Zoetis does have more long-term debt than I generally like to see, however the company still has amble current assets to cover all of their current liabilities as you can see below:

SEC.gov

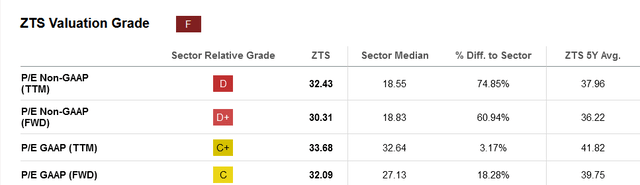

Valuation

As a leader in a global niche market, Zoetis trades at a premium valuation, as some of the metrics below illustrate:

Seeking alpha

However, I think Zoetis’s valuation is reasonable given its growth prospects and position as a leader within the pet healthcare industry.

I think P/E ratio is a good valuation metric for Zoetis. Last year Zoetis was trading at a P/E GAAP (FWD) ratio of 34.05 which, as you can see above, is below the current P/E GAAP ratio of 32.09. This is also well below the company’s five-year average of 39.75.

Given the company’s growth prospects, especially the noted billion-dollar opportunity with osteoarthritis pain and Wall Street’s belief that earnings per share will continue to rise as revenue grows at a rate between 8% to 10% over the next few years, I think investors feel comfortable buying that these levels. Although, the stock’s price was more attractive in April near $150, it is still below the $190 price back in January of this year. Thus, I feel comfortable adding to my position in the $175-$180 price range.

Risks

Zoetis lists numerous risks with the company’s risk factors section within their 10K, but I’m going to cover two main risks I foresee for the company.

As I noted with Wall Street Journal, I think safety concerns with products will always be a long-term risk associated with Zoetis. Aside from a decline in revenue, litigation would be a concern as well should a top-selling product, such as Librela, produce harmful side effects.

Second, as Zoetis is a global company and their international sales are a significant amount of the company’s overall sales, I think Zoetis is subject to more global economic and political risks. Continued global conflict in places like Israel, Russia/Ukraine and the Middle East could certainly negatively impact the company’s bottom line.

Conclusion

I think Peck stated Zoetis’s investment thesis perfectly when she said this on the latest conference call, “…For more than 70 years, Zoetis has been leading the industry with our commitment to innovation. We’ve invested over $5 billion in R&D since our IPO, which has brought more than 300 product lines to the market. Science is and always has been the great disruptor and at the core of our success in delivering the innovations that veterinarians, livestock producers and pet owners expect from us.

Despite some recent safety concerns, I still believe Zoetis is a high quality business. Zoetis has continued to grow revenue and create new drugs for both companion animals and livestock.

I think the bond between humans and pets is strong, and pet owners are more willing than ever to treat their pets.

Although Zoetis is not a cheap stock, I believe this company will reward patient long-term investors.

Read the full article here