MongoDB’s (NASDAQ:MDB) stock dropped by more than 20% in the aftermath of the first quarter of fiscal year 2025 (FQ1) results, despite revenues increasing by 22% YoY and beating topline estimates. However, it lowered sales guidance for the fiscal year ending in January 2025 (FY-25), implying reduced growth, from 14% to 12%.

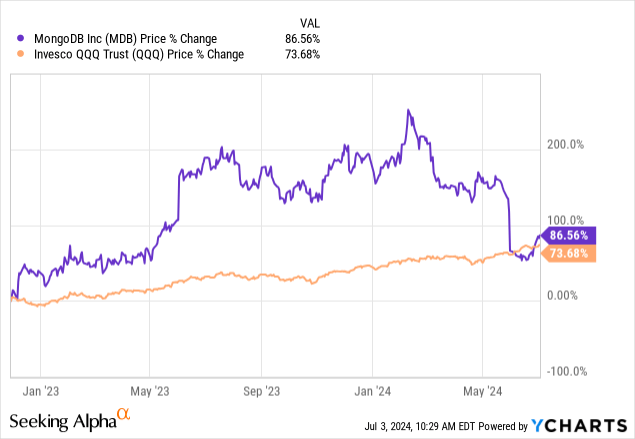

The price action since the end of November 2022, which coincided with the launch of ChatGPT is illustrated in the chart below and shows that the stock has outperformed the tech-heavy Invesco QQQ Trust (QQQ). In this respect, some are highly optimistic about MongoDB’s AI opportunities, which are expected to start materializing during this half.

However, this thesis aims to show that such optimism is unjustified given that, in addition to opportunities, Gen AI also comes with challenges. Hence, despite the stock trading around $265, it is not a buy as the price could fall further.

I start by investigating the reasons for demand weakness.

Faces Demand Weakness

For those who are new to its technology, MongoDB specializes in No SQL (or no sequel) or non-relational databases. In this context, there are basically two types of databases: relational databases, the standard database that stores information in tables and has been championed by the likes of Oracle (ORCL), Microsoft (MSFT), and others. Then there is the MongoDB non-relational database, which is designed with the cloud in mind as well as with the idea that the volume of data can grow exponentially, meaning that the data store has to be very scalable.

This means No SQL is an appropriate solution for customers who already have lots of data that is going to grow over time. Moreover, it differentiates itself by being document-based with the primary product called Atlas, a cloud usage-based business. Income is earned both through subscriptions and product licensing for on-premises deployments.

However, as mentioned earlier, Atlas has been suffering from slower-than-expected consumption which could have a downstream impact in the remainder of fiscal 2025 explaining the reason for the lower guidance. Coming back to FQ1, despite the double-digit growth, non-GAAP gross margins declined to 75% from 76% YoY and as per the CFO, this was due to Atlas’ share of the overall business increasing. Now, revenue growing at 22% YoY while margins decreasing by 1% could be due to lower product pricing to drive adoption in a highly competitive marketplace, one where newly acquired customers are consuming less than expected.

In this case, MongoDB competes with hyperscalers like Google (GOOG) and Amazon (AMZN) without forgetting Oracle and many others, and the problem when facing giants is the risk of losing market share due to product bundling, especially during a challenging macro environment. For example, it may be cheaper for a customer who has an IaaS subscription to the clouds of these giants to add a No SQL service than to look for a separate SaaS provider like MongoDB.

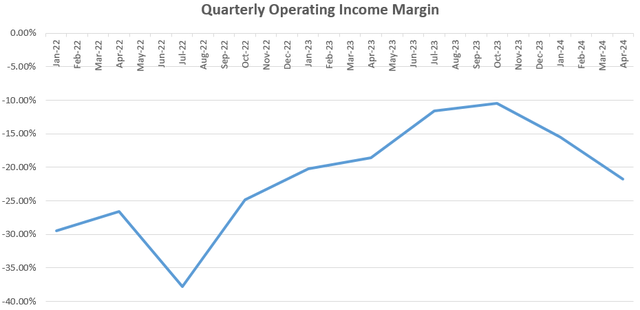

Now, I am not in a position to say what’s definitively going on but the fact that non-GAAP operating margins for FQ1 fell by 5% YoY may imply having to spend additional marketing dollars to “motivate” customers to sign multi-year deals, especially at a time when the pipeline for the rest of the year is coming less than expected. Also, as charted below, a downtrend in operating margins already started in the fourth quarter of fiscal 2024.

Chart built using income statement data from (seekingalpha.com/)

Faces Another Challenge in addition to Weak Macros

Now, the main reason for this weakness is attributed to a “softer macro environment”. Looking across the industry, other software companies like UiPath (PATH) seem to be suffering from elongated sales cycles, which are again being blamed on customers tightening their wallets and not willing to spend as much money as they had been previously. Well, this may be true because of the uncertainty caused by high interest rates (above 5%) and inflation persisting above 3%, but, this is only part of the explanation for two reasons.

First, the headwinds suffered by either MongoDB or UiPath are not aligned with Gartner, whose researchers expect that there should be more IT spending this year compared to 2023. Thus, growth for software and IT services are expected to accelerate by 13.9% and 9.7% respectively. The second reason seems related to the disruptive nature of Generative AI, especially the GPT (Generative Pre-Training Transformer) which enables text to be created out of large datasets in response to queries in a friendly manner. Thus, by encapsulating this feature in applications like ChatGPT, interactive tools have emerged that immensely facilitate the task of software development, a feature that can encourage more in-house teams to take control of their IT, which could come at the expense of outsourcing to companies like MongoDB.

However, looking into the rear mirror, MongoDB announced AI-powered capabilities to help developers become more productive back in September 2023, but this seems not to have yet shown up in MongoDB’s numbers. Looking further, the innovation has up to now been beneficial to chip and infrastructure companies, where the real investments are happening.

www.mongodb.com

However, after spending billions of dollars on advanced computing chips, customers need to see returns on investments, which should benefit software plays be it those specialized in databases or applications. For this purpose, the company has also launched MAAP (MongoDB AI Application Program) in collaboration with the three hyperscalers in May. Also included are industry-leading consultancies like Accenture (ACN) and AI model providers with the objective is to establishing an ecosystem including professional services to help customers start. MAAP is viewed as a growth driver, over time. The company has also partnered with a bank to modernize its customer service applications.

Thus, MongoDB may be at the start of its journey to benefit from AI, but, more than one and a half years since the popularization of Gen AI and in the absence of a dollar-based pipeline, it is too early to be optimistic. To this end, according to Gartner, this year should be about planning Gen AI which includes experimentation and prototyping to determine which aspect of the innovation will drive more efficiencies in their business or what is best for the customer experience. Gartner adds that this planning process should be beneficial more to data centers in 2024.

Talking disruption, according to McKinsey with the ability of Gen AI to lower the expenses associated with data migration and shifting away from legacy systems, it is probable for startups to emerge and take market share away from incumbents like for example MongoDB or even Oracle. McKinsey also estimates that with more companies like to undertake software development tasks including data access & synthesis in-house, churn for system integrators could increase by 1% to 3%.

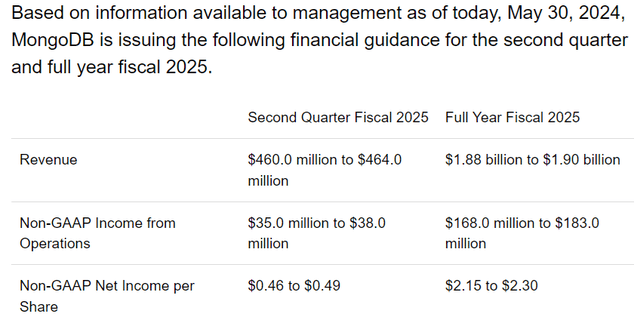

Therefore, the company not only faces large competitors but may face smaller startups that have been agile in leveraging Gen AI, or even the risk of seeing further weakness in multi-year deals as customers carry out more developments in-house, also pressured by weaker macros. In this case, MongoDB may have to provide discounts to lure customers, which may impact profitability and push it further away from breaking even (above chart). Hence, there is the possibility that it could fall short of attaining guidance for FY-25, or these may be reviewed lower. Alternatively, it could achieve the topline target but at the expense of EPS as it spends more marketing dollars.

FQ1 Earnings Press Release (seekingalpha.com)

Has Potential But The Downside is Likely to Continue because of High Expectations

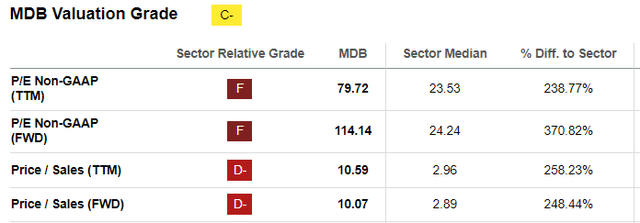

This is the reason for my pessimistic outlook for a stock that remains overpriced relative to the IT sector median by a large percentage both based on sales and earnings metrics as illustrated below. Hence, I estimate it could fall by 12.9% or the percentage by which it has outperformed QQQ as per the introductory chart. This results in a share price of $231 (265 x 0.871).

seekingalpha.com

Therefore, in case there are no AI-led breakthroughs to boost financial results, the stock could fall further.

This said, I could be wrong in my outlook given they do have $2 billion in cash versus only $1.2 billion of debt, and this keeps on growing. This is a cash-flow-positive business that has been generating more money from operations during the last three quarters. This means it can make an acquisition that could accelerate growth, but it will depend on execution.

Additionally, it could benefit from artificial intelligence like using the technology to migrate legacy and mission-critical workloads of large businesses whose developers are gone (have either retired or left). Such migrations are essential for regulatory and technological evolution reasons but are difficult to perform, entail high risks, and are costly. However, it is unlikely for customers to recruit new developers or hire startups for the job, which puts MongoDB in an appropriate position to secure such contracts as it can dramatically reduce migration duration and cost while proceeding systematically through pilot projects. As per the CEO, many have shown interest in such modernization opportunities that fall under the enterprise channel which could see the strongest growth, but he also mentions this is over the long term.

Moreover, such use cases involve dealing with the data, one of MongoDB’s strong points. Tellingly, data is a key ingredient for Gen AI models to be trained before they can deliver intelligent AI apps and MongoDB is well positioned, but its high valuations show that the market expects results rapidly, which appears unlikely. Moreover, high sales growth accompanied by lower margins tends to indicate more of a highly competitive environment where the company is not currently managing to differentiate itself through its technology.

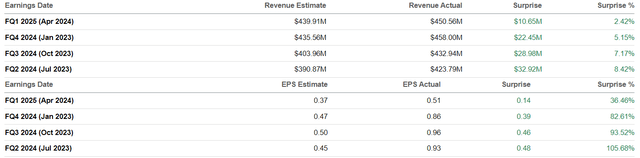

Therefore, I do not believe that AI opportunities will translate into sales this year making it more likely for the stock to be volatile, implying that it is not time to buy the dip. Finally, to justify my bearish stance, the percentage surprise or by which revenues and EPS have beaten estimates have both trended downward since the last four quarters as illustrated below. This may show that it is becoming increasingly difficult to close larger and more profitable deals.

Revenue and Earnings surprises – Quarterly (seekingalpha.com)

Read the full article here