In my opinion, there is a very large upside to be had in Zscaler (NASDAQ:ZS) stock over the next year due to present lower valuation multiples compared to historically. I believe that the company’s P/S ratio is likely to contract further, but high future estimated revenue per share growth from Wall Street analysts indicates outsized returns anyway. The company is one of the leaders in the SaaS cybersecurity field, and in my opinion, it offers the best valuation among other leading players at this time. The advanced cybersecurity market is currently in high growth amid trends in digitalization and AI, which is why I am bullish on Zscaler, given its lower valuation compared to major competitors like Palo Alto Networks (PANW) and CrowdStrike (CRWD).

Operational Analysis

Zscaler’s core products and services include Zscaler Internet Access, which provides secure access to external applications and internet destinations, and Zscaler Private Access, which offers secure access to internal applications. In addition, its Zero Trust Exchange is a cloud-native platform that connects users, devices, and applications using zero trust principles.

Zscaler’s security services are cloud-based without the need for on-premises controls. It also provides URL filtering, anti-virus, sandboxing, and other security controls. The company uses a distributed cloud architecture and has data centers established globally. It was recognized as a leader in the Gartner Magic Quadrant for Security Service Edge and serves over 30% of Forbes Global 2000 companies. The company processes approximately 400 billion transactions daily.

Significant long-term growth catalysts for the company include cloud adoption and digital transformation. McKinsey has stated the significance of cloud platforms in facilitating digital transformation, claiming that cloud platforms can “bring new capabilities to market about 20 to 40 percent faster”. In addition, new SEC cybersecurity disclosure rules, as discussed in the University of Maryland article, are likely to increase investment in cybersecurity.

Zscaler’s Zero Trust Exchange platform is key to its offering. The technology provides secure access, a reduced attack surface and comprehensive inspection, all with AI and machine learning integration on a cloud-native platform. Put simply, the Zero Trust Exchange platform eliminates the need for complex network segmentation and multiple-point products. Management has unified its services into a single, integrated cyber threat protection, data protection, zero trust connectivity, and digital experience management platform.

There is also future potential for management to adopt AI in its cybersecurity offerings and have AI-as-a-service solutions that automate threat detection, monitoring, response and mitigation tasks. While this is already being implemented to some degree, it is less extensive than it would need to be to operate fully autonomously, particularly as it relates to threat response. As the demand and needs of organizations become larger and more sophisticated as the cyber-threat landscape evolves, Zscaler’s TAM is likely to expand, in my opinion.

Financial & Valuation Analysis

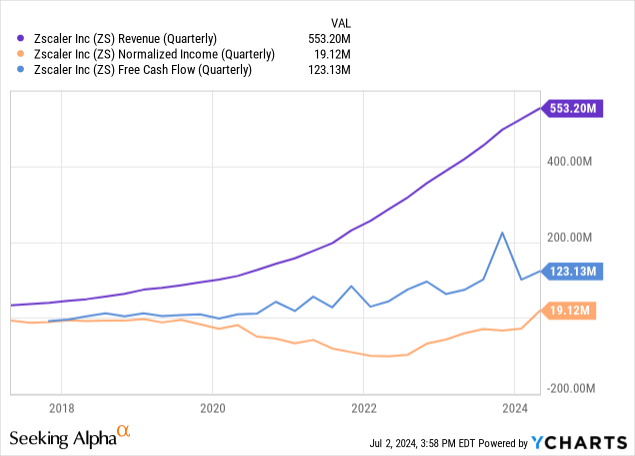

Zscaler has been delivering extremely strong revenue growth, but it is yet to deliver a profit, other than on a normalized basis, where it reported a profit for the fiscal period ending July 2023. However, its free cash flow growth has been good, primarily because the company has been giving stock-based compensation of very large amounts each year.

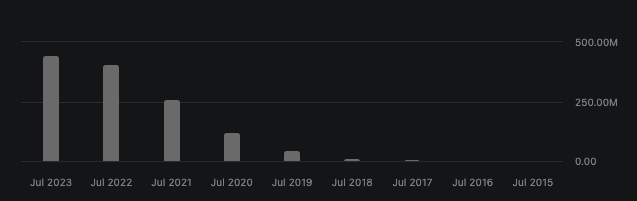

ZS Stock-Based Compensation (Seeking Alpha)

The fact that much of the net income loss is due to SBC is promising, in my opinion. It shows that the company’s fundamental growth is extremely strong, and while the SBC is diluting shareholder value, long-term investors likely do not mind, as the net benefit of high SBC on attracting talent and driving results is arguably worth the current depletion in profitability and value per share.

However, one area where I am less pleased is the company’s balance sheet because its equity-to-asset ratio is 0.26, and its debt-to-equity ratio, including lease obligations, is 1.13. Most of its current liabilities are unearned revenue, and most of its long-term liabilities are long-term debt. This is more of an issue to me than the high levels of SBC because I believe that this high level of liabilities has the potential to inhibit its growth and acquisition strategy moving forward.

CrowdStrike, which is one of Zscaler’s key competitors, has an equity-to-asset ratio of 0.37 and a debt-to-equity ratio, including lease obligations, of just 0.31. Palo Alto Networks has an equity-to-asset ratio of 0.25 and a debt-to-equity ratio, including lease obligations, of 0.34. Therefore, while high levels of liabilities are common in this relatively new industry, it is Zscaler’s level of debt to equity, which I believe significantly inhibits it at present compared to competitors. Such a high level of debt and the associated interest payments will certainly leave it with less liquidity to expand, develop and iterate effectively.

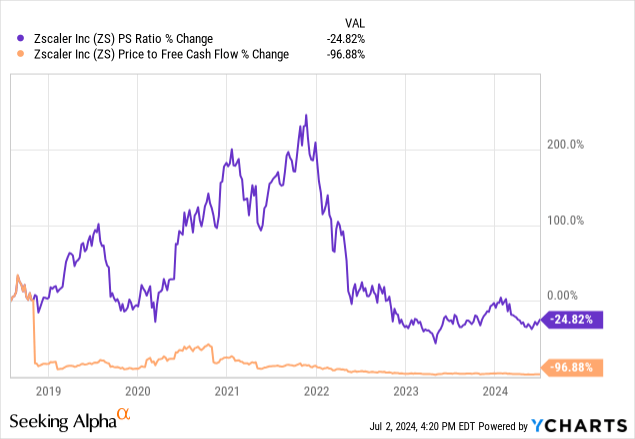

Given the lack of profitability thus far, it is difficult to ascertain a fair value for Zscaler. Instead, I think it is more appropriate to adopt a price target based on multiple estimates over the next 10 years. To start with, this is how the valuation multiples have adjusted since its IPO:

At this time, Zscaler has a forward P/S ratio of 14, compared to 24.67 as a 5Y average. It is difficult to ascertain what P/S ratio the market will tolerate for Zscaler moving forward. However, based on consensus Wall Street estimates, a revenue CAGR over the next 10 years of around 22.5% seems reasonable to me to predict what Zscaler will achieve. Given that, and the fact that this CAGR is significantly lower than the 52% revenue CAGR the company has delivered as a 5Y average, I think the P/S ratio will contract. In my opinion, a contraction to a P/S ratio of around 9 over 10 years is probable. Given that the current revenue per share is $13.69, my price target for 2034 is $937.58, implying a 16.86% price return CAGR given the present stock price of $197.39.

That being said, I think that investors must prepare for periods of high volatility, including periods where the stock price may become over-inflated due to moments of higher adoption of digital cybersecurity services alongside trends in AI. As such, I do not think it is unreasonable for investors to sell their position if the stock rises toward a point where the implied 10Y CAGR becomes closer to 10%. Doing so would mitigate risk from downside volatility that could occur if management does not meet quarterly expectations or competitive threats become more severe.

In addition to this, I think it is important that shareholders monitor the company’s profitability, as a failure to stabilize this over the next few years and maintain growth will likely dampen investor sentiment. Because we have not yet had reliable proof that management can sustain profitability on the net income level without high levels of SBC, I think some caution is warranted. In my opinion, a reduction in SBC is likely to improve overall profitability at this stage. So, I think it would be wise for management to begin looking at curbing the SBC program to begin favoring long-term net income.

Risk Analysis

The Zscaler ThreatLabz 2024 AI Security Report brought to light the increasing sophistication of AI-driven cybersecurity threats. Unauthorized AI applications, or “shadow AI”, can introduce vulnerabilities and data leakage risks. While it is promising that Zscaler has highlighted this threat and is actively working to mitigate the risk, potential vulnerabilities may arise if it cannot stay competitive. This risk is further enhanced by the fact that its balance sheet is weaker than I would like, potentially inhibiting the aggressive M&A it would likely benefit from to stay competitive in combating advanced AI-led cybersecurity threats.

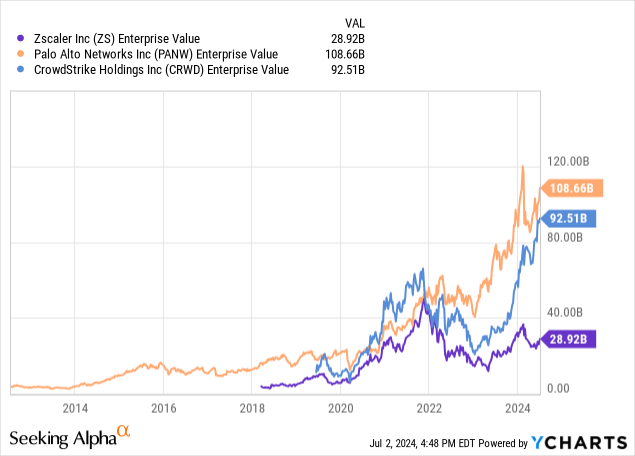

The rapid pace of technological change is also likely to have a constraining effect on the company managing to maintain profitability growth rate expansion. In addition to advances in threat capabilities, there are also likely to be iterations and developments from competitors, including CrowdStrike and Palo Alto Networks, who have both expanded into zero-trust architecture. Both competitors have a much higher enterprise value compared to Zscaler, giving them a much higher capacity to consolidate their moats as well as acquire emerging companies. I believe the threat to Zscaler purely based on size shouldn’t be underestimated at a time when AI cyber-threat capabilities are likely to intensify, and the larger, more prepared companies are better equipped to deal with this. Small-cap and mid-cap cybersecurity firms are definitely likely to face challenges, in my opinion, and large-cap companies like Zscaler will have to reinvest aggressively to remain proficient.

Conclusion

I think the likelihood of Zscaler achieving 15%+ price returns over the next 10 years is likely, even given the risks that could affect its profitability growth. I think the P/S ratio is likely to contract significantly, but the high levels of revenue growth anticipated offset this. In addition, the company’s SBC policy is probably due to begin to be eased to help aid its net income growth, as this is the biggest cause of the current lack of net income. That being said, a gradual and strategic approach to this would be wise for management to retain the necessary incentives to drive growth. The company has already developed significant free cash flow growth to prove that it is running a sustainable business model. Therefore, I am rating Zscaler a Strong Buy, with caution warranted from high volatility, which I presume is likely, and balance sheet risks creating some inhibition in management’s ability to compete in M&A over the long term.

Read the full article here