Investment Thesis

Compass Diversified (NYSE:CODI) is off to a great start according to its first quarter earnings report, with adjusted EBITDA up 28% YoY. The company is well-diversified and has various ownerships in innovative yet defensive businesses with valuable brands in my view. While I respect management’s savvy acquisition track record, I think the stock is still fairly priced and unlikely to outperform the S&P 500. If investors want stable income with low volatility, however, Compass Diversified may offer a better alternative to index funds as it will likely offer a smoother ride than the S&P 500. In the long term, however, I think Compass Diversified as this price point will not outperform the broader market so I give the stock a hold rating today.

Company Overview

Compass Diversified “is a publicly-traded holding company that provides shareholders with unique access to middle-market businesses – an attractive segment of the market historically reserved for private equity or other legacy players” according to its website. They target smaller businesses that earn an attractive return on capital with highly valuable brands and a strong customer base.

The company has a successful track record of creating value, as they have focused on defensive companies that can weather economic storms and perform well during cyclical lows in the economy. Their portfolio of companies can be categorized into two segments: branded consumer businesses and industrial businesses.

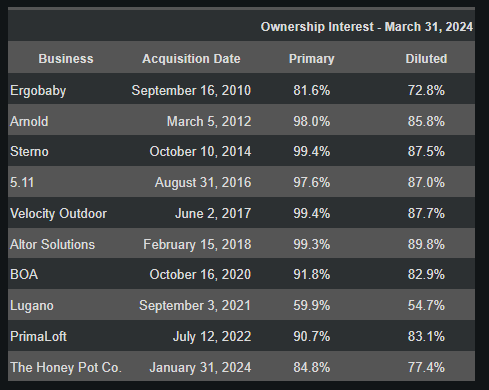

According to the annual report, as of March 31, 2024, they own the following businesses:

Annual Report (Seeking Alpha)

Investors can see that the portfolio is pretty concentrated on consumer branded products such as apparel, food warming products, high-end jewelry, and other businesses. My analysis of these portfolio companies is that in general they are consumer oriented and can pass on the cost of inflation to their customers pretty easily. Furthermore, they are relatively defensive in nature to me and thus have financial performance that is typically not cyclical.

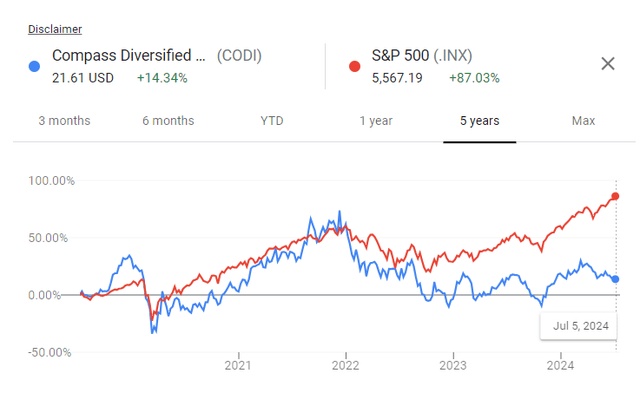

Management’s track record is quite good, but overall has not beaten the S&P 500 in terms of value creation. Over the past 5 years, the S&P 500 has increased 87% in comparison to CODI’s 14%, both excluding dividends. What this means to me is that management has focused on more defensive names revolving around consumer brands, while the S&P 500 has very high-flying tech names that have bigger market potential and better profit margins.

Google Finance

Thus, due to CODI’s lack of technology exposure, it seems to me it is a better defensive play, while the S&P 500 is more of an aggressive, offensive play for risk-tolerant investors. I think management has done the best they can, but since they only focus on these consumer brands, they can only go so far in terms of value creation. My conclusion is that it’s a good defensive pick that will do a good job in preserving investors’ capital, but unlikely to grow it significantly.

Lugano In The Spotlight

CODI reported earnings on May 1, 2024, with the following results,

- Net sales up 8% to $524.3 million and up 4% on a pro forma basis.

- Branded Consumer net sales up 11% on a pro forma basis to $375.4 million.

- Industrial net sales down 10% to $159.6 million.

While their industrial businesses may be affected by the overall macroeconomic economy more, the branded consumer businesses continue to hold up the financial performance. Overall, the first quarter earnings revealed significant growth and momentum for many of their portfolio businesses, demonstrating the power of those consumer brands management talks about consistently.

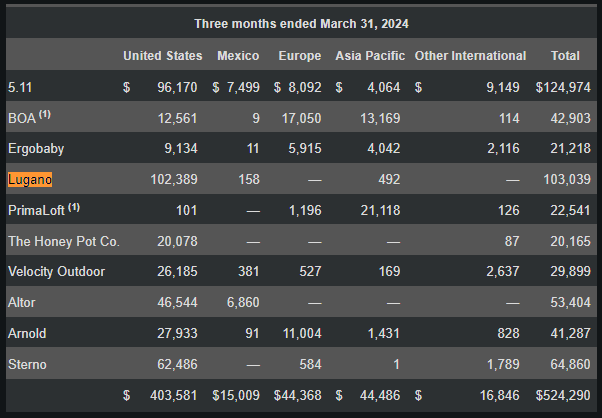

The big winner in the first quarter was the company Lugano, which had a 61% increase in net sales. Purchased for $256 million on September 2021, this high-end manufacturer and designer of jewelry has given shareholders significant value since its acquisition. I am awfully surprised that a jewelry company can have sales rise by so much, as most investors would assume tech names are the ones growing that rapidly.

After digging into the 10-Q, I found that Lugano still actually has room for growth internationally. The 10-Q reveals that sales went from $63 million in Q1 2023 to $102 million in Q1 2024, but most of it was in the United States. Investors can also see that revenues are beginning to show up for Lugano in Mexico and Asia Pacific, which signals to me that management is beginning to drive Lugano overseas and built a world recognized brand in jewelry.

10-Q

Therefore, I believe that companies such as Lugano and other names CODI has in their portfolio can still grow their sales internationally. Furthermore, I am very impressed that their consumer branded products have solid growth even during an inflationary environment, which leads me to believe their products have good pricing power and customer loyalty. Ultimately, it looks like the first quarter earnings reveal that their businesses are inflation-resistant, defensive growers, and have potential for growth overseas.

Leaning Into Healthcare

Recently, CODI acquired a significant stake in the Honey Pot Co. for $380 million. My take on this recent buy is that management seems to be leaning into the healthcare segment for additional traction and diversification in their business. Honey Pot is a leading feminine-care brand that specializes in making health products with plant-based ingredients.

It looks to me that management is looking to buy more businesses that are doing self-care, health, and wellness products, which to me makes the business more diversified and defensive. According to the 10-Q document, management explains,

We recently announced the launch of our healthcare effort as our third grouping of companies. We believe healthcare has multiple attractive, high-growth segments with strong industry tailwinds, is an acyclical vertical that we expect will bring diversification and stability to the current group of companies, and has strong alignment with the Company’s existing subsidiary priorities.

I like this focus and think it fits well to management’s strategy of non-cyclical, defensive, and branded businesses. In particular, I think home healthcare is appealing because brands can create trust and loyalty easily, people are willing to pay up to protect their health, and it is unlikely to be easily disrupted by AI or technological trends in my view. One report demonstrates the value opportunity for home healthcare,

The home health and home care industries are poised for significant growth in 2024. In fact, the home health care industry in the U.S. is expected to grow from $94 billion in 2022 to $153 billion by 2029.

Going forward, I expect management to lean in more into healthcare, which is seeing attractive tailwinds today. This Honey Pot Co. acquisition is the first of many likely coming acquisitions that are targeted towards protecting people’s well-being. With the surge in healthcare costs recently, people are looking for more affordable ways to treat themselves, and I think high-quality healthcare products that focus on prevention rather than the cure are likely to sell well in today’s economy. As a result, investors should expect more investments in this growing sector that syncs well with management’s defensive investment strategy.

Valuation – Fairly Valued At $20

I will be using management’s own guidance of adjusted earnings to do my valuation analysis. According to management’s outlook in the earnings press release,

In addition, the Company is raising its Adjusted Earnings guidance and now expects to earn between $148 million and $163 million ($145-$160 million previously) (see “Note Regarding Use of Non-GAAP Financial Measures” below) for the full year 2024.

Taking a midpoint of $150 million, I apply a fair earnings multiple of 10x, which is around the sector median to get a market cap of $1.5 billion. Divide by shares outstanding of 75 million gets me $20 fair value per share. Investors can see that the market agrees with my valuation currently, and has priced it around $20 per share.

Also, investors can see that the stock trades at 1.72x book value, which is around the 5Y average of 1.76x. Its dividend yield is pretty fair at 4.63%, which is in-line with the 1-year treasury rate of ~5%, currently. It looks to me that the stock is fairly priced, and will likely give investors satisfactory return with lower volatility.

I’m giving the stock a hold rating because although I like the defensive businesses CODI owns, it doesn’t seem like the stock can create more value compared to the S&P 500. Investors who are interested in buying a defensive portfolio of businesses that are low-volatility, steady earners may like CODI, but others who want more aggressive growth and technology exposure won’t find that in CODI. Whether the stock is a buy or not really depends on what the investor is looking for, and therefore I rate the shares as a hold to account for this personal factor.

Risks

Private equity largely depends on management competence and acquisitions driving value. If management suddenly fails to create value by focusing on price, cash flows, and competitive advantages stemming from brands, the company may lose value over time. Investors are making a bet on management capabilities because capital allocation will drive most of the shareholder value here.

Brands can lose favor over time. The whims and wishes of the consumer is the most difficult thing to predict, as fads and trends can put brands in and out of fashion. Given that most of these businesses are dependent on brands, it’s important that management picks the right brands to invest in or acquisitions may face impairment charges.

Competition is fierce for many of CODI’s businesses and could limit the growth potential of CODI. In the long term, I feel that technology oriented businesses that the S&P 500 owns may be faster growers compared to CODI, which is another reason I’m skeptical if CODI can outperform the index.

Hold Compass Diversified

Sometimes a stock can be a buy for one investor, and a hold for another. For a young, risk-tolerant investor with a long-time horizon, I think CODI makes no sense as an investment, as he or she is likely to do better in an index fund. But, for an older investor who is looking for safety, yield, and defensive names CODI may actually be a good choice to buy today. The bottom line, however, is that I do not think CODI can outperform the S&P 500 from here in terms of total return, which justifies a hold rating in my view.

Read the full article here