Introduction from John P. Calamos, Sr., Founder, Chairman and Global Chief Investment Officer

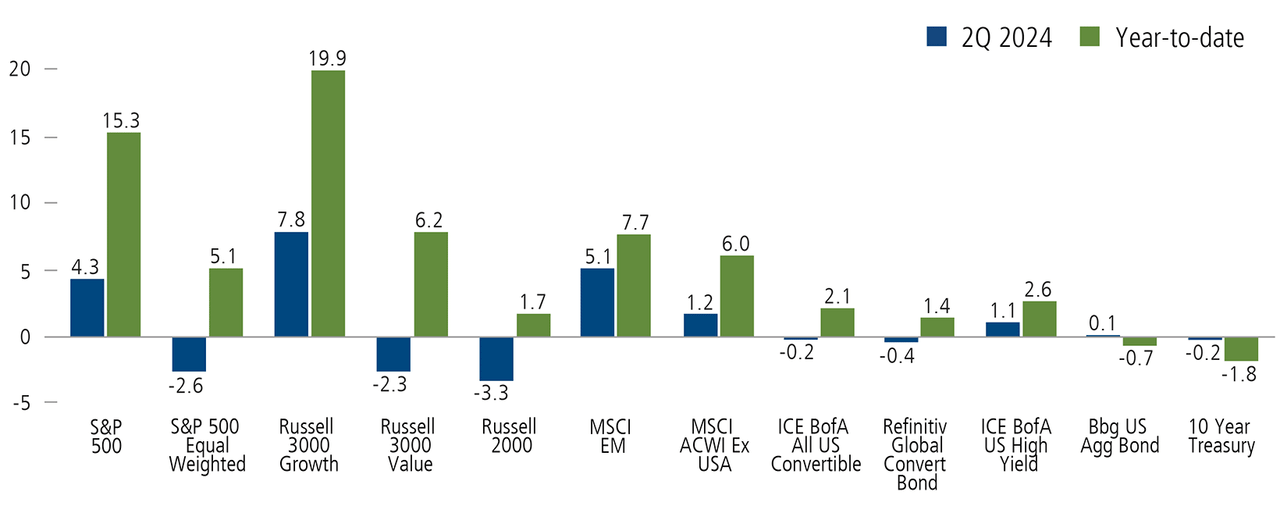

During the second quarter, investors focused on data that pointed to normalizing inflation and softening economic growth. This growth and inflation backdrop stoked anticipation of Federal Reserve interest rate cuts that may finally arrive this fall. Market performance was still relatively concentrated, as illustrated by the significant disparity between the market-cap-weighted S&P 500 Index and its equal-weighted counterpart. There were also notable return disparities by investment style and market cap. Within the US equity market, large-cap growth stocks posted especially strong gains, while large-cap value stocks once again lagged.

Globally, emerging markets advanced briskly after a more tepid performance in the first quarter. The convertible market, which includes many small and mid-cap companies, posted flat performance as investors gravitated to larger companies. Within the fixed income market, high yield bonds led the way as credit spreads remain historically tight.

Growth Equities Led the Way in 2Q 2024

Global asset class returns (%)

Past performance is no guarantee of future results. Source: Morningstar. Data as of June 30, 2024.

On the whole, the US economy looks to be in good shape, although we’ve seen a more mixed picture emerge. Certainly, falling inflation and continued strength in manufacturing and employment are key positives, but evidence is mounting that US consumers—the engine of the US economy—are cutting back as they draw down savings from Covid-era stimulus. Business confidence readings give cause for concern, but are not unexpected given the high level of fiscal policy uncertainty on the horizon.

As we look to the second half of the year, we are prepared for continued choppiness as the presidential election approaches. Outcomes could lead to vastly different fiscal policy trajectories, with far-reaching implications for all areas of the economy. We’re also mindful that the Federal Reserve is not locked into anything, as much as the market wishes it were. This last round of corporate earnings announcements provided plenty of good news and analysts expect a continued acceleration of earnings from here, but this may be hard to achieve if the trajectory of economic growth continues to moderate. We’re also attentive to the considerable divergence of growth across different areas of the economy and world.

However, we are confident in our ability to navigate the crosscurrents. We are encouraged to see markets that are less driven by macro factors and more attentive to the fundamentals of individual companies, including growth characteristics. Fundamentally driven markets set up well for our teams. Across asset classes, our teams have extensive experience analyzing bottom-up company characteristics, thematic trends, and security valuations, while always remaining attentive to understanding and managing risks on many levels. In the links that follow, they share their perspectives on where they are seeing opportunities across global asset classes.

Navigating the Obscurity of a More Normal World

By Michael Grant – Calamos Phineus Long/Short Fund (CPLIX)

Analyzing the economic cycle is a major part of assessing the outlook for financial markets. To correctly assess the economic cycle, investors need to consider the policy impacts of both central banks and fiscal authorities. Even then, the discipline of macroeconomics offers few precise answers. We suspect this imprecision will be felt more acutely in the coming quarters because the unusual features of the pandemic era are fading into the horizon.

For the past two years, we have pushed against the widely accepted discourse that recession was the “inevitable” consequence of higher Fed policy rates. Instead, we anticipated a resilient US economy benefiting from so much that was different. This started with the benefits of inflation for private sector incomes and balance sheets as well as the historic support of fiscal programs under both Trump and Biden.

Most have come around to our view that US recession risk in 2024 is negligible. Across equity and corporate bond markets, there is little anticipation of imminent stress. Investors have concluded they stand amidst an economic expansion of indeterminant length—a reasonable conclusion in the presence of friendly central banks. And yet, it is one underpinned by more obscurity and less coherence of economic and policy narrative.

Many of the drivers of this expansion appear to be waning. Employment markets are fully recovered, with consumer incomes more dependent upon wage inflation than job growth. Corporate profit margins are peaking but stable. Earnings can advance 5% or so in a not so terrible world of 5% advances in nominal GDP. Benignly, the landscape is moving beyond the unusual contours of the post-pandemic years, leaving a new debate about what is “normal.”

Investor confidence in today’s economy is supported by the favorable liquidity impulse of rising equity prices. The S&P 500 Index return through the first half of 2024 is one of the best for an election year, yet the performance of the average equity tells a different story.1 Here, we see an equity cycle that climaxed in March and has been consolidating as investors grapple with what this post-pandemic normal really looks like.

Debates Rage On: Inflation, Politics and Gen AI

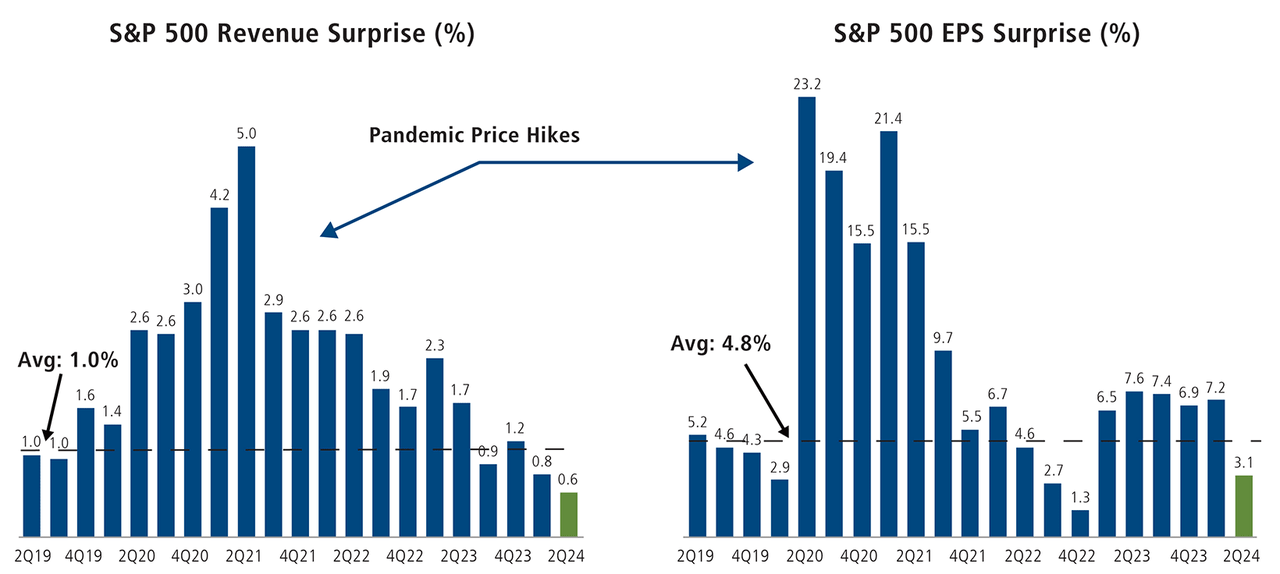

The path of US inflation in coming quarters feels unusually obscure. If disinflation is the new norm, nominal measures of economic activity will decelerate further into 2025. Little gas is left in the tank for the corporate sector, where aggressive price hikes through Covid pulled forward much of this cycle’s profitability. The concentrated focus on fewer and fewer outperformers in the S&P 500 Index makes sense in this context.

The Normalization of Nominal GDP = Muted Corporate Upside

Past performance is no guarantee of future results. Source: UBS

At the same time, service inflation is sticky2 because labor is tighter than before the pandemic and growth is now skewed toward services. Adverse base measurement effects will emerge from the June CPI onwards. This implies core inflation could trend higher at the same time that many are heavily exposed to duration. Whether “complacency” or “obscurity” is the better description of where things stand, inflation risks appear skewed to the upside.

Encouraged by the Fed’s carrot of imminent policy relief, investors have assumed that current policy rates are temporary. By taking advantage of the resulting inversion of yield curves, corporate borrowers are enjoying the growing divide between a restrictive policy rate and easy financial conditions. All of this supports a higher-for-longer policy narrative, ironically underpinned by the Fed’s conviction that gravitational forces will pull inflation back to 2%.

Investors entered 2024 convinced the Fed was ahead of the policy curve, with an asymmetric reaction function embedded in their guidance. We see no policy easing until after the election and one wonders if central bankers could again slip behind the curve. The key surveillance metric is the US 10-year Treasury yield. Any move approaching 5% will signal that the contours of consensus assumptions are shifting, possibly in a profound manner.

US Elections: About to Get Interesting

Upcoming US elections are the obvious event risk of H2, with significant consequences for the macro setting into 2025 and beyond. These elections are set to shape trade, immigration, industrial and competition policies, and fiscal constraints. While Biden and Trump may be similar in age and golf handicap, their rematch points to different directions on material policy fronts.

So far, financial markets have appeared nonplussed. This might reflect voter familiarity with the candidates; or it may simply be early for investors to focus on the opportunities and risks. Stable and rising markets may be judging Trump (with his lead in the polls) as the more friendly outcome; he is an effective cheerleader for the grassroots economy and especially small businesses.

That said, businesses have played a key role in the current expansion through hiring and fixed investment. Trump’s plans for a resumption of trade conflict may impact sentiment in the election run-up. In this respect, the latest dip in the June global PMI future output reading bears monitoring. The 2018–2019 trade war had large adverse effects on global business confidence and capital spending.

The elephant in the room is the shape of fiscal policy. The election winners will immediately be confronted with the expiration of the most important provisions of the 2017 tax cut. Today’s scale of fiscal deficit points to tensions between economic growth and taxes, and the monetary accommodation to smooth this over. Bond vigilantes have been few and far between, but the situation is ripe for a profound shift in market willingness to backstop Treasuries demand.

State of the AI Transition

Amidst all of this, financial markets have become enthralled by the AI narrative and its widely touted promise to transform “everything”. The major technology leaders have responded with a ~$1 trillion spending plan on AI-related capex. Remarkably, it is unclear if there will be much to show for this spending as practical applications have yet to emerge. Investors and corporate spendthrifts alike have embraced the old adage, “If you build it, they will come.”

History argues that today’s AI spending boom is unlikely to avoid the misallocation of capital that typically accompanies celebrated investment narratives. The sheer scale of spending implies the eventual returns will need to be outsized. One early challenge is that the three main channels of payout —advertising, e-commerce and subscription fees—will require a material shift of consumer habits that is not yet apparent.

This monetization debate is ongoing. What is less debatable is that this is exceptionally expensive compared with prior technology shifts like the internet and personal computers. To justify today’s costs, AI technology must soon solve complex and trillion-dollar problems. In contrast, prior technology cycles emerged in the wake of low-cost solutions with better understood roadmaps for future business models or paths to cost savings.

Crossing this chasm will occur only gradually. One hurdle is the intensive capital and power requirements of AI datacenters. Energy constraints will be the biggest bottleneck as big tech faces the same regulatory, interconnection and supply chain constraints as utility companies. The total capacity of power projects waiting to connect to the grid grew ~30% in 2023, with wait times between 40 and 70 months.

Bubbles Take Time

Investment bubbles can take a very long time to burst. Most burst because the cost of capital changes or final demand deteriorates, thus affecting the deployment of capital. In contrast, the companies leading today’s charge are the largest, most cash-flush entities in the world. It is hard to imagine what will cool their enthusiasm. Sustained corporate profitability could allow sustained experimentation with negative ROI projects for some time.

And it is not clear that AI-related stocks should be judged “bubbly.” One clear signal of a stock bubble is rising share price volatility as valuations become disconnected from fundamentals, leaving sentiment and momentum to dominate. In contrast, the shares of AI leaders have largely kept pace with rising fundamentals—prices appear high rather than extreme. Volatility measures across US technology have been flat to down—not up as in a typical bubble.

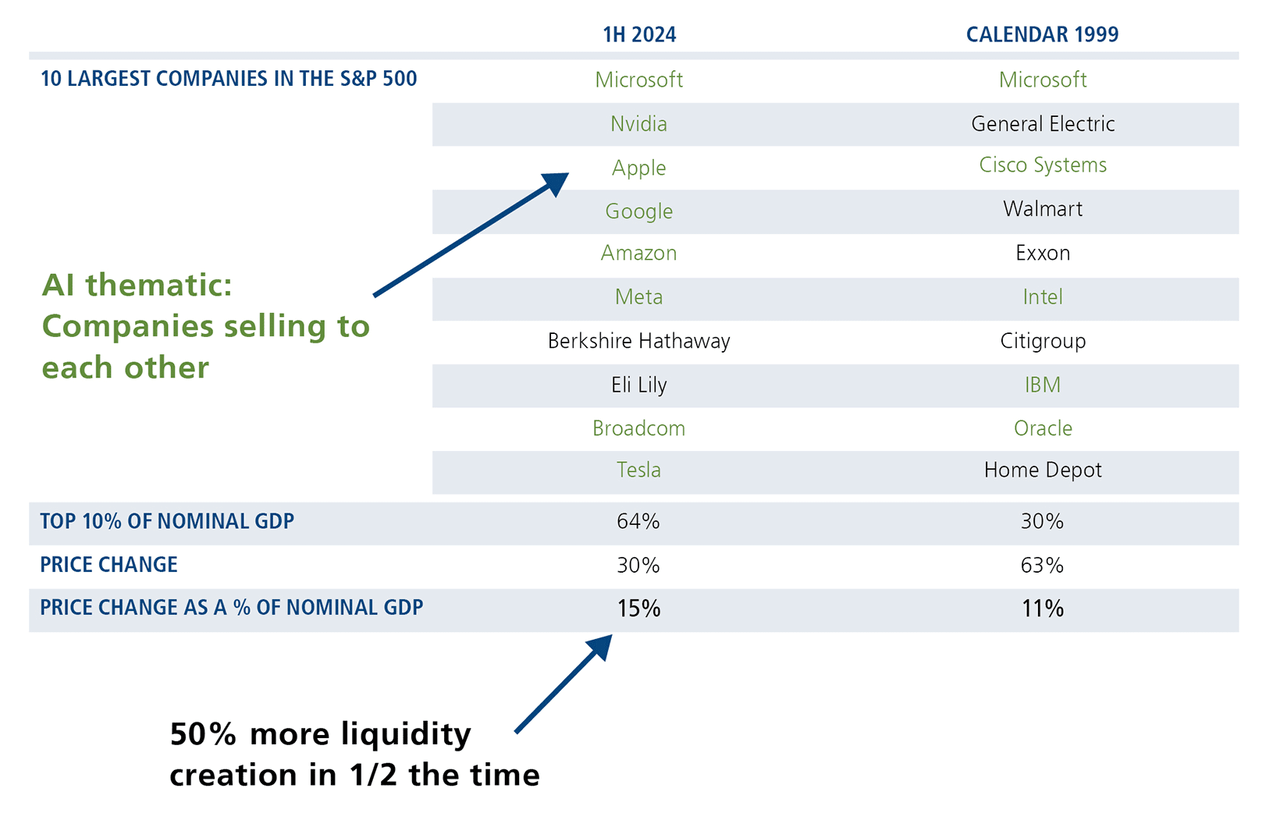

The key feature of today’s AI narrative is the sheer scale of their market capitalizations relative to nominal GDP,3 which stands in contrast to historical experience. For example, the gains in market capitalization through the first half of 2024 exceed the aggregate gain of 1998 and 1999 combined relative to nominal GDP at that time. If an AI bubble does emerge in the coming year, the scale of liquidity creation could be unmanageable.

The Tail Is Now Wagging the Dog

Past performance is no guarantee of future results. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be and should not be interpreted as recommendations.

Any investor who lived through the internet bubble of the late 1990s will be inclined to draw comparisons. Do we stand at the peak like March of 2000? Or is March of 1999 the better roadmap when another year of enthusiasm lay ahead. One difference between then and today is the more robust health of the US corporate sector, leading us to wonder if the AI narrative fades with a whimper rather than a bang.

Investment Conclusion: CPLIX

The major contributors to benchmark performance in 2024 have been the AI winners, including Nvidia, Taiwan Semiconductor and the hyperscalers Google, Microsoft, and Amazon. From this point, we view the AI investment theme as more skewed to the downside. We have reduced fund exposures to the “picks and shovels” narrative, and semiconductors in particular.

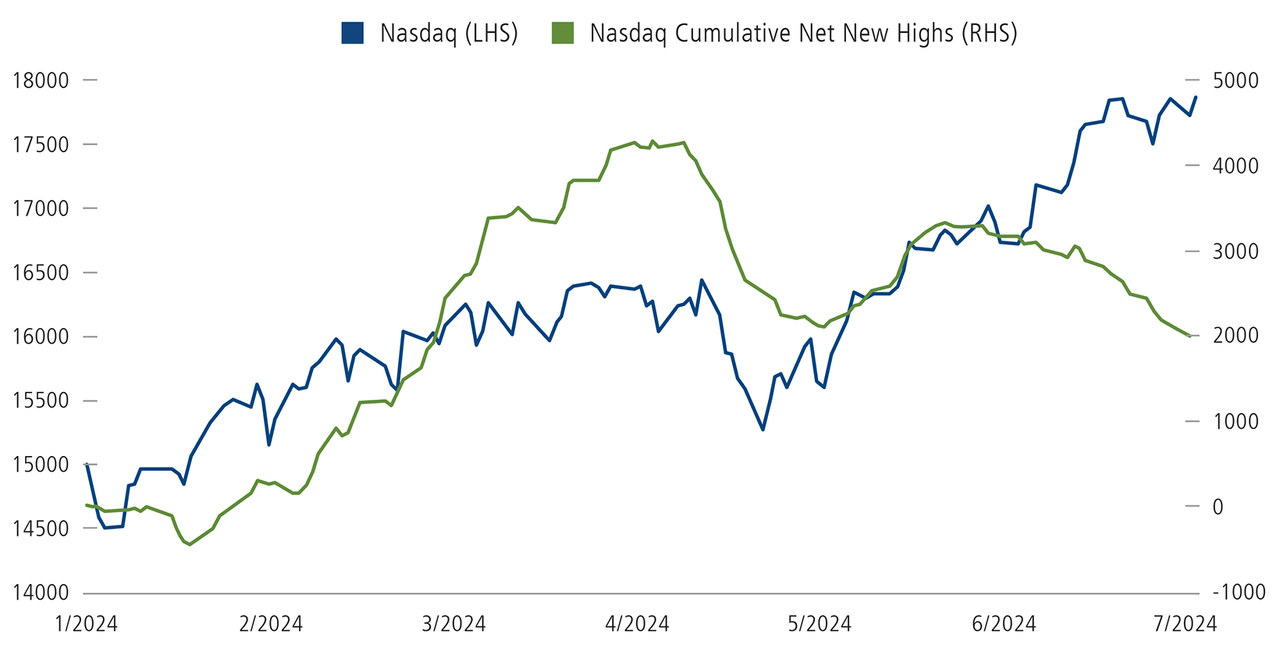

The performance divide between the S&P 500 led by the concentration of mega-cap returns and the broader equity universe points to a narrowing long opportunity. Breadth measures of advances versus declines, or new highs versus new lows have been more negative than positive across the technology universe. It is easier to short a Nasdaq stock than to short the Nasdaq Index. We believe this is an ideal environment for our long/short approach.

Narrow Market Breadth:It is easier to find Nasdaq shorts than it is to short the Nasdaq

Past performance is no guarantee of future results. Source: Bloomberg. The Nasdaq Composite Index is a market capitalization weighted index of more than 2500 stocks listed on the Nasdaq, with an emphasis on technology stocks.

Our interpretation of the average stock action is that equities climaxed in late spring. Markets are now stuck in consolidation until some fundamental light can pierce the clouds of obscurity. For this reason, CPLIX equity exposures are low relative to history and positioning is focused on the alpha opportunity (rather than market beta) to generate returns into autumn.

Our key message is that it is hard to have high conviction across many of today’s debates. The odds still favor an expansion that lives on and an inflation setting that is sticky. The problem is the lack of humbleness across key parts of the equity universe—a complacency encouraged in part by central bankers.

1The equal-weighted S&P 500 has underperformed the market-cap weighted S&P500 by more than 10% in 2024. In Q2, the S&P500 Index rose 3.9% in price terms, contrasting with the 3.1% decline in its equal-weighted equivalent. The S&P 500 Index is considered generally representative of the US large cap stock market. Indexes are unmanaged, do not include fees or expenses and are not available for direct investment.

2The Atlanta Fed’s measure of Sticky CPI is still running above 4% year-over-year. The Consumer Price Index (CPI) is a measure of inflation.

3Nominal Gross Domestic Product (GDP) represents the total value of all goods and services produced in an economy during a specific time period, measured at current market prices.

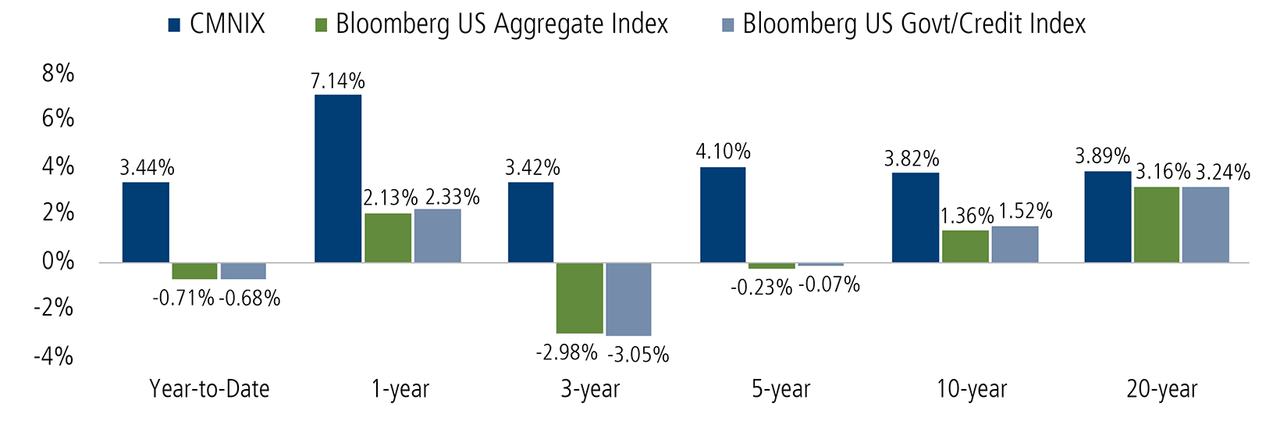

Breaking Through as Bonds Fight to Break Even

By Eli Pars, CFA, – Calamos Market Neutral Income Fund (CMNIX)

Traditional bonds struggled to earn their coupons in the second quarter and are essentially flat year to date. The continued deferral of future interest rate cuts hasn’t helped the case for bonds.

We believe the fund’s recent and long-term performance also demonstrates the merits of our approach as an alternative to cash. In our last commentary, we noted that the fund’s one-year return of more than 7% has still easily surpassed a fed funds rate of more than 5%, a backdrop currently in place—though perhaps for not much longer if markets are right about the Fed’s timeline for cuts.

CMNIX Has Demonstrated Strength over Bonds through Interest Rate and Market Cycles

Data as of June 30, 2024

Source: Morningstar. Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. All performance shown assumes reinvestment of dividends and capital gains distributions. The fund’s gross expense ratio as of the prospectus dated 3/1/2024 is 0.97% for Class I shares.

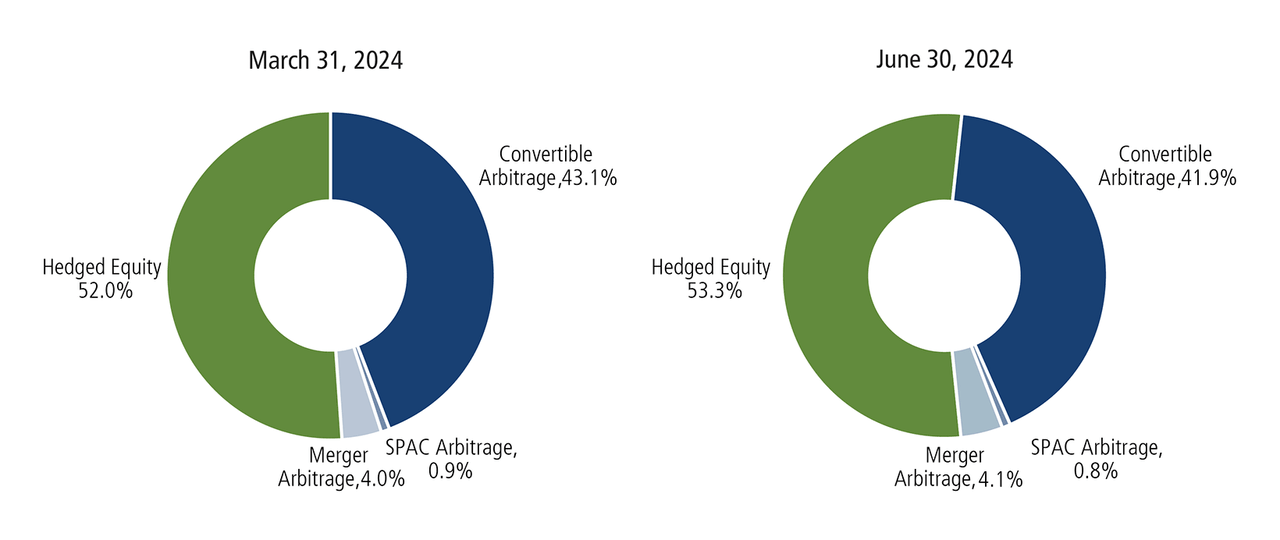

We continue to like the trades we have on in convertible arbitrage and hedged equity, and we have maintained a roughly balanced allocation between the arbitrage and hedged equity sleeves.

CMNIX Allocation

Arbitrage Strategies

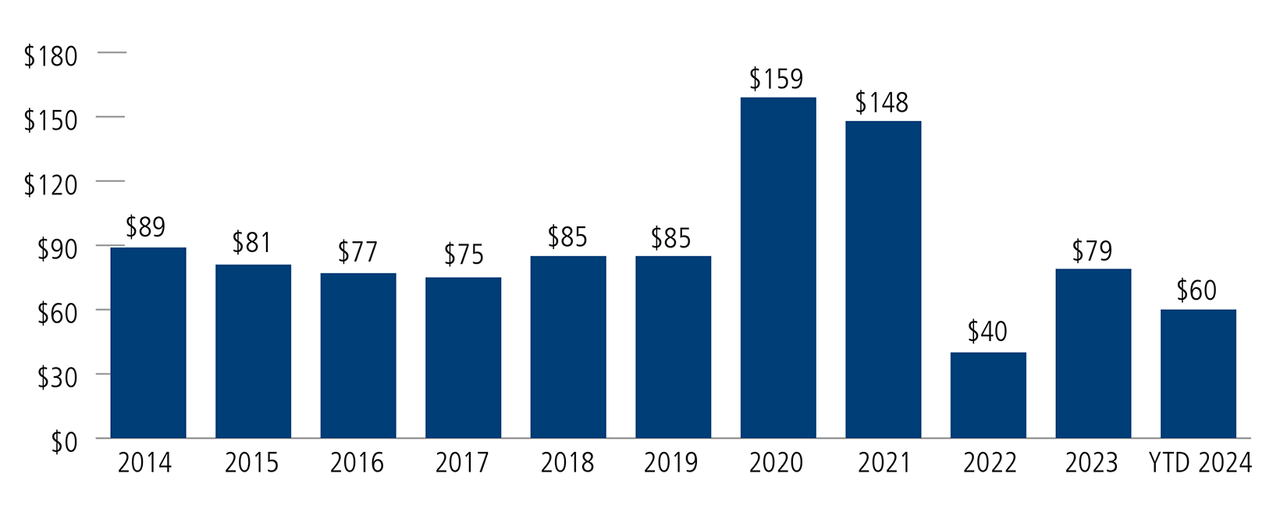

Our arbitrage strategies generally continued to perform well, anchored by our convertible arbitrage book. We continue to like the opportunity set in convertible arbitrage and are excited about the prospects offered by a growing new issue calendar. The second quarter saw more than $34 billion in global issuance, taking the first half total to $60.2 billion.

Over the past year, we have written extensively about the maturity walls in investment grade and high yield debt providing fuel to the convertible new issue market as companies seek to refinance debt at the lower borrowing costs associated with issuing convertibles instead of nonconvertible debt. We are seeing this play out, albeit at a modest pace. Part of our thesis has been that we would see an uptick in investment-grade convertible issuance as well, given a higher interest rate backdrop. This is also happening, with investment grade issuers accounting for almost one-third of the second quarter’s issuance. This included a $5 billion new issue for an A-rated Chinese online retailer, one of the largest convertible bond issues we have ever seen.

Global Convertible Issuance Provides a Favorable Backdrop for Convertible Arbitrage

Global convertible issuance, $ billions

Source: BofA Global Research. Data as of June 30, 2024.

Hedged Equity

The opportunity set in the options market has allowed the fund’s hedged equity strategy to maintain its defensive posture while still earning a decent return. This favorable capture has been driven by the positive standstill yield our hedge generates in a world of higher interest rates. More specifically, the recent rise in the fed funds rate flows through to the option market in higher call and lower put prices. (For more on this, see our video blog “Higher Rates are an Opportunity for Hedged Equity Strategies,” where Dave O’Donohue walks through how higher rates impact option pricing.) We anticipate keeping this hedge profile as long as we find it the most attractive trade in the option market.

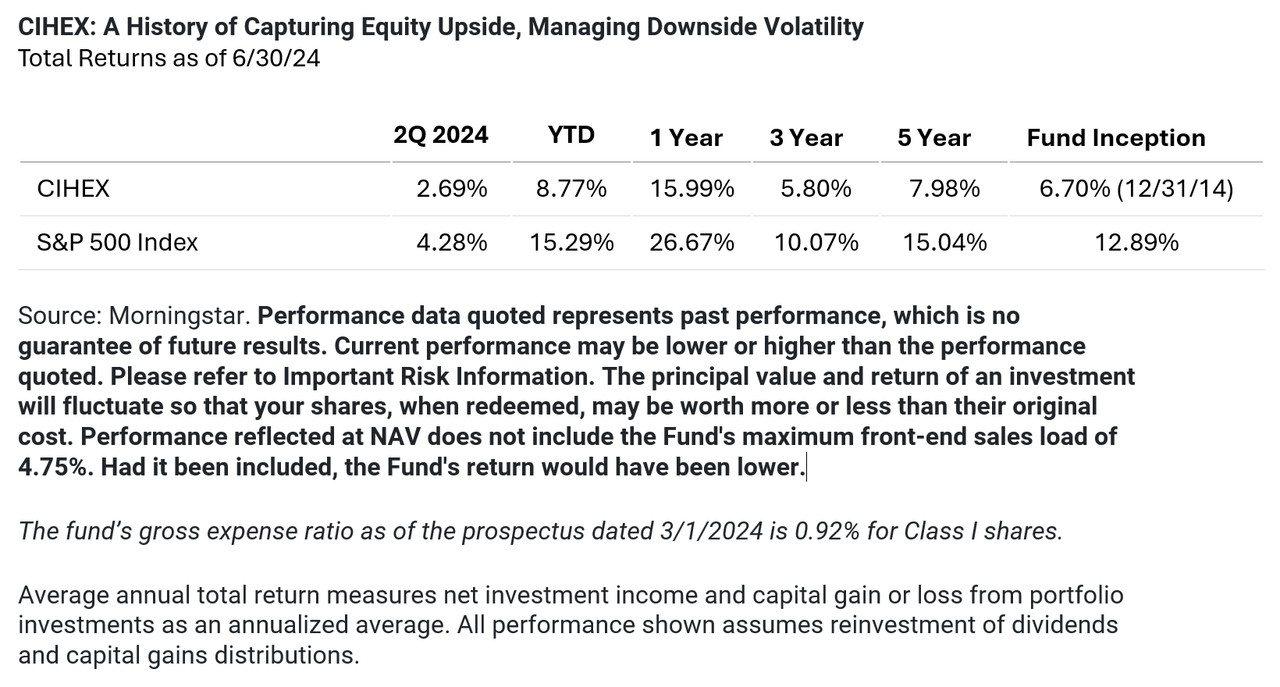

The More Things Change…

By Eli Pars, CFA – Calamos Hedged Equity Fund (CIHEX)

As an equity alternative, Calamos Hedged Equity Fund employs an active options-based strategy to seek upside participation in the equity market while limiting downside exposure. Given the uncertainties in the market and the potential for the unexpected, we are dedicated to being favorably positioned for as many market outcomes as possible.

We believe this flexible approach is a key differentiator and one of the most important ways we add value over time for the fund’s shareholders. That said, while there are times when we are really active in terms of adjusting our hedge, there are other times when we establish a trade that we really like and the dynamics in the market give us every reason to keep that trade going.

That’s where we are today. As we head into the second half of 2024, our outlook on the current 65/35 trade is that “if it’s not broken, why fix it?” To recap, last year, market conditions provided us with the opportunity to establish an especially attractive option trade structured to pursue 65% of the market’s upside with just 35% of the market’s downside at its expiration in December 2024. (For more on this trade, see our post, “Focused on Capitalizing on—Not Capping—Equity Upside” and “CIHEX Set to Capitalize on What We’re Calling a “Cicada Trade.”)

For the most part, we’ve kept the trade fairly steady, although not completely static. As markets move, the 65/35 trade may be less advantageous for new money entering the fund. Consequently, we did tweak the hedge a couple of times this year as the equity market continued to rally.

While the 65/35 trade has served us well, we are always looking to the future and the many different scenarios that may evolve. We are confident that our active and flexible approach, combined with our decades of experience, will position us well to take advantage of whatever the market brings.

US Convertible Securities: Harnessing the Tailwinds of Normalizing Economic Data and Issuance

By Jon Vacko, CFA, and Joe Wysocki, CFA – Eli Pars, CFA

Equity markets extended year-to-date gains during the second quarter of 2024 and finished the first half of the year with a strong advance. The S&P 500 Index continues to reach new all-time highs, helped by a backdrop of stable economic growth, a lack of a sustained resurgence of inflationary pressures, and monetary policy indicating the Fed’s desire to reduce interest rates for the first time this cycle.

Although we would not be surprised to see variability in economic data in the coming months, we remain optimistic that the overall economic growth, inflation, and monetary policy trends will continue normalizing along their current trajectories. This normalization can provide a further tailwind for risk assets, including the potential for a broadening of equity market leadership. However, as we enter the back half of the year, we are keeping a close eye on the potential for increased volatility around a contentious US presidential election that will likely have fiscal policy implications for years to come.

Within Calamos Convertible Fund (CICVX), our overall focus remains on bottom-up company selection and actively managing security-specific risk/reward tradeoffs. Broadening of equity market leadership could be particularly beneficial for small-cap and mid-cap growth companies, which are well-represented in the convertible universe. We maintain our preference for balanced convertible structures that provide favorable asymmetric payoff profiles by offering potentially attractive levels of upside equity participation with less exposure to downside moves.

Technology, consumer discretionary, and health care are CICVX’s largest sector allocations. As we have discussed, we favor companies that are executing well despite macro uncertainties, with improving margins and free cash flow, accelerating returns on invested capital, and attractive equity valuations. We also focus on identifying innovative companies positioned to benefit from cyclical and secular themes that can serve as tailwinds to individual corporate performance. These include companies advantageously positioned as businesses seek solutions to higher labor, manufacturing, and interest costs in the current economic environment. We also are investing in companies exposed to artificial intelligence, productivity enhancements, and cybersecurity trends. We expect the convertible market will provide opportunities to participate in these fast-growing trends for years to come.

The convertible new-issue market was strong in the first half of the year, with global issuance up approximately 50% relative to the same period in 2023. We continue to see deal terms that carry higher coupons and lower conversion premiums compared to last year’s issuance, as well as a higher percentage of investment-grade credits. A significant amount of this year’s issuance has been brought to market to refinance existing debt, a trend that we believe can benefit a broad subset of issuers.

We remain optimistic about issuance prospects going forward as companies increasingly recognize the lower borrowing cost benefits of convertibles in lieu of traditional bonds in an environment of higher interest rates. We believe the combination of a sizable amount of debt maturing in 2025 and 2026 across bond markets, the possibility of a higher-for-longer interest rate scenario, and the fact that convertibles have served as growth capital for leading small and mid-cap companies throughout the full business cycle should serve as accelerants for continued solid issuance.

Ready for Choppier Waters

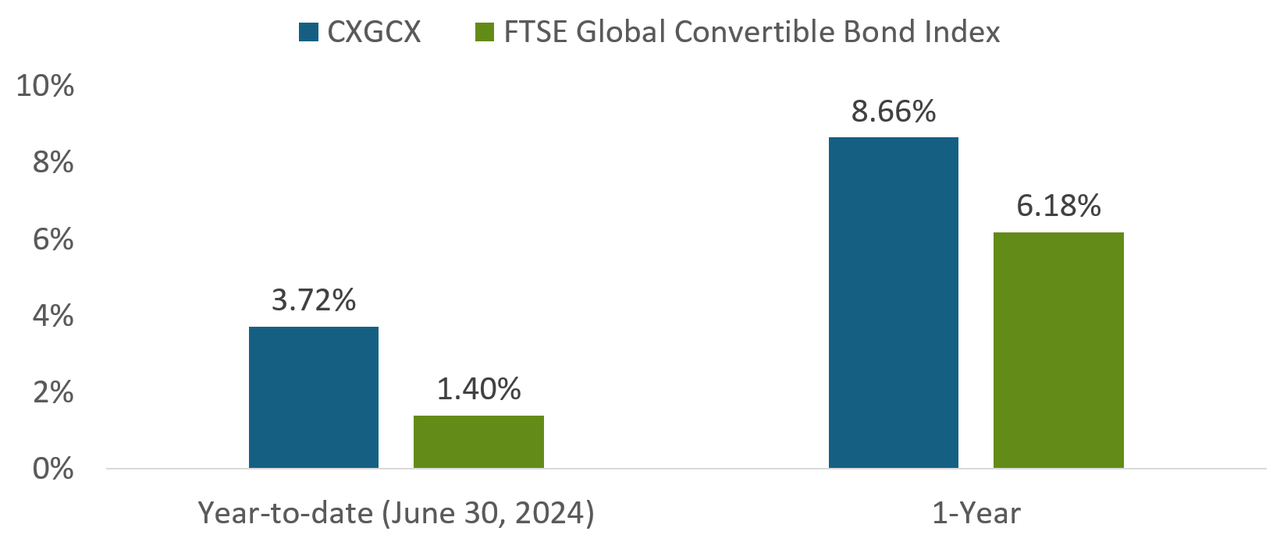

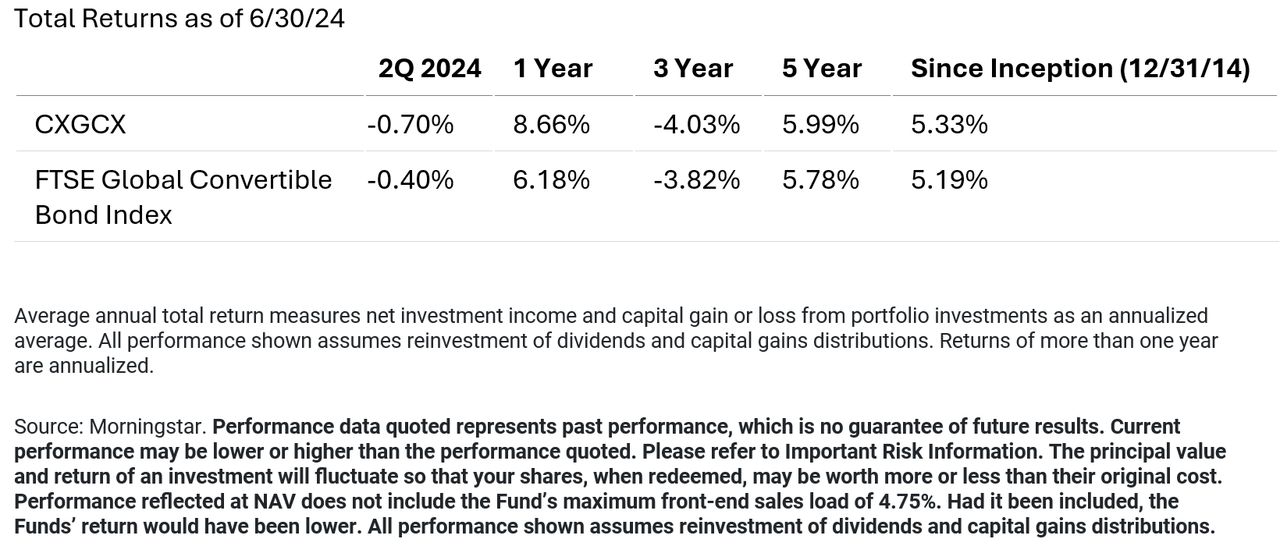

By Eli Pars, CFA – Calamos Global Convertible Fund (CXGCX)

Although it was a slow quarter for the global convertible market and the fund, Calamos Global Convertible Fund generated solid return of 3.72% through the first half of the year, well ahead of the FTSE Global Convertible Bond Index 1.40% return. This continued a streak of outperformance since the start of 2023.

Calamos Global Convertible Fund versus the Global Convertible Market

Source: Morningstar. Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load of 2.25%. Had it been included, the Fund’s return would have been lower. All performance shown assumes reinvestment of dividends and capital gains distributions. As of the prospectus dated 3/1/2024, CXGCX’s gross expense ratio is 1.09%.

We believe that our experience and depth of knowledge have been key to the fund’s performance over time. We’re using Calamos’ time-tested approach and capital structure research to identify compelling bottom-up growth opportunities benefiting from long-term secular trends. This has led us to a wide array of growth opportunities, including convertibles issued by companies participating in niches within the global AI ecosystem as well as those at the forefront of country-specific trends. For example, we have a core holding in a convertible issued by a leader in India’s tourism industry, which is well-positioned to capitalize on favorable demographics.

The global convertible market has always been characterized by a high degree of innovation, with structures evolving to serve the needs of investors and issuers alike. While it is a truly global market, there are differences from country to country. Our depth of experience helps us navigate and capitalize on these nuances—some might call them quirks—of the global convertible market. For example, over the past quarter, we redeployed assets from two companies that had served the fund well. One, a Japanese semiconductor equipment manufacturer, was approaching its first call date. Japanese issuers generally don’t call convertible bonds issued in Japan and are more likely to call bonds issued in the offshore or euro market, as in this instance. With the call approaching, and the bulk of the issue getting converted by other holders, we sold the position.

We also sold the fund’s position in an Indian mobile phone operator, an issuer offering the high-quality fundamentals and exposure to secular growth tailwinds that we like. Although the issue was not callable in the manner that US investors are familiar with, it was subject to a “clean-up call” popular in Europe and Asia ex-Japan. This clause allows an issuer to call a bond if less than 15% of the issues remain outstanding. Over time, the performance of the underlying equity and the convertible structure resulted in the issue being slowly converted away by investors seeking to lock in gains. We decided to have control over our exit timing and sold at what we saw to be a good price.

Our Outlook

We believe that the global convertible market will continue to provide an attractive way to access the growth potential of innovative companies. As we discussed in our previous commentary, the resilience of the US economy has been somewhat surprising to us, and there’s likely more downside risk than many investors realize. Normalizing inflation and economic data give the Fed more air cover to begin rate cuts, which should provide tailwinds for risk assets. However, economic data is softening, there’s geopolitical risk around the world, and no one has a crystal ball when it comes to the Fed. In terms of the presidential election, the biggest surprise would be no surprises. All in all, there’s every reason to favor lower-volatility approaches.

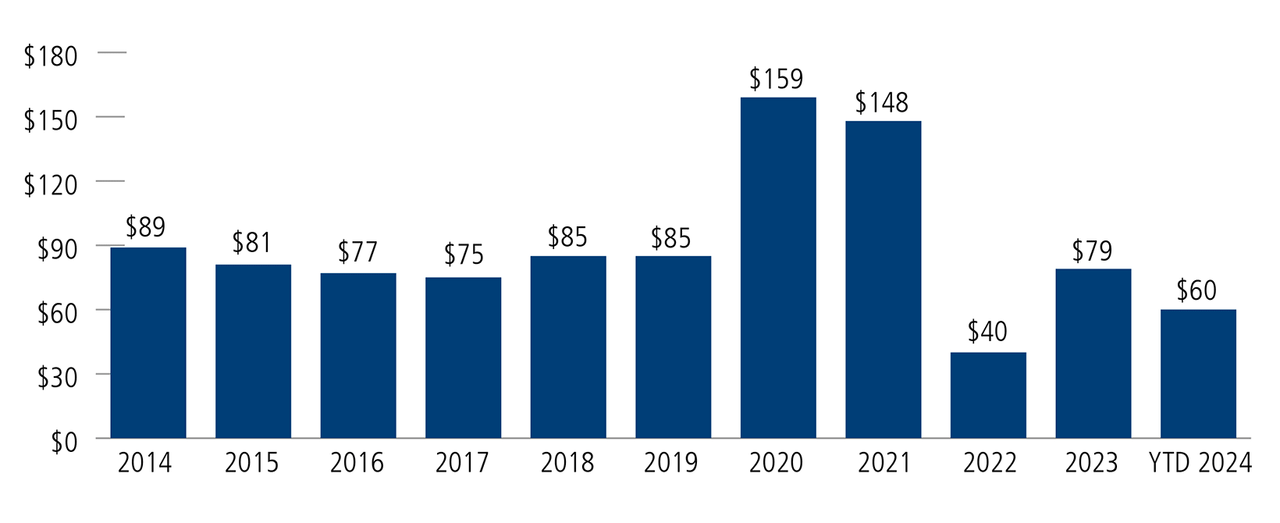

New Issuance Provides a Breadth of Choices

Moreover, we continue to be excited about the prospects offered by a growing new issue calendar. The second quarter saw more than $34 billion in global issuance, bringing the year’s first-half total to $60.2 billion.

Global Convertible Issuance Gives Us a Breadth of Choice

Global convertible issuance, $ billions

Source: BofA Global Research. Data as of June 30, 2024.

Over the past year, we have written extensively about the maturity walls in investment-grade and high-yield debt providing fuel to the convertible new issue market as companies seek to refinance debt at the lower borrowing costs associated with issuing convertibles instead of nonconvertible debt. We are seeing this play out, albeit at a modest pace. Part of our thesis has been that we would see an uptick in investment-grade convertible issuance as well, given a higher interest rate backdrop. This is also happening, with investment-grade issuers accounting for almost one-third of the second quarter’s issuance. This included a $5 billion new issue for an A-rated Chinese online retailer, one of the largest convertible bond issues we have ever seen.

Positioning Highlights

Calamos Global Convertible Fund continues to emphasize balanced convertibles that offer attractive levels of upside equity market participation and downside risk mitigation. We’ve remained active in the new issuance market and also locked in gains from well-performing names.

The consumer discretionary, information technology and health care sectors are among the fund’s largest allocations as of the end of the quarter. From a regional standpoint, the fund’s largest allocations are to the United States and Emerging Asia. We are underweight to the former and overweight to the latter. The fund also maintains its long-standing underweight to European convertibles, which reflects our concerns about geopolitics (most notably the war in Ukraine), inflation, and overall economic conditions.

Growth Dispersion Highlights the Benefits of Selectivity

By John Hillenbrand, CPA – Calamos Growth and Income Fund (CGIIX)

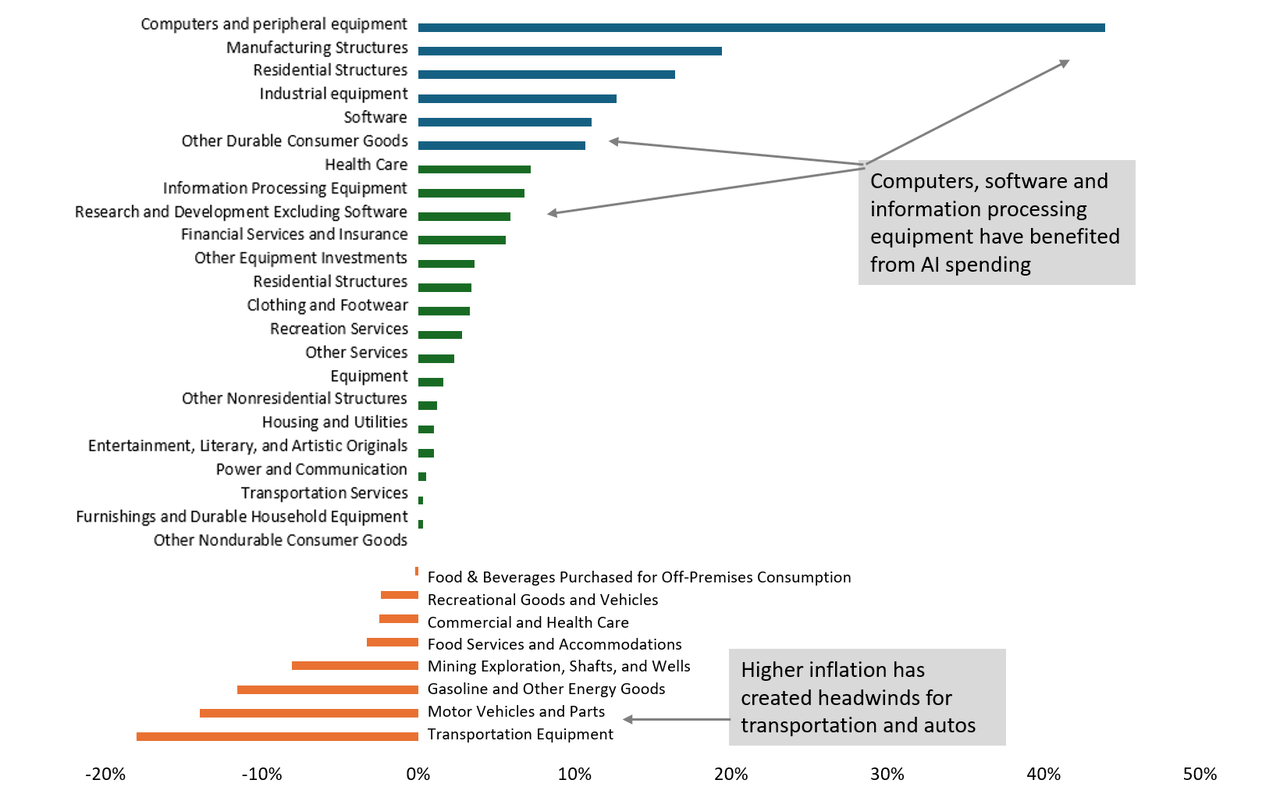

The economy continues its normalization process as the extraordinary measures put in place in response to the pandemic unwind. Real GDP and employment growth have, in aggregate, slowed to more normal levels, although growth dispersion continues across GDP components, as shown below.

There’s Significant Dispersion Among Real GDP Growth Categories

1Q 2024 YOY

Source: Bloomberg

The impact of corporate spending around AI can be seen in the above-average growth rate in computers, software, and information process equipment, while higher interest rates have negatively impacted demand for transportation and motor vehicles during the first quarter. Inflation continues to slow but not yet to a normalized level, again exhibiting dispersion across consumption categories.

We believe many of these trends should persist through the rest of the year. In the current environment, we see above-average corporate spending in select IT categories, continued infrastructure spending, healthcare innovation, sustained spending from higher-end consumers because of the wealth effect, and improved discretionary spending at the middle- and lower-income levels because of growth in real wages. However, upcoming tighter US fiscal budgets, continued higher interest rates, and the impact of ongoing global conflicts may counterbalance these growth drivers.

The second half of 2024 should provide insights into future monetary and fiscal policies. The developments in growth and inflation should provide greater clarity on future monetary policy, while the US elections should provide insights to fiscal policy. The path of fiscal policies appears murky currently, as the make-up of the Congress appears too close to call. Tax policy, spending priorities, regulation, and immigration are key areas in which we could see change. We remain alert to significant developments that would tip the scale. In the interim, we believe our focus on larger cap, high-competitive-moat companies in stable demand areas should provide some stability to the portfolio.

Given our expectation of positive economic growth over the next year, we are assessing the investment opportunities with a continued focus on real growth and return improvement areas. In addition to areas with favorable cyclical factors, we believe companies that can improve profitability in a slower-growth environment are favorable investments. Many companies are focused on improving their returns on capital through improved efficiencies, normalized supply chains, and revised investment strategies based on the current interest-rate environment. The pace of corporate cost-cutting and restructuring has increased over the past several quarters across several areas, providing more opportunities to identify companies with improving returns on capital. Over the short- and intermediate-term, improved real returns on capital should drive higher equity prices.

Calamos Growth and Income Fund pursues lower-volatility equity participation through a multi-asset-class approach. We believe the best positioning for this environment is a focus on specific areas with real growth tailwinds, on companies with improving returns on capital in 2024, and on equities and fixed income with valuations at favorable expected risk-adjusted returns. We see compelling prospects for companies with exposure to new products and geographic growth opportunities (examples can be found in health care and AI-related infrastructure and software), and specific infrastructure spending areas (in materials, industrial, and utility sectors).

We are selectively using options and convertible bonds to gain exposure to some higher-risk industries in this low-volatility environment. From an asset-class perspective, cash and short-term Treasuries remain useful tools to lower volatility in multi-asset-class portfolio, given their yields.

Positioned for Market Upside, but with a Measure of Prudence

By Matt Freund, CFA, and Michael Kassab, CFA – Calamos Growth Fund (CGRIX)

Despite persistent forecasts of an economic slowdown and numerous indicators signaling weakness—notably, the Leading Economic Indicators’ consistent decline since December 2021—the economy demonstrates unexpected vigor.

We believe the economic resilience of these past several quarters can be attributed, in part, to the lingering effects of Covid-related stimulus measures and robust fiscal spending, which effectively counterbalanced the impact of elevated short-term interest rates. At the same time, a growing wealth effect and rising incomes have mitigated the adverse impacts of persistently high inflation and sustained consumer spending. However, there are recent signs of emerging weakness, particularly among lower-income consumers.

Equity Market Dynamics: The AI Revolution

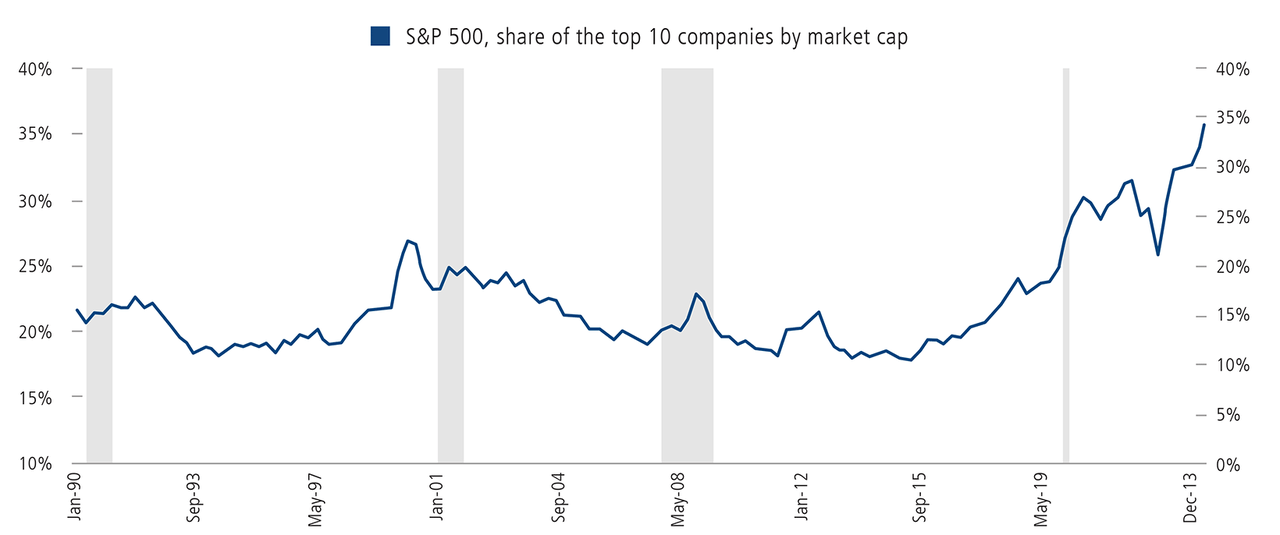

Recognizing AI’s significant opportunities, investors have directed their attention—and capital—toward potential “AI winners.” This focus has led to a historic concentration of market value in a handful of stocks. Currently, the four largest companies in the S&P 500 account for nearly 25% of the index, a level of concentration not witnessed since 1964.

Technology-related sectors have emerged as clear frontrunners, consistently outperforming benchmark returns. However, it’s crucial to note that the average growth stock’s performance has been more subdued than many investors realize. For example, the capitalization-weighted S&P 500 Technology sector delivered an impressive 34% return in the first half of the year, but the same group of companies yielded a more modest 12.6% return when weighted equally.

Market Trends and Factor Performance

This market dynamic has fostered intriguing trends. Momentum—the tendency for rising stocks to continue their upward trajectory—has emerged as the dominant factor influencing performance. Conversely, fundamentals and valuations, which typically drive outperformance over extended periods, have exerted minimal influence on stock performance.

As a result, valuations have surpassed historical averages. However, with earnings growth projected to accelerate in the latter half of the year (current expectations place S&P 500 earnings for 2024 at approximately $245 per share, representing an 11% increase from 2023) we do not anticipate that these elevated valuations will negatively impact returns.

Looking Ahead: Challenges and Opportunities

There are indications that many of the tailwinds propelling the economy are beginning to dissipate. Financial conditions show signs of softening, and stress signals are emerging among the most vulnerable consumer segments. Additionally, the upcoming US election and many geopolitical risks pose significant challenges for investors.

In this complex environment, we are focusing on risk management and identifying high-quality companies capable of generating substantial cash flow and earnings growth while maintaining robust and flexible financial positions. Although we expect technology to remain at the forefront of investment opportunities, the proliferation of AI benefits across various sectors should broaden the landscape for potential investments.

As AI’s transformative impact permeates the broader economy, we anticipate a corresponding expansion of investment prospects beyond the technology sector, potentially leading to a more diverse and balanced market environment.

Stock Picking Matters

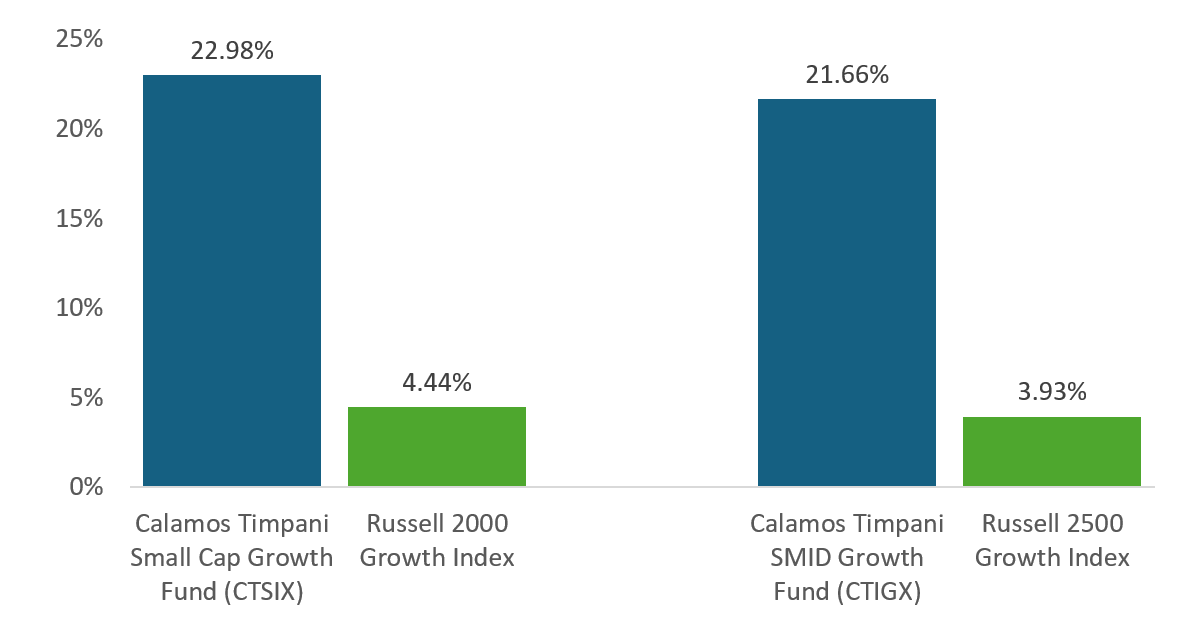

By Brandon Nelson, CFA – Calamos Timpani Small Cap Growth Fund (CTSIX), Calamos Timpani SMID Growth Fund (CTIGX)

Stocks were mixed during the second quarter. At the index level, large cap growth stocks rose sharply, and everything else fell. However, at the stock-specific level, many individual stocks up and down the market-cap spectrum performed spectacularly. In a refreshing turn of events, this quarter and the year-to-date have been less about rotation relating to macro factors like interest rates and more about stock picking driven by company-specific fundamentals.

One area of fundamental strength relates to increased data center spend. Governments and large companies are spending billions of dollars to build data center infrastructure to enable generative AI (Gen-AI). Since last spring, we have been investing in companies receiving that spend, including companies with exposure to Gen-AI servers, power/thermal management equipment, and construction site data center development.

Another area of fundamental strength relates to commercial aerospace replacement parts (i.e., aftermarket parts). Passenger miles are in a strong uptrend, but manufacturing constraints are delaying new airplane construction, which means older planes must fly for longer. This additional wear-and-tear increases demand for aftermarket parts—at healthy profit margins for the companies selling them.

These are just two of the exciting themes within the Calamos Timpani Small Cap Growth Fund (CTSIX) and Calamos Timpani SMID Growth Fund (CTIGX). We have uncovered several additional fundamental themes as well as other, one-off exciting individual stocks.

What’s especially encouraging is that the market is finally embracing our flavor of stocks again—companies with strong fundamental momentum (i.e., fast and underestimated growth). We believe these tailwinds have legs and that we are in the early stages of a multi-year upcycle for our particular investment style.

Calamos Timpani Funds: Security Selection Fuels Year-to-Date Performance

Year-to-date return through 6/30/2024

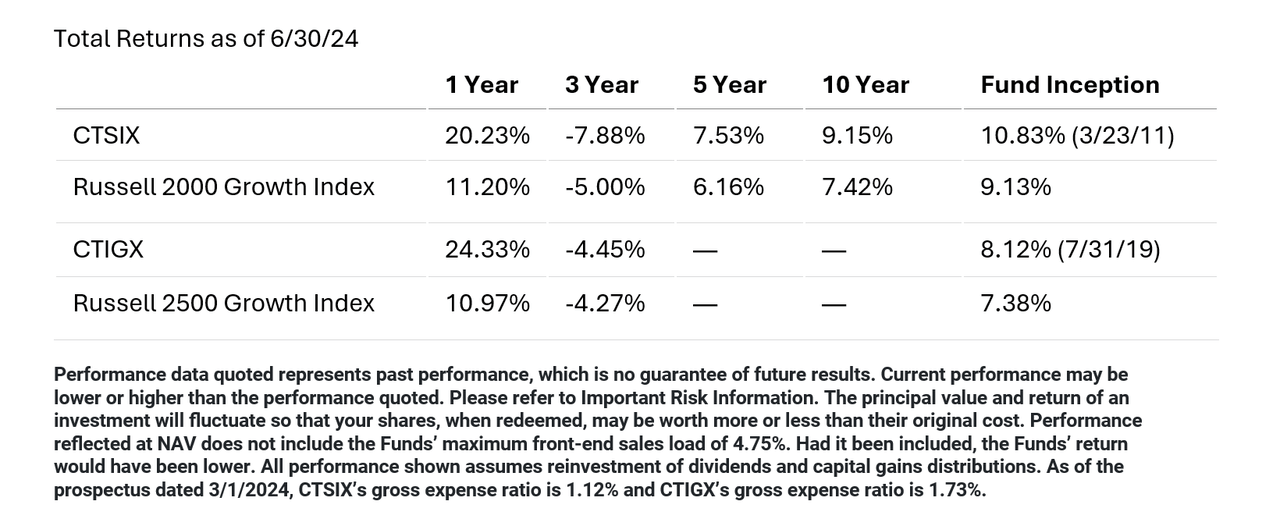

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Funds’ maximum front-end sales load of 4.75%. Had it been included, the Funds’ return would have been lower. All performance shown assumes reinvestment of dividends and capital gains distributions. As of the prospectus dated 3/1/2024, CTSIX’s gross expense ratio is 1.12% and CTIGX’s gross expense ratio is 1.73%. (Source: Morningstar.)

Zooming out, we’re also excited about the prospects for small caps overall. It’s been well documented that small caps have lagged large caps for several years despite having compelling growth fundamentals. This is reflected in valuation metrics of small caps versus large caps (currently in the 10th percentile).* The US Federal Reserve is increasingly likely to cut interest rates in the coming months, which we see as a powerful catalyst to trigger small cap outperformance. A catch-up trade for the asset class may soon be on the horizon, further increasing our optimism.

*Source: Jefferies, as of June 30, 2024, valuations of small caps versus large caps, lower percentiles indicate more favorable relative valuations for small caps.

Average annual total return measures net investment income and capital gain or loss from portfolio investments as an annualized average. All performance shown assumes reinvestment of dividends and capital gains distributions. Returns of more than one year are annualized

The Russell 1000® Index measures the performance of the large-cap segment of the US equity universe. The Russell 2000® Index measures the performance of the small-cap segment of the US equity universe. The Russell 2000® Growth Index measures the performance of the small-cap growth segment of the US equity universe. It includes those Russell 2000® companies with higher price-to-value ratios and higher forecasted growth values. The Russell 2500® Growth Index measures the performance of the small to midcap growth segment of the US equity universe. It includes those Russell 2500 companies with higher growth earning potential. Unmanaged index returns, unlike fund returns, do not reflect fees, expenses or sales charges. Investors cannot invest directly in an index.

Finding Much to Like in Global Equity Markets

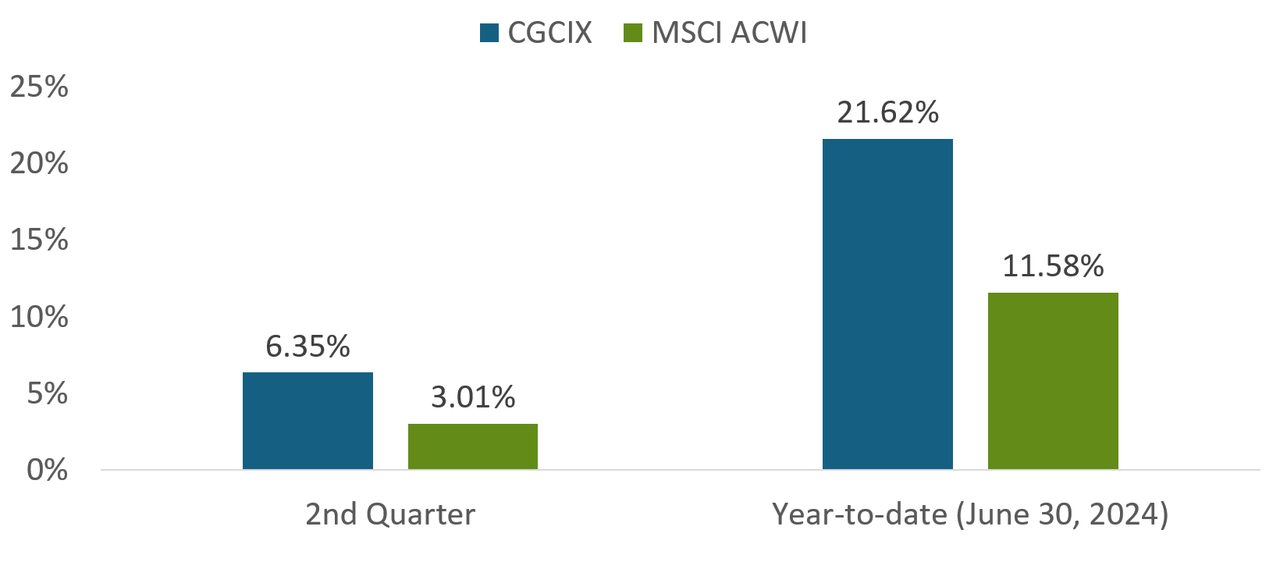

By Nick Niziolek, CFA, Dennis Cogan, CFA, Paul Ryndak, CFA, and Kyle Ruge, CFA – Calamos Global Opportunities Fund (CGCIX)

Global equity markets added to year-to-date gains during the second quarter, even though economic data regarding the growth and inflation outlook remained mixed. Peak Covid re-opening tailwinds and peaks in inflation and accelerating growth are all in the rearview mirror for most major economies. Even so, we believe the global economy is resilient overall, and recession is not our base case. Regarding our macro framework, we believe we are in a period of disinflationary growth characterized by decreasing inflation and decent economic fundamentals, which is a generally benign backdrop and an ideal environment for growth equities, including those with secular tailwinds.

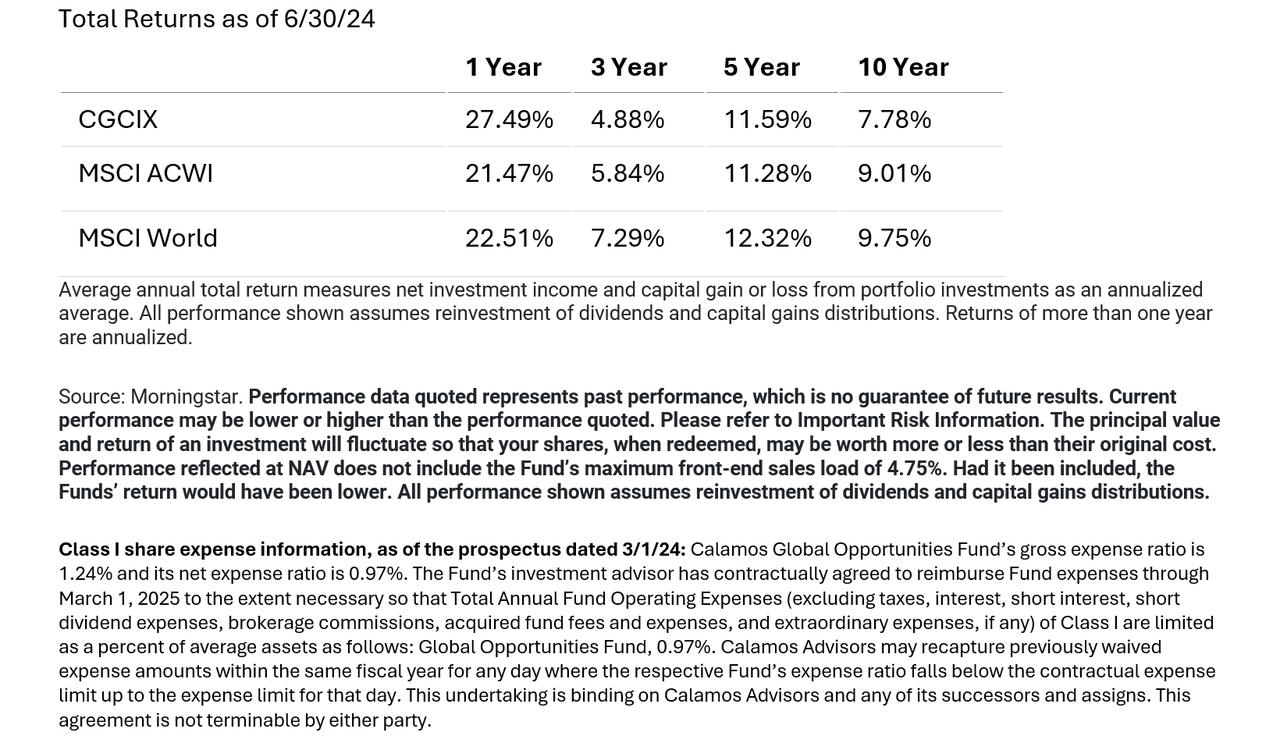

Calamos Global Opportunities Fund Has Performed Strongly in 2024

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load of 4.75%. Had it been included, the Fund’s return would have been lower. All performance shown assumes reinvestment of dividends and capital gains distributions. As of the prospectus dated 3/1/2024, CGCIX’s gross expense ratio is 1.24%. ( Source: Morningstar.)

Below, we highlight some key positioning themes in Calamos Global Opportunities Fund:

US Markets: More to Cheer than Just the Mag 7

Although Calamos Global Opportunities Fund is modestly underweight to the US versus the MSCI ACWI Index, US companies are the fund’s largest country weighting as of June 30, 2024. The disinflationary growth narrative certainly appears to be in force in the US: Some recent economic data and indicators have weakened, but overall growth remains solid, and inflation continues to fall. This creates a favorable backdrop for companies benefiting from strong and sustainable growth, including those at the center of powerful secular growth themes. Our investment process is focused on finding the best of these. Secular growth has been a driver of the market’s strong year-to-date performance, and CGCIX has been positioned for these tailwinds as well.

One of the most common concerns—or even complaints! —that investors are voicing these days relates to the concentration of the market’s returns in a small number of stocks, most often— the “Magnificent Seven. ” We find this a little confusing. Consider the Russell 1000 Index. Although on a market-cap-weighted basis, it is true that a relatively small number of companies have driven a large portion of the Index’s year-to-date return, it’s also true that more than 100 names have returned more than 25% year-to-date. These performers represent a variety of industries, market caps, and growth themes. For active managers who are willing and able to express conviction, we believe there will continue to be many opportunities to invest in companies that the market will reward for their strong fundamentals and ability to grow their intrinsic values. And this is only in the US; globally, the opportunity set is even greater!

Japan: Targeting Pockets of Opportunity

Japan counts among our top five country weightings as of the end of the quarter. We recently returned from a research trip to Japan, which included company tours, meetings with senior management teams, and spirited debates and discussions with some of our peers. Although the tone from company management teams was generally optimistic and investor interest in Japanese equities is high, we are mindful of changing sentiment within the domestic economy. In 2023, we were struck by how the average worker was cheering inflation—and the significant wage gains inflation fueled. However, the realization that inflation is eroding purchasing power is sinking in. This new reality is likely to have knock-on effects on consumer-driven sectors of the economy.

Consequently, although the combination of valuations, improved corporate governance, and a focus on optimizing capital allocation supports our optimistic view of Japan’s equity market, we have emphasized global companies domiciled in Japan because these multinationals can also benefit from the continued unfolding of the global capex cycle.

Another cause for optimism within the Japanese equity market centers on the success of recent retirement savings reforms, which have led to increased investments in local and overseas markets. New savings plans create a steady flow of capital from the retail segment into the capital markets and have also increased the average person’s interest in the markets. We believe this higher engagement will help drive additional reforms and incentivize companies to be shareholder-friendly.

The Opportunity of EM Convertible Securities

We use convertible securities opportunistically to improve the fund’s risk/reward skew. Convertibles allow us to capture equity market upside with potentially less downside exposure, providing an attractive way to access growth opportunities. Over recent quarters, we have increased our exposure to emerging market convertibles. We have built exposure to attractive businesses by investing in convertible structures that are less volatile than their underlying equities while still providing exposure to the stock market’s upside.

During the second quarter, several large Chinese internet companies issued convertible bonds to fund stock buybacks, and their management teams communicated to the market that they believed the underlying equities were significantly undervalued. In several cases, we also had a favorable view of valuations and invested in these newly issued convertibles to participate in well-priced access to growth.

Industrials: A Closer Look

Our exposure to the industrial sector is multi-dimensional, spanning secular, turnaround/capital improvement, and more cyclical names. Reflecting the sector’s breadth of opportunity, the fund includes a meaningful overweight to industrials. The secular opportunities for data center infrastructure are among the most exciting for the sector. Both power and thermal equipment will see an uptick in demand because AI chips and servers use three to four times more electrical power than traditional central processing units. According to the IEA, global data center total electricity consumption is expected to double from 2022 to 2026.

As overall electricity consumption rises, new infrastructure investments will be made inside data centers (e.g., new servers, cooling equipment, and additional power supplies) and outside the centers to expand power generation and transmission to meet demand.

Our overweight also reflects the bottom-up fundamentals in many industrial companies, including improved operational efficiencies, margins, and cash flows; and new management teams committed to strengthening competitive positioning. Japan-domiciled companies are well represented within our industrial holdings, where country-specific factors provide new catalysts for management teams to improve operational efficiencies, eliminate noncore holdings, and return capital to shareholders—a welcome shift after years of stagnant corporate evolution.

It’s a Market of (Global) Stocks, not a Stock Market

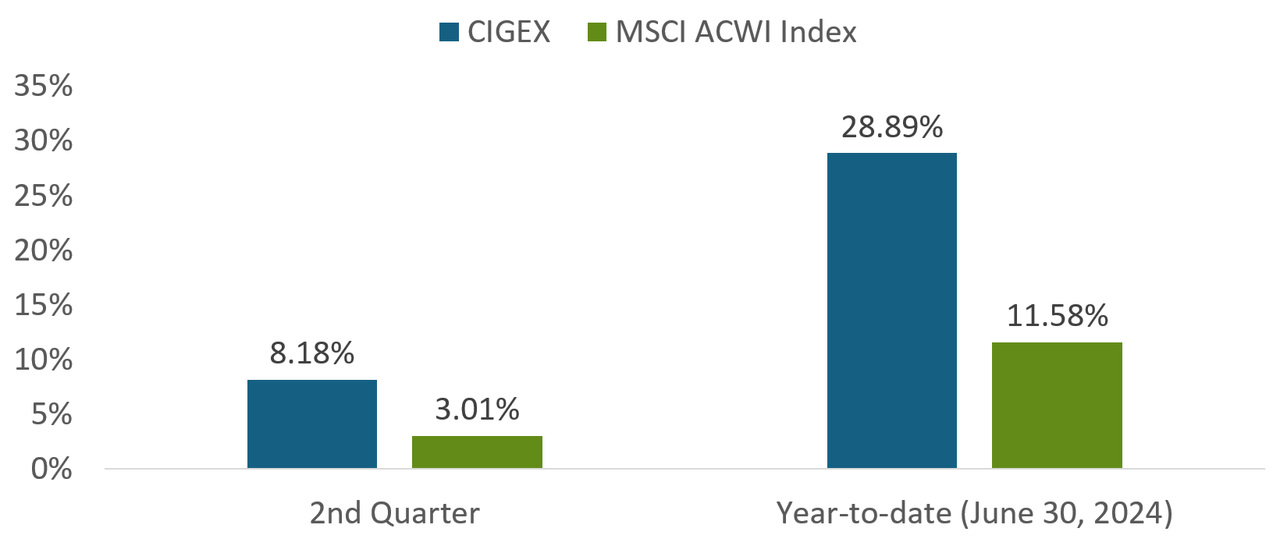

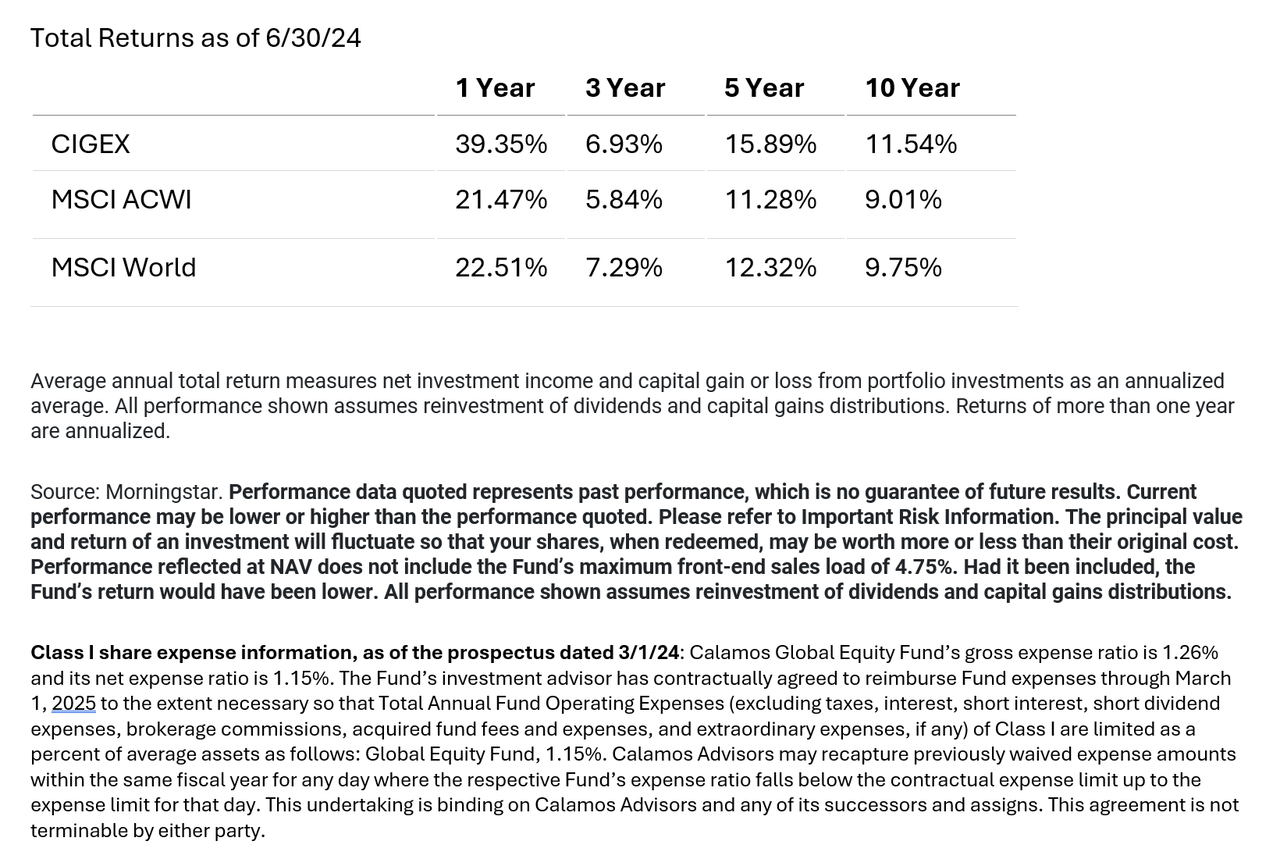

By Nick Niziolek, CFA, Dennis Cogan, CFA, Paul Ryndak, CFA, and Kyle Ruge, CFA – Calamos Global Equity Fund (CIGEX)

Global equity markets added to year-to-date gains during the second quarter, even though economic data regarding the growth and inflation outlook remained mixed. Peak Covid re-opening tailwinds and peaks in inflation and accelerating growth are all in the rearview mirror for most major economies. Even so, we believe the global economy is resilient overall, and recession is not our base case.

Regarding our macro framework, we believe we are in a period of disinflationary growth characterized by decreasing inflation and decent economic fundamentals, which is a generally a benign backdrop and an ideal environment for growth equities, including those with secular tailwinds.

Calamos Global Equity Fund Has Performed Strongly in 2024

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Funds’ maximum front-end sales load of 4.75%. Had it been included, the Funds’ return would have been lower. All performance shown assumes reinvestment of dividends and capital gains distributions. As of the prospectus dated 3/1/2024, CGCIX’s gross expense ratio is 1.26%. (Source: Morningstar.)

Below, we highlight some key positioning themes in Calamos Global Equity Fund:

US Markets: More to Cheer than Just the Mag 7

Although Calamos Global Equity Fund is underweight to the US versus the MSCI ACWI Index and MSCI World Index, US companies are the fund’s largest country weighting as of June 30, 2024. The disinflationary growth narrative certainly appears to be in force in the US: Some recent economic data and indicators have weakened, but overall growth remains solid, and inflation continues to fall. This creates a favorable backdrop for companies benefiting from strong and sustainable growth, including those at the center of powerful secular growth themes. Our investment process is focused on finding the best of these. Secular growth has been a driver of the market’s strong year-to-date performance, and the fund has been positioned for these tailwinds as well.

One of the most common concerns—or even complaints!—that investors are voicing these days relates to the concentration of the market’s returns in a small number of stocks, most often— the “Magnificent Seven.” We find this a little confusing. Consider the Russell 1000 Index. Although on a market-cap-weighted basis, it is true that a relatively small number of companies have driven a large portion of the Index’s year-to-date return, it’s also true that more than 100 names have returned more than 25% year-to-date. These performers represent a variety of industries, market caps, and growth themes. For active managers who are willing and able to express conviction, we believe there will continue to be many opportunities to invest in companies that the market will reward for their strong fundamentals and ability to grow their intrinsic values. And this is only in the US; globally, the opportunity set is even greater!

Japan: Targeting Pockets of Opportunity

Japan counts among our top five country weightings as of the end of the quarter. We recently returned from a research trip to Japan, which included company tours, meetings with senior management teams, and spirited debates and discussions with some of our peers. Although the tone from company management teams was generally optimistic and investor interest in Japanese equities is high, we are mindful of changing sentiment within the domestic economy. In 2023, we were struck by how the average worker was cheering inflation—and the significant wage gains inflation fueled. However, the realization that inflation is eroding purchasing power is sinking in. This new reality is likely to have knock-on effects on consumer-driven sectors of the economy.

Consequently, although the combination of valuations, improved corporate governance, and a focus on optimizing capital allocation supports our optimistic view of Japan’s equity market, we have emphasized global companies domiciled in Japan because these multinationals can also benefit from the continued unfolding of the global capex cycle.

Another cause for optimism within the Japanese equity market centers on the success of recent retirement savings reforms, which have led to increased investments in local and overseas markets. New savings plans create a steady flow of capital from the retail segment into the capital markets and have also increased the average person’s interest in the markets. We believe this higher engagement will help drive additional reforms and incentivize companies to be shareholder-friendly.

Industrials: A Closer Look

Our exposure to the industrial sector is multi-dimensional, spanning secular, turnaround/capital improvement, and more cyclical names. Reflecting the sector’s breadth of opportunity, the fund includes a healthy overweight to industrials. The secular opportunities for data center infrastructure are among the most exciting for the sector. Both power and thermal equipment will see an uptick in demand because AI chips and servers use three to four times more electrical power than traditional central processing units. According to the IEA, global data center total electricity consumption is expected to double from 2022 to 2026.

As overall electricity consumption rises, new infrastructure investments will be made inside data centers (e.g., new servers, cooling equipment, and additional power supplies) and outside the centers to expand power generation and transmission to meet demand.

Our overweight also reflects the bottom-up fundamentals in many industrial companies, including improved operational efficiencies, margins, and cash flows; and new management teams committed to strengthening competitive positioning. Japan-domiciled companies are well represented within our industrial holdings, where country-specific factors provide new catalysts for management teams to improve operational efficiencies, eliminate noncore holdings, and return capital to shareholders—a welcome shift after years of stagnant corporate evolution.

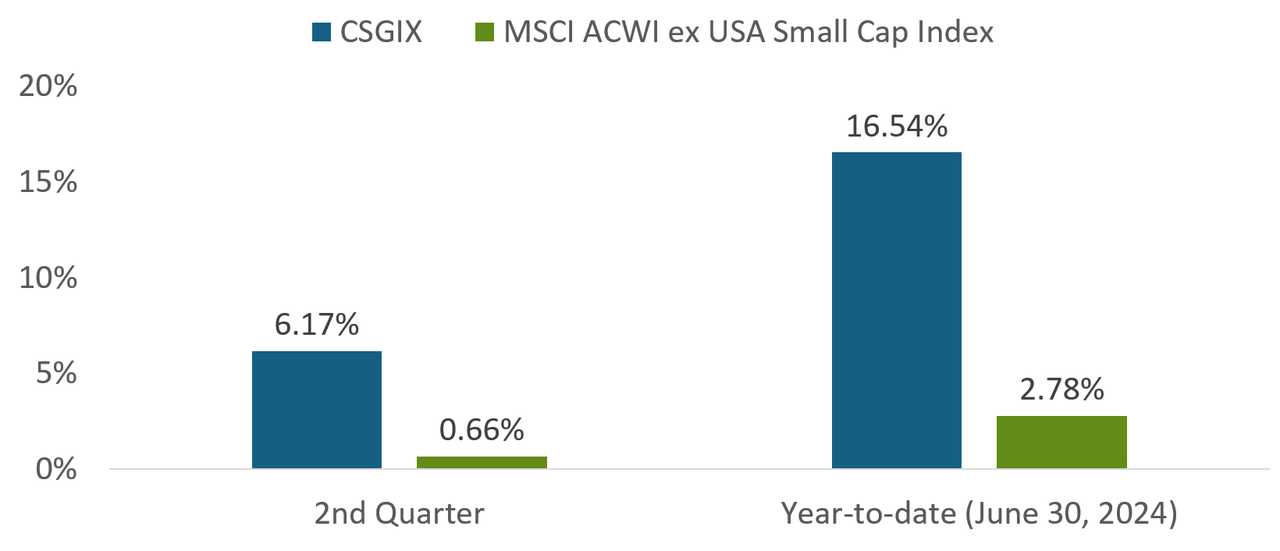

Uncovering Big Prospects in International Small Caps

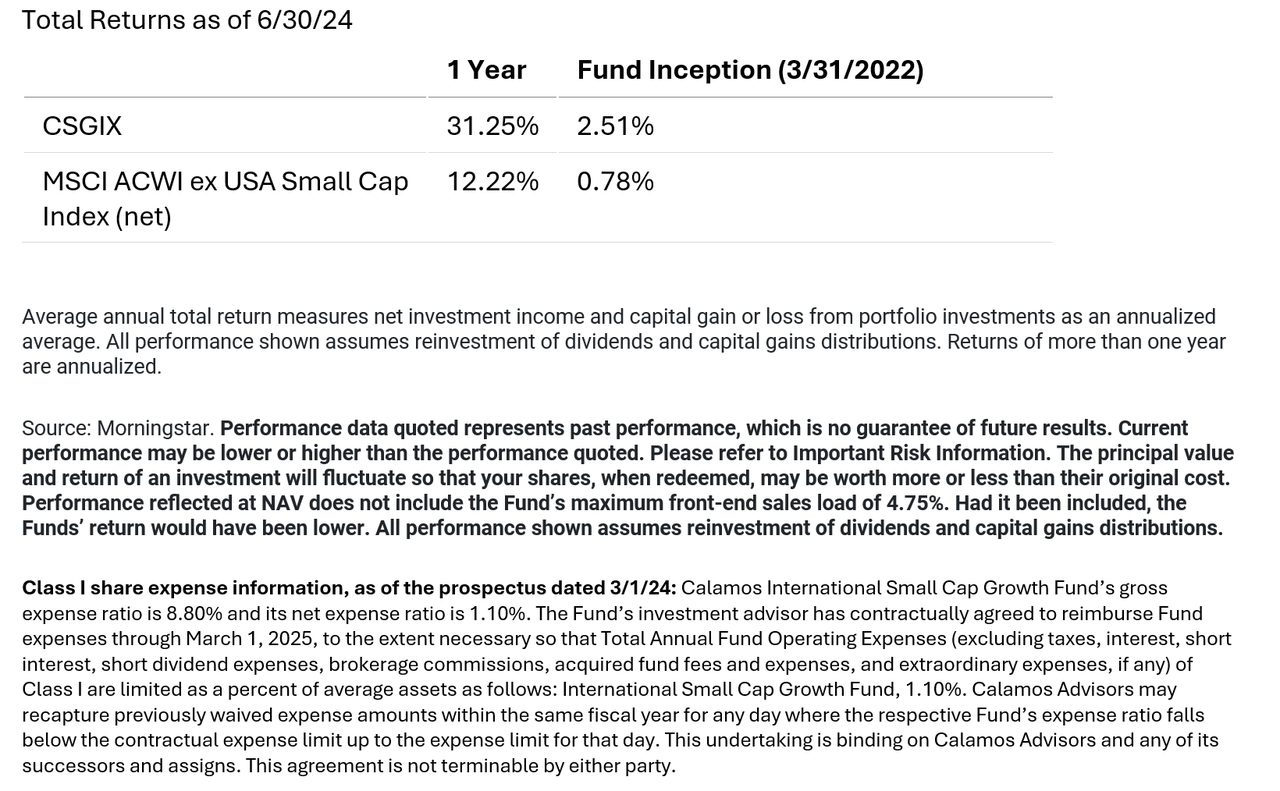

By – Nick Niziolek, CFA, Dennis Cogan, CFA, Paul Ryndak, CFA, and Kyle Ruge, CFA – Calamos International Small Cap Growth Fund (CSGIX)

Peak Covid re-opening tailwinds and peaks in inflation and accelerating growth are all in the rearview mirror for most major economies. Even so, we believe the global economy is resilient overall, and recession is not our base case. We believe we are in a period of disinflationary growth characterized by decreasing inflation and decent economic fundamentals, which is a generally benign backdrop and an ideal environment for growth equities, including small caps.

Calamos International Small Cap Growth Fund Has Performed Strongly in 2024

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load of 4.75%. Had it been included, the Fund’s return would have been lower. All performance shown assumes reinvestment of dividends and capital gains distributions. As of the prospectus dated 3/1/2024, CSGIX’s gross expense ratio is 8.80%. (Source: Morningstar.)

As we turn the corner into the second half of the year, we believe Calamos International Small Cap Growth Fund is well positioned to harness the tailwinds of this disinflationary growth environment. Drawing on our proprietary process, we are identifying companies with quality attributes that are participating in growth trends—both global and regionally specific—across international markets.

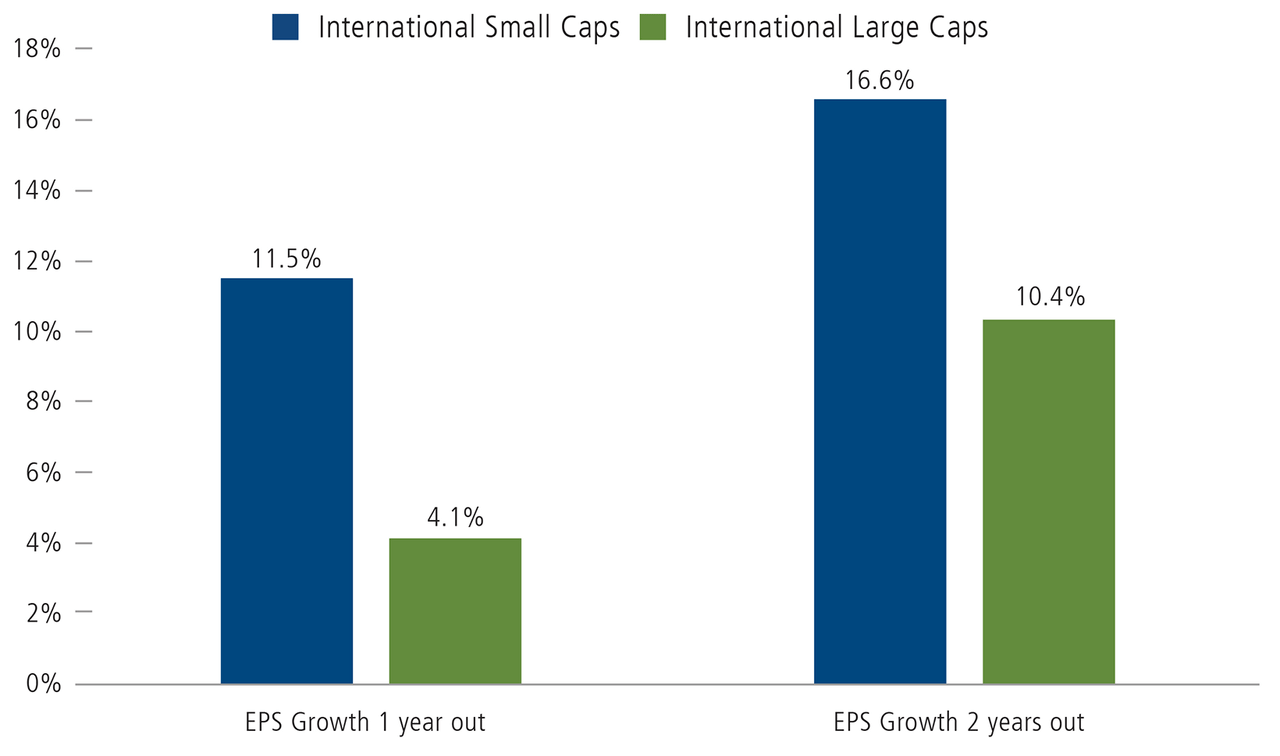

We believe that the case for international small caps is strategic but especially strong in the current environment. We are finding many international small caps that offer more attractive growth potential relative to international large caps, and the valuations of international small caps are, on the whole, more attractive than those of US small caps and the broader international equity market.

International Small Caps: Positioned for Better Growth

Estimated earnings per share growth

Past performance is no guarantee of future results. Source: Bloomberg. International small caps are represented by the MSCI ACWI ex USA Small Cap Index. International large cap stocks are represented by the MSCI ACWI ex USA Index. Data as of 6/15/2024.

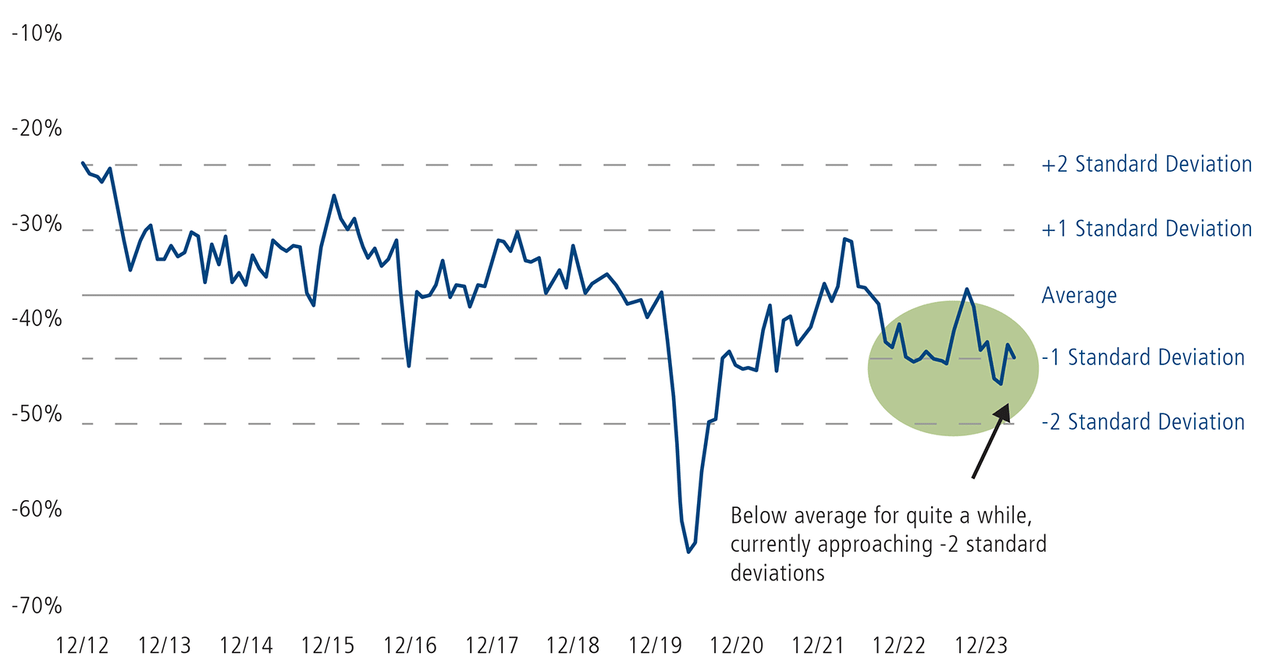

International Small Caps Offer Attractive Valuation Potential Versus US Small Caps

MSCI ACWI ex-US Small Cap Forward P/E Discount/Premium vs. Russell 2000 Index

Past performance is no guarantee of future results. Source: Bloomberg. The lower the value, the wider the discount of forward P/Es of international small cap stocks compared to US small cap stocks. Data as of May 31, 2024.

As shown above, the valuation differential has widened to nearly two standard deviations, which we believe represents an especially compelling opportunity. Moreover, while international small caps are participating in global growth themes, they also provide access to other growth tailwinds, such as the localization of supply chains. We believe our depth of fundamental and thematic research positions us to capitalize on market inefficiencies, which are even more pronounced in overseas markets versus the US. Below, we take a closer look at three areas of conviction within the fund: opportunities within Japan, India, and the industrials sector.

Votes Are in: India’s Growth Story Is Intact

The fund’s second largest weighting is to India, and our allocation is more than double the weighting within the MSCI ACWI ex USA Small Cap Index as of June 30, 2024. We’ve been bullish on India for quite some time, where the encouraging economic and policy reforms championed by Prime Minister Narendra Modi are just one of many catalysts. Although India’s equity market hit a bit of an air pocket after recent national election results diverged from exit-poll expectations, we believe India’s growth story and investment cycle are strong.

While Modi won his third straight term as prime minister and a ruling coalition led by the incumbent Bharatiya Janata Party (BJP) and a second party held the majority, the BJP lost seats. Although this contributed to a selloff in Indian equities immediately following the election, the market has since steadied and regained ground.

We believe pre-election policies are likely to stay on track. Major post-election ministry appointments should provide continuity of policy direction, with ministerial heads of Roads & Highways, Railways, Home, Defense, and Ports all retained by the BJP. Moreover, the government-mandated crop price implemented post-election aligned with the average hike over the past decade, easing concerns that the government would implement populist policies to appease the rural population. Additionally, there could be some positives resulting from the structure of the current coalition government, including a lower chance of constitutional and sweeping policy changes. The coalition may act as a check to keep the BJP honest in doing what it has said it would do.

Accordingly, our long-term thesis on India hasn’t changed. The investment cycle continues, and the government’s healthy fiscal position can support existing policy direction. The fund continues to access India’s growth primarily through real estate and capex-driven industries that will benefit from the continuation of the investment cycle and government policies that encourage infrastructure and manufacturing growth. We have also identified opportunities in consumer-facing industries that can benefit from India’s favorable demographic trends, such as the rapid growth of the country’s middle-class and working-age populations.

Japan: Targeting Pockets of Opportunity

Japan is the fund’s largest allocation on absolute basis as of June 30, 2024. We recently returned from a research trip to Japan, which included company tours, meetings with senior management teams, and spirited debates and discussions with some of our peers. Although the tone from company management teams was generally optimistic and investor interest in Japanese equities is high, we are mindful of changing sentiment within the domestic economy. In 2023, we were struck by how the average worker was cheering inflation—and the significant wage gains inflation fueled. However, the realization that inflation is eroding purchasing power is sinking in. This new reality is likely to have knock-on effects on consumer-driven sectors of the economy.

Consequently, although the combination of valuations, improved corporate governance, and a focus on optimizing capital allocation supports our optimistic view of Japan’s equity market, we have emphasized global companies domiciled in Japan because these multinationals can also benefit from the continued unfolding of the global capex cycle.

Another cause for optimism within the Japanese equity market centers on the success of recent retirement savings reforms, which have led to increased investments in local and overseas markets. New savings plans create a steady flow of capital from the retail segment into the capital markets and have also increased the average person’s interest in the markets. We believe this higher engagement will help drive additional reforms and incentivize companies to be shareholder-friendly.

Industrials: A Closer Look

Our exposure to the industrial sector is multi-dimensional, spanning secular, turnaround/capital improvement, and more cyclical names. Reflecting the sector’s breadth of opportunity, the fund’s allocation to industrial companies is its largest and more than double that of the MSCI ACWI ex USA Index. The secular opportunities for data center infrastructure are among the most exciting for the sector. Both power and thermal equipment will see an uptick in demand because AI chips and servers use three to four times more electrical power than traditional central processing units. According to the IEA, global data center total electricity consumption is expected to double from 2022 to 2026.

As overall electricity consumption rises, new infrastructure investments will be made inside data centers (e.g., new servers, cooling equipment, and additional power supplies) and outside the centers to expand power generation and transmission to meet demand.

Our overweight also reflects the bottom-up fundamentals in many industrial companies, including improved operational efficiencies, margins, and cash flows; and new management teams committed to strengthening competitive positioning. Japan-domiciled companies are well represented within our industrial holdings, where country-specific factors provide new catalysts for management teams to improve operational efficiencies, eliminate noncore holdings, and return capital to shareholders—a welcome shift after years of stagnant corporate evolution.

Perspectives on Emerging Markets Opportunity

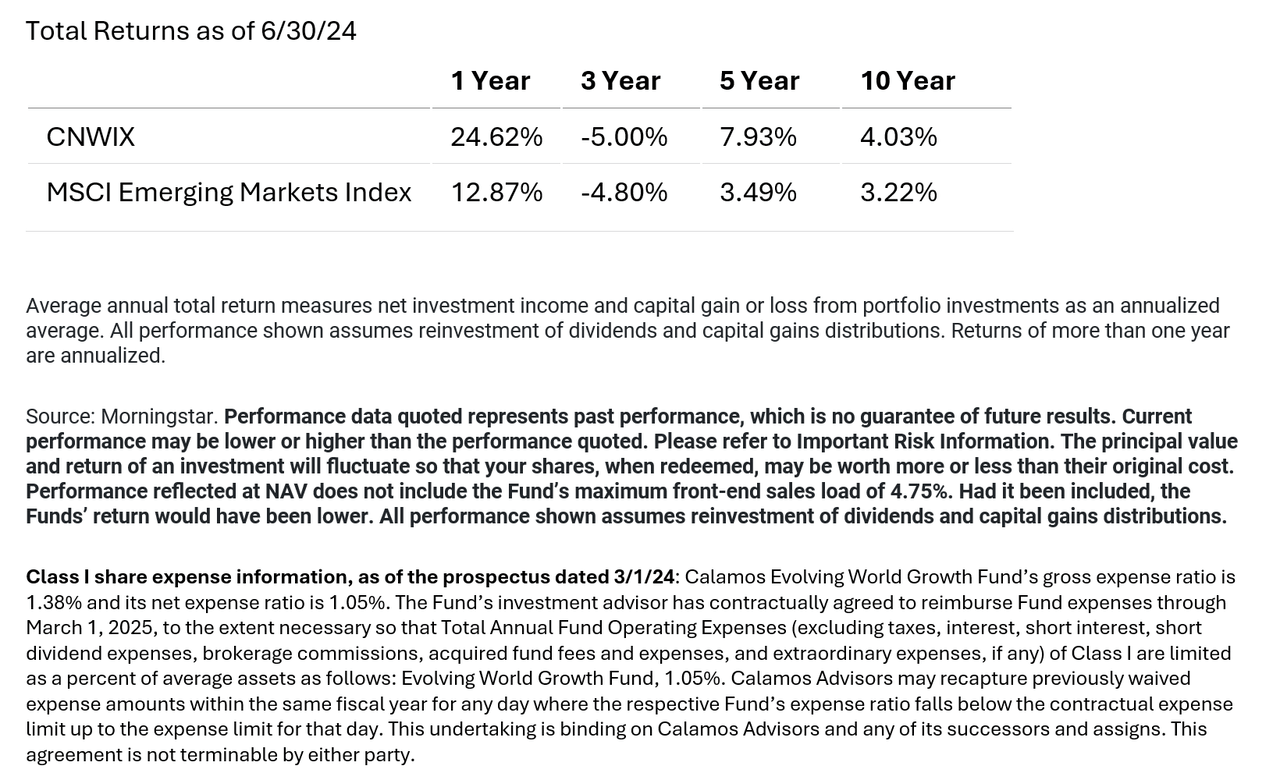

By Nick Niziolek, CFA, Dennis Cogan, CFA, Paul Ryndak, CFA, and Kyle Ruge, CFA – Calamos Evolving World Growth Fund (CNWIX)

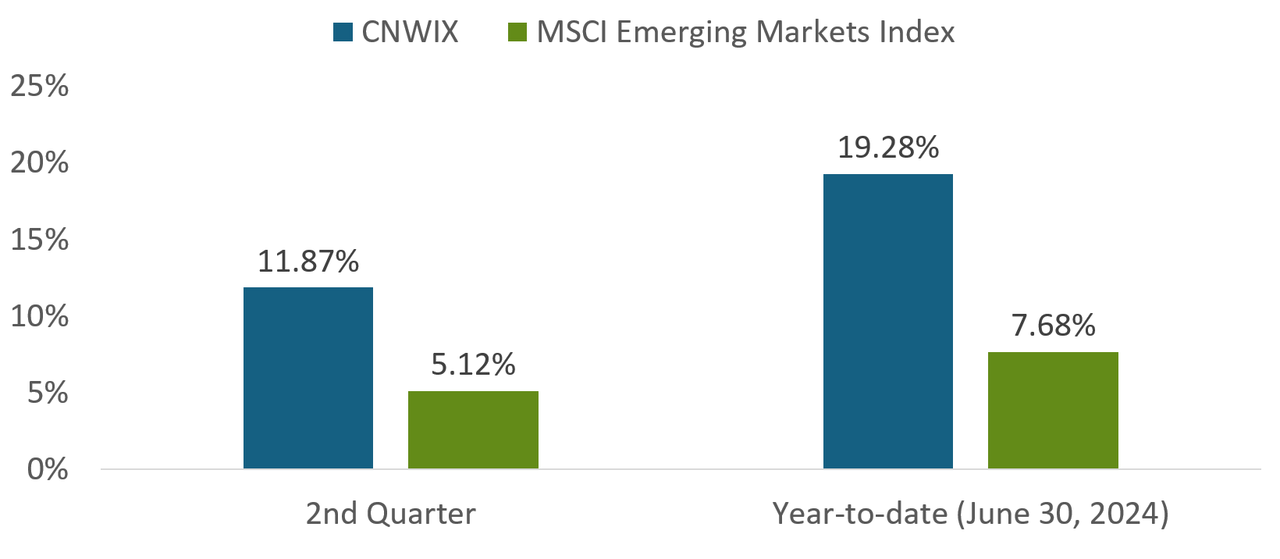

Global equity markets added to year-to-date gains during the second quarter, even though economic data regarding the growth and inflation outlook remained mixed. Emerging market equities performed with strength during the quarter: The MSCI Emerging Markets Index’s return of 5.1% outpaced both the S&P 500 Index (up 4.3%) and the MSCI ACWI ex USA Index (up 1.2%).

Calamos Evolving World Growth Fund Has Performed Strongly in 2024

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Funds’ maximum front-end sales load of 4.75%. Had it been included, the Funds’ return would have been lower. All performance shown assumes reinvestment of dividends and capital gains distributions. As of the prospectus dated 3/1/2024, CNWIX’s gross expense ratio is 1.38%. (Source: Morningstar.)

Peak Covid re-opening tailwinds and peaks in inflation and accelerating growth are all in the rearview mirror for most major economies. Even so, we believe the global economy is resilient overall, and recession is not our base case. Regarding our macro framework, we believe we are in a period of disinflationary growth characterized by decreasing inflation and decent economic fundamentals, which is a generally benign backdrop and an ideal environment for growth equities, including those with secular tailwinds. Below, we highlight some key positioning themes in Calamos Evolving World Growth Fund:

Industrials: A Closer Look

Our exposure to the industrial sector is multi-dimensional, spanning secular, turnaround/capital improvement, and more cyclical names. Reflecting the sector’s breadth of opportunity, the Fund’s allocation to industrial companies is more than double that of the MSCI Emerging Markets Index. The secular opportunities for data center infrastructure are among the most exciting for the sector. Both power and thermal equipment will see an uptick in demand because AI chips and servers use three to four times more electrical power than traditional central processing units. According to the IEA, global data center total electricity consumption is expected to double from 2022 to 2026.

As overall electricity consumption rises, new infrastructure investments will be made inside data centers (e.g., new servers, cooling equipment, and additional power supplies) and outside the centers to expand power generation and transmission to meet demand.

Our overweight also reflects the bottom-up fundamentals in many industrial companies, including improved operational efficiencies, margins, and cash flows; and new management teams committed to strengthening competitive positioning. Japan-domiciled companies are well represented within our industrial holdings, where country-specific factors provide new catalysts for management teams to improve operational efficiencies, eliminate noncore holdings, and return capital to shareholders—a welcome shift after years of stagnant corporate evolution.

The Opportunity of EM Convertible Securities

We use convertible securities opportunistically to improve the fund’s risk/reward skew. Convertibles allow us to capture equity market upside with potentially less downside exposure, providing an attractive way to access growth opportunities. Over recent quarters, we have increased our exposure to emerging market convertibles. We have built exposure to attractive businesses by investing in convertible structures that are less volatile than their underlying equities while still providing exposure to the stock market’s upside.

During the second quarter, several large Chinese internet companies issued convertible bonds to fund stock buybacks, and their management teams communicated to the market that they believed the underlying equities were significantly undervalued. In several cases, we also had a favorable view of valuations and invested in these newly issued convertibles to participate in well-priced access to growth.

Votes Are in: India’s Growth Story Is Intact

The fund’s largest country weighting is to India, representing more than one-third of the portfolio and more than twofold its benchmark’s weight as of June 30, 2024. We’ve been bullish on India for quite some time, where the encouraging economic and policy reforms championed by Prime Minister Narendra Modi are just one of many catalysts. Although India’s equity market hit a bit of an air pocket after recent national election results diverged from exit-poll expectations, we believe India’s growth story and investment cycle are strong.

While Modi won his third straight term as prime minister and a ruling coalition led by the incumbent Bharatiya Janata Party (BJP) and a second party held the majority, the BJP lost seats. Although this contributed to a selloff in Indian equities immediately following the election, the market has since steadied and regained ground.

We believe pre-election policies are likely to stay on track. Major post-election ministry appointments should provide continuity of policy direction, with ministerial heads of Roads & Highways, Railways, Home, Defense, and Ports all retained by the BJP. Moreover, the government-mandated crop price implemented post-election aligned with the average hike over the past decade, easing concerns that the government would implement populist policies to appease the rural population. Additionally, there could be some positives resulting from the structure of the current coalition government, including a lower chance of constitutional and sweeping policy changes. The coalition may act as a check to keep the BJP honest in doing what it has said it would do.

Accordingly, our long-term thesis on India hasn’t changed. The investment cycle continues, and the government’s healthy fiscal position can support existing policy direction. The fund continues to access India’s growth primarily through real estate and capex-driven industries that will benefit from the continuation of the investment cycle and government policies that encourage infrastructure and manufacturing growth. We have also identified opportunities in consumer-facing industries that can benefit from India’s favorable demographic trends, such as the rapid growth of the country’s middle-class and working-age populations.

International Growth Opportunities in Focus

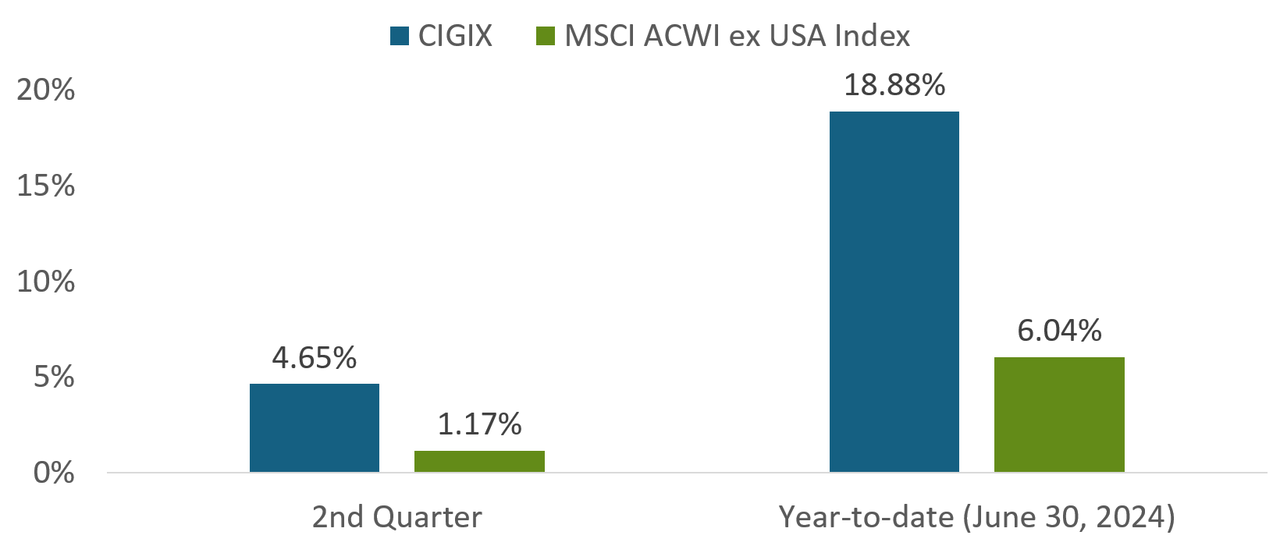

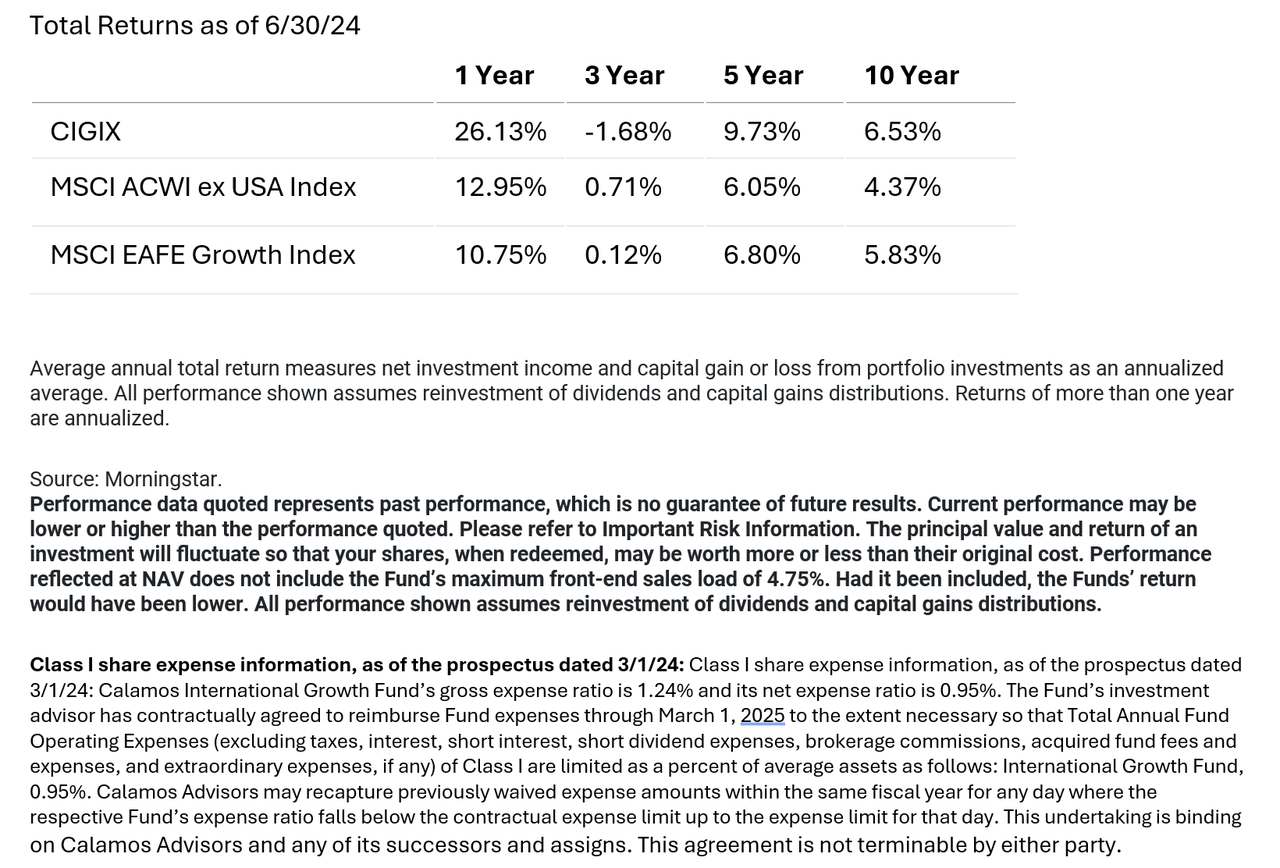

By Nick Niziolek, CFA, Dennis Cogan, CFA, Paul Ryndak, CFA, and Kyle Ruge, CFA – Calamos International Growth Fund (CIGIX)

International equity markets added to year-to-date gains during the second quarter, even though economic data regarding the growth and inflation outlook remained mixed. Emerging market equities performed with notable strength during the quarter: The MSCI Emerging Markets Index’s return of 5.1% outpaced the MSCI ACWI ex-USA Index (up 1.2%), and the MSCI World Index (up 2.8%).

Calamos International Growth Fund Has Performed Strongly in 2024

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load of 4.75%. Had it been included, the Fund’s return would have been lower. All performance shown assumes reinvestment of dividends and capital gains distributions. As of the prospectus dated 3/1/2024, CIGIX’s gross expense ratio is 1.24%. (Source: Morningstar.)

Peak Covid re-opening tailwinds and peaks in inflation and accelerating growth are all in the rearview mirror for most major economies. Even so, we believe the global economy is resilient overall, and recession is not our base case. Regarding our macro framework, we believe we are in a period of disinflationary growth characterized by decreasing inflation and decent economic fundamentals, which is a generally benign backdrop and an ideal environment for growth equities, including those with secular tailwinds. Below, we highlight some key positioning themes within Calamos International Growth Fund:

Japan: Targeting Pockets of Opportunity

Japan is our second largest allocation on absolute basis as of June 30, 2024. We recently returned from a research trip to Japan, which included company tours, meetings with senior management teams, and spirited debates and discussions with some of our peers. Although the tone from company management teams was generally optimistic and investor interest in Japanese equities is high, we are mindful of changing sentiment within the domestic economy. In 2023, we were struck by how the average worker was cheering inflation—and the significant wage gains inflation fueled. However, the realization that inflation is eroding purchasing power is sinking in. This new reality is likely to have knock-on effects on consumer-driven sectors of the economy.

Consequently, although the combination of valuations, improved corporate governance, and a focus on optimizing capital allocation supports our optimistic view of Japan’s equity market, we have emphasized global companies domiciled in Japan because these multinationals can also benefit from the continued unfolding of the global capex cycle.

Another cause for optimism within the Japanese equity market centers on the success of recent retirement savings reforms, which have led to increased investments in local and overseas markets. New savings plans create a steady flow of capital from the retail segment into the capital markets and have also increased the average person’s interest in the markets. We believe this higher engagement will help drive additional reforms and incentivize companies to be shareholder-friendly.

Industrials: A Closer Look

Our exposure to the industrial sector is multi-dimensional, spanning secular, turnaround/capital improvement, and more cyclical names. Reflecting the sector’s breadth of opportunity, the Fund’s allocation to industrial companies is its largest and more than double that of the MSCI ACWI ex USA Index. The secular opportunities for data center infrastructure are among the most exciting for the sector. Both power and thermal equipment will see an uptick in demand because AI chips and servers use three to four times more electrical power than traditional central processing units. According to the IEA, global data center total electricity consumption is expected to double from 2022 to 2026.

As overall electricity consumption rises, new infrastructure investments will be made inside data centers (e.g., new servers, cooling equipment, and additional power supplies) and outside the centers to expand power generation and transmission to meet demand.

Our overweight also reflects the bottom-up fundamentals in many industrial companies, including improved operational efficiencies, margins, and cash flows; and new management teams committed to strengthening competitive positioning. Japan-domiciled companies are well represented within our industrial holdings, where country-specific factors provide new catalysts for management teams to improve operational efficiencies, eliminate noncore holdings, and return capital to shareholders—a welcome shift after years of stagnant corporate evolution.

Votes Are In: India’s Growth Story Is Intact

The fund’s largest country weighting is to India, with an overweight that is more than triple the weighting within the MSCI ACWI ex USA Index. We’ve been bullish on India for quite some time, where the encouraging economic and policy reforms championed by Prime Minister Narendra Modi are just one of many catalysts. Although India’s equity market hit a bit of an air pocket after recent national election results diverged from exit-poll expectations, we believe India’s growth story and investment cycle are strong.

While Modi won his third straight term as prime minister and a ruling coalition led by the incumbent Bharatiya Janata Party (BJP) and a second party held the majority, the BJP lost seats. Although this contributed to a selloff in Indian equities immediately following the election, the market has since steadied and regained ground.