The Vanguard International Dividend Appreciation Index Fund ETF (NASDAQ:VIGI) has underperformed significantly so far this year. But that’s been the case for just about any stock not considered a Magnificent Seven name. While it’s hard to know when the tide may turn in favor of other niches, including foreign equities, at some point valuation will matter and diversification will pay dividends, so to speak.

I am upgrading VIGI from a hold to a buy. I was cautious about this low-cost ETF late last year, and the fund indeed has underperformed the S&P 500 by about 12 percentage points since the previous analysis. A strong dollar lately has certainly hurt, but a general preference for US mega-cap stocks has been the primary culprit for VIGI’s negative alpha.

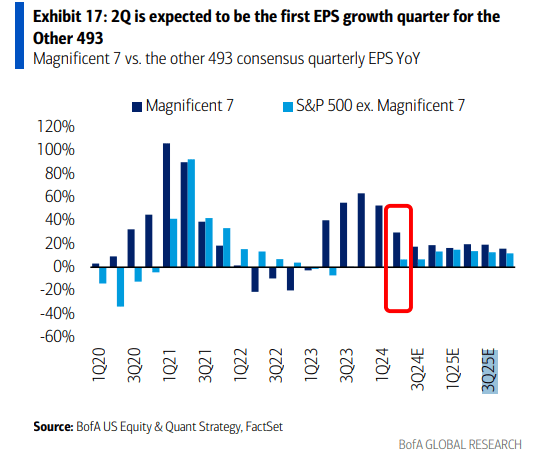

What could be the catalyst for a change in the zeitgeist? Perhaps it is the reality that EPS growth among the Mag 7 is set to cool this reporting season. If we see other areas cast in a better relative light, then money moving away from the biggest of big US tech-related names, into areas such as the “Other” 493 and ex-US stocks, could lead to significant mean reversion favoring VIGI.

2Q is expected to mark the first growth quarter for the Other 493

BofA Global Research

According to the issuer, VIGI seeks to track the performance of the S&P Global EX-US Dividend Growers Index through a passively managed, full-replication strategy. Fully invested at all times, the primarily large-cap ETF invests in companies from both developed and emerging market countries that have a track record of growing dividends year over year.

Despite soft relative returns since Q4 2023, VIGI has grown to become a $7 billion ETF, as measured by assets under management (as of July 8, 2024) – that’s up from just $5 billion last November. Investors seeking growing dividends from firms located outside the US borders have apparently been drawn to VIGI’s low 0.15% annual expense ratio, though the current trailing 12-month dividend yield is just 1.9%, about 0.5 percentage points above that of the S&P 500.

Share-price momentum has been lukewarm at best so far this year, following an impressive thrust off its low late last year. But VIGI sports a solid risk rating given its diversified portfolio and generally low annual standard deviation. Additionally, the fund’s liquidity grade is high – average daily volume is north of 200,000 shares while its 30-day median bid/ask spread is not overly wide at five basis points, per Vanguard.

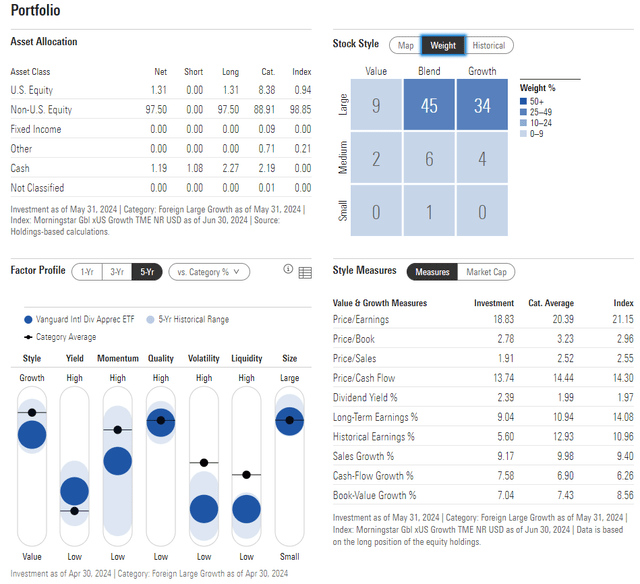

Now let’s review where VIGI’s portfolio stands today. Now a 4-star, still Gold-rated ETF by Morningstar, there isn’t too much change in the style box positioning. It is still a large-cap growth fund, and the allocation to SMIDs is about the same. While VIGI is two turns more expensive on a price-to-earnings ratio basis today, it is marginally cheaper in a relative sense considering that the S&P 500 is more than 21x earnings.

VIGI: Portfolio & Factor Profiles

Morningstar

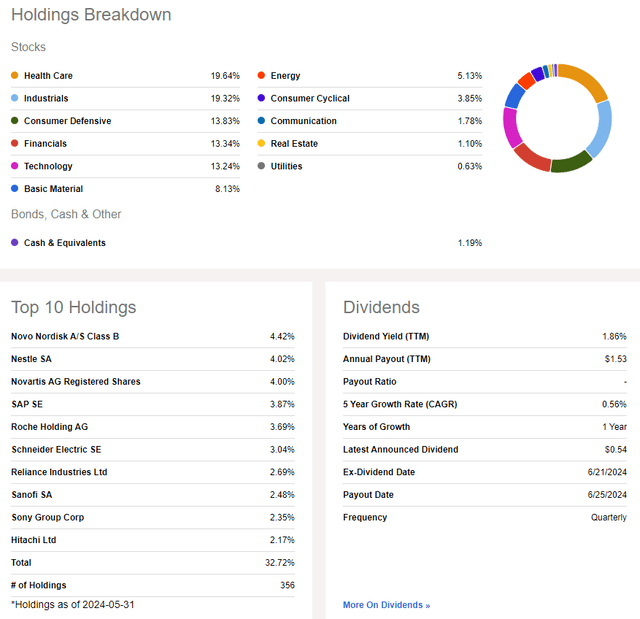

VIGI has solid sector diversification. Health Care is the largest weight at close to 20% – shares of GLP-1 developer Novo Nordisk (NVO) is the biggest single stock position. Industrials, a more risk-on and cyclical niche of the international equity market, is the runner-up in size. Of course, a low weight to Information Technology presents a possible risk if that sector continues to outperform.

VIGI: Holdings & Dividend Information

Seeking Alpha

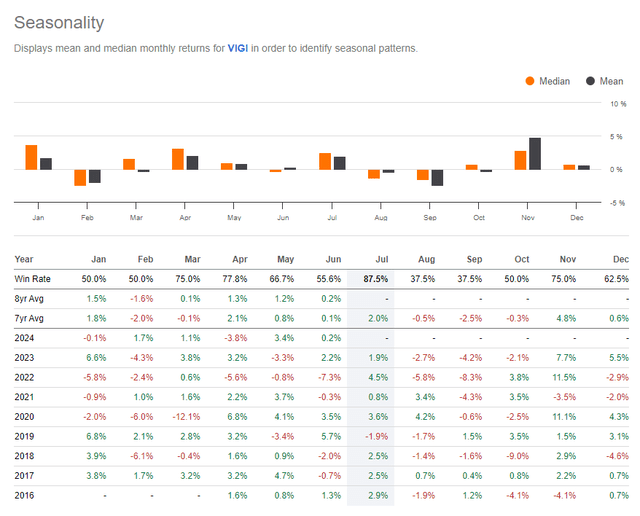

Another risk is weak seasonal trends. While July has historically been a positive month, the August through October stretch has often featured increased volatility and weaker returns.

VIGI: Weak August-October Returns

Seeking Alpha

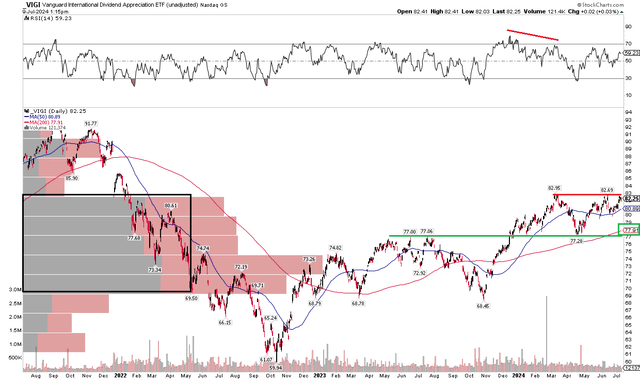

The Technical Take

With a strong relative valuation, diversified portfolio, and admittedly bearish seasonal trends ahead, VIGI’s technical picture looks a bit better today compared with my original analysis. Notice in the chart below that shares rallied through an area that I noted was key resistance last time. Today, the $77 to $78 is now support, while $82 to $83 has emerged as an area of selling.

But with a rising long-term 200-day moving average and a series of higher lows off the October 2022 nadir, the primary trend appears to be controlled by the bulls. A technical risk is a minor bearish RSI divergence when analyzing the oscillator at the top of the graph. Offsetting that is a high amount of volume by price in the $70 to $81 range, so pullbacks should be met with significant buying support.

Overall, VIGI’s trend looks better today. I would like to see the ETF rally through $83 to set up the next leg of what appears to be a multi-year bull market.

VIGI: Watch $83 For a Breakout, Long-Term Support at $77

StockCharts.com

The Bottom Line

I have a buy rating on VIGI. I see this low-cost, diversified dividend-growth portfolio as priced reasonably today with improved technical trends.

Read the full article here