About the Company

General Dynamics (NYSE:GD) is one of the largest global defense companies in the world, and it consists of four segments: Aerospace, Marine Systems, Combat Systems and Technologies. GD has returned a solid 7.6% year to date compared to the S&P 500 Trust ETF (SPY) which has gained nearly 17%. Conversely, over the past year, General Dynamics has outgained SPY by nearly 5%, returning almost 31% while SPY has a respectable return of 26.5%.

Financial Metrics

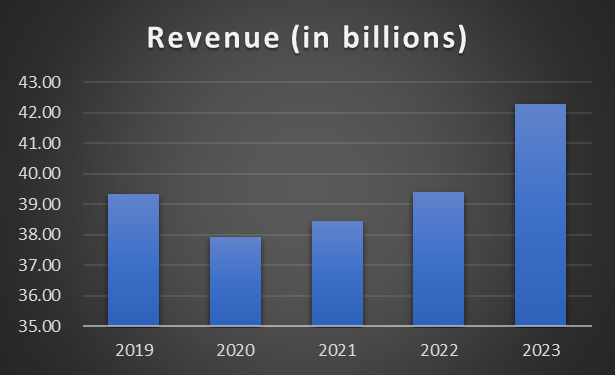

As you can see from the chart below, General Dynamics ended the previous decade on a downward trend, with revenue decreasing 3.6% from 2019 to 2020. However, following the pandemic, sales have increased every year, going from $38.4 billion in 2021 to north of $42 billion in fiscal year 2023, resulting in a compound annual growth rate of almost 5%, very respectable for a mature company.

GD’s Annual Reports

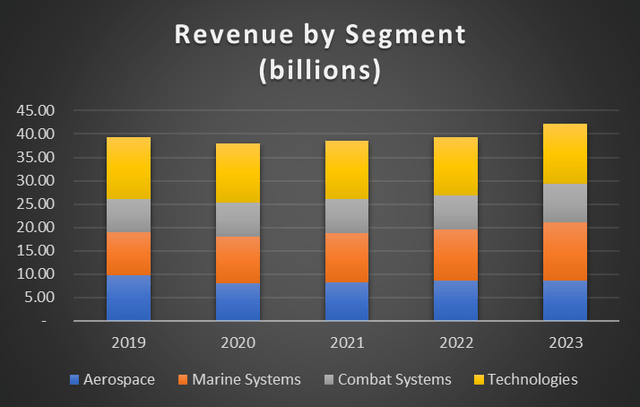

As mentioned above, GD operates four segments, and what I like most about this aspect of the company is all segments have contributed somewhere in the neighborhood of 18 to 34 percent of revenue over the past five years…essentially, no one segment contributes an abundance of revenue compared to the remaining segments; thus, GD is not heavily reliant on one area of the company. The Technologies segment has contributed the most revenue overall but has been trending downward as a percentage of total revenue. In 2019, Technologies contributed 34% of revenue but now contributes just 31% and is also growing at the slowest pace out of all the segments with a CAGR of less than 1% since 2019. The Aerospace portion saw a dramatic drop in revenue during the height of the pandemic, as one would expect; however, it has still yet to return to pre-pandemic levels. The Combat Systems segment has consistently made up about 20% of revenue, which is in line with overall revenue growth, 4.61% to 4.82%, respectively. Lastly, is the Marine Systems portion of the company which has seen the highest CAGR since 2019 at a very impressive 7.7%, including a nearly 13% increase in 2023.

GD’s Annual Reports

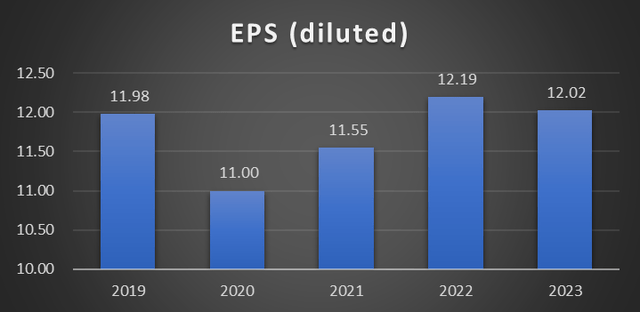

GD’s earnings per share have gone up and down some over the past five years, ultimately resulting in CAGR from 2019 to 2023 of 0.08%. To no one’s surprise the worst year was in 2020 which saw a decrease of about 8%, thanks to the pandemic. Analysts have forecasted 2024 earnings per share to be about $14.50 per share, which would clearly be the best year in a while for General Dynamics and would result in an increase of more than 20%.

GD’s Annual Reports

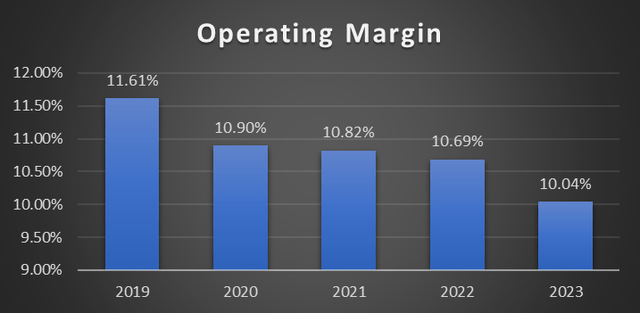

The last financial metric I want to discuss is the operating margin, which has been unfortunately been trending downward every year since 2019. In 2019, the operating margin was 11.61% and dropped about 6% in 2020 to 10.90%; however, in the most recent fiscal year this metric is just barely above 10%. Thankfully, in the company’s 2023 4th quarter earnings call Phebe Novakovic, Chairman and CEO, gave some 2024 guidance and stated, “We anticipate operating margin of 11% up 100 basis points from 2023.” This should provide shareholders with some confidence as the company sees demand for its products and has plans to return its operating margin to pre-pandemic levels.

GD’s Annual Reports

The Dividend

General Dynamics has been paying a dividend for more than 30 years and currently yields near 2%. The company’s 3-, 5-, and 10-years CAGRs are all above 6%, which makes the 7.6% increase announced earlier this year in March a decent surprise for shareholders. GD has maintained a modest payout ratio over the past five years, between 35 and 45 percent. While the payout ratio has been trending upward, I believe there is still a good amount of room for the company to increase their dividend.

Valuation

To determine if a stock is possibly over or undervalued, I employ two methods. The first is dividend yield theory, which is based on the premise that if the current yield is higher than the historical yield, the company is undervalued and vice versa if the yield is lower. The other, more common method is the price to earnings ratio, which is calculated by dividing the current price by the earnings per share for the prior twelve months. While neither is an exact science, they are time efficient ways to determine if a company is worthy of further research.

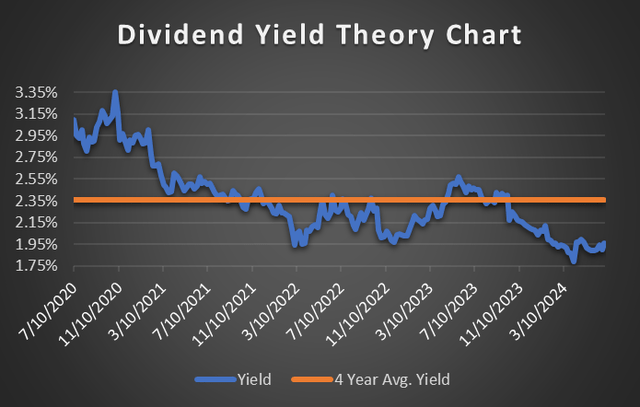

As with many companies during the pandemic, GD’s yield reached a ten-year high, reaching nearly 4%, just prior to my chart starting below. Following the height of the pandemic, the yield dropped some but continued to linger around the 3% mark until early in 2021. For about the next year, the yield didn’t stray far from its 4-year average of 2.35%. In February 2022, the yield began to drop and even dipped below 2% for a short time before rebounding back to its average. Since then and up until late last year, GD’s yield hadn’t changed much, only drifting slightly above and below its average. However, in November 2023, the yield began to plummet and reached a chart low of 1.79% in April, it has since increased, but only slightly. With all that said, using dividend yield theory, General Dynamics is moderately overvalued right now as the yield is about 16% below its 2.35% chart average.

Author created using data from Zacks.com

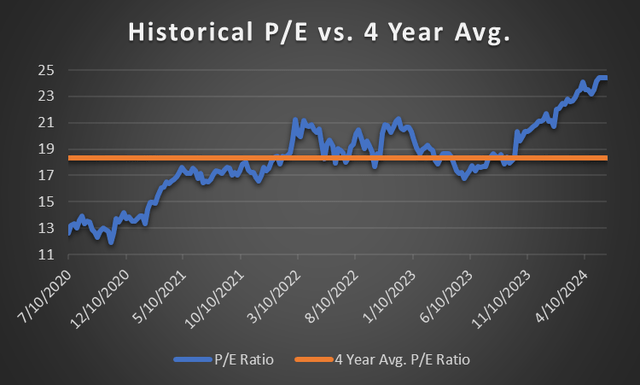

The price to earnings ratio was clearly at a low point coming out of the pandemic, before meaningfully rising in March and April of 2021. For the next few years, the p/e ratio remained relatively flat, with a few bumps throughout 2022 before declining to near its chart average of 18.3. Late last year, the p/e ratio started to rise and has continued to do so, reaching a new high almost weekly. Analysts are estimating 2024 earnings of about $14.50 per share, using that combined with the company’s 4-year average of 18.3 we reach an approximate price of $266, about 5% below its current price of $280.

Author created using data from Zacks.com

Risks

As with basically all military contractors, you are relying heavily on one customer, the US government, to approve defense budgets. Typically, this is not an issue, especially with some of the geopolitical turmoil that is occurring worldwide; however, I could potentially see this becoming an issue given this is an election year and other topics may take priority.

Additionally, military contractors also rely heavily on suppliers to deliver materials and components. A disruption in the delivery of these items could lead to delayed production of products, and thus GD unable to recognize revenue when they had originally planned. Along those same lines, GD must continually innovate products in order to win future contracts with the government. In order to innovate, GD must hire and retain skilled labor, that, in addition to employees gaining, and maintaining, proper security clearances to work on specialized projects are all important aspects of GD’s continued success.

Final Thoughts

Overall, the company has been growing revenue and earnings per share, albeit the latter has been inconsistent but on an upward trend, nonetheless. GD has some work to do regarding its operating margin, but management appears to be aware of the negative trend and expects a 100-basis point increase in 2024. The company offers a safe and growing dividend with a moderately-attractive 2% yield that is well covered. Its only knock, for me, is the valuation which appears to be slightly overvalued; thus I am rating the company a hold and would like to see a reasonable pullback before adding General Dynamics to my portfolio.

Read the full article here