When a management is cautious in making claims about a better year ahead despite a healthy balance sheet, we take it as a positive sign that a bottom in the stock price is lurking around the corner. Huntsman Corporation (NYSE:HUN) is one of those companies that may seem to be performing poorly on the surface, but in our view has a good return potential as a cyclical stock.

A Diversified Product Portfolio

The company’s products are used by a variety of industries as raw material, which is probably why the sales decline has somehow stabilized at current levels, and we believe the trend will continue at least for some time. Its products are used in a range of industries, listed as follows;

adhesives, aerospace, automotive, construction products, durable and non-durable consumer products, electronics, insulation, packaging, coatings and construction, power generation, and refining; elastomers, insulation, footwear, furniture, industrial, oil and gas, liquid natural gas transport, printed circuit boards, consumer, appliances, electrical power transmission and distribution, recreational sports equipment, and medical appliances markets.

The product mix catering to both the consumer discretionary as well as non-discretionary sectors helps ensure the demand is stable during a tougher macro-environment, with an upside when the economy picks up again.

A Secular Decline in Revenue Since 2014

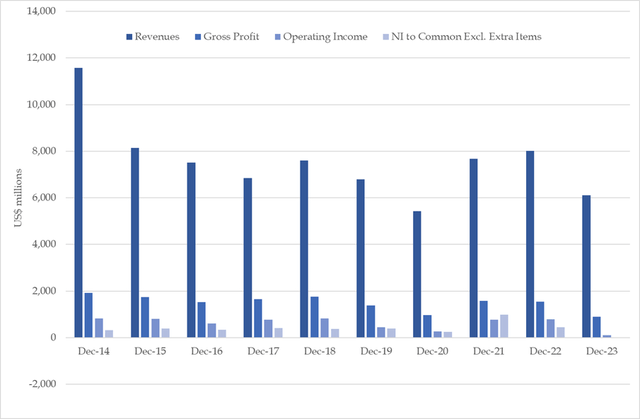

Although Huntsman has a relatively stable capex and inorganic growth program, the sales have consistently declined over the last decade. The machinery value on the balance sheet has stagnated around current levels and the number of full-time employees has come down by nearly 63% to 6,000 from 16,000 in 2014. The revenues in 2014 reached US$11.58bn and seem to have bottomed out at US$5.4bn during 2020 despite the fact that the company spent an average 1.8% of annual revenues in R&D, US$340m in average annual capex and also made a few relatively small acquisitions. These initiatives have not helped in arresting the secular decline, and barring the Covid related growth during 2021-22, the downward spiral has returned recently, and it is indeed a cause of some concern.

It’s clear that the business is affected by the systemic cyclical turbulence, and it is difficult to call the exact trough especially as the economic growth is still strong. One may even argue that there could be more downside than upside potential, with the potential soft landing which has been anticipated for such a long time now.

Management Outlook

During the earnings call for 1Q’2024 earnings, the management was careful in making any claims on having reached a cyclical trough. All the remarks on any performance improvement were laced with a caution about the sustainability of the uptrend. It was good to see better numbers and the company appeared to be treading water carefully, with a particular remark on their approach in the future. “We will not jeopardize our investment-grade rating for short-term gains.”

Let’s look at the comments made by the management during earnings call for the 4Q’2023 and 1Q’2024.

- to recover lost volumes – make some modest gains while expecting more throughout 2024, but concerns remain over the sustainability of such gains

- need to improve cashflows – seeing improvements in this area as well, but it may face headwinds in working capital later with sales volume and pricing picking up

- focus on the costs in the face of global inflationary and regulatory pressures

- continuously assess the portfolio, make sure the value of the assets the company owns is maximized and how the capital is deployed for growth. The EBITDA or Interest coverage requirements might make them sell some of the assets. It is likely and should not be ruled out, but one would definitely question the rationale to sell at a discounted price.

- focus on the environmental and safety performance – it is comforting to know that the management seems to believe in the long-term vision and not compromising on that for short-term gains.

Another interesting comment made by the management on the growth in the EV space and company’s position as it is affected.

As we think about EVs, we essentially supply everything that goes into an ICE vehicle goes into an EV vehicle in our polyurethanes division, which is our largest division with automobile applications. But we also have a number of applications that we’re developing right now that are in the pipeline, some of them that are merging into EVs that are coming from the other divisions as well, around structure, strength, light-weighting, adhesion, insulation, and so forth.

There is some merit to their comments around growth in EV volumes from China and its positive impact on the polyurethanes volumes, but it is better not to pre-maturely assume a bullish outlook until we see some improvement in the pricing power. The company is expecting approx. US$150-200m in additional EBITDA to be unlocked based on the above, but the proof of the pudding is in the eating. Therefore, we would like to first see some solid sales volume growth without a compromise on pricing.

Having said that, we are optimistic about the company’s prospects in the long run on account of the commercial scale Miralon project (construction to begin in 2025-26), MDI splitter in Geismar, amines expansion, and urethane catalyst expansions. Most importantly, any reduction in mortgage rates should spur housing starts, which should help the current volumetric growth in North America last longer.

Financial Performance & Valuation

If we look at the current cycle post-covid, there is a persistent decline in revenues and EBITDA across all the business segments, but the encouraging part was the uptick in North American sales volumes in the recent quarter. Although it is not ideal to see the corresponding negative impact on prices as it was quite sizable for the volume growth achieved. The company faced similar kinds of margin headwinds during the year 2023 and if the current trend continues, there is a strong possibility that the annual results in 2024 could push the stock price lower towards better accumulation levels.

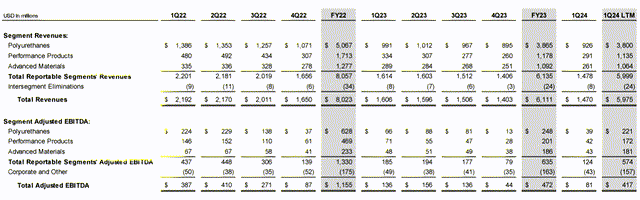

Huntsman Corporation – 1Q’24 Earnings

The interesting part here though is that between 2014 and 2022, the revenues declined by 31%, but the gross profits were down by only 20% with a 270bps improvement in gross margin. We believe any improvement in the macro environment would help lift the EPS from continuing operations back to the long-term trend, as the company’s balance sheet seems quite healthy even during the current stress on the P&L side.

Seeking Alpha Seeking Alpha – Analyst Calculations

Seeking Alpha – Analyst Calculations

Based on the cautious management outlook on the margin improvement for the rest of the year, we may see a better price zone for accumulation (if not already there). As you can see from the table above, the company’s profit margins tend to move in a cycle and for such a company, it would be important to consider a cross cycle performance to arrive at a reasonable valuation range.

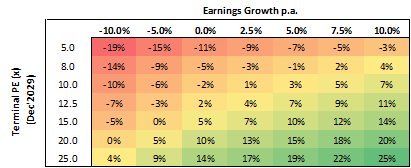

We took an average of the last 10 years EPS and ran sensitivity analysis on the expected annual returns, based on various earnings growth rates and the terminal P/E multiples using the close price ($21.46) on July 9, 2024. As it is clear from the table below, it would take a really good earnings performance for the next 5 years and higher than average P/E multiple for a solid out-performance on returns.

Analyst Calculations

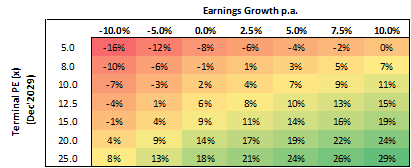

We ran another sensitivity analysis using the same factors but the only change being a lower stock buy price (e.g. $18), which results in the following sensitivity table. As you can see, at $18 as the purchase price, the required earnings growth and the terminal P/E multiple are lowered significantly for a much better return profile. To add some relevant context to the discussion, the historical 5Y average FWD P/E multiple for Huntsman has been 14.87x.

Analyst Calculations

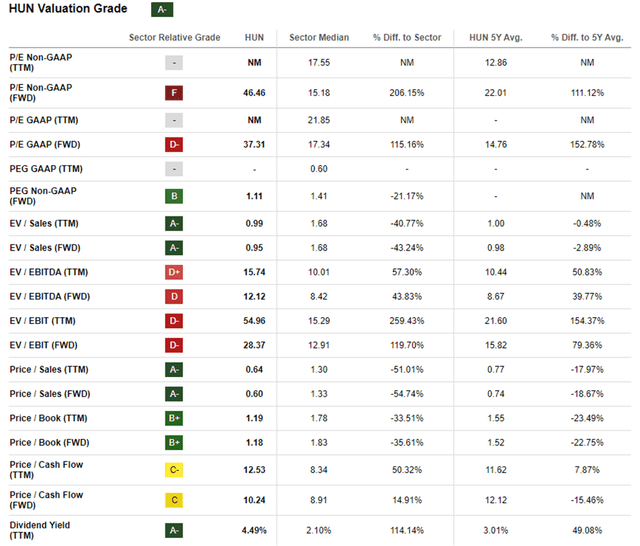

When you consider the Huntsman’s valuation ratings, it is obvious that the company is already cheap on the basis of dividend yield and P/B multiple. The other multiples such P/E and EV/EBITDA could also come within historical range in case of any further downtrend in the stock price, and profitability improvement with a cyclical upturn in the inventory buildup and subsequently higher product pricing.

Seeking Alpha

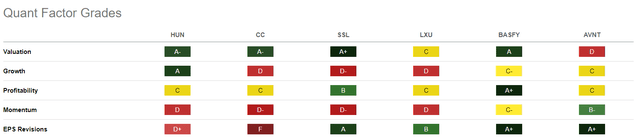

This is further confirmed by the quant ratings on a comparative basis as shown below. If the profitability starts picking up, the momentum and EPS revisions would likely be upgraded as well, but it is very likely that the stock price would have bottomed out long before that in our view.

Seeking Alpha

Downside Risks

We have based our positive outlook on the key assumption of a soft landing and quicker recovery in aggregate demand. Despite a decently growing US economy, the company is facing challenges in raising their product prices, which is not very encouraging. If this depressed market condition is prevalent for a longer period, the inflection in stock price could take longer and the trend might be choppier than preferred. In addition, the production volumes might be adversely affected on account of unexpected plant closures, higher trade barriers and tariff among other factors.

Conclusion

We are positive about the company’s prospects in the long term based on business fundamentals and decent enough levered free cash flow. If there is a further deterioration in profitability due to margin pressures in the next 12 months, there could be some downward movement in the stock price and that should be taken as an opportunity to accumulate the stock, provided the long-term business fundamentals are intact, and the balance sheet is still strong.

Read the full article here