Shares of Phillips 66 (NYSE:PSX) have been a strong performer over the past year, rising by about one-third, but performance has been materially weaker of late with PSX down by about 23% since the beginning of April as concerns have intensified around the direction of the refining cycle. Given concerns about relative valuation, I downgraded shares to a “hold” in April. While I was right to downgrade them, I did not move sharply enough as the stock has fallen by 22% since that analysis, lagging the market’s 7% gain by a significant margin. Given this decline, now is a good time to ask if PSX shares are cheap enough to buy or if there is a larger problem with the company’s fundamentals.

Seeking Alpha

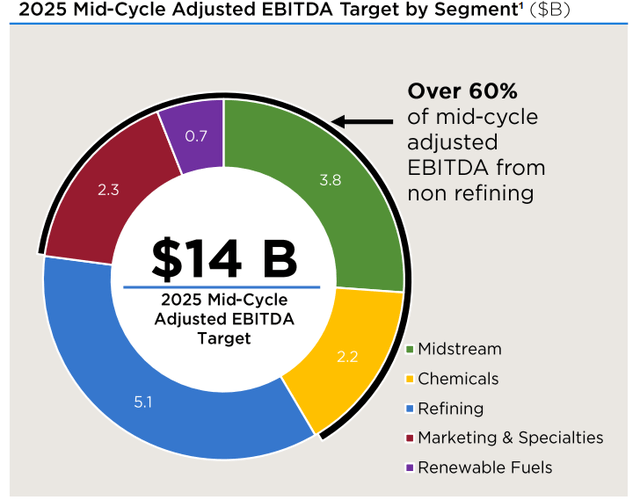

There are three large independent US refiners, Phillips 66, Valero (VLO), and Marathon (MPC). Of the three, PSX is the most diversified company in my view, given its wholly-owned midstream assets and JV ownership of a chemical business. Indeed, on a mid-cycle basis, PSX aims to generate the majority of its EBITDA away from refining. Growth cap-ex and M&A activity has also been focused away from refining to increase this diversification.

Phillips 66

Now more recently, refining has been generating a disproportionate share of earnings. That is because refining profits last year were better than “mid-cycle” as tight markets in the wake of Russia’s invasion of Ukraine led to wide crack spreads, leading to excess profits. At the same time, the Chemical business has been very weak due to limited demand from China’s construction sector, leading it to under-earn vs its 2025 target.

Still given this diversification, I do think PSX should generally have less volatility to crack spread than MPC or VLO over the long-term. In the near term, refining tends to drive incremental profits or losses, given crack spreads are more volatile. 80% of midstream revenue is fee-based for instance, though there is volume risk, which means earnings should move less quarter to quarter.

This sensitivity to crack spreads in the short term explains much of PSX’s weakness over the past three months. As you can see below, crack spreads have narrowed considerably over the past three months, which has weighed on refining sentiment. Speaking at a conference in June, PSX noted crack spread developments have been disappointing to many. It saw product demand sluggish through May, blaming it on weakness among lower-income consumers. Indeed, it has seen some refinery run cuts in Asia and Europe that have higher cost crude, which could help mitigate extra supply.

Energy Stock Channel

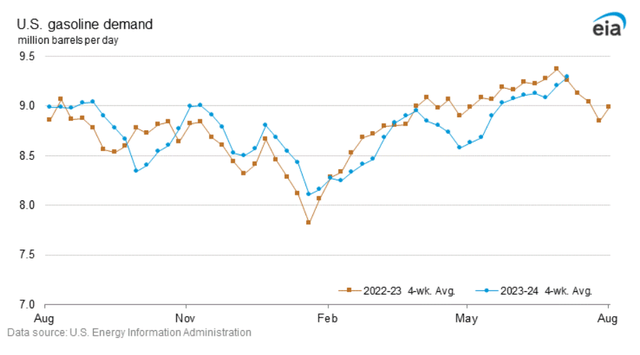

Now, in the near term, I am more optimistic on crack spreads. PSX was right that demand had been disappointing. However, after the latest EIA report, I am increasingly confident that this weakness was transitory and not a rolling over by consumers. As you can see below, in April/May, gasoline demand was running about 3-4% below 2023 levels. However after this past week, we have rallied back to 2023 levels.

EIA

Much of the West Coast had unfavorable weather earlier this year, which may have reduced driving. We are also seeing record TSA activity, which should support jet fuel demand. This year’s summer driving season had a slow start, driving crack spreads (the differential between crude and gasoline/diesel pricing) lower, but the demand picture is appearing brighter. Moreover, with the Federal Reserve appearing set to begin cutting rates in September, my confidence in a soft economic landing, which supports product demand, is rising.

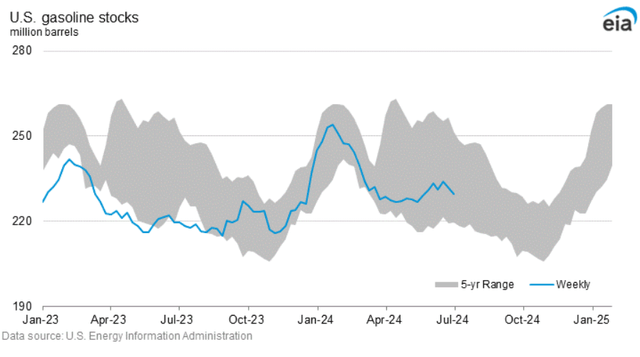

When product demand was running surprisingly weak, we saw gasoline inventories rise a bit, which is unusual for this time of year, though they remain at a relatively low level. Encouragingly, they did drop this past week. While each week can be volatile, it will be important to see gradual declines over the next two months to validate my view crack spreads are bottoming.

EIA

Tactically, I would also add that as Goldman Sachs (GS) noted, meteorologists expect this year to be a particularly active Hurricane Season. Indeed while Hurricane Beryl did not impact energy infrastructure, a storm of that strength this early in the season is unusual. Given the fact that the Gulf Coast is the center of the US refining industry, an active hurricane season may cause supply-side disruptions that reduce product inventories and raise crack spreads.

Just as lower crack spreads have weighed on PSX stock, a rebound should help put a floor under the stock, and wider spreads will be helpful after a mixed Q1 performance. In the company’s first quarter, Phillips 66 earned $1.90, and it generated $1.2 billion of operating cash flow, excluding working capital. Still, operating results left room for improvement.

Sticking with refining first, refining income declined to $228 million from $797 million in Q4, weighed down by inventory hedging. It captured just 69% of the market. Refining was down even more dramatically from $1.6 billion a year ago when margins were unsustainably high from diesel shortages.

While large declines were to be expected, its Q1 performance was disappointing. That was because its refining margin of $10.91 was down from $14.41 in Q4. Crack spreads were $15.77. It targets 75% capture (which is not an overly aggressive target), so this underperformance cost about $120 million. In Q2, crack spreads are wider than Q1, even as they have come in recently, and utilization should be 2-3% higher due to less turnaround activity. As such, we should see earnings rebound materially, likely well past $500 million.

Midstream operating income fell by $141 million to $613 million last quarter due to weakness in its NGL business due to lower volumes and weaker margins. Winter storms disrupted production, and while it earns a fee, there is some sensitivity to NGL pricing, which has been weak. With a better production environment, we should see some improvement here. This unit has also seen PSX work to optimize its asset base.

It previously brought DCP in-house, adding $1 billion of EBITDA. It aimed for $300 million of synergies, but it now expects to pass $400 million, a positive development. Recently, PSX sold its 25% stake in the Rex Pipeline for 10.2x EBITDA or a $1.3 billion valuation, as part of its $3 billion asset sale target. Rex has had a difficult operating history as it was not originally positioned for higher Eastern natural gas production (as we have seen from the Marcellus Shale), and I view this valuation as attractive. At the same time, it is spending $550 million on a tuck-in natural gas G&P business, Pinnacle Midland, which should provide cost synergies with its existing asset base.

Finally, Chemicals operating income nearly doubled sequentially to $205 million. This unit is comprised of PSX’s ownership stake in CP Chem. This was up a more modest 4% from last year. The commodity petrochemical business has been very difficult over the past two years, as China is the marginal consumer of these products. The significant slowdown in its real estate market amid developer bankruptcies has caused significant headwinds. In fact in 2023, Chemicals EBITDA was just $1.1 billion, half of its $2.2 billion “mid-cycle” target.

Fortunately, we are seeing signs that this is improving. CPChem has low-cost ethane feedstock in the US & Middle East while European producers have had to ration production given low ethylene pricing. European rationing has helped to normalize the market. While there is still too much inventory, prices have inched up to $0.175 per pound in Q2 from $0.165 in Q1 after falling below a dime last year.

Given uncertainty around Chinese demand, I do not expect a significant rebound from this unit, but we should see better results in 2024 than in 2023. Over the years, CPChem has been a powerful source of cash for PSX. However, distributions were small in 2022, and given market weakness, there were none in 2023. I do not see scope for a large distribution this year, but we may see some cash sent to PSX.

Phillips 66

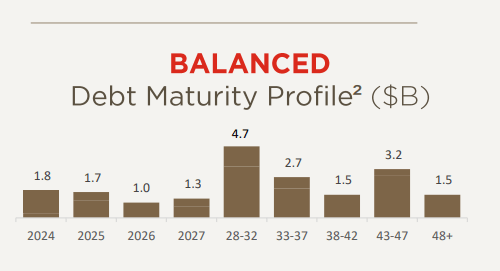

PSX also carries $1.6 billion of cash and $20.2 billion of debt. That leaves it with 38% debt-to-capital vs its 25-30% debt to capital target. 3-4% of this is due to a higher working capital balance, which should run down, and PSX has healthy cash flow. However, I expect it to use some asset sale proceeds to de-leverage by paying off some maturing debt. Overall, its debt maturity profile is well staggered, which limits interest rate risk.

Phillips 66

PSX does pay a $1.15 dividend, which it raised 10% last quarter, giving shares a 3.5% yield. Its share count is also down about 7.5% over the past year thanks to repurchases. With refining profits having fallen, I expect the pace of share count reduction to slow.

Overall, PSX is not a company I would describe as “firing on all cylinders.” Indeed, by being so diverse, it rarely will be as not all of its markets move in sync. Of course, this also means it is unlikely all of its units face significant pressure at the same time, muting both the upside and downside to results. Still, I do expect to see results improve sequentially. And if my view crack spreads are bottoming holds, that improvement should persist beyond Q2.

With $2.2 billion in cap-ex, PSX should generate at least $5.8-6.4 billion in free cash flow this year, given my view on crack spreads. If it achieves its 2025 targets, its mid-cycle free cash flow capacity will be about $7.5 billion. This leaves PSX well positioned to continue returning about $5 billion/year to shareholders while gradually retaining cash flow to pay down debt.

This gives shares an 11% 2024 free cash flow yield, and if we eventually see chemicals return to paying material distributions in 2025, that free cash flow yield will rise substantially. Now, PSX is trading at a premium to MPC, which has a 16% capital return yield and stronger cash position, reflecting its CPChem stake and diversification.

I have rated MPC a strong buy given my conviction in the durability of the refining cycle. As you can see below, while they have fallen, crack spreads are wider than pre-COVID. My view has been this will likely persist because there is limited incremental refining capacity with it almost impossible to see new refineries built in the developed world. With this outlook, I view companies like MPC with more direct refining exposure and a cheaper valuation most attractive.

Energy Stock Channel

That said, I view PSX now as attractive given a double-digit free cash flow yield and tentative signs that chemicals can improve this year. Ultimately, PSX will be exposed to the economic cycle. A recession would reduce product demand and crack spreads. A rollover in China would reduce chemical pricing, though this segment appears to have already passed its bottom. I view those risks as largely in the price.

Given its underperformance and likely sequential improvement, I am raising shares to a buy. With its diverse business and fee-based midstream cash flows, I view a 9-10% free cash flow yield as fair, which can bring shares back toward $150-155 without giving credit to a Chemicals acceleration. While not my preferred refiner, for investors seeking more diversity and a secure dividend, PSX is now attractive with the potential to return nearly 20% barring a recession.

Read the full article here