Investment Thesis

The last time I talked about Delta Air Lines (NYSE: NYSE:DAL), I discussed the company’s FY23 fourth quarter results and argued why a combination of a resurgence in international travel andstrong demand for the airline’s premium products supports its long-term growth story. I had a BUY rating on the stock. Since my article was published in February 2024, the stock has gained 8.45%, underperforming the S&P 500, which gained 13.2% during the same period.

In this article, I dissect the airline’s second-quarter results and argue that despite being the industry leader,and despite the strong demand seen for its premium products, the airline has not been immune to the challenging business conditions that have plagued the industry. As such, cracks have started to appear in its long-term growth story.

Second Quarter Highlights

DAL had an underwhelming quarter, in my opinion, missing out on both the top and bottom-line estimates. While Q2 total revenues of $16.7 billion beat analyst estimates by $953.9 million, adjusted operating revenues, which exclude third-party refinery sales, came in at $15.4 billion, down 1.2% y/y and missed analyst estimates by $300 million. Non-GAAP EPS came in at $2.36, down 12% y/y and missing analyst estimates by $0.02.

Although the company saw its free cash flows growing 16% y/y, this was mostly due to a sharp reduction in capital expenditures, which declined 23% y/y. Operating cash flows saw a decline of 7% y/y. The company also saw its operating margins decline 14% y/y, reaching 14.7%.

The guidance also fell short of analyst estimates. For the third quarter, the company expects revenues to grow between 2 and 4%. Operating margins are expected to come between 11 and 13% and non-GAAP EPS is expected to come between $1.70 and $2.00, falling well short of analyst consensus of $2.05. The airline, however, reiterated its full-year guidance, with non-GAAP EPS projected to come between $6 and $7, and free cash flows expected in the range between $3 billion and $4 billion.

Demand Remains Strong But Lower Airfares & Oversupply of Seats Paint a Different Picture

“Demand for travel on Delta remains robust. Our core customer base is healthy, and demand for premium products continues to outperform the main cabin”

Glen Hauenstein, Delta Air Lines President

One of the common themes throughout DAL’s second-quarter earnings call was management’s argument that demand continued to be strong. Mr. Hauenstein was not bluffing when he made the aforementioned quote, as based on airport passenger data, the summer season is set to be the busiest ever. This was evident when last Sunday saw daily travellers passing through US airport security cross the 3 million mark for the first time ever. However, this upbeat outlook on demand is being overshadowed by an industry-wide oversupply of seats.

During the earnings call, management highlighted that seat growth accelerated at a faster pace than normal demand growth well into the summer months, which had an impact on main cabin unit revenues. This was further evidenced by the airline’s Total Revenue per Available Seat Mile (TRASM), a proxy for efficiency, declining 2.6% y/y. To make matters worse, fuel expenses jumped 11.9% y/y, which, when combined with lower fare discounting, had an adverse impact on the overall profitability, as evidenced by the 30% y/y decline in net income. The discounts offered also hurt the third-quarter outlook, with the midpoint of Q3 EPS guidance ($1.90) falling well short of analyst expectations of $2.05.

The glut of airline seats, especially at the lower end of the market, is expected to stabilize by August according to the management. This could be one of the reasons why, despite a 30% y/y decline in net income, management reiterated its FY24 EPS guidance. However, this thesis would play out only if low-cost carriers play ball, and dramatically decline their seat capacity. In the fourth quarter of last year, the average capacity per flight had increased by 8%, resulting in 160 seats per flight.

And while premiumization has helped DAL offset some of the headwinds caused by the glut of seats, it does come at the cost of business travel. Although corporate travel demand for DAL grew double-digits during the second quarter, and while a corporate survey showed that 90% of the participants expected their travel volumes to at least stay the same in Q3 and beyond, the presence of videoconferencing continues to cause a headwind for this segment. In inflation-adjusted terms, corporate travel this year would be 13% lower than in 2019, according to the U.S. Travel Association, and is expected to remain flat thereafter. As such, from a profitability perspective, premiumization might not entirely offset the permanent reduction in corporate travel.

In addition to seat oversupply, primarily driven by low-cost carriers, thanks to their “fewer planes, more seats,” strategy, yet another factor that has been preventing the airline industry from catering to the demand is the supply chain issues faced by both Boeing and Airbus. The issues plaguing Boeing have been well-documented. However, despite such an opportune moment to capitalize upon, Airbus was also hit with supply chain issues, subsequently impacting its deliveries. The company mentioned that it would fall short of its delivery target of 800 this year, by 30 units. It is now expected to reach its goal of producing 75 Airbus A320neos a month only in 2027, a year later than its initial projections, as delays at engine manufacturers Pratt & Whitney and CFM International have negatively impacted its delivery timeline.

As one of the biggest customers of Airbus, management argued during the earnings call that DAL would be insulated from Airbus’s woes, with its delivery schedule expected to suffer only weeks and/or months of delay and not years. And while the hit to deliveries would help in alleviating the oversupply of seats, it does lead to another headache for DAL, one related to fuel efficiency.

Given that one of the growth levers of the company is fuel efficiency, any major delays in its plans to renew the fleet would have a material impact on its profitability. Fuel efficiency during the second quarter was 1.1% better y/y, coming in at 14.3 gallons per 1,000 ASMs. On a sequential basis, there was a marginal improvement, as Q1 fuel efficiency stood at 14.2 gallons per 1,000 ASMs. However, the y/y rate of improvement has slowed down (1.1% in Q2 vs 1.9% in Q1). Although DAL’s plans are on track for now, the delay in the arrival of new aircraft would be a major cause for concern for both the airline as well as its investors.

Taken together, the current business conditions along with supplier issues have been a major hit for DAL, although they have not been as bad for the company compared to some of its peers. While the aggressive expansion of capacity would come to an end soon, the inability to tackle higher fuel expenses due to issues with Airbus would continue to be a drag on profitability. Add to it the fact that airline fares in the U.S. declined for the fourth month in a row, down 5.1% y/y in June, and are projected to fall through August. So, while there is robust demand, the levers that DAL can pull to capitalize on the demand remain constrained for now.

Revenue Diversification Helps DAL Avoid a Nightmare Quarter

One of the bright spots of DAL’s second quarter was the revenue growth seen in its other segments. In my opinion, if it weren’t for these segments, the quarter would have been far worse. Premium, loyalty, and other diversified revenue streams accounted for 56% of the company’s total revenue.

DAL’s “premiumization,” strategy has been a major success, and this quarter was no different. Revenues from this segment jumped 10% y/y with positive unit revenue growth. Load factors were in the mid-to-high 80s and fare structures for the Premium Select were more than double that of the economy segment, which provided a boost to the company’s revenues and margins. The airline’s plans to launch free Wi-Fi in the Premium cabins on all of its international flights by the end of the summer suggests that the company continues to see strong demand in the segment. The tickets for the premium segment also continue to sell faster than the main cabin, which suggests that consumers continue to show a preference for extra features and comfort. However, the next challenge would be for the airline to see how to grow Premium to a level where the permanent reduction in corporate travel can be offset.

The airline’s loyalty program also continues to show impressive growth. Q2 saw the segment’s growth at 8% y/y, and nearly 30% of the airline’s active SkyMiles members opted for the Delta SkyMiles AmEx credit card. Remuneration from American Express was $1.9 billion, registering a growth of 9% y/y. Finally, the cargo segment also registered strong growth, jumping 16% y/y.

The revenue diversification helped DAL weather the storm to a certain extent. It also explains why the company stands out from some of its competitors, who have been hit with the challenging business conditions a lot harder.

Valuation

|

Forward P/E Approach |

|

|

Price Target |

$42.00 |

|

Projected Forward P/E Multiple |

6.5x |

|

Projected FY24 EPS |

$6 |

|

Forward PEG Ratio |

0.83 |

|

FY25 Earnings Growth |

7.8% |

|

Projected FY25 EPS |

$6.47 |

Source: DAL’s Q2 FY23 Earnings Release, LSEG Data (formerly Refinitiv), Seeking Alpha, and Author’s Calculations

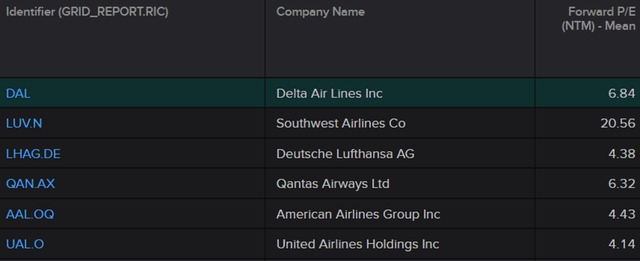

DAL, according to LSEG Data (formerly Refinitiv) currently trades at a forward P/E of 6.8x, slightly below the industry median of 6.95x, but above some of its peers such as American Airlines and United Airlines. The airline is also trading cheaply relative to its historical multiples of 7.4x (5-year historical median) and 8.2x (10-year historical median). Despite the strong demand cited by management during the earnings call, the question of efficiency remains. In addition, with airline fares coming down, and competitors, especially the low cost carriers bringing their own versions of “premiumization,” the environment remains challenging even for a market leader like DAL. As such, I have assumed a forward P/E of 6.5x for my calculations, which is the company’s historical 2-year median forward P/E multiple, slightly lower than my previous estimate of 6.7x.

LSEG Data (formerly Refinitiv)

As mentioned earlier, management reiterated the FY24 EPS guidance, which is projected to come in between $6 and $7. Given the challenges that I described above, I have adopted a conservative approach and have assumed FY24 EPS to come in at $6, the lower end of the guidance range, and below my previous estimate of $6.5.

According to Seeking Alpha, the company’s PEG ratio stands at 0.83, well below the industry median of 1.68. At a forward PEG ratio of 0.83 and a forward P/E multiple of 6.5x, we would get an earnings growth rate of 7.8%, which is a reasonable estimate in my opinion, since it is not far from its mean long-term growth rate of 9.6%. The lower estimate also appropriately factors in the challenging macroenvironment and the capacity constraints that the airline has to deal with at present. At an earnings growth of 7.8%, the FY25 EPS is projected to come in at $6.47.

A forward P/E multiple of 6.5x and an FY25 EPS of $6.47 would yield a price target of $42, which represents a 6.6% downside from current levels. While I don’t recommend shorting the stock at these levels, I believe that profit-taking at these levels would be a good idea. For new investors, in my opinion, it is best to avoid the stock at current levels. Overall, I am downgrading the stock to a HOLD.

Risk Factors

In addition to the challenges that I have outlined in this article, there are also the risk factors, that I mentioned last time, such as the geopolitical risks. Although these risks have stabilized, they have not completely abated, and as such, their impact on DAL’s fuel costs has to be considered.

Finally, while transatlantic travel continues to grow, the Eurozone region, especially France and Germany continues to remain weak. In addition, there is political instability in regions such as France, which could harm transatlantic travel, especially after the Paris Olympics. And while there is strong demand for travel to Japan, as a result of the weakness seen in the Japanese Yen, there are reports that Japan’s $1.5 trillion Government Pension Investment Fund, during its once-every-five-years review, could redirect some of its dollar-denominated assets to yen assets, which has the potential to prop up the yen. This could cut short the surge in travel demand seen in Japan.

Concluding Thoughts

DAL had a dismal second quarter, despite registering record revenues. Challenging business conditions, driven by an oversupply of seats have hit the airline hard, despite the strong demand that continues to exist for air travel. Higher fuel expenses also had a negative impact on the airline’s profits, which led to a subpar second quarter as well as a subpar third-quarter guidance.

The only bright spot was that premiumization continues to be a hit among consumers, and this, combined with loyalty and cargo, prevented the quarter from being worse. There was a lot of optimism from the management, especially about the deceleration in seat growth. However, it is far from certain that stability in the seat growth would help the company’s fortunes in the near term. The delivery issues facing Airbus also call into question the timeline of DAL’s fleet revamp, which subsequently could have an adverse impact on its ability to be fuel efficient.

DAL continues to be an industry leader and the challenging business conditions probably had the least effect on the airline relative to its peers. However, that does not mean that you buy into this stock, especially at current levels. In my last article on DAL, I talked about how airline stocks are trading vehicles rather than long-term investments. And while I suggested then that DAL belongs to the latter category, I no longer believe that to be the case, at least in today’s environment.

Read the full article here