We previously covered ZIM Integrated Shipping (NYSE:ZIM) in April 2024, discussing its uncertain prospects in FY2024, with the management’s underwhelming guidance pointing to an uncertain dividend payout in the near-term.

At the same time, with the Red Sea conflict already triggering elevated freight spot rates – well balancing the container ship company’s higher lease obligations and the longer transit through the Cape of Good Hope absorbing part of the capacity over-supply, we did not expect the company to go into significant cash flow/ debt issues in 2024.

Since then, ZIM has further rallied by +49%, well outperforming the wider market at +9%, as the spot prices continue to rise and the company offers decent FQ1’24 dividends while raising the FY2024 guidance.

Even so, we do not recommend anyone to chase the stock here, with the stock’s flattish movement since May 2024 implying a fully baked in upside potential, with the forward dividend yields also not rich enough to justify buying the stock at current inflated levels.

ZIM Has Been Volatile & Will Likely Remain So In The Intermediate Term

ZIM’s 3Y Stock Prices

Trading View

For the uninitiated, ZIM is a container ship company that has had a volatile past five years, attributed to the uncertain COVID-19 pandemic in 2020, the subsequent global supply chain issues, the normalization post pandemic, and currently, the ongoing geopolitical events in the Red Sea.

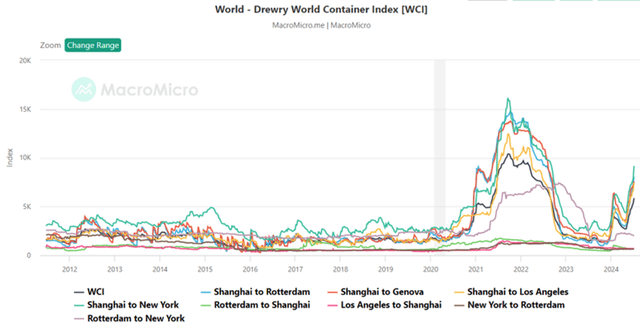

Drewry’s World Container Index

Macro Micro

With the Drewry’s World Container Index [DWCI] tracking the freight costs of 40-foot container via eight major routes, including spot rates and short-term contract rates, it is undeniable that ZIM’s prospects are closely tied to the rather volatile rates as observed in the above chart over the past five years.

For reference, ZIM recognized an average freight rate per TEU of $1,009 (+3.7% YoY) and adj net incomes of $12M in FY2019 (+126.9% YoY), when the average spot rates were at $1,530.

During the heights of the pandemic, the container company reported an average freight rate per TEU of $3,240 (+16% YoY) and net incomes of $4.63B in FY2022 (inline YoY), with spot rates at $6,220.

By FY2023, ZIM’s freight rates have normalized drastically to $1,203 (-63% YoY) with it triggering impacted net incomes of -$0.62B (-113% YoY), as spot rates also decline to $1,660.

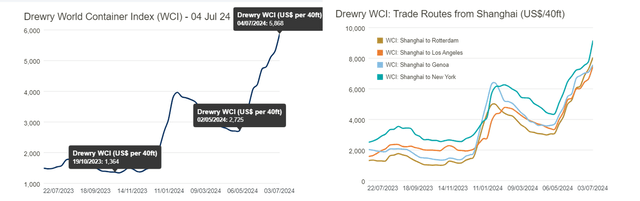

Drewry’s World Container Index

Drewry’s World Container Index

As discussed in our previous article, we had hypothesized that the ongoing Red Sea conflict and subsequent fleet diversion through the Cape of Good Hope might potentially trigger near-term tailwinds for ZIM, based on the rising spot rates from $1,364 on October 19, 2023 (prior to the Red Sea attacks) to $2,725 on May 02, 2024.

This conjecture has materialized after all, with ZIM reporting excellent freight rates of $1,452 (+31.7% QoQ/ +4% YoY) and net incomes of $92.1M in FQ1’24 (+162.8% QoQ/ +258.5% YoY).

Based on the established dividend policy at 30% of net income usually paid out as dividends between Q1 and Q3, it is also unsurprising that the management has paid out $28M in dividends (NA QoQ/ NA YoY), or the equivalent of $0.23 per share in FQ1’24 (NA QoQ/ NA YoY).

At the same time, readers must note that the spot rates have further risen to $5,868 by July 04, 2024, building upon the average Q2 spot rates of $3,670, implying that ZIM’s upcoming FQ2’24 earnings call expected on August 14, 2024 is likely to exceed expectations with another prospective dividend paid out.

The same optimism has also been shared by the management in the FQ1’24 earnings call, with the FY2024 adj EBIT guidance raised to $200M at the midpoint (+147.3% YoY), up from the original guidance of breakeven (+100% YoY).

With the “freight rates to remain stronger for longer than initially anticipated due to a combination of continued pressure on supply and availability of equipment and a recent uptick in demand,” we believe that the ZIM stock remains well supported at these heights, with the market likely hopeful for another rich FQ2’24 payout.

Higher Spot Rates May Not Last, However

Even so, we must highlight that ZIM has received 30 newbuild vessels thus far, with another 16 new deliveries expected through 2024.

With the container ship supply growth still expected to exceed demand growth in 2024, it is unsurprising that we have seen its balance sheet impacted as the lease liabilities grew to $3.71B (+14% QoQ/ +24% YoY) and cash/ equivalents declined to $687.9M (-26.3% QoQ/ -64.1% YoY) in FQ1’24.

As a result of the over supply, we may see ZIM report a deteriorating balance sheet through H2’24 as the management continues to execute its fleet renewal, with it likely to trigger a higher net finance expenses (interest expenses) up from the annualized sum of $281.2M reported in FQ1’24 (+38.3% YoY).

At the same time, ZIM continues to offer a pessimistic commentary on “a more challenging second half of this year irrespective of the duration of the Red Sea crisis as more newbuilds, particularly large capacity vessels are delivered.”

This well negates Maersk’s (OTCPK:AMKBY) optimistic commentary with “the Red Sea disruptions … likely to remain well into the second half of the year, which together with strong container market demand will support stronger rates and volumes.”

As highlighted by the ZIM management in the FQ1’24 earnings call, readers must also monitor the ongoing development in container spot rates and supply/ demand balance, since it remains to be seen if the “stress in the global supply chain” may last.

As a result, readers may want to monitor ZIM’s and Maersk’s commentaries in the upcoming FQ2’24 earning calls, especially since the macroeconomic outlook remains uncertain, worsened by the “low unemployment and high inflation.”

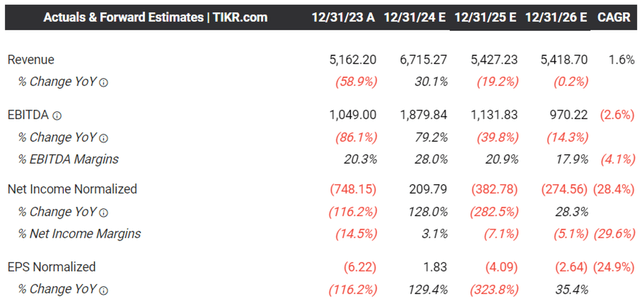

The Consensus Forward Estimates

Tikr Terminal

As a result of the mixed prospects, it is unsurprising that the consensus continues to remain cautious as observed in the relatively stable forward estimates, with ZIM expected to report a brief profitability respite in FY2024, before reverting to the red through FY2026.

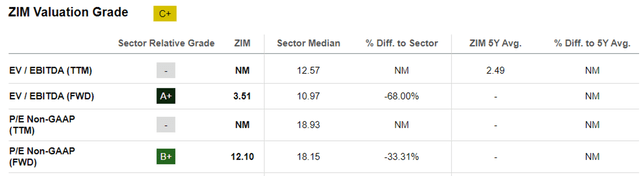

ZIM Valuations

Seeking Alpha

And it is for this reason that we believe ZIM is expensive here, with the FWD EV/ EBITDA valuations of 3.51x more expensive than its 4Y average of 2.49x.

Even when compared to its direct container company peer, Maersk at 3.02x with projected profitability through FY2025, we believe it is apparent that ZIM’s current valuations do not offer a margin of safety.

So, Is ZIM Stock A Buy, Sell, or Hold?

ZIM 2Y Stock Price

Trading View

With ZIM already failing to break out of its recent heights while returning to its three month trading ranges of between the $18s and $24s, it seems apparent that the market remains uncertain about its intermediate term prospects despite the rising spot rates.

With an uncertain H2’24, we believe that the market’s reaction remains reasonable for now, especially since ZIM continues “to assume that the second half of ’24 might be weaker than the first half,” despite the management shifting part of its next twelve months contracted prices to spot prices from a ratio of 50/50 to 35/65, respectively.

Anyone looking to time the market and the ongoing Red Sea events must also be very careful, especially since the ZIM stock has well outperformed at +86.5% on a YTD basis, compared to the wider market at +17.6% and Maersk at -6.1%.

Assuming another $0.23 (if not more) in FQ2’24 payouts, we are also looking at a base case forward dividend yield of 4.7%, nearing the US Treasury Yields of between 4.24% to 5.37%, though lower than other high yield dividend stocks, such as those offered in the tobacco or telecom or mREIT industries.

Combined with the elevated short interest of 11.1% at the time of writing, we believe that it may be more prudent to maintain our Hold rating for the ZIM stock.

Naturally, those whom have continued holding on since the pandemic may continue to enjoy the variable dividends. This is especially since the rich payouts since the heights of 2021 have compensated investors for the inherent volatility of commodity-linked stocks, such as ZIM.

Read the full article here