CRSP’s Gene Editing Technology Has Finally Been Approved

CRSP’s Gene Editing Technology

CRSP

CRISPR Therapeutics AG (NASDAQ:CRSP) is a biotech company specializing in genetic editing technology, namely the Clustered Regularly Interspaced Short Palindromic Repeats [CRISPR]-associated protein 9, CRISPR-Cas9, allowing the precise alteration of specific sequences of genomic DNA.

CRSP Pipeline

CRSP

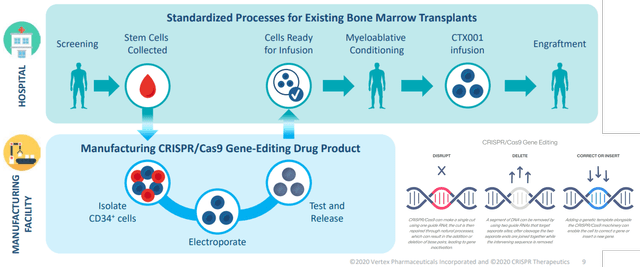

CRSP’s Casgevy has already received the US FDA approval in January 2024 and the EU EC in February 2024, for the treatment of Severe Sickle Cell Disease and Thalassemia – both in partnership with Vertex Pharmaceuticals Incorporated (VRTX).

With a Severe Sickle Cell Disease market size of $12.38B by 2032 and Thalassemia market size of $4.2B by 2031, the biotech’s prospects are more than decent indeed, as the regulatory approval brings the previously pre-revenue company in 2023 to a new promising phase in 2024.

This also builds upon CRSP’s relatively robust pipeline, with five other therapies already in various stages of clinical trials, with it triggering further top/ bottom-line expansions assuming a successful regulatory approval.

CRSP’s Investment Thesis Remains Expensive, Despite The Recent Pullback

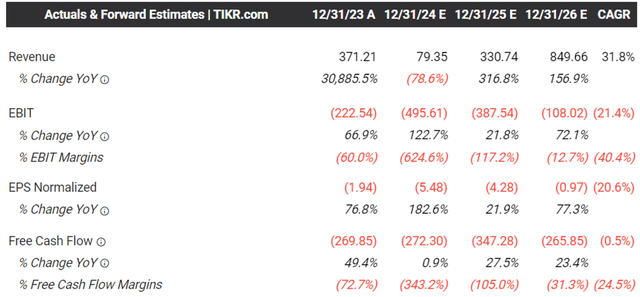

The Consensus Forward Estimates

Tikr Terminal

Even so, while CRSP’s Casgevy has received its regulatory approvals, readers must note that the therapy’s revenue recognition will only occur “near the end of the patient journey at infusion” during the nine to twelve months process.

As a result, while the biotech company is expected to report its next quarterly earnings call in August 2024 (estimated), readers may want to temper their expectations, since Casgevy is not expected to be top/ bottom-line accretive over the next two quarters.

The same has been observed in CRSP’s underwhelming top/ bottom-line growth projections over the next few years, with it expected to remain in the red – albeit with accelerating sales growth.

For now, most of its revenue recognition is attributed to its collaboration and/ or grant revenues, depending on the milestones achieved for Casgevy and other candidates.

At the same time, the management has been raising cash through dilutive capital raises, as observed in the growing net cash on balance sheet at $2.1B (+24.2% QoQ/ +11.7% YoY) and expanding share count of 81.79M (+3.2% QoQ/ +3.9% YoY) in FQ1’24.

Moving forward, we believe that CRSP is likely to further dilute its long-term shareholders, since the Casgevy monetization is likely to occur only from Q4’24 or Q1’25 onwards, with the other pipeline approvals potentially happening only in the second half of the decade.

At the same time, the nature of investing in nascent biotech stocks has always been speculative anyway, since only ~8% of clinical trials have been able to achieve the coveted regulatory approval.

As a result, while the CRSP management has been reporting promising early results in its clinical trials, it remains to be seen when further regulatory approval and/ or commercial revenue recognition may occur.

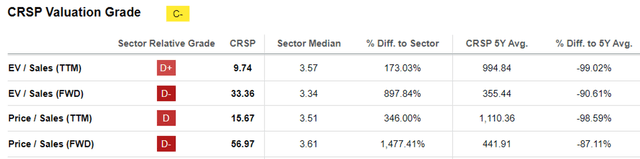

CRSP Valuations

Seeking Alpha

And it is for these reasons that we believe CRSP remains expensive at FWD EV/ Sales of 33.36x and FWD Price/ Sales of 56.97x, compared to its 1Y mean of 24.98x/ 37.61x, VRT at 4.89x/ 4.52x, and the biotech sector median of 3.34x/ 3.61x, respectively, with it offering interested investors with a reduced margin of safety.

Patent Dispute May Trigger Near-Term Headwinds

Most importantly, readers must note that CRSP does not hold any patent for the CRISPR-Cas9 gene editing technology, with those honors currently owned by Editas Medicines (EDIT).

This also explains why VRTX has had to pay $100M in licensing fees for Casgevy, on top of the annual fees ranging between $10M and $40M prior to the therapy’s patent expiry in 2034.

Even so, the patent dispute for the CRISPR-Cas9 gene editing technology has yet to end, despite the US Patent and Trademark Office ruling in favor of the Broad Institute of MIT/ Harvard and EDIT currently being the exclusive licensee of CRISPR patents.

With the other two inventors (and their research institutions), known as CVC, appealing the latest decision here and here, readers may want to pay attention to the developing situation indeed.

This is especially since the patent courts in Europe, China, and Japan have ruled for CVC – a direct opposite of the US ruling for Broad, with it potentially triggering further uncertainties in VRT’s and CRSP’s top/ bottom-line performance globally.

So, Is CRSP Stock A Buy, Sell, or Hold?

CRSP 6Y Stock Price

Trading View

As a result of the slower financial recognition and uncertainty surrounding its patent, we can understand why CRSP has lost much of its recent gains while retesting its previous bottom of $50s and trading below its 50/ 100/ 200 day moving averages.

As the stock continues to trade comfortably between its established support level of $40s and resistance level of $70s since November 2021, we believe that its intermediate-term investment thesis is likely tied to its swing trade potential, before the stock eventually grows into its premium valuations.

Lastly, readers must note that CRSP is likely to remain volatile ahead, attributed to the elevated short interest of 17.5% at the time of writing, worsened by the $10.6M of insider selling over the last twelve months (-31% sequentially).

As a result of the potential volatility, we prefer to initiate a Hold rating for now.

Those looking to add may do so if the CRSP stock remains well supported at $50s. Even so, they must size their portfolios according to their risk appetite and investing trajectory, since the Casgevy monetization is likely to be limited during the initial stages.

Read the full article here