Investment Thesis

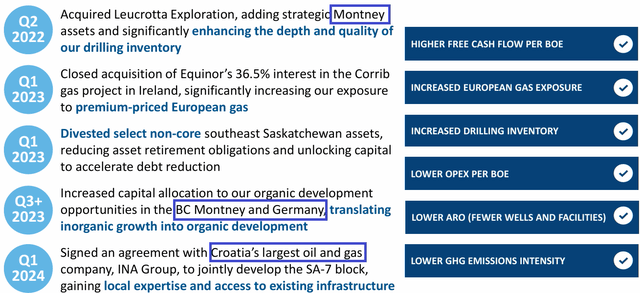

Vermilion Energy (NYSE:VET) is launching new projects in Mica Montney, Croatia, and Germany, which could accelerate both production and unlevered FCF in the coming years. Besides, the company appears well positioned to benefit from an increase in the gas price in Europe, where the war with Russia could affect markets. In addition, with expertise in many jurisdictions and some cash in hand, the promises about potential M&A transactions could bring FCF growth. Considering the recent stock repurchase program, which is expected to reduce the total share count by 10%, in my view, the demand for the stock could accelerate.

My Price Target: My DCF model and review of previous transactions in the oil and gas industry revealed a price target between $16.9 and $20.

Vermilion Energy: Diversified Operations

Vermilion is an international energy producer conducting acquisition, exploration, and development of production assets in North America, Europe, and Australia.

2024E productions include 31% of oil condensate, 22% of European gas, 32% of North American gas, and 15% of Brent oil. In my view, international operations will most likely bring less FCF volatility and operating risks. Besides, the company’s international profile brings potential acquisition opportunities, which may enhance business growth.

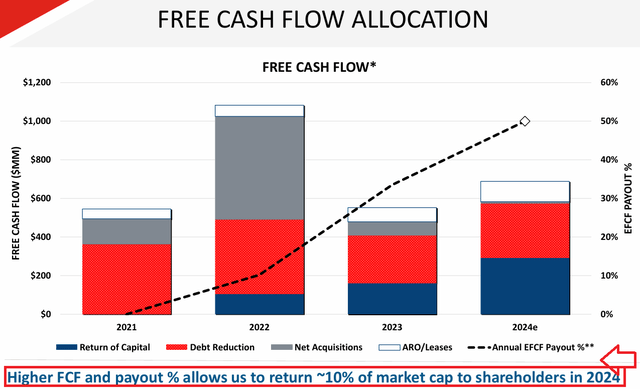

Targeting Return Of Capital of 50% Of EFCF for FY 2024

The company appears quite cheap, and managers seem to be fully aware of it. In my view, the recent debt reduction, dividend increases, and share buybacks are intended to enhance the current stock price.

Source: Company’s Presentation

According to the last presentation to investors, Vermilion returned over $40 per share to shareholders from 2003 to 2020, and the FCF payout increased from 0% in 2021 to about 50% in 2024. Taking into account these efforts, the current EV/EBITDA ratio, and PE, I would be expecting demand for the stock in the coming years.

Long-Term Debt Reduction, Increase In The Cash Per Share, And Book Value Per Share

From 2014 to 2020, the company reported an increase in the total amount of cash, increase in the total amount of Net Property, Plant & Equipment, and an increase in the total amount of assets. In my view, everything in the balance sheet indicates that the business model is growing. The ratio of total assets/total liabilities also stands at more than 1.7x, so I would say that the financial situation is quite stable.

Source: Seeking Alpha

In the last two years, VET reported a significant decrease in the total amount of debt. I do not think that the market did have a look at the recent reduction in leverage. From about $1.5 billion in long-term debt reported a few years ago, VET decreased its long-term debt to around $689 million. As soon as more investors have a look at the following figures, I think that the EV/EBITDA and the price/cash flow ratio will most likely increase.

Source: Seeking Alpha

With the reduction in the total amount of debt, the cash per share and the tangible book value per share increased significantly. The cash per share increased from $0.97 in 2014 to $1.18 in 2024. The tangible book value per share is close to $13.7 right now. It means that investors buying right now are buying below the tangible book value per share.

Source: Seeking Alpha

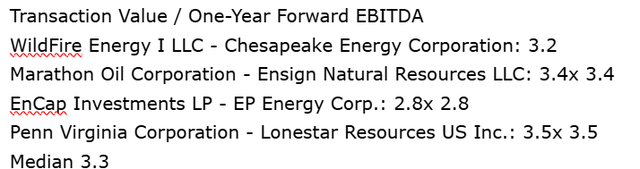

Precedent Transactions

I reviewed previous transactions executed in the sector, which included the acquisitions of Chesapeake Energy Corporation (CHK) and Ensign Natural Resources LLC, among other transactions. The median transaction value/forward EBITDA obtained from the list of transactions was close to 3.3x.

Source: Author’s Compilations

2024 forward EBITDA of $1100 million is, in my opinion, in line with previous EBITDA figures reported in the past, and appears conservative. Previous EBITDA figures, which were obtained from Seeking Alpha, are shown below.

EBITDA: 706.4 339.8 1,672.60 1,946.40 1,146.60 1,048.30

(From 2019 to 2024)

If we assume EV/Forward EBITDA of 3.3x, the implied valuation would stand at close to $3.3 billion or 3.3x$1100 million. If we subtract the current net debt, and divide by the share count, the implied target price would be $16.9.

- Total Enterprise Value:3300

- Net Debt: 537.70

- Equity: 2,762.30

- Shares: 163.40

- Target Price: 16.91

Discounted Cash Flow Expectations, And My Assumptions

With the war in Ukraine, the amount of gas delivered from Russia to Europe decreased significantly. Europeans continue to demand gas, so I would be expecting an increase in the price of gas in Europe. VET’s position in Europe and VET’s production of gas could benefit significantly from the current environment.

I also expect that the company’s operational expertise in Australia, Canada, Ireland, France, the Netherlands, and other regions in Europe could bring a number of new opportunities. With multiple teams and knowledge about a large number of jurisdictions, I think that VET is ready to study different oil and gas projects all over the world. Under my discounted cash flow model, I assumed that M&A could drive a role of enhancing FCF growth. The company claims to have 27 years experience of operating in Europe and acquiring from the majors. In addition, according to the last presentation given to investors, in the North American basins, the company appears to be evaluating small tuck-in acquisitions in the company’s core areas.

As noted in the most recent presentation, the company continues to optimize its drilling and competition processes through the company’s 2024 BC program. The program resulted in cost savings of close to 15% as compared to the previous BC program. As a result, in my view, we could see certain improvement in future unlevered FCF growth in 2024.

In the last few years, we saw how VET increased its headcount from about 503 employees in 2015 to around 740 employees in 2024. Given the current amount of cash in hand and new projects in Mica Montney, Croatia, and Germany, I expect further headcount increase. With new employees, I think that both production and unlevered FCF growth may increase.

Source: Company’s Presentation

For my FCF model, I took into account the guidance given for 2024, which includes production of 82k-86k boe/d and E&D capital expenditures of $600-$625 million. Besides, I studied the reserve life index reported by VET in a recent presentation. 2P average is close to 14 years. However, I assumed that management will use cash in hand for future development of reserves and acquisition of new producing reserves. Hence, I assumed that production will continue in 2035 and 2040.

I usually do not talk about financial figures in the past. However, in this case, the unlevered FCF growth is so impressive that it is worth having a look at. The unlevered FCF increased from $92 million in 2014 to around $591 million in 2024. In ten years, the company’s unlevered FCF figure was only negative once. Have a look at the numbers below before I offer my forecasts.

FCF: 92.2 59.5 233.9 249.9 294.4 215.6 183.4 (89.7) 518.9 572.4 591.3

(From 2014 to 2024)

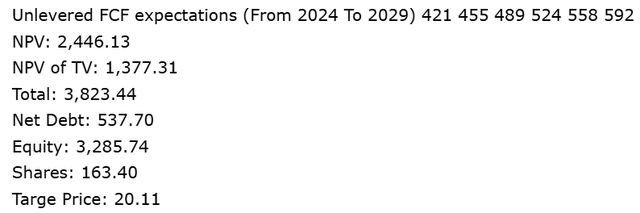

My unlevered FCF expectations include $421 million in 2024, $489 million in 2026, and $592 million in 2029. The sum of discounted unlevered future free cash flow from now to 2029 using cost of capital of 6.2% is equal to $2.44 billion. For the terminal value, I used an EV/FCF multiple of 3.3x. The sum of the terminal value and the net present value of future FCF is equal to $1.3 billion. Finally, if we assume net debt of $537 million, and divide by 12.044 million shares, the implied target price would be $20 per share.

Source: Author’s Calculations

Stock Repurchases Could Accelerate The Demand For The Stock

Recently, management announced a large stock repurchase program of around 10% of the total public float from July 12, 2024 to July 11, 2025. Stocks purchased are expected to be cancelled upon their purchase by Vermilion. In sum, the share count is expected to decline significantly in 2024 and 2025. If new market participants buy the stock expecting share price increases, the demand for the stock could increase. I see the stock repurchase program as a magnificent stock price catalyst.

The NCIB allows Vermilion to purchase up to 15,689,839 common shares, representing approximately 10% of its public float as at June 28, 2024, over a twelve month period commencing on July 12, 2024. The NCIB will expire no later than July 11, 2025. The total number of common shares Vermilion is permitted to purchase on the TSX is subject to a daily purchase limit of 180,974 common shares, representing 25% of the average daily trading volume of 723,899 common shares on the TSX calculated for the six-month period ended June 30, 2024; however, Vermilion may make one block purchase per calendar week which exceeds the daily repurchase restrictions. Any common shares that are purchased under the NCIB will be cancelled upon their purchase by Vermilion. Source: Press Release

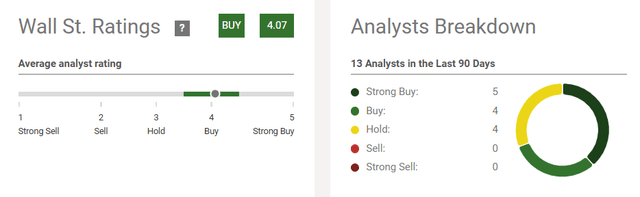

Review From Other Analysts

Out of the work of 13 analysts that I could consult in S&P, the average target price is close to 39% higher than the current market price. 5 analysts revealed a buy rating, 4 analysts gave a mark of outperform, and four analysts gave a hold note.

Source: Seeking Alpha Source: Seeking Alpha

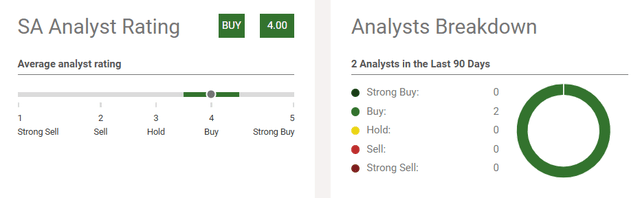

I did not find a single analyst who is a seller on this name. Clearly, it seems that there is stock demand in Wall Street for this company. Seeking Alpha analysts also gave a buy rating.

Source: Seeking Alpha

Risks From Changes In The Price of Oil And Gas

According to the most recent presentation to investors, VET hedged close to 20%-30% of its corporate total production. Hence, in my view, changes in the price of natural gas and the oil could bring certain unlevered FCF volatility. In addition, I could not see any information about hedges done for production in 2026, 2027, 2028, and 2029. Lower expectations about production from 2026 or lower expectations about future oil price or gas price could lower future unlevered FCF growth.

I would also expect risks coming from failed estimation of proven and probable reserves. If reservoir engineers overestimate the total amount of potential production of gas or oil, I think that future unlevered FCF may be lower than expected. In the worst-case scenario, analysts may write about the decrease in net sales growth, and investors may dump shares in the market. Consequently, the stock price may decline.

The company uses pipeline systems, rail, trucks, and takers, among other ways of transport. Shutdowns or lower logistic capacity than expected could affect the company’s ability to deliver products. In addition, VET works with third parties, which may fail to successfully deliver crude oil, natural gas, and other products. Under certain circumstances, I would expect a decline in net sales growth and unlevered FCF.

The business model conducted by VET is subject to a significant amount of environmental legislation and regulations. Failure to comply with regulations, changes in regulations with respect to carbon taxes, or enhanced emissions reporting obligations could reduce future unlevered FCFs.

Conclusion

VET’s diversified production of gas and crude oil, its exposition to the gas market in Europe, and new projects in Mica Montney, Croatia, and Germany could accelerate both production and net sales growth. I would also expect that new acquisitions promised in the last quarter may enhance the unlevered FCF expectations from market analysts. Clearly, the company knows many markets and many jurisdictions, so it appears ready to assess a number of international opportunities. Another stock price catalyst is the new stock repurchase of 10% of the total share count. In my view, as soon as new analysts review the new buyback program, the demand for the stock could accelerate. My price target is between $16.9 and $20, which is the result of a DCF model and the review of past transactions in the industry. Many other analysts have a price target that is not far from that of mine.

Read the full article here