Investment Thesis

Gaming and Leisure Properties (NASDAQ:GLPI) has recently signed a term sheet regarding the sale-leaseback transactions, development investment, and adjustment of terms regarding its purchase option. The transaction has not yet closed and is subject to several conditions. The fundamental terms outlined within the term sheet are very attractive for GLPI:

- with ~8.3% blended initial cap rate GLPI may realise a high spread on investment given its cost of capital

- the transaction contains a 15-year lease term with attractive, CPI-linked rent escalations ranging from 1% to 2%

- the Company strengthened its relationship with a global casino operator

- GLPI improved the terms of its purchase price (incl. the price, and therefore, the initial cap rate)

Moreover, GLPI has an outstanding occupancy rate (100% since inception), high dividend yield, and attractive valuation. On top of that, it operates within a unique property sector accompanied by niche value drivers.

Therefore, I believe that GLPI is still buyable, even after its recent stock price increase – especially regarding the fundamental conditions of the signed term sheet. That is a “buy” rating from me – I am bullish on GLPI.

Introduction

GLPI is a triple-net lease REIT that targets gaming properties across the US. This property sector provided unique value drivers that support GLPI’s value proposition, such as:

- resilience to economic turmoil

- immunity on the “Amazon effect”

- high barriers to entry with a strict regulatory environment limiting the new competition

- the limited ability of the tenants to switch location

- highly differentiated assets, which can be a brand in itself

- the complete mission-critical character of properties to its tenants

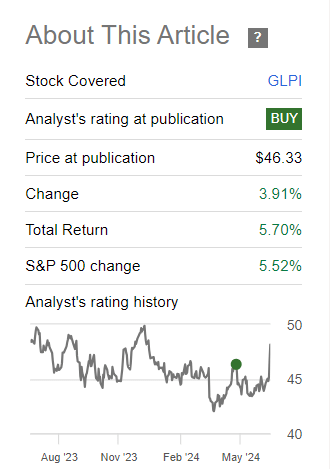

On June 26th 2024, the Company announced that it would release its Q2 2024 10-Q report on July 2nd, 2024 – I’m really looking forward to the update. The quality of the sector and GLPI’s business is confirmed through its business metrics. The Enterprise operated on a 100% occupancy rate since inception and is capable of securing deals with initial lease terms of 25-30 years (with renewal options). Also, the triple-net character of its agreements, under which the tenant is responsible for the substantial part of costs related to maintaining and operating the property, combined with solid annual rent escalators embedded within GLPI’s leases (often CPI linked with certain caps) contributes to its future growth prospects. It’s been some time since I last covered GLPI. Its stock price is currently ~3.9% higher than at the publication date, with a total return of ~5.7% delivered. Without further ado, let’s examine GLPI’s recent term sheet and its valuation outlook.

Seeking Alpha

Overview Of GLPI’s Recent Term Sheet

On July 12th 2024, GLPI announced that it had signed a binding term sheet regarding the investment volume of $1.585b. For clarity, the transaction hasn’t been closed/realised yet. The parties (GLPI and Bally Corporation (BALY)) outlined the fundamental terms of transactions within a term sheet; however, the completion of an agreement still depends on several conditions being met. To quote from GLPI’s press release:

Key conditions include but are not limited to:

- (a) valid assignment of the current ground lease to GLPI or acquisition by GLPI of the fee interest in Chicago

- (b) the final structure and pro forma capitalization of Bally’s following the proposed Standard General acquisition, or similar transaction, in the event any agreement is reached with the board of directors of Bally’s

- (c) completion of customary due diligence on the Chicago site

- (d) receipt of all necessary gaming regulatory and other third party approvals.

There are three subjects on the term sheet:

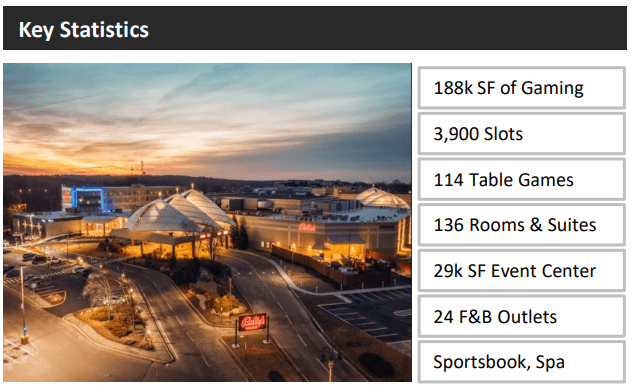

- casino development investment in Chicago amounting to $1.19b

- sale-leaseback investment concerning two properties amounting to $395

- favourable adjustment of GLPI’s call option on Bally’s Lincoln

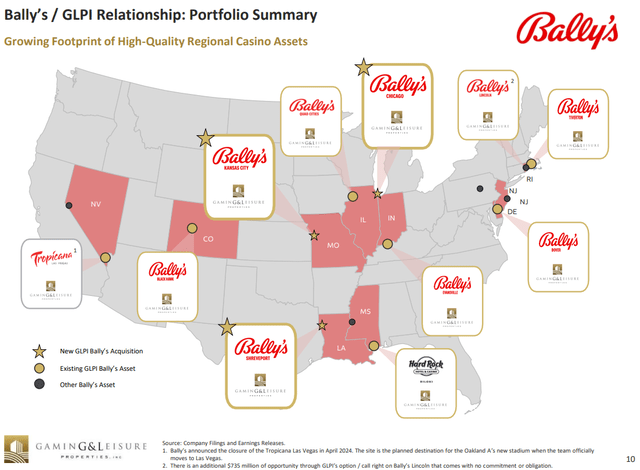

I’m looking forward to the final agreement as each part of the term sheet is favourable to GLPI. The Company may strengthen its relationship with Bally and further diversify its portfolio securing the stance of the most geographically diversified gaming-oriented REIT. Moreover, the completion of the transaction will be immediately accretive to GLPI in terms of AFFO per share. The overall strength of its portfolio will benefit from securing a flagship property in Chicago – America’s 3rd largest city with positive growth drivers.

GLPI’s acquisition summary – presentation

Let’s review the key terms of the transaction (overall):

- total investment volume of $1.585b (excl. the call option)

- solid 15-year term; however, GLPI has a history of securing longer terms

- pro-forma rent coverage exceeding 2.0x

- CPI-linked contractual rent escalations (with a 1% floor and 2% cap, so ranging from 1% to 2%)

Moreover, the transaction (excl. call option) has a blended initial cap rate of 8.3%, which is an attractive level given GLPI’s cost of capital. Let me provide you with a quick estimation:

- I derived the cost of equity from GLPI’s 2024 AFFO per share guidance ($3.73 at the midpoint) divided by its recent stock price ($48.14)

- I estimated its cost of debt based on its BBB- credit rating

- I assumed the current capital structure while estimating the debt-to-equity ratio

With the above assumptions, I estimated GLPI’s WACC (weighted average cost of capital) to be ~7.0%, meaning that the investment spread implied through this term sheet equals ~1.3% (given an 8.3% blended cap rate). For details, please review the table below.

Cash Flow Venue based on GLPI and Seeking Alpha

GLPI’s acquisition summary – presentation

GLPI’s acquisition summary – presentation

Regarding the purchase option on Bally’s Lincoln – GLPI improved its conditions by reducing the price from $771m to $735m, which resulted in a more attractive initial cap rate of ~8.0% as opposed to the primary 7.6%.

GLPI’s acquisition summary – presentation

Valuation outlook

Being an M&A advisor, I usually rely on a multiple valuation method that is a leading tool in transaction processes, as it allows for accessible and market-driven benchmarking within a specific peer group. Within the reference group, I’ve included VICI Properties (VICI), which is GLPI’s closest peer (business-wise), EPR Properties (EPR) – a leading non-gaming experiential property REIT, as well as a few retail/service-oriented REITs due to their triple-net lease business model. While this may not be a perfectly comparable peer group due to GLPI’s specific niche, I believe it can still provide a valuable reference point.

With that said, the forward-looking P/FFO multiple stood at:

- 12.8x for GLPI

- 11.6x for VICI

- 8.9x for EPR

- 15.7x for Agree Realty Corporation (ADC)

- 15.4x for Essential Properties Realty Trust (EPRT)

- 13.4x for NNN REIT (NNN)

For transparency, I don’t believe that VICI’s and EPR’s multiples fairly represent the values of their businesses. I provided a rationale for that here:

- VICI Properties: Undervalued Despite Elite Business Metrics; I’m Buying

- EPR Properties: One Of The Best Risk-To-Reward Ratios In The Industry

Therefore, despite their closest comparability to GLPI, I don’t consider their multiples a level that GLPI will approach. Nevertheless, I’ve included the companies on the list above, as some of you may not agree with me on that, and I respect that.

GLPI’s valuation has improved recently, which I believe was caused by three factors:

- positive data on inflation

- the quality of fundamental terms of the described term sheet

- the market’s recognition that GLPI’s multiple doesn’t accurately reflect its long-term ability to generate cash flows

Considering the quality of GLPI’s business model and the recent market/business developments, I believe that its P/FFO multiple will exceed 13.0x. Given the stance of a business, I expect it to range from 13.0x to 14.0x, assuming no material adverse changes and no major shifts in the economic environment.

Key Takeaways

GLPI’s Strengths And Opportunities

- outstanding occupancy rate (100% since inception)

- impressive lease terms, often amounting to 20 – 30 years

- favourable contractual rent escalators, especially impactful on GLPI’s bottom line given the triple-net character of its leases

- positive and high investment spreads

- operations within a sector accompanied by unique value drivers

- well-laddered debt maturity profile (for details, please refer to my previous analysis linked within the Introduction section)

- attractive valuation with further upside potential

- high and well-covered dividends

GLPI’s Weaknesses And Risk Factors

- relatively slow AFFO per share growth in the 2019 – 2023 period (for details, please refer to my previous analysis linked within the Introduction section)

- naturally, any potential problems of its tenants could translate into GLPI’s financial situation – especially given a relatively high concentration

- should GLPI ever step out of its niche, I believe we may observe increased stock price volatility (regardless of the rationale)

- prolonging the high interest rate environment will negatively impact GLPI’s financial performance by forcing it to refinance at a higher cost (~6% of its debt is maturing in 2024 with more debt maturities in the upcoming years – e.g. ~12.7% of its debt in 2025)

Read the full article here