Co-produced by Austin Rogers

About a year ago, we performed a broad analysis of commercial mortgage REITs to see if we could find any compelling value.

While the spread-based business model of residential mREITs is unappealing to us and has resulted in poor long-term returns, commercial property mREITs have better records, to varying degrees.

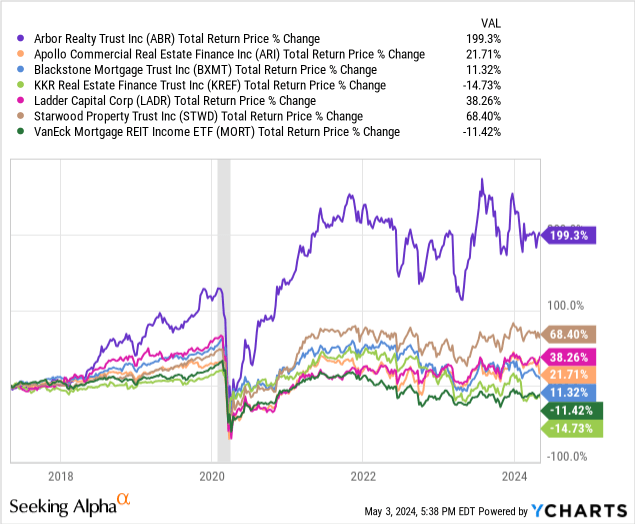

On a total return basis, only one commercial mREIT has underperformed the VanEck Mortgage REIT Income ETF (MORT), which is heavily weighted toward residential mREITs:

YCHARTS

That single commercial mREIT underperformer, KKR Real Estate Finance Trust (NYSE:KREF), only just began to underperform a few months ago with the announcement of a dividend cut.

The possibility of this sort of thing happening was exactly why we chose to avoid investing in any mREIT common shares last year. We only invested in two high-yielding mREIT preferred shares (ABR.PR.F; KREF.PR.A) and both have performed well so far.

We have unswervingly avoided office real estate since COVID-19 because of our bearishness on the sector, and we believe this avoidance has been justified. That goes for mREITs as well. All but the multifamily lenders (NexPoint Real Estate Finance (NREF) and Arbor Realty (ABR)) had between 18% and 34% of total exposure to office when we looked a year ago.

Interestingly, almost all the mREITs we examined last year have enjoyed positive price appreciation since then. All but one: KREF.

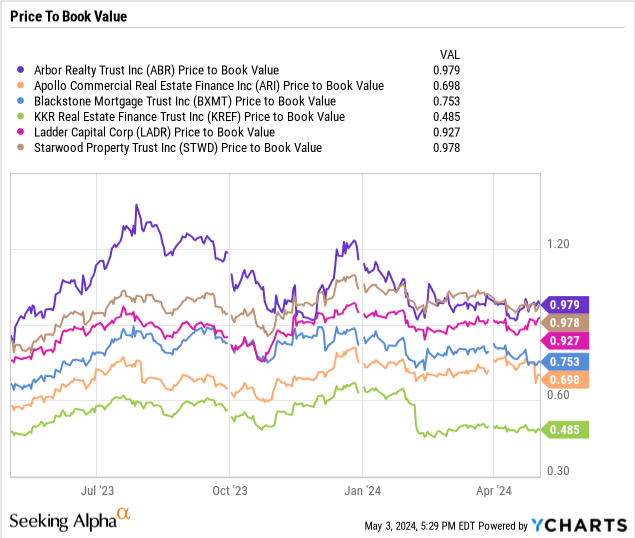

Thus, it’s not surprising to see that all but KREF now trade at higher levels relative to their respective book values than they did a year ago.

YCHARTS

If book value is to be believed (and the book value metric is generally far more accurate for mREITs than for equity REITs because of the lack of depreciation), then the common equity of KREF is buyable today at basically 50 cents on the dollar.

Whenever an mREIT trades at this big of a discount to book value, it implies that the market believes losses are coming. In KREF’s case, this discount implies even more losses are coming, perhaps enough to bankrupt the mREIT if worse comes to worst.

But it could also be the case that the market’s pessimism about KREF is overdone and that the stock price has been driven unreasonably low due to the dividend cut.

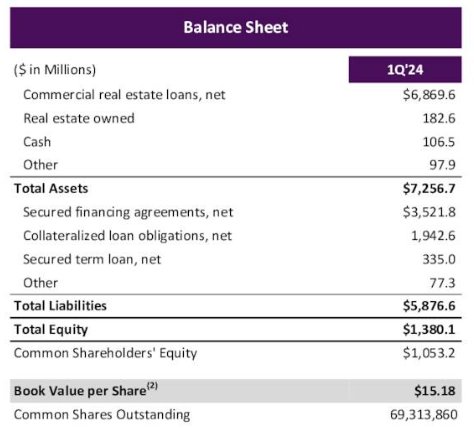

Seeking Alpha contributor Trapping Value suggests avoiding or selling KREF and that another dividend cut is likely. And TV certainly has a good point about KREF being heavily leveraged. Assets on the balance sheet total about $7.5 billion, not including provision for credit losses, while total debt is about $5.8 billion. So, a loss of $1.7 billion (23%) or more on its loan portfolio would wipe out all shareholder equity for KREF.

The risks are high for KREF right now, but so are the potential rewards.

Also consider the fact that two executive officers of KREF (the CEO and COO) purchased a combined $350,000 of KREF common stock a few months ago, right after the dividend cut announcement. And the price they paid ($9.72 per share) is right around where the stock still trades today.

Let’s look at a few other points in favor of KREF.

A Closer Look At KREF

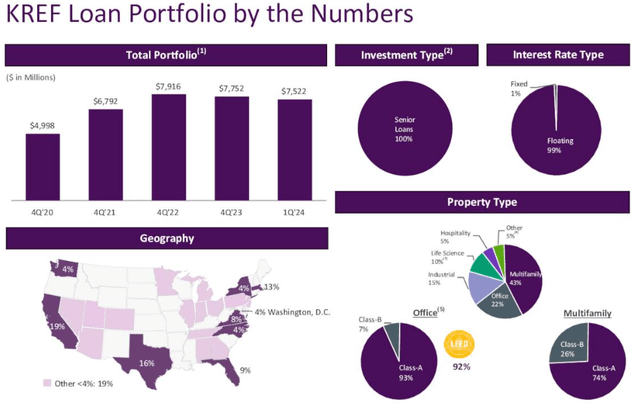

KREF is a mainly multifamily and industrial mREIT with 58% of its loans backed by properties in those two sectors. All of its loans are senior in the capital stack, and 99% are floating rate.

KKR Real Estate Finance

Office makes up 22% of the loan book, and this is the most troubled sector right now. Fortunately, though, 93% of its office properties are Class A, which should minimize operational downside and any potential losses.

Its parent company is KKR & Co. (KKR), one of the leading alternative asset management companies, giving KREF access to a vast network and resources to originate and manage its loan portfolio. KKR even owns 14% of KREF.

Its weighted average loan-to-value sits at 65% as of Q1, 2024. While higher than one would like to see right now, that metric implies that KREF’s underlying real estate properties would need to drop in market value by 35% or more for it to take permanent losses.

That could happen. As you can see from the top left chart in the image above, over 1/3rd of its loans were originated from Q4 2020 to Q4 2022, a period of low interest rates and elevated property prices. It is entirely possible that some of the underlying properties for KREF’s loans originated in 2021 and 2022 have lost 35% or more of their previous market value.

However, as we’ll see below, KREF’s management has expressed confidence that they will be able to sell their owned real estate and reinvest the proceeds to recoup some of their lost distributable earnings, implying that KREF’s ultimate losses won’t be major.

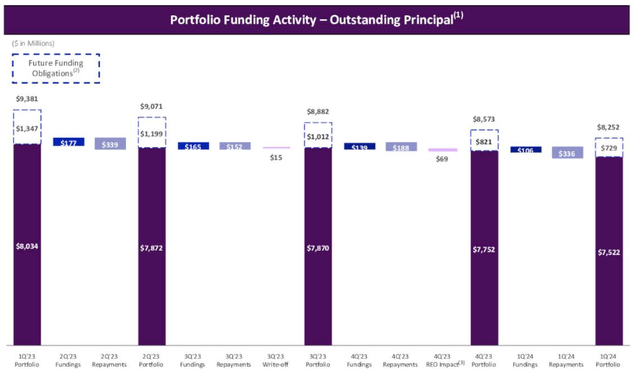

In the last year, KREF has played defense, funding fewer new loans than the amount of loan repayments.

KKR Real Estate Finance

This has gradually shrunk the total loan book without meaningfully shrinking operating cash flow.

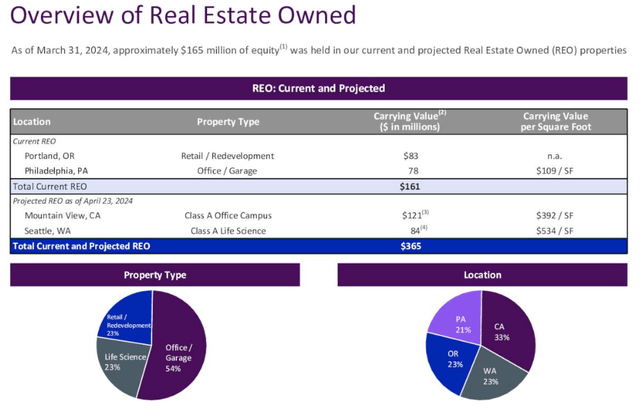

KREF has about $183 million in owned real estate that it is working to position for sale. Usually, this just involves leasing up the building to make it more attractive to investors, but there are operating expenses that go along with owning real estate.

KKR Real Estate Finance

That book value per share of $15.18 is only really reliable if no more losses are borne in KREF’s loan book and the owned real estate actually gets sold for around $183 million.

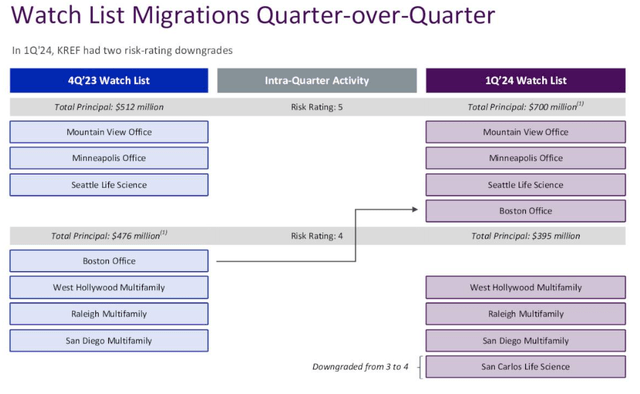

But it should be noted that KREF’s watch list includes four properties with a total principal balance of $700 million (3.8x KREF’s owned real estate value) with the highest risk rating below outright default.

KKR Real Estate Finance

Additionally, KREF has another four properties with a principal balance of $395 million at the next lowest risk rating of 4. These are stressed properties that may or may not recover from here.

As we’ll see below, management believes that there should not be further risk migration in its portfolio for the foreseeable future.

The four Risk Level 5 properties that KREF now owns after foreclosure are not exactly what you’d want to own in today’s market.

KKR Real Estate Finance

Office and life science are suffering from oversupply right now, and the West Coast states lack the level of population and job growth enjoyed by other areas of the country.

Nevertheless, management remain confident in their ability to reposition and sell these properties in a timely manner.

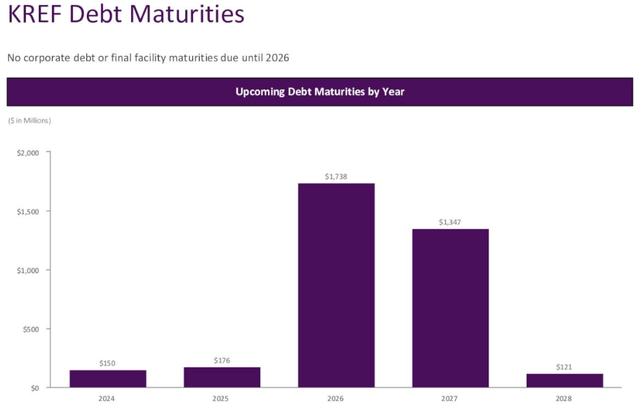

KREF’s balance sheet is a beneficial aspect of the company. Even though debt is high at 2.1x debt-to-equity, there are no corporate-level debt maturities until 2026 and few asset-secured maturities between now and then.

KKR Real Estate Finance

This minimizes the pressure on KREF from interest expenses.

Then again, since KREF’s portfolio is virtually all floating rate loans, maturing debt is not the primary threat that the mREIT has to worry about right now.

Commentary On The Q1 Conference Call

Here are a few highlights from the Q1 2024 conference call:

- KREF’s largest property sector of multifamily (overwhelmingly Class A) is performing well.

Multifamily represents 43% of our portfolio and has performed well with weighted average rent increases of 3.4% year-over-year.

- First, though KREF has been mostly inactive on the investment front over the last year or so as it works through credit issues, management foresees becoming active again in the next few quarters.

With US bank still largely on the sidelines and the increased market activity, our expectation is for this supply demand imbalance to normalize and potentially reverse, creating an attractive opportunity for KREF to fill this void as we resume lending in the next few quarters.

- Although office real estate fundamentals remain poor and aren’t getting much better anytime soon, KREF doesn’t believe any more of its own office loans will default or become problematic.

In KREF’s portfolio, we continue to feel we have identified the potential office issues within our watch list and do not anticipate further negative ratings migration to the watch list from the office sector.

- Management have expressed confidence that the newly reset dividend is sustainable. The yield is over 10%!

As we stated last quarter, we set our dividend at a level that we can cover with distributable earnings ex losses with our performing loan portfolio under a number of different scenarios. Our expectation is that in the near term, DE ex losses will continue to be significantly higher than our dividend.

- KREF does not have liquidity issues.

With the help of KKR Capital Markets, KREF continues to maintain high levels of liquidity with $620 million of availability at quarter-end, including $107 million of cash on hand and $450 million of undrawn corporate revolver capacity.

- Selling and reinvesting KREF’s owned real estate provides potential upside to distributable earnings.

As we mentioned last quarter, we will patiently optimize our REO portfolio, and as we sell those assets, we believe we can reinvest the capital to generate an additional $0.12 per share in distributable earnings per quarter.

For all these reasons, we are today considering opening a position in the common equity of KREF. We believe that they are likely to face much smaller losses going forward than what’s implied by the large discount to book and if we are correct, then the upside potential could be 50-100% in the coming years, and you earn a very high dividend yield while you wait. We will wait for Q2 results before making an investment decision.

Read the full article here