Overview

KKR Income Opportunities Fund (NYSE:KIO) operates as a closed end fund that prioritizes high levels of current income through its investments in different fixed income and loan instruments. As a dividend investor, I believe that assets like this can have their use cases and help boost your portfolio’s dividend income at a faster pace. Unlike traditional dividend growth stocks that aim to grow earnings year after year to support distribution increases, these income focused assets only have to merely survive by doing the bare minimum in order to fund their high yields. We will cover the structure and strategy that KIO uses to generate enough capital to support its large 10.4% dividend yield, as well as the caveat that’s attached to this high yield.

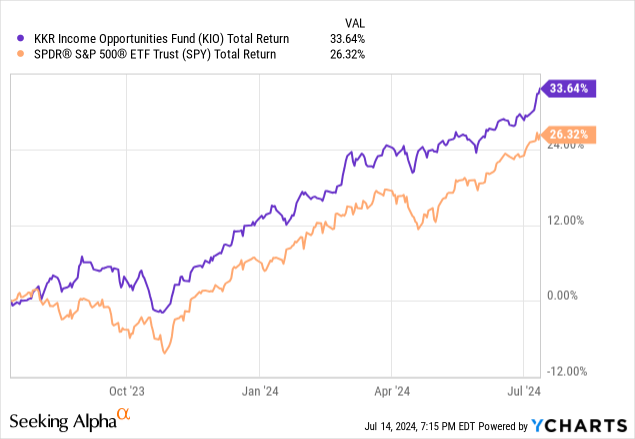

While most investors aren’t buying income based assets like this to outperform the S&P 500 (SPY), it’s still pretty interesting that KIO can outperform the SPY in total return. We can see that KIO has a total return of 33.6% over the last year, compared to the S&P 500’s total return of 26.3% over the same time frame. This outperformance has come from a combination of both a consistently high distribution rate and recent price appreciation over the last year. After all, the fund does have a secondary objective to provide some level of capital appreciation.

However, I do believe that KIO is currently overvalued. Since it operates as a closed end fund, the price can vary from the underlying value of the net assets. As a result, I typically aim to get into these sort of investments while the price trades at a discount to its net asset value. At the moment, the price trades at one of the highest premiums over the last decade. This is the primary driver behind my current hold rating.

KIO is externally managed by KKR Credit Advisors and has a public inception dating back to 2013. The fund has an annual management fee of 1.7%. This means we have over a decade of historical performance to reference. KIO aims to utilize a diverse set of credit instruments to capitalize on different corporate credit environments. The higher distribution rate from an investment like KIO has the ability to offset the current higher interest rate environment as well.

Structure & Strategy

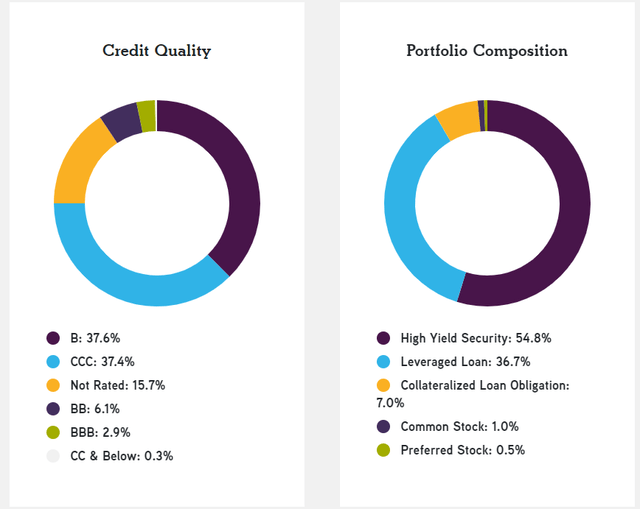

KIO supports its generous yield by making investments into different fixed income and loan instruments. This includes exposure to leveraged loans, collateralized loan obligations, and high yield securities. The caveat to the high distribution rate is the fact that KIO’s portfolio of investments is below investment grade rated. ‘Below investment grade’ is usually used in conjunction with the term junk. While this may potentially introduce a higher level of risk, it also presents a higher potential reward through the continued high yield.

The term junk scares a lot of investors but what most people don’t realize is that the majority of companies in the world fall into this category. A stat I found on Econ Library is that approximately 95% companies with revenues over $35M are rated as noninvestment grade. This even includes some well known companies that are included in KIO’s portfolio such as JetBlue, Hilton Grand Vacations, Rolls-Royce, and even Burger King France.

For reference, credit quality ratings of a BB+ and below are considered junk. We can see that the majority of KIO’s portfolio is invested in B-rated and CCC-rated, accounting for 37.6% and 37.4% respectively. High yield securities account for over half of the portfolio composition, making up 54.8%. Leveraged loans account for 36.7% and collateralized loan obligations sit at a small 7% exposure. Lastly, common stock and preferred stock sit at 1% and 0.5% respectively.

KKR Funds

As part of their portfolio, there are about 185 different issuers with an effective duration of 1.49 years. The investments have an average coupon rate of 11.53% and an average yield to maturity of 15.63%. Lastly, approximately 42.8% of the portfolio is invested on a floating rate basis, while the remaining portion is comprised of fixed rate investments. This mix is quite interesting to me because the fixed rate investments offer a sense of stability and likely a lower risk of default as borrowers know exactly what their obligations are every month.

The floating rate investments in the portfolio have the ability to really benefit in the current interest rate environment. As rates rise, so do the required interest payments that borrowers are required to pay. This can help KIO rake in higher levels of interest income. The Fed continues to leave interest rates unchanged as of their latest meeting, which has likely helped KIO boost its total net investment income and contribute to a more comfortable margin of safety when it comes to the distribution coverage.

KIO Factsheet

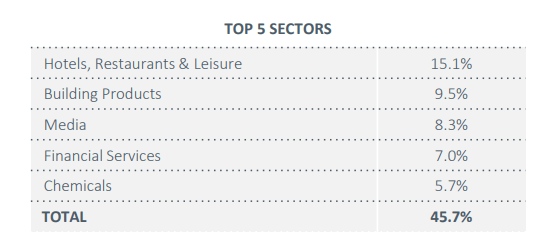

Lastly, KIO has been able to continue a consistent distribution rate despite being exposed to investments related to businesses that are cyclical in nature. Hotels, Restaurants, and & Leisure account for the largest sector exposure at 15.1%. These are sectors that may be reliant on growing levels of consumer spend. This is followed by building products accounting for 9.5% of the sector exposure and media accounting for 8.3%.

Financials & Risk Profile

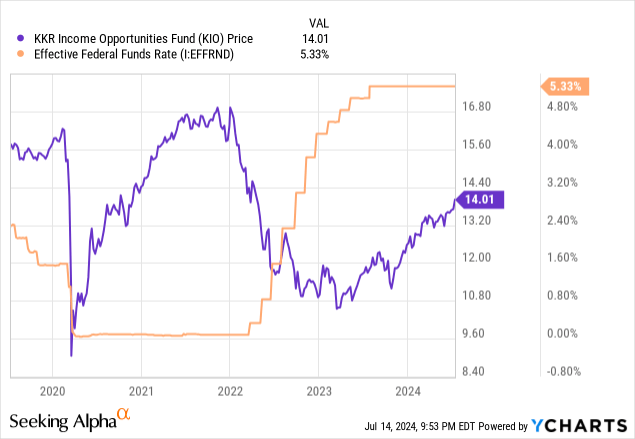

A lot of the risk around these junk rated investments comes from the fear of default. Interest rates definitely have an influence on these types of investments and it’s clear when we look at the price relationship that KIO shares with the federal funds rate. We can see that when interest rates were cut to near zero levels in 2020, the price of KIO thrived to the upside. This was an environment that catered to growth as capital was cheaper to obtain, and it was more cost-effective for businesses to allocate capital towards different growth initiatives.

Conversely, when interest rates started to hike rapidly throughout 2022 and 2023, we saw KIO slide to the downside. This was probably the best time for entry but also may have been the scariest. Since the large majority of the debt investments within KIO’s portfolio are junk rated, this means that higher interest rates likely put more strain on these businesses and shrank operating profits. Higher interest rates can increase the rate of defaults within this space, but historical data has shown us that is not typically the case.

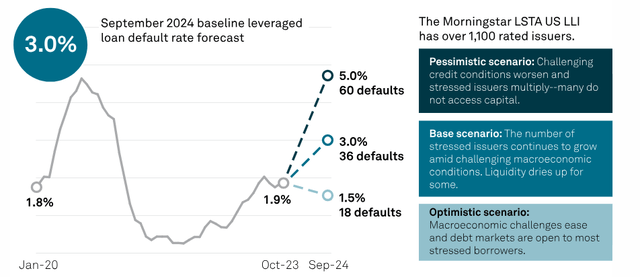

Data compiled by S&P Global shows us that the baseline leveraged loan default rate is forecast to sit around the 3% mark. Using the sampled data, in an optimistic scenario defaults could be as low as 1.5%. However, in a more pessimistic outlook, the default rate could reach as high as 5%. However, I believe that the tide may be turning on the current high interest rate environment.

S&P Global

The current unemployment rate now sits at 4.1% and has consistently increased over the last year. Additionally, inflation has consistently cooled since March and now sits at the 3% mark. Lastly, the US Presidential elections are upcoming at the end of 2024 and this can cause higher levels of volatility and uncertainty in the markets. I believe the combination of these things can serve as incentives for the Fed to begin cutting rates by the end of the year. Of course, this is assuming that inflation continues to cool, and the unemployment rate continues its upward course.

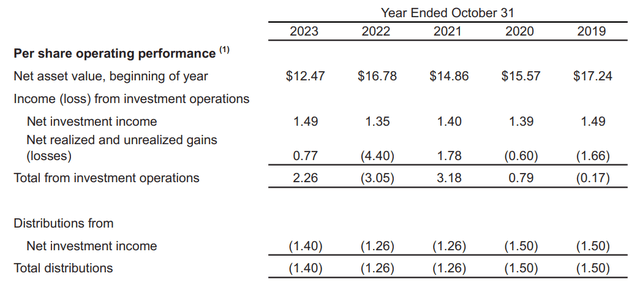

Taking a look at the most recent annual report for 2023, we can see that net investment income landed at $1.49 per share, while net realized gains amounted to $0.77 per share. Thankfully, net investment income alone was enough to fully cover the annual distribution amount of $1.40 per share. The excess gains of the fund can positively contribute to NAV growth going forward. It may also free up capital for KIO to continue investing into new areas of growth in the portfolio.

We can see that the prior year’s performance resulted in a total loss in investment operations of $3.05 per share, which contributed to the net asset decline. However, the fund is able to retain funds from positive performing years so that they can fund any shortcomings on net investment income to fund the distribution.

KIO Annual Report

I believe that future interest rate cuts would likely increase the volume of potential borrowers since it would be more cost effective to acquire capital. This may unlock lots of new opportunities for KIO to continue growing their total portfolio and fuel additional growth of net investment income. Additionally, lower interest rates may contribute to higher NAV growth since borrowers on a floating rate basis may see some relief and larger operating margins.

Dividend

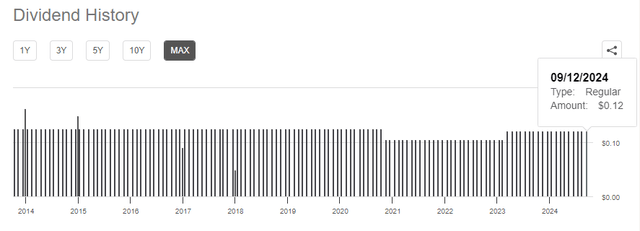

Another part of the appeal of holding a fund like KIO is that the distribution is issued to shareholders on a monthly basis. This may be ideal for investors that are nearing, or already at, retirement age and depend on the income generated from their portfolio to fund lifestyle expenses. As of the latest declared monthly dividend of $0.1215 per share, the current dividend yield sits at 10.4%. This monthly rate has also been confirmed through September, which instills confidence that the fund management already knows they will be able to maintain this distribution for a few more months.

Looking back over the last decade, we can see that KIO’s dividend has remained relatively stable over time. This stability has made it a great long term pick for income investors. To be fair, the distribution was slightly reduced in 2020 down from a prior monthly rate of $0.13 per share. The dividend has slowly crept its way back as internal performance improves.

Seeking Alpha

One of the potential downsides of the distribution history is that there has been a lack of growth over the last decade. If you are looking for a consistently increasing dividend income without having to put in any effort, you may want to look elsewhere. However, the lack of formal distribution raises doesn’t necessarily mean that you can’t grow your income with KIO. All it means is that you’ll have to front more cash and make the conscious effort of continually reinvesting additional capital over time.

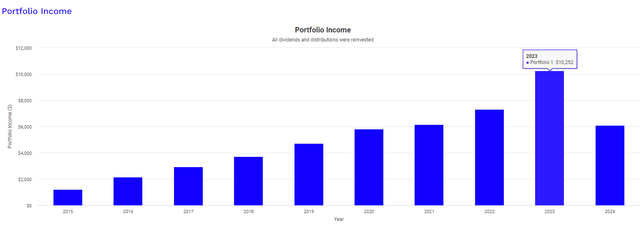

As a way to better visualize the growth that can take place, I ran a back test over the last year using Portfolio Visualizer. This bar graph represents an initial investment of $10,000 at the start of 2015. It also assumes that you added a fixed monthly contribution of $500 throughout the entire holding period over the last decade. Since the distribution rate hasn’t grown, you have to effectively create your own growth through additional capital being invested on a consistent basis. Lastly, this graph assumes that all dividends received over the course of the last decade were reinvested back into KIO to help accumulate more shares and further compound your income received.

Portfolio Visualizer

In 2015 your dividend income received would have been $1,234 for your first year. Fast forwarding to 2023, the annual dividend income received would have grown to about $10,252. As we can see, despite the lack of raises, you would have been able to raise your dividend income year after year through continued investment and reinvestment. The growth would have been relatively stable year over year as well, as you can see from the bar graph. Retired investors that have had a longer lifetime of accumulation will likely have a larger initial investment amount to start with, which would result in an instant higher upfront distribution received.

Something to mention is that the distributions received from KIO are typically classified as ordinary dividends. As a result, an investment in KIO would have less favorable tax consequences, versus an investment in a more traditional dividend growth stock. This may be offset by holding KIO in a tax advantaged account, and therefore may not be suitable for all investors.

Valuation

In terms of valuation, KIO does happen to trade at the absolute highest premium to NAV level than it ever has over the last decade. The price trades at a current premium to NAV of 4.32%. For this reason, I am choosing to stay on the sidelines and away a better entry opportunity if the price is ever discounted. Just as a reference, KIO has traded at an average discount of about 7% over the last three years. The recent price run up has now made entry here unattractive. Over the last three years, the highest discount we’ve seen the price drop to is 14.6%.

CEF Data

Therefore, entry here would not be ideal for investors looking to lock in the maximum dividend yield possible. I plan to personally wait for a price retraction before considering a position in KIO. The NAV does, however, sit considerably lower, ending 2023 at $12.47 per share. This is down from 2019’s end year total NAV of $17.24 per share. Therefore, I would like to see how NAV growth plays out after the US Presidential elections and more of a normal interest rate environment. As a result, I am maintaining a current hold rating on KIO and plan to revisit it at a later date.

Takeaway

In conclusion, KIO is a solid option for income focused investors that are looking for a reliable source for high yielding dividend income. Although the portfolio is focused on non-investment rated vehicles, performance has been solid from a net investment income perspective as the distribution remains to be fully covered. Additionally, I believe that future interest rate cuts will provide relief and improve fund performance going forward. However, the price currently trades at a decade high premium to NAV, and I will be waiting for a better price entry at some point in the future.

Read the full article here