In our previous article, we discussed the upcoming CPI report. The market got a spectacular number, the “ideal CPI,” if you will. CPI inflation dropped like a rock from 3.3% to 3.0%, better than the anticipated 3.1%. The better-than-expected inflation reading brings the market closer to the highly anticipated rate cut, with the CMEGroup’s rate cut probabilities for September surging to over 90%. So, with inflation falling and rate-cut probabilities increasing, why did our favorite tech stocks sell-off?

Nvidia (NVDA), one of Wall Street’s top darlings, dropped by nearly 6%. Tesla (TSLA) declined by a whopping 8.5% in Thursday’s post-CPI session. Micron (MU), another AI favorite, slid by 4.5%. SoundHound AI (SOUN) spiked to $6.18 (22% gain) in the early session but closed up by only 6% on Thursday. Alphabet (GOOG) (GOOGL), Amazon (AMZN), Apple (AAPL), Microsoft (MSFT), Meta (META), and all the mega-cap tech stocks closed lower after the stellar CPI report.

The first words that come to mind are pullback and rotation. The mega-cap tech segment has led stocks higher for a long time, and recently, technical conditions became overheated. We can also argue that many valuations in the mega-cap tech space have become “stretched,” at least in the near term. This dynamic doesn’t mean valuations won’t go even higher, but these stocks may need a break in the near term.

On the other hand, other areas in the market became neglected, especially mid/small cap stocks. The positive CPI reading has increased the probability of a rate cut sooner than later, and we could see the first cut in September. Lower rates are very positive for the R2K stocks (small/mid caps), as lower rates lead to growth in the domestic economy, and many small/mid caps derive much of their revenue in the U.S.

Of course, lower rates are also positive for the mega-cap tech stocks, but we may see a transitory period of rotation and some pullbacks before our favorite tech stocks shoot for stars again. For context, let’s look at several charts that could enable us to determine why the pullback rotation period is occurring and how long it could last. Let’s also look at appropriate buy-in and add levels, just in case the correction gathers steam.

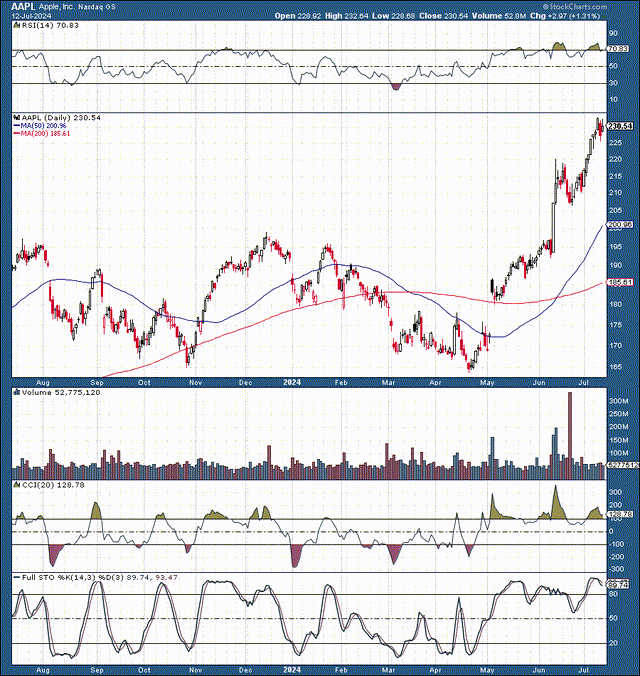

1. Apple Stock

AAPL (StockCharts.com | Advanced Financial Charts & Technical Analysis Tools)

Apple is like the grandaddy of AI consumer hardware (in a good sense). The stock has had a considerable rally recently due to its AI prospects, becoming the world’s most valuable company again. While the recent breakout and uptrend are constructive, Apple’s stock became massively overbought on a near-term basis.

Apple’s stock surged by about 42% since about mid-April. The RSI hit around 80, and other technical indicators illustrate that the stock became overbought. Also, Apple’s 2024 P/E ratio shot up to around 35, which is rather pricy for a hardware stock, even with its AI potential.

Why the pullback should be transitory:

While Apple seems expensive here, it could benefit considerably from the next AI-iPhone cycle and the general integration of AI into its enormous ecosystem of products and services. The positive news is that Apple’s sales growth and EPS estimates could be revised higher as future earnings and guidance could beat consensus estimates. Technically, $215-200 appears like a solid area to buy in or add shares, in my view (roughly a 7-15% pullback).

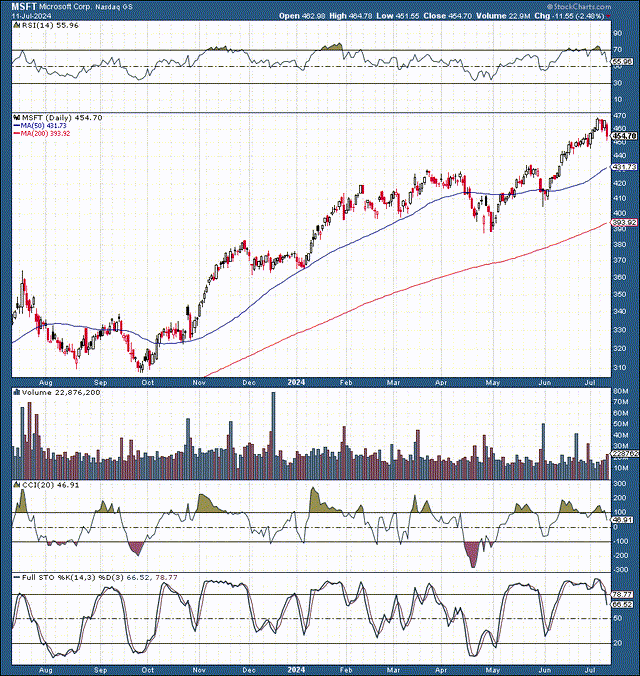

2. Microsoft

MSFT (StockCharts.com | Advanced Financial Charts & Technical Analysis Tools)

Microsoft is the second most valuable company globally. Its stock appreciated by about 52% from its 52-week low. These multi-trillion-dollar companies account for massive portions of major averages. At roughly 7% each, Microsoft, Apple, and Nvidia comprise roughly 21% of the S&P 500’s total weight.

Microsoft’s RSI ran up to well above 70, as its stock surged substantially above its 200 and 50-day MAs. We also see the full stochastic moving below 80, implying that near-term momentum is worsening, signaling that the stock could correct more. From a valuation perspective, Microsoft’s P/E ratio of nearly 40 seems stretched despite its enormous AI presence.

Why the pullback should be transitory:

While Microsoft appears expensive, the company has massive AI potential and will likely continue garnering a high multiple. Moreover, its EPS and sales growth estimates could be revised higher in future quarters, as the company will likely report better than anticipated results and guide higher. Technically, a solid buy-in/add area could be around the $430-420 support zone (roughly an 8-12% pullback).

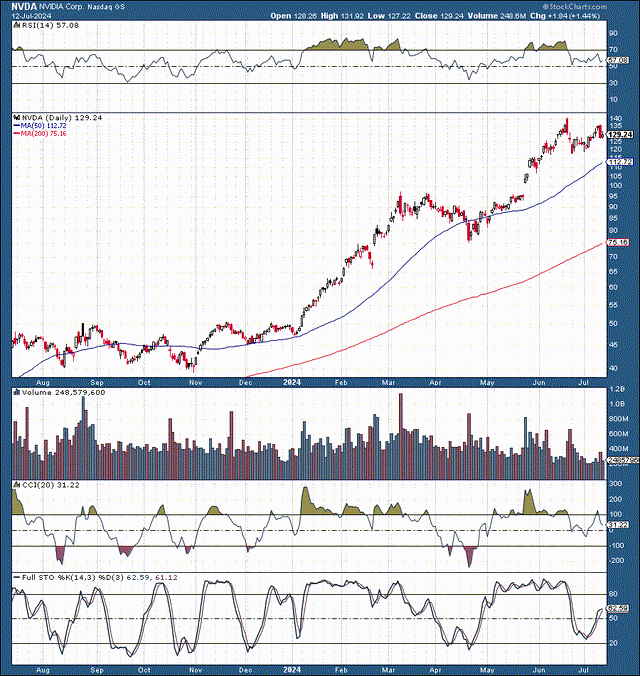

3. Nvidia

NVDA (StockCharts.com | Advanced Financial Charts & Technical Analysis Tools)

Nvidia has had an incredible run. In fact, this is the most significant appreciation for a mega-cap company in history. Nvidia is up (trough to peak) by about 250% from its 52-week low (roughly $40-140). However, if we go back slightly to its split-adjusted bear market bottom in late 2022, Nvidia was up by an astounding 1,200%.

We’re talking about a 13x return in under two years. I often say that trees can’t grow to the sky, and we should not expect Nvidia to rise perpetually without transitory periods of decline. Nvidia recently went through about an 18% pullback, but we may see more consolidation and a more significant pullback in the weeks ahead.

Technically, Nvidia became massively overbought recently. We also witnessed a blowoff top and a subsequent lower high. This dynamic implies that there may be more consolidation and transitory downside ahead. Also, the stock became quite expensive, with a fiscal 2025 P/E ratio of nearly 50 and trading at around 26 times the estimated fiscal 2025 sales. Also, we should not forget that Nvidia remains primarily a hardware company despite its enormous lead in AI.

Why the pullback should be transitory:

Despite its hefty valuation and significant hardware segment, Nvidia is still the undisputed king of AI. Nvidia is also gaining more share in services and software, making it the top one-stop shop for enterprise AI solutions. Furthermore, Nvidia’s sales should continue surging, leading to increased profitability, and its forward P/E ratio is only around 35, arguably inexpensive for a company in its dominant market-leading position. Still, the technical pullback may continue, and a solid buy-in/add level may be around $115-100, roughly an 18-28% pullback from its recent top.

Watch The Data, Earnings, And The Fed

I believe three crucial elements will determine the timing and magnitude of a possible broad market pullback. Now, we’re seeing rotation, but the rotation may eventually transition into a correction. I’m not timing the market, but my best guess is that a broader pullback/correction may arrive around mid to late August, lasting into September. Of course, we will see about this.

The Data – Inflation must remain in its downward trend, and the labor market should remain in the Goldilocks zone. We don’t want the labor market showing too much strength, as this could make the Fed hold off on cutting rates for longer. On the other hand, we must avoid deterioration, as this dynamic would imply a hard landing/recession scenario is back on the table.

The Fed – The probability of a September rate cut is around 95%. This means the market has priced in at least one rate cut by the September FOMC event. If the probability of a rate cut declines below 80-90%, or if the Fed surprises by not cutting in September, there could be a substantial selloff ahead.

Earnings – Earnings must remain on point. Most companies need better-than-expected sales and EPS numbers, especially the high-quality AI-related mega-cap names. More importantly, we need better-than-anticipated guidance as AI revenues and efficiencies continue increasing and spreading around the market.

The Bottom Line

Despite the potential for more volatility and transitory downside in high-quality tech stocks, I am not selling the bulk of my Nvidia shares. The AI bull market is likely still in its early to mid stages, and Nvidia’s stock could be considerably higher next year. However, that doesn’t mean we won’t have notable pullbacks and corrections of 10%, 20%, and even 30% in some of our favorite stocks.

I continue to adjust around the peaks and troughs, implementing covered calls and other option strategies to maximize income, limit downside, and mitigate risk. Also, despite the possibility of a broad market correction, I am keeping my year-end SPX target in the 6,000-6,200 range.

s

Read the full article here