Transcript

We think the world could be undergoing a transformation on par with past technological revolutions.

It’s being driven by mega forces like the rise of artificial intelligence, the low-carbon transition and the rewiring of supply chains. Those three in particular could unleash a potentially massive wave of investment, reshaping economies and markets. The size, speed and impact of that investment is highly uncertain. So several starkly different outcomes are all feasible, in our view. We think this transformation presents exciting investment opportunities.

The three themes for the BlackRock Investment Institute’s 2024 midyear outlook are: getting real, leaning into risk and spotting the next wave.

Our first theme: Getting real. We see the biggest opportunities in the real economy as investment flows into infrastructure, energy systems and technology – and the people driving them. We think companies will need to evolve their business models. Company fundamentals will matter even more.

Next, leaning into risk. Investors may be tempted to wait for clarity on how the transformation will pan out. But we see potentially large rewards for leaning into risk. We look for investments that can do well across outcomes and lean into the current most likely one.

The third theme is spotting the next wave. The path of the transformation could shift over time – and potentially suddenly. This theme is about looking for the next wave of investment opportunity and being ready to overhaul portfolio allocations to capture it.

The bottom line is: we see a possible investment boom ahead that could transform economies and markets. We are taking risk by leaning into the transformation and are ready to reassess as the outlook changes.

We see unprecedented waves of transformation creating an unusually wide range of outcomes. Our 2024 Midyear Global Outlook shows how, rather than waiting for clarity, we’re leaning into risk. We stay overweight U.S. equities and the artificial intelligence (AI) theme yet monitor valuations. We like private markets as a way to access early winners. Elsewhere, we go overweight UK equities and stay overweight Japan. We favor short-term bonds for income and prefer quality in credit.

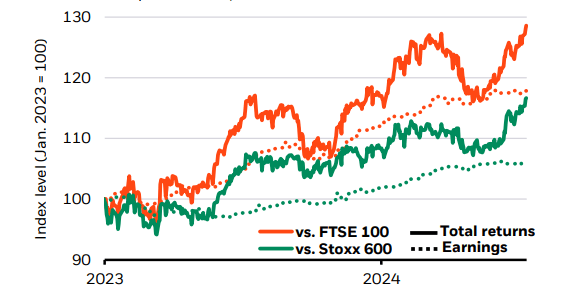

All about earnings

S&P 500 relative performance, 2023-2024

Forward looking estimates may not come to pass. It is not possible to invest directly in an index. Index performance does not account for fees. Source: BlackRock Investment Institute, with data from LSEG Datastream, July 2024. Notes: The chart shows the S&P 500 relative performance of total returns and 12-month forward earnings vs. the UK’s FTSE 100 and Europe’s Stoxx 600 indexes.

A transformation of a historic scale could be unfolding. Investment opportunities transcend the unusual macro backdrop of sticky inflation, higher interest rates, slower growth and elevated debt. U.S. equities had a banner first half of 2024 versus other developed markets (DMs) even as markets priced out Federal Reserve rate cuts. The strength of U.S. stock gains has been matched by corporate earnings beating expectations, led by a handful of AI names. See the chart. As a result, we see concentration as a feature, not a flaw, of today’s market environment. We expect some volatility ahead as markets grapple with a wide range of outcomes – as shown by last week’s brief retreat in tech shares. Recent low market volatility doesn’t reflect all risks ahead, in our view. We still think the next 6 to 12 months is a time to lean into risk, but we prepare to reassess as new opportunities arise.

In the near term, we see a concentrated group of AI winners driving returns. We stay overweight U.S. stocks and the AI theme. AI-related data center investment could rise by 60-100% annually in coming years, according to a mix of forecasters, including the International Energy Agency. We see the AI theme playing out in three phases. This first AI buildout phase is already producing early winners – including big tech firms, chip producers and companies supplying key inputs like energy, utilities, materials and real estate. Yet, this phase faces challenges, such as whether the power grid can keep pace. We think markets and central banks underappreciate the inflationary impact of this early phase. The next phase could see investment broadening to companies looking to harness AI’s power. The final phase – potential economy-wide AI productivity gains – is highly uncertain. These gains can only come after AI capabilities are fully deployed, a process that could take many years.

Going overweight UK equities

We also lean into risk by going overweight UK equities. We see the Labour Party’s landslide UK election victory increasing the likelihood of a two-term government. The potential for long-term policy implementation should bring relative political stability, in our view. We think perceived stability can help improve sentiment – especially among foreign investors who own more than half of UK shares. We added to our overweight to Japan equities in March due to corporate reforms. Wage gains are filtering into mild inflation and corporate pricing power, reinforcing our optimism on a long-term strategic horizon.

We balance our risk-on view by staying selective in fixed income, focusing on quality. We prefer short-term government bonds and credit that are delivering much higher income than pre-pandemic. We are overweight short-term investment grade credit, given signs that lower-quality pockets are starting to show cracks from higher-for-longer rates. Strategically, we like private credit over public. Private credit defaults remain relatively limited. Private markets are complex, with high risk and volatility, and not suitable for all investors. By region, we like long-dated UK gilts over long-dated U.S. Treasuries strategically.

Bottom line

We see unprecedented transformation unfolding in the real economy. We lean into risk as a result. In stocks, we like the U.S., UK and Japan. We prefer quality income in fixed income – especially in short-term credit – and like private credit.

Market backdrop

U.S. stocks hit a new record high last week, while 10-year Treasury yields fell to around 4.21%, down nearly 50 basis points from their April highs. The U.S. CPI for June came in surprisingly soft, but we think this level of inflation is unsustainably low given ongoing wage pressures. The drop in yields sparked a surge in small cap shares and a brief retreat in tech shares. We think this reflects how markets can become choppy again, even if leaning into risk will be rewarded.

We expect the ECB to hold rates steady this week after their policy meeting. We think the ECB will act on forthcoming data in September but see rates staying higher due to inflationary pressures in the longer term. Overall, this remains an atypical rate-cutting cycle.

Read the full article here