Introduction

Lululemon (NASDAQ:LULU) cannot seem to catch a break in 2024. Let me list six reasons why I think its share price has plummeted:

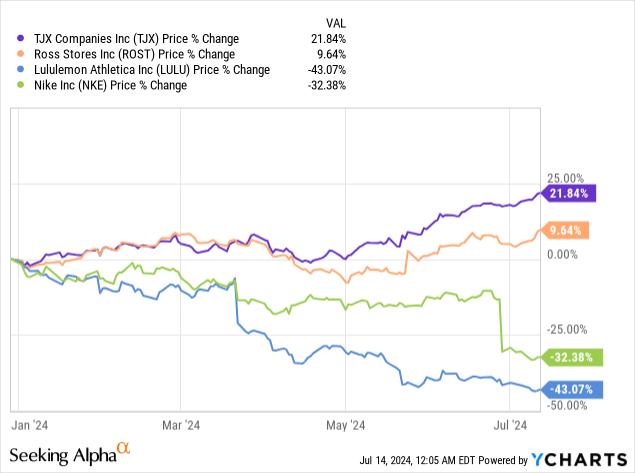

- Shares have fallen by over 40% since the start of the year (they had surged in late 2023 when Lululemon got admitted into the S&P 500) With Lululemon’s share price reaching a new 52-week low, investors have capitulated and run for the hills.

- Chief Product Officer has resigned for a better opportunity, with merchandising missteps in the backdrop.

- It’s a more saturated U.S. market as evidenced by their U.S. market only growing 2% (this means negative growth, after adjusting for inflation).

- Rising competition like Alo and Vuori are nipping at their heels, with comparisons to Under Armour.

- And the worries of a stretched U.S. consumer over persistent inflation which is reflected in a 9-10% growth, when the Street was expecting 12.5%.

- The market is worried whether Lululemon is going out of fashion, as denim and wide bottoms are back in fashion.

My BUY thesis for Lululemon

While investors may be getting a bargain as the stock is relatively cheap compared to its historical multiples, I still find the company trading fairly. While I am a short-term bearish, this premium brand still offers a lot of value to the patient investor, as Lululemon:

- continues to deliver best-in-class returns on capital,

- enjoy long runway of growth in International markets,

- disrupts the sports industry by catering to the female demographic first.

A Justified Reset On Negative U.S. growth

Before going further, we should address the elephant in the room, which is to deep dive into my hypothesis of why Lululemon is down over 40% in 2024.

With not much news to go on, the market is no doubt fretting over the weakness in the U.S. consumer. According to this recent poll, over 56% of respondents feel the U.S. is already in a recession despite recent GDP data still indicating growth, albeit slowing to 1.6%. In short, we are still going through a “vibecession” and it will likely not end until the Fed starts cutting rates. The Fed has already rolled back the prospect of three rate cuts this year, while dangling the possibility of one rate cut before year-end. This reality has endeared the market to discount retailers which are viewed as more “recession-proof”, relative to premium brands like Lululemon or Nike (NKE) which are more sensitive to economic trends.

Add to the above, the saturated athletic apparel market. Alo Yoga in particular doesn’t follow Lululemon’s community-based marketing approach, but has successfully employed a celebrity endorsement strategy by actively courting actresses and celebrities, to generate their buzz and build their hype.

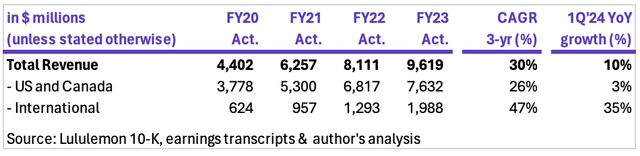

The cumulative impact of the vibe-cession and market saturation has already impacted Lululemon’s growth trajectory. In the June earnings call, sales in the North Americas market only grew 3% year-on-year (a far cry from the breakneck 26% 3-yr CAGR that Lululemon enjoyed between 2020 to 2023. In the U.S., growth was even more abysmal, where growth was up a meagre 2%, which when adjusted for inflation means negative real growth!

Lululemon’s 10-K filings

While management maintains full year 2024 net revenue growth of 11% to 12%, this is largely on the back of continued international expansion of 35%. Also, as U.S. and Canada makes up 80% of overall sales, I think the market is discounting international growth, and wants to take a “wait and see” approach.

A Look at Lululemon’s Valuation

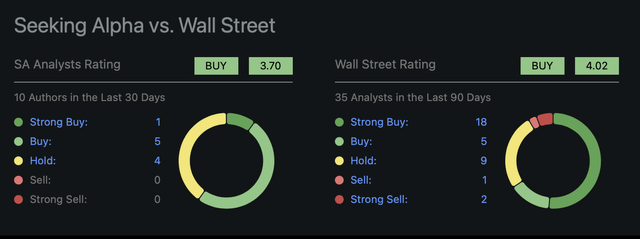

Observing what SA Analysts think of Lululemon, it is apparent that the majority think the bottom is here, as 60% of analysts think it’s a Buy/Strong Buy, while the remaining 40% think it’s a Hold. Wall Street Analysts, on the other hand, are more optimistic, with 50% of analysts calling it a Strong Buy.

Analyst’s community sentiment on Lululemon (Seeking Alpha)

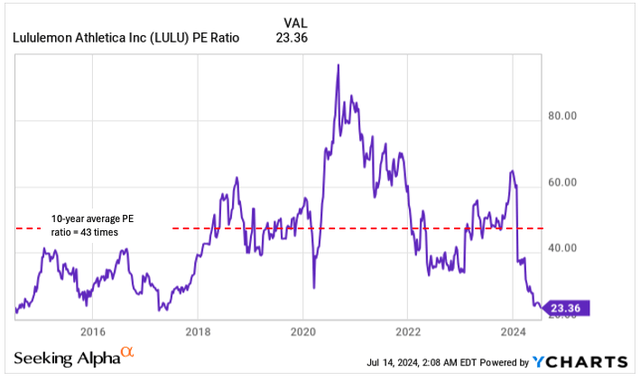

I think the reason analysts are bullish on Lululemon has more to do with its historical multiples rather than its existing fundamentals. The last time it traded at a P/E ratio of 23x was exactly 10 years ago, and when you contrast this with the 10-year average P/E ratio of 43x, Lululemon looks extremely cheap today.

Lululemon ten year P/E multiple (Ycharts)

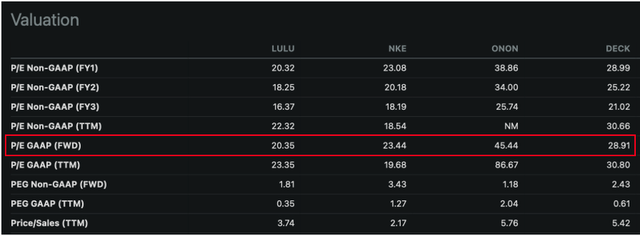

In addition, when comparing the forward P/E multiples of Lululemon, Nike, On Holdings (ONON), and Decker Brands (DECK), Lululemon’s multiples lag even those of Nike. The same Nike which just suffered its worst day in its 40 years trading as a public company.

Valuation multiples against select peers (Seeking Alpha)

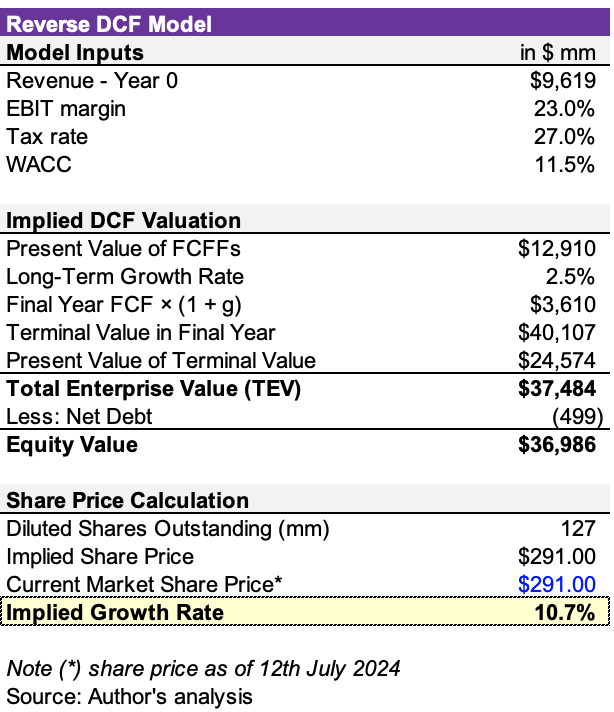

However, the market is forward-looking and sophisticated, and so I performed a reverse DCF calculation to calculate the implied growth rate that the market is expected. Based on my calculations (which I caution readers to be prudent and more on the conservative side), the current share price of $294 per share implies the market is pricing in an implied 5-year growth rate of 10.7%.

Author’s analysis, latest 10-K

The implied revenue growth rate of 10.7% is very close to the current FY24 guidance of 11% – 12%, and could imply that Lululemon is trading in line with the 2024 guidance provided by management. For existing shareholders, the takeaway is that we might only see a re-rating once growth exceeds 11%, which is likely only possible once its U.S. market sales returns to inflation-adjusted growth.

Why Lululemon remains attractive over the long term

I’ve purposely written this article in a contrarian manner to share my hypothesis on why Lululemon has fallen 40% over the past 7 months. Nevertheless, I feel that there remains a lot of value and growth within the Lululemon brand, despite all the bearish sentiments held by the market.

1. Best in Class Return on Capital

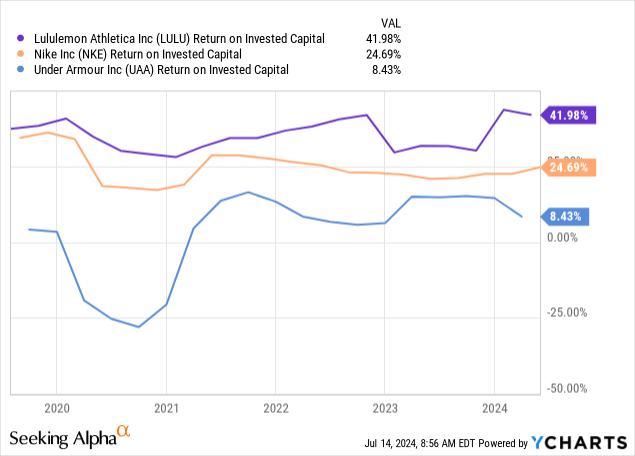

Firstly, Lululemon maintains superior efficiency and profitability, as measured by ROIC. Lululemon’s ROIC of 42%, far exceeds Nike’s ROIC of 25%, and trounces that of Under Armour’s 8%. This is a testament to strong brand, product innovation and quality products that Lululemon has been able to bring to market.

2. Long runway in International, particularly China

For the full year 2023, international was only 21% of our business, and over the long run, I see the potential for it to grow to 50% as we continue to expand our presence outside of North America.

– CEO Calvin McDonald

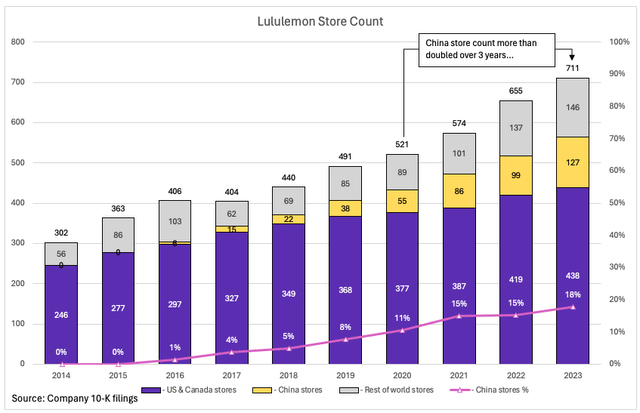

While the market doesn’t hype it much, Lululemon is expanding fast internationally. Over the past three years, China store count has doubled (see the yellow segment in chart below). And from an existing base of 127 stores in China today, CEO Calvin McDonald has been cited as aiming to grow it to 220 stores by 2026, which is almost another doubling.

Lululemon 10-K filings

I believe the continued growth of Lululemon in China to be sustainable, and can be explained below:

1) Post the pandemic lockdowns, the Chinese market is adopting the wellness lifestyle in droves, with many people getting into fitness activities like yoga, tennis and running for the first time.

2) Female empowerment as an ideal is very in-vogue with urban Chinese women who are earning and spending more on themselves. The Lululemon brand fits this ideal, as it embodies female strength and wellbeing.

3) Lululemon formula for success (community-based marketing) in the Americas market resonates even better in Asia. Mega events such as “Summer Sweat Games” are very successful in driving local brand awareness, and Lululemon has mastered social media engagement on platforms like TikTok and Xiaohongshu.

Lululemon’s growth in China is akin to what Nike and Starbucks experienced in China in the 2010s, and serves a large middle-class looking for a premium brand with that magic “IT factor”.

3. Disrupting Sports Categories by Focusing on the Female Athlete First

While Lululemon started with the aim to disrupt the yoga apparel industry, it has since extended far beyond. From a merchandiser of yoga leggings, Lululemon has extended its product range to running, golf, tennis. This diversification strategy capitalises on the existing brand equity, broadens its appeal to a larger audience, and positions it as a comprehensive athletic and lifestyle brand.

And herein lies the biggest revelation I had while pondering on a brand like Lululemon. This company is the first S&P 500 athletic apparel company that caters to women first, before men. When the likes of Nike or Adidas develops a new product, they would concentrate on winning in the men’s category, because men’s as a demographic has historically had the highest engagement in sports activities (i.e. when the average person thinks of a basketball, soccer, or tennis player, they envision a male athlete).

But for a company which derives the majority of its revenues (~64%) from women’s products, Lululemon will always devote its resources towards building out its female range of products. While men are spoiled for choice when it comes to sports apparel and equipment, women may not have enjoyed as many options as men in the past.

Lululemon derives majority of revenue from women’s products (Lululemon 10-K report)

According to a Deloitte press release, they forecast that women’s elite sports will generate over $1 billion in revenue for the first time in 2024. And per this study, advertiser spend for women’s live sports has more than doubled from 2018 to 2022. To conclude, Lululemon’s advantage of building products for women first, is profound, as I expect women will continue to be a growth demographic in the overall athletic apparel industry.

The Risks and Headwinds

The apparel industry is a competitive one, and Lululemon faces intense competition from both established players like Nike, as well as emerging brands like Alo Yoga and Vuori. Make no mistake, if Lululemon cannot continue to innovate on product or marketing, it will see its pricing, branding and market share get diluted.

In addition, while Lululemon is an athletic apparel brand, it is subject to the fashion whims. It is worth noting that wide-legged pants has been in trend for a few seasons now, and denim is also officially back. Should it prove true that customers are sufficiently stocked on leggings, and are more interested in buying wide-legged pants and jeans, investors could see Lululemon sales further impacted.

Lastly, the fate of Lululemon in 2024 ultimately hinges on the strength of the U.S. consumer and indirectly the unemployment numbers. A sudden deterioration in U.S. unemployment could lead to a general pullback in consumer spend, which will no doubt affect Lululemon’s sales in its U.S. market. However, per Goldman Sach’s economics research, this is not in their base case, as they expect the labor market to continue to drive income growth and spending.

Final Thoughts

Investors have to come to terms with the new reality that Lululemon is now competing in crowded waters, and further innovation is needed to both defend market share and bring growth back to the high teens.

While I believe that Lululemon is currently trading fairly given its outlook, its superb brand, loyal customer base, best in class margins, global growth runway, and expanding product lineup for women makes it a compelling long-term investment. Hence, I maintain a BUY rating on it.

Read the full article here