The last time I published an article on PDD Holdings (NASDAQ:PDD) was in February of this year. Back then, I argued that investors should be cautious with PDD as the company faced multiple short-term headwinds. However, in the long term, PDD’s moat is still intact. Since then, PDD’s stock has been essentially flat, even after another blow-out quarter. It appears to me that while some existing concerns have been exacerbated, new concerns have also emerged. I think investors are overwhelmingly focused on the short-term headwinds, thus under-appreciating PDD’s long-term potentials. Therefore, I am maintaining my “buy” rating for PDD.

Accounting concerns

I believe the quality of PDD’s earnings has become the biggest short-term concern for PDD’s stock. For instance, in this article, the author wrote that during PDD’s Q1 earnings call, an analyst asked about how PDD achieved profitability growth despite intensified domestic competition. PDD’s management did not give a direct answer. However, the answer lies in PDD’s financial statements. Specifically, PDD benefited from impressive operating leverage as sales and marketing expense only accounted for 27% of revenue, compared to 43.2% of Q1 of FY2023. R&D expense accounted for 3.4% of revenue, compared to 6.7% of revenue of Q1 of FY2023. Operating leverage resulted in an increase of PDD’s non-GAAP net margin to 35.3%, from 26.9% in Q1 of FY2023.

Another concern is related to PDD’s interests and investment income. PDD reported interests and investment income of RMB50.5 billion, which increased 245% from RMB14.6 billon in Q1 of FY2023. However, total cash and short-term investments only increased 49.5% from Q1 of FY2023. I think this concern is legitimate. The most plausible explanation I can think of is that PDD has increased its short-term investments overseas, where interest rates are much higher than China. I have not verified whether this is the case, and the company did not provide any information on the disconnect between the increase in interests and investment income and the increase in investment assets.

Intensifying competition

The other big concern with PDD is the price war in China’s e-commerce market. Both Alibaba (BABA) and JD.com (JD) stepped up their efforts in trying to contain PDD’s growth. Their efforts are showing some short-term results. For instance, it was reported by WSJ that the gap between PDD’s growth rate and Alibaba’s growth rate has narrowed as “analysis estimated that PDD’s GMV rose 18% on the year during the 618 event, outperforming estimated growth of 12% at Alibaba’s major platforms”. The acceleration of Alibaba’s GMV growth is undeniable, as Alibaba also reported “double-digit year-over-year growth in GMV” for its Taobao and Tmall Group during its Q4 FY2023 earnings call.

However, Alibaba’s GMV growth is achieved with tremendous pressure on its margins. The adjusted EBITA margin for the Taobao and Tmall group has declined even though GMV growth accelerated. It remains to be seen whether Alibaba’s management can continue to handle investor’s pressure to balance its margin and GMV growth. In the short term, I expect the price war to continue.

Political and regulatory concerns

I have written about the escalated political scrutiny PDD’s Temu has faced in the U.S. There are plenty of reports covering the U.S. government ban on TikTok’s U.S. business. Therefore, I will not delve into this issue here. I believe there’s another political concern, which for some reason has been less-talked-about by many investors, but may have a real impact on PDD’s valuation level for a while. This concern is manifested by the introduction of four bills put together by Congresswoman Victoria Spartz and Congressman Brad Sherman in March, “to mitigate the strategic, commercial, and national security threats posed by China to the American economy and financial markets.”

Of the four bills, the following two will absolutely negatively PDD’s valuation if passed.

No Capital Gains Allowance for American Adversaries Act: This bill would eliminate the capital gains tax break for investments in companies based in China, Russia, Belarus, Iran, and North Korea. It also eliminates a related tax break, the “step-up in basis” at death, for investments in such companies. The SEC will require disclosure that no tax breaks are available for these stocks.

No China in Index Funds Act: Index mutual funds minimize their expenses by simply investing in all the companies in a certain market sector, without looking closely at the individual companies. There are unique difficulties in evaluating the risks of investing in Chinese companies. Americans should not invest in these companies without carefully evaluating the risk. This bill will keep these hard-to-evaluate Chinese stocks out of index mutual funds.

The exclusion of Chinese companies from index fund is obviously a big negative for all Chinese ADRs. However, the impact of the elimination of the capital gains tax break may require some explanation. Under the current system, some institutional investors, such as endowments and foundations, are exempt from capital gains on their investments, including their gains on Chinese ADRs. U.S. institutional investors have very little capital gains on Chinese ADRs, as Chinese ADRs have been one of the worst performing asset classes in the past three years. However, PDD has been the rare exception to the Chinese ADRs that has generated capital gain for tax-exempt institutional investors. Therefore, if the bill is passed in the future, these tax-exempt institutional investors are extremely likely to tell their G.P to dump their PDD stock before the effective date. Some institutional investors might already have done so.

PDD’s long-term moats remain intact

As I wrote in my initial investment thesis, PDD’s long term competitive advantages include its focus on “white label” products, its differentiated merchant ecosystem, its superior algorithm and a much more efficient operating structure. Even though PDD has faced the above headwinds, the aforementioned competitive advantages still hold for PDD. This is evidenced by PDD’s continuous margin improvement driven by PDD’s impressive operating leverage as a result of higher monetization rate and superior operating efficiency.

Financial projections and valuation

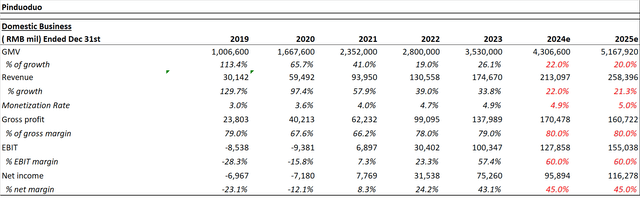

In terms of financial projections, I have updated my model to incorporate the latest quarterly results. I have underestimated PDD’s monetization rate and operating margin in my previous model. In the current model, I am assuming PDD can maintain the current monetization rate and operating margin for FY2024 and FY2025.

author’s estimate

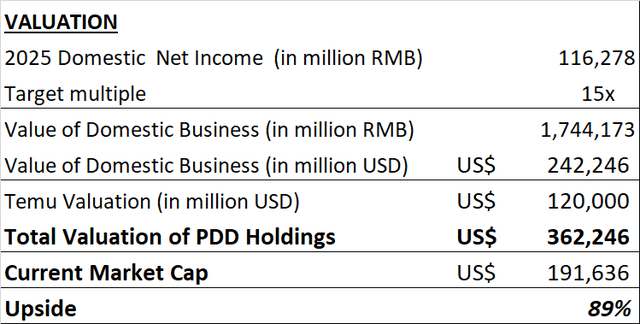

As far as valuation is concerned, I’m applying the same multiple of 15 times 2025 net income for the domestic business. For Temu, to be conservative, I used the same valuation of the Temu business even though Temu’s growth rate has been much faster than I expected.

author’s estimate

Based on my financial projections, PDD has an upside of almost 90% in less than two years.

Conclusion

PDD has faced multiple headwinds both domestically and in the U.S. These headwinds may continue to put pressure on PDD’s valuation level. However, I still believe over the long term, PDD’s competitive advantages will hold. Therefore, I continue to give PDD Holdings a “buy” rating.

Read the full article here