Co-authored by Treading Softly

The concept of being a “black sheep” has been around for centuries. Originally, some ministers in England believed that if a sheep was born with black fleece, it was a mark that the devil had been involved in its creation. Scientists later determined that black sheep are affected by a recessive gene that causes their fleece to gain the color. The typically dominant gene causes colors to be suppressed, and therefore, the fleece grows to be black. Based on genetics, about one in four sheep are predestined to be born with black wool. Interestingly, the concept of evil being tied to the black sheep has slowly changed and morphed through society, causing a black sheep to be considered an outcast in the situation despite it being similar in every way except its color. As a result, it is immediately unliked by the rest of the group or by the observer.

When it comes to the market, investors have very clear expectations about what different sectors do at different times. If a company within that sector moves in a different direction than the rest, it is immediately labeled as being a black sheep. For example, within the real estate sector, REITs are expected to struggle when rates are high but thrive when rates are low. This is because they’re viewed as bond-like or bond-adjacent investments. So, when interest rates climb, they sell off; when interest rates fall, they benefit. If a REIT were to move in the opposite direction of the rest of the group, in any of those circumstances, it would be given a wary eye and likely avoided by investors who simply want to see the sector move uniformly as expected.

Today, I want to examine a company that is moving opposite to expectations within the sector, which is causing many investors to view it sentimentally instead of fundamentally. We eschew this approach when we use our Income Method. We look at things at a fundamental level to make our investment decisions.

Let’s dive in!

The Black Sheep of BDCs

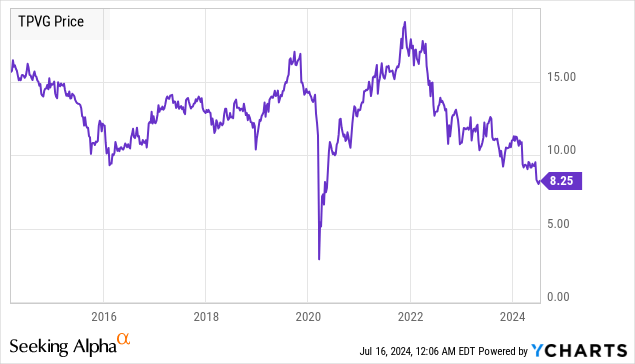

TriplePoint Venture Growth (NYSE:TPVG), yielding 19.4%, is a BDC (Business Development Company) that specializes in the “venture capital” niche. While we are seeing many BDCs trading at high valuations, TPVG has gone the other way. Once a BDC you would pay a substantial premium for, TPVG is now trading at a discount to its last reported NAV (Net Asset Value). As a result, its yield is nearly 20%, people are bearish, there are calls for dividend cuts, and the world is coming to an end.

In a market where most BDCs are trading near their all-time highs, a BDC that is trading at its all-time low is either a huge bargain or a disaster. There isn’t much in-between.

When TPVG crashed this much in 2016, it was a bargain, and from 2016 to 2019 it went on to have a full recovery. The current downswing has been longer and steeper. In both cases, the decline was driven by declining NAV caused by credit losses.

Over the past year, TPVG has realized the largest credit losses it has ever seen. Borrowers defaulted on their loans, and TPVG had recoveries that were certainly lower than they had hoped.

Credit losses tend to be lumpy. Everything is fine until it isn’t. In the case of TPVG, with their focus on venture-stage businesses, they tend to be investing in companies that are not necessarily cash flow positive. Businesses preparing for an IPO are usually rewarded for growth and momentum. As the IPO market deteriorated, Venture Capitalists had to make decisions to keep supporting companies or to pull the plug and cut their losses. The companies had to reorient themselves from pushing for growth no matter what, to being cash flow positive. That’s a transition some companies succeeded at better than others. The result for TPVG was some borrowers going to bankruptcy and realized losses that impacted their NAV and share price.

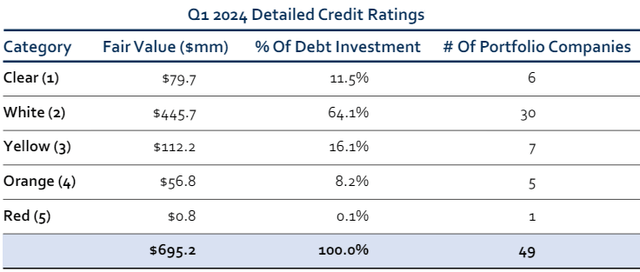

The essential question for investors today is whether this wave of credit losses is coming to an end, or whether there is more to be revealed. TPVG’s internal credit ratings show approximately 8.3% of its portfolio was in the lowest “orange” or “red” categories. Source

TPVG Q1 2024 Presentation

Management discussed the companies on this watch list in the Q1 earnings call. Co-founder and CEO James Labe noted that one of the companies in the orange category, TFG Holdings, was acquired in Q2 and will be removed from the watch list. So with that removal, the orange category will be closer to 5.6% of the portfolio. Management also indicated that they expected some of the investments in the Yellow category to be upgraded as they were in the process of raising capital and would be upgraded when those efforts are successful.

The credit risk appears to be stabilizing. The next question is whether the dividend is safe.

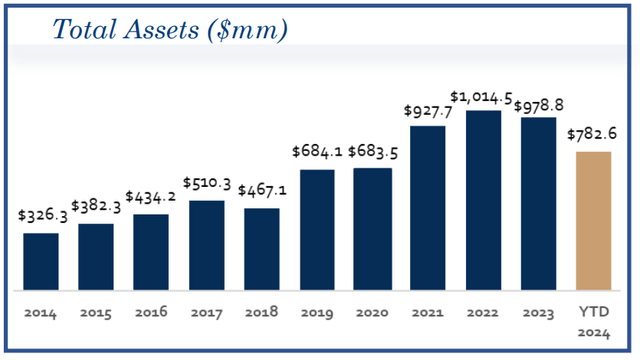

In Q1, TPVG’s NII (Net Investment Income) was $0.41, still covering its $0.40 dividend, but not a lot of extra room. NII has declined because TPVG has fewer assets. Fewer loans paying interest directly lead to lower NII. Assets declined about $196 million from 2023 to 2024.

TPVG Q1 2024 Presentation

Credit losses played a role, but TPVG also received $135 million in prepayments while only funding $82 million in new loans in the past four quarters. Dealing with credit issues, TPVG pulled in its horns. TPVG management guided for funding to increase this year, remaining in a range of $25-$50 million/quarter but trending toward the high end in the second half. This is a level they believe they can maintain while remaining within their leverage target.

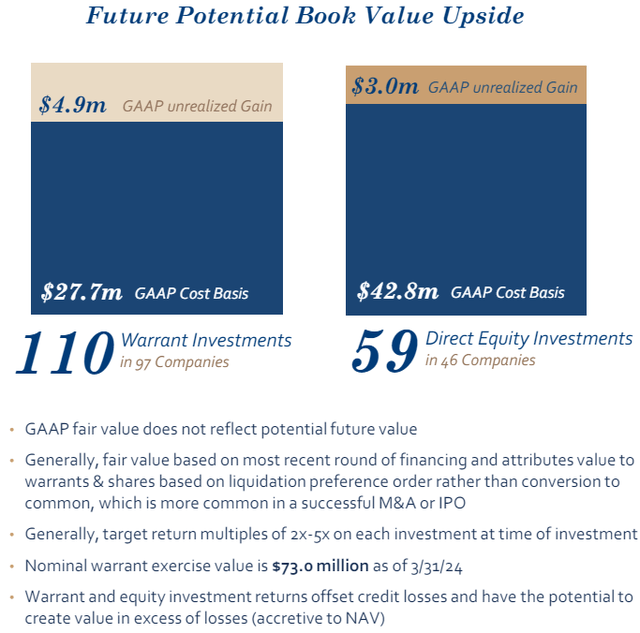

Rebuilding NAV will be a longer-term task. And is not likely to meaningfully occur in 2024. TPVG knows it is investing in a riskier portion of the market, so to offset that risk, it takes warrant and equity positions in the companies it lends to.

TPVG Q1 2024 Presentation

The returns from these equity positions can range anywhere from nothing to a lot. When a company that borrows from TPVG is acquired or IPOs, TPVG gets the opportunity to monetize these investments. Since GAAP accounting is limited in the ability to write up the value of non-traded equity investments, the gains add directly to NAV. This is how TPVG increased its NAV from 2016 through 2019.

The times when credit issues are high are the opposite of the times when equity is most likely to be monetized for large gains. When the cycle turns, these holdings will be what drives TPVG’s NAV in a positive direction.

The bottom line is that we believe that the wave of defaults is likely near the end. TPVG weathered a storm and the damage is now generally known. Now in the trough, it is time to rebuild, a process that will certainly take time. Is the dividend “safe”? Let’s put it in perspective – most BDCs are paying out the highest dividends they have ever paid. That isn’t going to last forever. It is a very safe bet that most BDCs are going to pay out less in 3 years than they are paying out today. The “supplemental” dividends that most BDCs are paying out aren’t sustainable. That’s why the management teams are calling them “supplements”. They are the result of the extremely positive impact that rising rates have had on companies that generally own floating-rate debt and have fixed-rate debt of their own that they don’t have to refinance for a few years. Either the floating rate will come down, and revenue will shrink, or rates will stay high, and BDCs will have to refinance at higher rates, and their cost of debt will go up. Either way, the dividends that all BDCs are paying should be seen through the lens that earnings are mainly thanks to temporary conditions. Many of those supplements will go away.

TPVG didn’t do a supplement. Instead, it opted to hike its “regular” dividend to $0.40 in 2023. An 11% increase from the $0.36/quarter it paid for nine years. Is it “the end of the world” if TPVG decides to go back to its historical $0.36/quarter because that is more sustainable? When it was “only” paying $0.36/quarter, TPVG reached a peak price of nearly $19/share.

I love dividends as much as the next guy. Some accuse me of liking them too much. Yet, there is a fundamental truth of all RICs (Regulated Investment Companies), they are required by law to distribute substantially all of their taxable income or pay an excise tax. This includes BDCs, property REITs, mortgage REITs, and Closed-end funds. As a result, when they have a particularly great period for earnings, they have to raise their dividends. That great period doesn’t last forever (as no great period ever does). So when earnings decline, it is usually prudent to trim back the distribution.

It strikes me as a bit odd that some of the same people who gleefully bought at $14-$15 to collect $0.36/quarter in dividends worry when they consider paying $8-$9 to collect $0.40/quarter. Suddenly, there is a concern that the dividend might be cut at some unknown point in the future to $0.36/quarter.

When it comes to an investment like TPVG, the question we need to ask is whether it is a well-managed company that ran into a rough spot and is now an absolute bargain, or whether management made material and unforgivable errors and can no longer be trusted. My view is the former, and I’m happy to be a buyer at these prices.

Conclusion

With TPVG, we can see a black sheep in the BDC sector because, unlike its peers, it benefits when rates fall. This difference causes many investors to incorrectly assume the company is an utter failure because its sector is thriving with higher rates, but it isn’t.

If you’re an income investor, you’re already a black sheep in the market compared to the many others who invest in passive market-wide ETFs or focus on trading for capital gains alone. You know what it means to be misunderstood and maligned by those who are well-meaning but completely misinformed. I appreciate Seeking Alpha for creating an environment where all investing methods can be seen, heard, and supported as routes to achieve our individual goals within the market.

When it comes to your retirement, you need to follow the methods that help you achieve your goals. You don’t want to be thrown off course by every swing in sentiment or every fad that blows through the market. I’ve been investing long enough to have seen many fads come and go, with everyone thinking you’re crazy not to get in on this “new thing”. Finances have never changed. You need cash to pay your bills. You need cash to buy groceries. You need cash coming in from somewhere. I look at trillions of dollars flowing through the markets and tap into that as the source of my income — one black sheep at a time. That’s the beauty of my Income Method. That’s the beauty of income investing.

Read the full article here